The Third Interim Dividend of 2.20 pence per Ordinary Share (August 2023: 2.10 pence per Ordinary Share) will be payable to Shareholders on the register as at 30 August 2024, with an associated ex-dividend date of 29 August 2024 and a payment date on or around 30 September 2024.

Dividend Guidance Reaffirmed

The Board is pleased to reaffirm its guidance of a full year dividend of not less than 8.80 pence per Ordinary Share for the financial year ended 30 June 2024 (2023: 8.60 pence). This is expected to be covered by earnings and to be post-debt amortisation.

If it’s nearing the time to start to spend some of hard your earned profits, de-accumulation.

Some Trusts to consider.

MRCH, CTY dividend heroes. A safe dividend as u can get in the market with the chance of capital gains.

AGR, PHP secure dividends, until they aren’t.

SMIF, SDIP pay a monthly dividend. SDIP the more risky but a higher yield, SMIF total yield depends on any surplus paid as a final dividend.

10K invested in

SMIF a monthly dividend of £56 plus the final undetermined dividend

SDIP a variable monthly dividend of £68

It’s likely u may lose some capital with all of the above Trusts at some stage of your holding but as long as the dividends are paid, u have no intention to sell, the value matters very little.

The income target for 2024 is 9k, which will be beat.

If we use the figure of 9.5k, re-invested at 7% compound growth this would equate to a ‘pension’ of 19k in ten years time. Much better if u have longer in your accumulation stage.

An option would be use the funds to buy an annuity currently around 7% per annum. The figure in ten years time is the unknown, it could be higher or it could be the same as 2022

Canada Life figures show the 65-year-old with a £100,000 pension pot could buy an annuity linked to the retail price index (RPI) that would generate a starting annual income of £3,896. That’s up from £2,195 in the New Year following a 77% spike in rates this year.

That’s a huge gamble on the income for the rest of your life.

I forget to mention if u buy an annuity u have to donate all of your hard earned but with a dividend de-accumulation plan u keep all your capital.

The amount of capital will be substantial as u re-invest your dividends but the actual figure is of no interest as u never intend to sell any of your Trusts unless in an unseen emergency.

As u approach your de-accumulation stage u might want to invest some of your earned dividends in Government Gilts if u want to withdraw a specific sum on a specific date. It’s your hard earned and there are no pockets in shrouds.

No 30%+ or 20%+ monthly gainers to report this week – the top performer on Winterflood’s list of highest monthly movers could ‘only’ manage a 13.5% gain. Is the recent spike in market volatility taking its toll?

By Frank Buhagiar•13 Aug, 2024

The Top Five

Crystal Amber (CRS) jumps from fourth to top spot on Winterflood’s list of biggest monthly movers in the investment company space. And that’s on the back of no news. In fact, nothing out from the small-cap investor since the 31 July 2024 Investee company update: Morphic Medical. The update highlighted an independent valuation of CRS’ equity interest in Morphic that came in at around US$75.8m (£59.1m). This would increase CRS’ unaudited NAV per share to 172.67p from 117.85p. Interestingly, CRS’ ‘mere’ +13.5% gain on the month (down from +32.9% previously) enough to secure top spot – a symptom perhaps of the uptick seen in market volatility this past week or so.

Jupiter Green (JGC), a new entry into the top five – a gain of +12.8% good for second place. As with CRS above, no news out from the environmental investor, but a look at the graph shows the shares started their move higher on 25 July 2024, round about the time of the latest doceo video update from investment manager Jon Wallace. The power of a good communications strategy there for all to see – the discount has since narrowed from -26% to around -15%.

Downing Strategic Micro-cap (DSM) managed to keep its place on the list despite a more than halving in the share price gain to +12.2% from +29.9%. There was yet another twist in the micro-cap investor’s tussle with activist investor Milkwood. Quick recap: DSM looking to wind itself up and return capital to shareholders; Milkwood looking to stop the realisation strategy in its tracks and get its nominees appointed to the board at the 5 August general meeting. The result of the general meeting though saw a clean sweep for the existing DSM board. As announced by the company “None of the Requisitioned Resolutions were carried.” Ball back in Milkwood’s court.

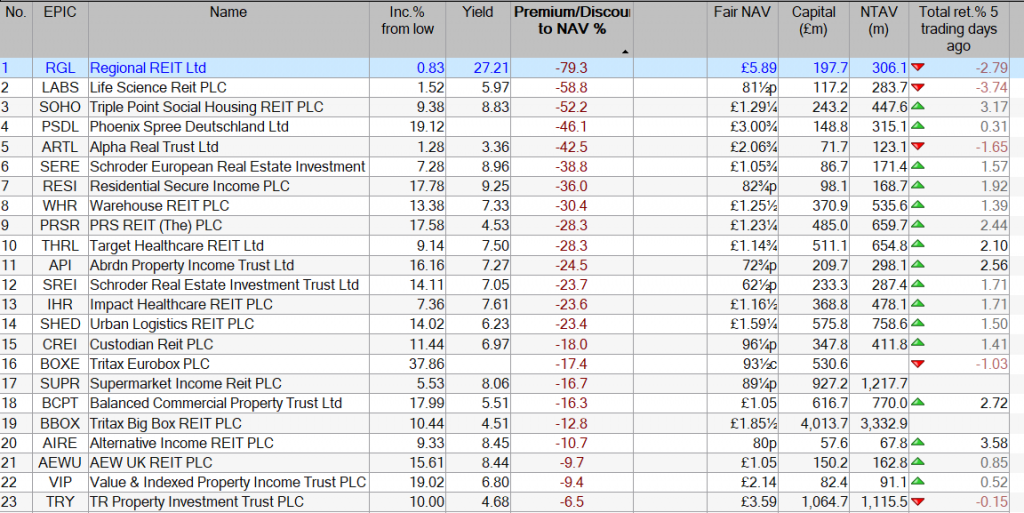

PRS REIT (PRSR) also in third place after exactly matching DSM’s +12.2% rise. Shares in the build-to-rent fund have been on the march ever since the 18 July 2024 Fourth Quarter Update. Second half of the press release’s title says it all “Continued Strong Portfolio Performance”. As for what strong portfolio performance looks like, how about an 11.7% increase in like-for-like rental growth compared to 12 months earlier. That’s not all, “The estimated rental value of the 5,396 completed homes at 30 June 2024 was £65.1m per annum, an 18% increase on the same point last year.”

JPMorgan US Smaller Co. (JUSC) returns to the list after a one-week absence. Two weeks ago, the shares were up +13.5% on no material news flow. Two weeks on and the monthly gain stands at +10.5% on no material news flow. Not much to report on the corporate front then. Different story in terms of markets. Take the Russell 2000. 31 July, the US small-cap index stood at 2254; by 7 August, it was nursing a 10% fall. JUSC couldn’t buck the trend, but it did outperform – over the same period the shares were off only -5.5%. Keep that up and the fund could be on course for another year of outperformance.

Scottish Mortgage

Scottish Mortgage’s (SMT) share price finished the week ended Friday 9 August 2024 down -7.6% on the month. That’s an improvement on the previous -8.6% deficit. The NAV monthly loss stretched to -7.6% from -5.6%. The wider global sector’s loss meanwhile increased marginally to -4.1% from -3.8% seven days earlier. With the tech-heavy Nasdaq largely flat, SMT’s ongoing buyback programme making the difference perhaps, enabling the global growth investor’s share price to outperform.

The Results Round-Up – The Week’s Investment Trust Results

Impax Environmental Markets is staying optimistic after a difficult half year; Witan looks like it’s going out with a bang after posting an 11% NAV total return for what could be its last half year subject to completion of the merger with Alliance; while, JPMorgan American does even better, clocking up a +19.1% NAV total return.

IEM reported a flat(ish) NAV total return per share of -0.5% for the half year,some way off the MSCI World’s +12.2% and the FTSE Environmental Technology 100 Index’s +7.4%. The investment managers put this down to the fund’s bias to mid and small caps, “IEM invests in companies which generate at least 50% of their revenues from Environmental Markets. These tend to be mid and small caps. Small and mid-cap companies have suffered disproportionately from the ‘higher for longer’ interest rate environment, underperforming their large cap counterparts by over 8% over the Period.” And the underperformance was not just down to what IEM held, but also what it didn’t have, specifically notholding AI chip-designer Nvidia, along with Apple, Microsoft, Amazon, Meta and Alphabet, accounts for a -5.7% drag on relative performance.

Despite the shortfall, Chairman, Glen Suarez, continues to have “great confidence that the hypothesis underpinning the Company’s investment strategy – that sustainability pressures create opportunities for companies providing environmental solutions – remains well positioned to deliver financial outperformance over the long-term.” Until then, the investment managers are taking comfort from the fact that performance within the portfolio has been encouraging. Earnings growth has been above that of the broader market. And then there is valuation, “the portfolio’s valuation premium relative to global equity markets has fallen to below its ten-year average.” Underlying portfolio company growth, below average valuation, no surprise “the Manager remains optimistic.” So too does the market, it seems – share price tickled higher over the course of the week.

Investec: “we believe that entrenched secular drivers continue to strengthen. However, this specialist sector is now experiencing a painful valuation normalisation process after a wall of liquidity drove valuations to unsustainable levels. We maintain our Buy recommendation.”

Witan’s (WTAN) Final Results?

WTAN released what could be its last Half-year Report as a stand alone investment company. That is, if its proposed combination with fellow global multi-manager investor Alliance (ATST) gets the green light from investors. And if it is the last, then the fund is going out with something of a bang after reporting a +14.3% shareholder total return and an 11% NAV total return for the half year compared to the benchmark’s +11.7%.

Easy write-up for Chairman, Andrew Ross, but when it came round to writing the outlook section of his statement, was the Chairman in the middle of his supper? “Notwithstanding a sharp bout of volatility in early August, equity markets as a whole seem to have taken the view that, whatever flies there may be in their proverbial soup, they are focused on the substance, not the swimmer. This insouciance, complacency to some, is helped by the increased proximity of easier monetary policy, after the prospect of rate cuts retreated for much of early 2024.” Investors weren’t put off by talk of flies, the results were good for a marginal uptick in the share price.

Winterflood: “Proposed merger with Alliance Trust (ATST) to create c.£5bn multi-manager investment trust, following current ATST strategy. Assuming shareholders approve the transaction, total dividends for FY24 are expected to be at least 6.28p per share, +4% from FY23 (6.04p), marking 50th consecutive year of dividend increases.”

JPMorgan American (JAM) Today and Tomorrow

JAM’s new Chairman, Robert Talbut, had a relatively straightforward first half-year statement to write courtesy of a +19.1% total return on net assets per share in sterling terms. That’s 3% above the total return of the S&P 500’s +16.1% in sterling terms. According to the Investment Managers “The large cap portion of the portfolio, which, at over 94% of the Company’s assets is its biggest allocation, added the most value over the period. Gearing was also slightly additive given the market’s rally. The Company’s small cap allocation, which averaged approximately 5.7% over the period, modestly detracted from relative returns.”

In terms of outlook, the Investment Managers went all nautical “with economic growth solid, unemployment low, most of the journey back to 2% inflation completed, and rates set to decline, the US economy should continue to provide a rising tide to support most investment boats for the rest of this year and into 2025.” JAM one of those investment boats on the rise – share price tacked on 13p on the day of the results to close at 1002p.

Numis: “JAM has built a strong track record since a strategy change in May 2019, shifting to a higher-conviction approach for the large cap component, combining the ‘best ideas’ from JPM AM’s growth and value investment teams. Since then, it has produced NAV total returns of 124.0% (16.5% pa), which compares to 107.2% (14.8% pa) for the S&P 500 and the fund has been one of the standout performers in the universe in recent years.”

abrdn Asian Income (AAIF) – Incoming!

AAIF’s +6.8% NAV total return for the half year, a little behind the MSCI AC Asia Pacific ex Japan’s +9.6% increase. Tables turned over longer timeframes though: AAIF has outperformed the Index over 3 and 5 years in both NAV and share price total return terms. According to Chairman, Ian Cadby, income is playing an increasing role in both the markets and the company’s respective total returns. That’s because “More than 50% of Asian equity total returns now come from dividends and dividend growth.” And in terms of AAIF, based on lastyear’s 11.75p dividend, as at 30 June 2024, the shares were trading on a 5.5% dividend yield. Income by name, income by nature.

And yet, as Cadby points out, “we believe little of this significant progress is priced into markets, with the MSCI Asia Pacific ex Japan Index trading on just 13xPE, compared to the S&P 500 Index on nearly 21xPE. We believe that the often overlooked dividend credentials of Asian equities will become ever more attractive, with investors increasingly recognising the income potential of some of the world’s most exciting companies.”Based on the positive reaction of AAIF’s share price to the results, perhaps investors are now starting to take note.

Winterflood: “Board intends for FY24 dividend to exceed FY23 (11.75p). Net gearing at period-end 7.1% (31 December 2023: 7.5%), as £32.2m of £50m RCF drawn. Ongoing charges 0.86% (FY23: 1.00%) following fee reduction.”

Invesco Bond Income Plus (BIPS) Adopting a Defensive Stance

BIPS’ NAV and share price total return for the first half came in at +3.6% and+3.9% respectively – pretty much in line with the ICE BofA European Currency High Yield Index’s +3.9%. According to the Portfolio Managers’ Report credit-risk assets, rather than bonds, were the main drivers over the period. “The better performance for credit-risk assets reflected changing investor perceptions of the key macroeconomic drivers – growth and inflation. Data on economic activity has generally been a bit stronger than predicted, increasing confidence in corporate earnings and the consequent ability of companies to repay.”

Looking ahead, the portfolio managers are prepared for potential bumps in the road “there is potential for economic activity to weaken. This poses a challenge to corporates, who could face a difficult re-financing environment along with weaker earnings. The balance sheets of more leveraged or weaker businesses may come under strain in these conditions.” As a result “We have reduced our exposure to credit risk in this environment while also maintaining liquidity so that we can take advantage of opportunities that may arise in such weaker market conditions.” Share price too adopting the wait and see approach – shares largely unchanged on the day.

Winterflood: “Managers noted that investment grade market total returns were largely flat in H1, while sovereign (Gilt) returns were mildly negative. High yield spreads over government bonds tightened over the period, reflecting increased risk appetite as economic data was somewhat stronger than anticipated.”

£20,000 in savings ? Here’s how I’d target a large second income from the UK’s property market

Story by Royston Wild

Historically, investing in property’s been a great way to make a strong and sustainable second income. Buy-to-let was particularly popular with those looking to invest their savings.

But conditions have become a lot tougher for private landlords over the past decade. So I’d forget buy-to-let. Here, I’ll reveal what I think’s a much better way to make money from the UK property market.

Fading appeal

But before I do, let’s quickly look at why buy-to-let’s become increasingly unattractive with Britons.

The Tenant Fees Act in 2019 brought in measures like transferring certain costs from tenants to landlords, and capping deposits. The restriction of mortgage interest relief and higher stamp duty on second properties has also had an impact.

Property owners have faced higher mortgage costs since the Bank of England began hiking interest rates.

The effect of all of this has been big. According to price comparison website Finder, the average landlord in April made £4,000 less a year in profit than in 2020, despite monthly rents shooting steadily higher.

Better property buys?

It’s still possible to make money as a landlord, but I’d rather find other ways to make money with bricks and mortar.

Fortunately, UK share investors have what I consider to be an excellent alternative to buy-to-let. Real estate investment trusts (REITs) are companies that invest in a pool of properties in one or across multiple sectors.

We’re talking about hospitals, shopping centres, offices, factories and hotels, for instance. This gives investors a lot of choice, and allows them to spread risk across a wide variety of properties.

Investors also don’t have to pay large upfront sums to get involved with REITs. And under sector rules, these companies must pay at least 90% of annual rental profits out in the form of dividends.

But on balance, I think investment trusts would be a better choice for me.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.