Continuing on from doing nothing, I’ve changed the chart.

505p is the price if u had re-invested the dividends elsewhere

722p is the equivalent price if u re-invested the dividends back into SCF without the benefit of hindsight.

The price spends as much time falling as rising, so sitting and sticking to your plan is all that matters, belt and braces, just in case u buy at the wrong time.

NESF might not be everyone’s cup of tea but at the end of the day when all’s said and done, is it tidy?

Thanks for reading The Oak Bloke’s Substack.

It’s another FTSE250 company. The OB has covered far too many of these large caps recently; he’s in danger of needing a revised disclaimer and garnering a new reputation if this non-nano cap nonense carries on.

But I promised articles around renewables over several articles, so I picked out what I saw as my faves. This is my final fave.

My favouriting is that I picked out all the high yielders and those with the juiciest discounts and what I see as deep value. Those with a “meh” discount and/or “meh” yield I’ve overlooked and perhaps will come back to…. perhaps you, reader, can point out any that are obvious value and overlooked. I did look over several and I wanted to like JLEN with its fragrant bio-methane holdings. Besides just think of the dad joke OB titles I could use. For example: I’m just JLEN from the block, used to NAV a little – now I NAV a lot…..

But I didn’t think JLEN was very good value, so that article is on hold.

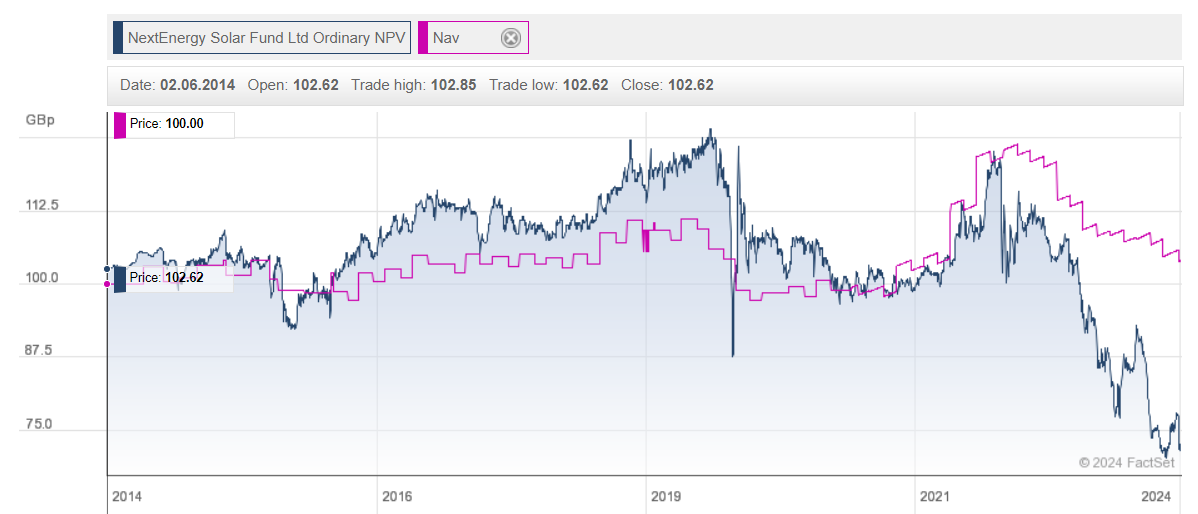

Next Energy Solar

NESF is a large solar investment trust. After years of trading at a premium to NAV, both its NAV and share price have fallen away, albeit its NAV has reverted to 2021 levels – do we see a clue there that “noise” both increased then decreased the assets. Let’s investigate that.

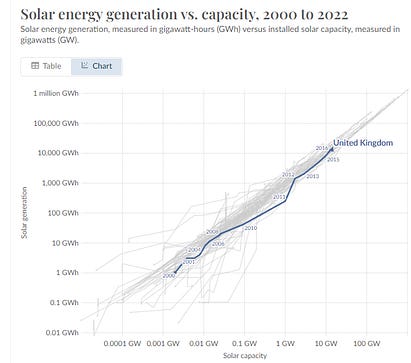

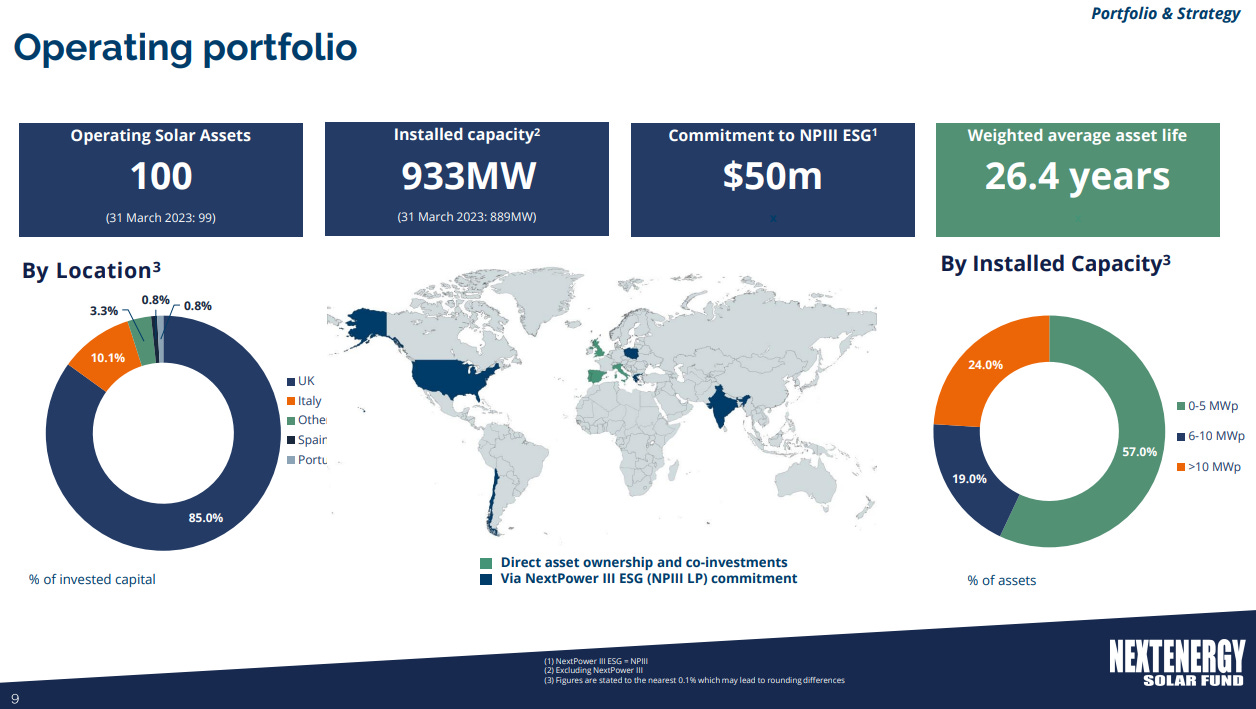

NESF has a large UK footprint, with 10% Italy, and 5% RoW. Its assets are long life, and 933MW capacity and 599GWh generated in 2023 tells us that the energy yield was 7.3% of capacity, while in 2022 the energy yield was 9.1% (599000/(933*365*24)).

The 2022 yield is spot on to the average based on our world in data (you can click on the chart below). It reveals that capacity and generation are fairly consistent between countries. I had wrongly assumed that yield for the UK was lower than say Italy or the Sahara Desert, but the data doesn’t show that. So 85% of solar being in the UK isn’t the disadvantage I’d first imagined it would be. At least not using today’s technology.

The UK yield vs every other country in the world – as you generate more power (horizontal line) you generate more power (vertical line) – there’s not much variance between the equator and the north pole

The answer to this apparent riddle/contradiction is a lower temperature offsets lower irradiance. While more irradiance means more power, more heat shortens the life of equipment and reduces the efficiency of solar too. That factoid has gobsmacked me.

NESF appears to have an impressive portfolio of assets, with low costs of debt (2/3 fixed and 1/3 floating but on very advantageous rates and with 10+ years repayment structures), while revenue has a degree of protection from price fluctuations through hedging, ROC (renewable obligation certificates) and subsidy. As at 31/3/23 NESF had agreed fixed UK pricing (hedged) covering 88% of budgeted generation for the 2023/24 financial year, 44% of budgeted generation for the 2024/25 financial year and 13% for the 2025/26 financial year.

Income in the September 2023 interim covers dividends 1.8X.

The forward yield is a very impressive 11.8%. (based on a 8.43p per share dividend)

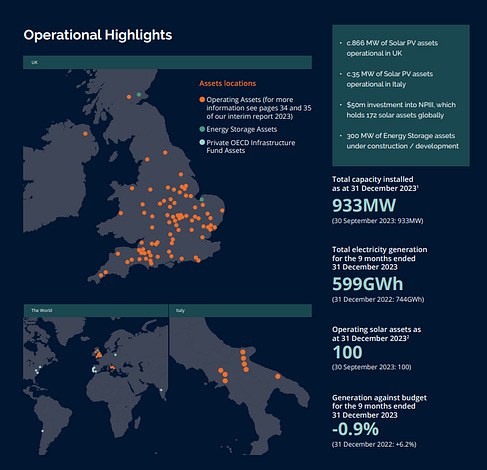

Eagle-eyed readers will spot energy storage assets in the above map, and this is a growth area for NESF. These enable NESF to capitalise on existing infrastructure including existing grid connections and inverters, meaning OPEX is optimised, but also that solar generation can be sold at optimal times (i.e. early evening). The idea being that the 92 UK sites could be retrofitted over time with energy storage. Currently 1 site is nearly live, 1 has planning, and 4 applications are in progress.

Interestingly, the power price forecasts include a “solar capture” discount, which reflects the discount on pricing in daylight hours versus during baseload hours. With the introduction of storage such a discount disappears – so a positive reversion for the NAV that not only do you add the asset to the NAV but you also remove the solar capture discount too.

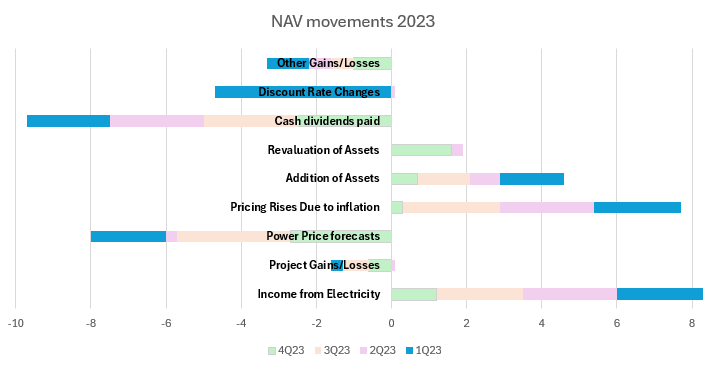

Forecast Prices & Discount Rates

NESF reveals substantial drops due to discount rates increasing to 8% and short term power prices falling also.

When you strip out that “noise” and focus on the real movements roughly inflation protections offsets power price forecast changes, income nearly covers dividends (and in the 25% higher irradiance in 2022 would have fully covered the dividend), while asset capital gains offset project losses and other losses.

The net NAV fall is the 5p/share discount rate change.

Looking forward it appears that Power Price forecasts will eventually return to a positive, as will the discount rate. It wasn’t clear to me that the forecasts are considering the subsidies, the ROCs and hedges that NESF employ. Much of current year is hedged and one and two years ahead also.

4Q24 (1st Jan 2024 to 31st March 2024) meanwhile, shows a further power price forecast decline only slightly offset by positive pricing inflation changes. Going forwards income should rise due to rising capacity which in the 4Q24 update a week or so ago surpassed 1GW.

So future NAV should revert and there’s even scope for some NAV growth, although the large dividend swallows up most of the income so this is predominantly an income stock.

Conclusion

The dividend looks far safer than one might suppose looking at the discount to NAV and recent share price falls. This share actually looks fairly boring and safe, underneath its racy yield and apparent losses through temporary factors which wax and wane. It was a fairly complicated share to understand and compared to SEIT and HEIT the reporting felt inferior. I found much less hidden value compared to the others, also.

Just the obvious value.

That long term the idea that power prices are going to be anything other than upwards based on growing demand and challenges with supply is ignoring the laws of physics. So falling forecasts will revert eventually.

That short term, those power price forecasts might even revert later this year. Today it was announced that El Nino has ended and La Nina has begun. This suggests a colder winter for Europe in 2024. That combined with complacency and our new government knifing Oil & Gas in a populist tax grab, isn’t going to help keep the lights on.

The one area of hidden value is its strategy of adding storage to existing grid connections which is a genius move. Without a connection there is a 5 year average wait for such connections – where those with existing connections have, err, the power. Boom boom.

John D Rockefeller would have liked the UK stock market Story by Simon English

The richest man in history was probably John D Rockefeller, founder of Standard Oil, later broken up into seven smaller companies, one of which is now Exxon Mobil.

At his death, he was worth $700 billion in today’s money.

Elon Musk or Jeff Bezos might top him, but neither plans to die so we may never get a final score.

Both have vainglorious plans for the future – Musk intends to save humanity from itself, Bezos just himself, it seems.

Rockefeller might have been less fun than today’s tycoons. Certainly by the end he was bored, and heard to say: “Do you know the only thing that gives me pleasure? It’s to see my dividends coming in.”

Rockefeller bought shares that paid dividends and sold the losers to offset capital gains tax. It worked.

That plan, enacted in the UK lately, might even have made Rockefeller break a smile. In the three months to March, London listed shares paid out £12 billion in hard cash to investors, the best for several years, and not bad for a period when the stock market itself was in the doldrums.

Elsewhere in Europe, dividend payments fell.

The flip side of big companies being cautious is that they have had cash they have rightly returned to investors in the form of higher divis and share buy backs

You don’t have to be an investor solely looking for income to find, as Rockefeller did, something awfully reassuring about the clunk of cash from shares into your bank account.

Now the market for flotations seems to be improving, finally, perhaps we can stop worrying about London’s status as a global financial centre.

Even when the stock market was gloomy, most of the rest of the City functioned fine, and the dividend payouts were a symbol of the inherent sturdiness of most of our big firms.

As someone once said about America, there is nothing much wrong with the City that can’t be fixed by what is right with it.

Don’t miss out on the possible resurgence of the domestic market, experts warn.

By Matteo Anelli

Senior reporter, Trustnet.

Momentum is gathering for UK stocks, which surged through record highs last month, and the upcoming elections are drawing even more attention to the domestic market.

Indeed the FTSE 100 peaked at 8,445.8 in May, almost 600 points ahead of its pre-Covid levels, although it remains some way below the likes of the US’ S&P 500 index (11.2% return year-to-date), with the UK large-cap index up 9% in 2024 so far.

Whether this resurgence will be enough for investors to reconsider their preference for global investments and return to the unloved UK market remains to be seen, but experts are becoming more vocal about the opportunities cropping up domestically.

Trustnet has recently asked whether it’s time for a patriotic punt on the UK stock market and many commentators pointed out the favourable entry point due to cheap valuations, increased international merger and acquisition (M&A) activity, improvement in economic data, imminent rate cuts and “voracious” share buybacks.

On top of that, many UK stocks have surged past most of the magnificent seven, with very few people noticing.

Hal Cook, senior investment analyst at Hargreaves Lansdown, said there is a lot to like about the UK stock market.

“With mature industries such as banks, oil and gas and tobacco, the UK has been known as a good place to look for dividend income, but there are plenty of growth opportunities too – from big consumer goods companies selling their products globally to smaller businesses looking to grow into the giants of tomorrow,” he said.

“We think this combination and the discount on offer compared to other regions make the UK an attractive place to invest right now.”

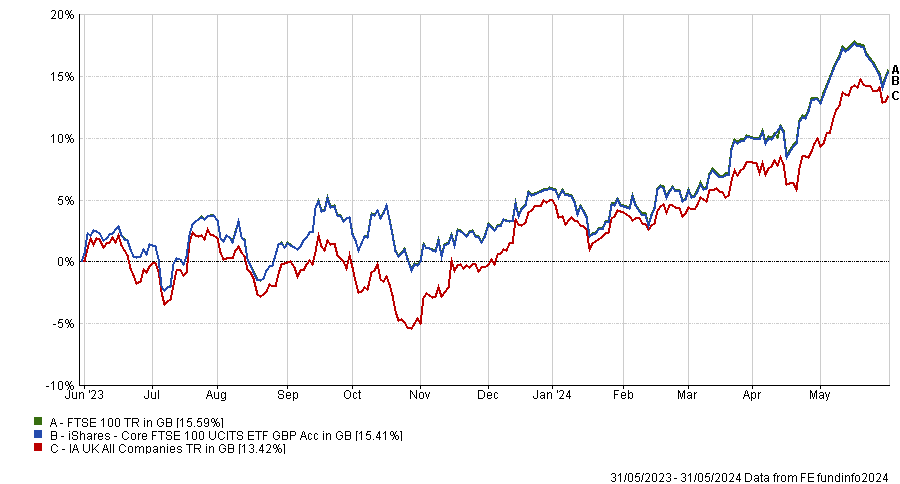

The main way – and the cheapest – to invest in the UK are exchange-traded funds (ETFs), according to Cook, whose preference was for two iShares and one Vanguard solutions.

For investors who want to get exposure to the largest UK companies, he recommended the iShares Core FTSE 100 ETF, which tracks the performance of the FTSE 100 index.

Performance of fund against sector and index over 1yr Source: FE Analytics

“It does this by investing in every company and in proportion with each company’s index weight. This is known as full replication, which can help the ETF track the index closely,” he said.

The £2.2bn fund is passively managed by Blackrock, has achieved an FE fundinfo passive fund Crown-rating of five, and only charges 0.07%.

ETFs also offer access to income-paying stocks and Cook’s pick was iShares UK Dividend ETF, a low-cost option for tracking the performance of the FTSE Dividend UK+ index with a price tag of just 0.40%.

Performance of fund against sector and index over 1yr Source: FE Analytics

This £848m vehicle offers exposure to 50 of the highest dividend-paying stocks listed in the UK, while still making sure it’s diversified across multiple sectors. The trailing 12-month yield is currently 5.45%.

Finally, medium-sized companies enthusiasts should consider the Vanguard FTSE 250 ETF, which aims to track the performance of medium-sized companies in the UK as measured by the FTSE 250 index.

Performance of fund against sector and index over 1yr Source: FE Analytics

FE Investments analysts highlighted this fund for its simple method of replicating the performance of the index by direct ownership of all the underlying securities as well as its usage of stock lending, a practice by which a select third party borrows a limited amount of the passive fund’s holdings in exchange for a fee.

This supplements fund returns and compensates for the trading costs involved with direct ownership of the securities.

Among the investment management houses, Hawksmoor has been betting big on a UK recovery. Chief investment officer Ben Conway said that a FTSE 250 tracker would be a good option to capture a broad spectrum of opportunities in the mid-cap space, but fans of active management can also consider Aberforth Smaller Companies and Odyssean.

Not everything will be smooth sailing for the UK, however, and work remains to be done in a number of areas. The finance industry has been advocating for a number of changes to get Britain back on track.

A Dividend Hero Trust where to GRS, u just need to re-invest the dividends, whilst in the Accumulation stage and then switch into a higher yielder before u start De-accumulation.

A belt and braces strategy would be to pair trade the Trust with a higher yielder and hold thru thick and thin. When markets are weak your dividends will be buying u more Trusts at a higher yield. A strategy to GRS in great markets but even a better strategy in falling markets.

nordvpn special coupon code 2024 350fairfax.org stantonharmon@sfr.fr

Hello there! Do you know if they make any plugins to safeguard against hackers? I’m kinda paranoid about losing everything I’ve worked hard on. Any tips? Here is my homepage; nordvpn special coupon code 2024

£££££££££££

Sorry, can’t help, unless anyone else can answer the question.

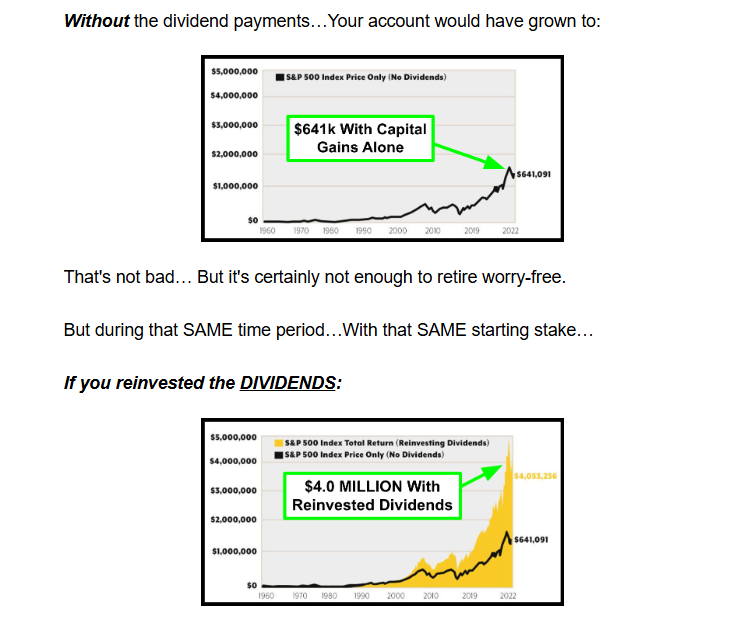

Dividend stocks are possibly the only investment where you have the opportunity for capital growth as well as income.

It’s truly empowering once you see the impact that dividend stocks can make on any account size.

Imagine the peace of mind that could give you, knowing that your nest egg could be growing without having to make massive annual contributions.

Or slaving away at the computer screens trying to pick some miracle stock.

The key ingredient is DIVIDENDS.

And when you look at it over the scope of time, the difference dividends make is truly mind boggling.

Just visualize a $10k investment in the S&P 500 since 1960 with me.

That means dividends were the ONLY difference between not having enough to make it through retirement.

Or retiring in the TOP 1% of all U.S. Households!

And the best part is, there’s no extra legwork on your end to collect these dividends – just sit back and watch.

As long as a company doesn’t cut its dividend, you’re guaranteed cash!

££££££££££££

Sadly I will not be able to show you how to become a multi-millionaire but I can post some building blocks for a better retirement by earning passive income every day, even when markets are closed, of £25 a day gently increasing as dividends are re-invested.

Aberforth Split Level Income Trust ex-dividend payment date Abrdn European Logistics Income PLC ex-dividend payment date Balanced Commercial Property Trust Ltd ex-dividend payment date BlackRock Sustainable American Income Trust PLC ex-dividend payment date Capital Gearing Trust PLC ex-dividend payment date Downing Strategic Micro-Cap Investment Trust PLC ex-dividend payment date Edinburgh Investment Trust PLC ex-dividend payment date Henderson European Focus Trust PLC ex-dividend payment date JLEN Environmental Assets Group Ltd ex-dividend payment date Riverstone Credit Opportunities Income PLC ex-dividend payment date Utilico Emerging Markets Trust PLC ex-dividend payment date VH Global Sustainable Energy Opportunities PLC ex-dividend payment date

Some observations, I believe they are now called bullet points.

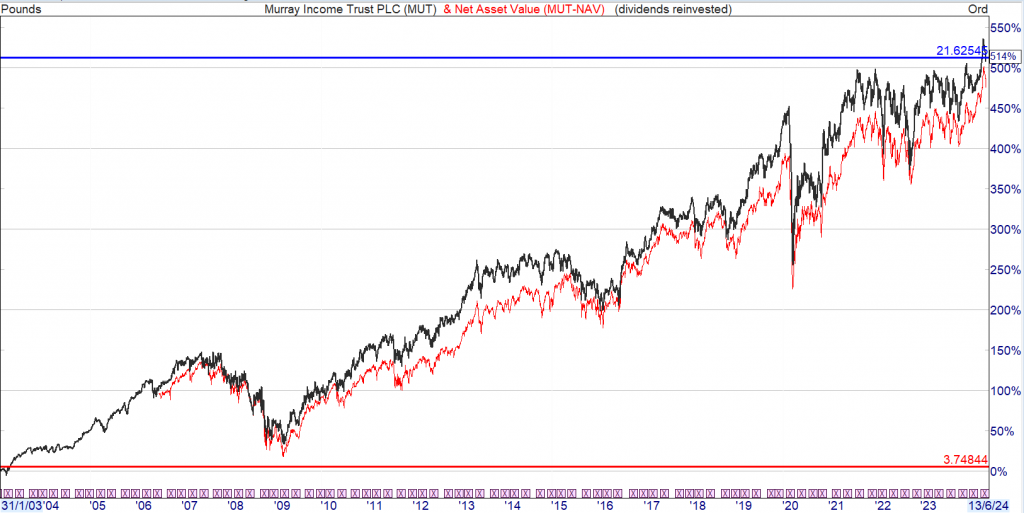

MUT pays a ‘safe’ modest dividend. From 2003 thru 2009 if u were a long term holder u hadn’t made a bean. Although there was an opportunity to book some profit and to re-invest lower down. Even without the dividends the Trust has provided enough capital to re-invest in a higher yielder.

With the dividends simply re-invested, remembering it only pays a modest dividend. No skill required apart from being a bump on a log.