Before we get to the specific numbers, let’s run through the process of how this would all work. Cash gets moved to the ISA, where it then becomes available to invest. By selecting shares that pay out dividends, the investor can benefit from a source of income. Typically, these dividends get paid out a couple of times a year, in line with half-year or full-year accounts.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

To keep things easy, some might just buy a FTSE 100 fund that distributes the income, using the average dividend yield of 3.54%. This is an idea, but I feel that with more active stock-picking, a much higher yield can be achieved without taking on a huge amount of risk

For example, an investor could achieve an average yield of 7% by including a dozen shares from the FTSE 100 and FTSE 250. This would include stocks from a range of sectors, with different dividend payment dates throughout the year.

Real estate options

One example that might be considered for inclusion in such a portfolio could be Land Securities Group (LSE:LAND). The firm is one of the largest commercial property owners. This ranges from office spaces right through to shopping centres.

Over the past year, the share price has been down 13%. Part of this reflects the ongoing concern around commercial property, such as the continued desire for some to work from home. Another factor is the 34.9% loan-to-value ratio from the latest results. With interest rates staying higher than expected for longer, refinancing existing loans or taking on new loans is going to cost more than previously expected.

Even though these remain risks going forward, I think it’s a good stock for an income investor to consider. The current dividend yield is 7.11%, with a dividend cover of 1.27. Any coverage figure above 1 shows that the company can pay the dividend from the latest earnings, which is a good sign.

Running the numbers

If someone were to invest £1666 a month (£20k a year) in a portfolio yielding 7%, the numbers could add up quickly. If this was kept up for seven years, then in year eight, it could make £1,154 a month in passive income.

The post Fully using the £20k ISA allowance could make this much passive income appeared first on The Motley Fool UK.

The Board intends to pursue a dividend policy with quarterly dividend distributions. The level of future payment of dividends will be determined by the Board having regard to, amongst other things, the financial position and performance of the Group at the relevant time, UK REIT requirements, and the interest of Shareholders.

Empiric Student Property PLC ex-dividend date Fidelity European Trust PLC ex-dividend date Primary Health Properties PLC ex-dividend date Schroder Japan Trust PLC ex-dividend date UIL Ltd ex-dividend date Value & Indexed Property Income Trust PLC ex-dividend date VH Global Energy Infrastructure PLC dividend payment date

Buy Investment Trusts that pay a dividend and re-invest those dividends to buy more Investment Trusts that pay a dividend.

Look at value creation potential, not just balance sheet value

The current preferred yield for the Snowball is plus 7%. If u buy a Trust trading at discount to NAV, u could get a bid, if u are lucky, or as market sentiment improves the NAV gap could close. When you re-balance your portfolio any Trusts printing a profit, the profit could be crystallized and re-invested in the Snowball, subject to relative yields.

Buy to hold (but be prepared to sell)

If an Investment Trusts radically changes it’s dividend policy, u need to sell even at a loss. You simply need to read the RNS when the dividend is anoucced.

Stick to what you understand

Build your knowledge of Investment Trusts by Doing Your Own Research

It takes money to make money

If you invest 10k at a yield of 7%, and re-invest at 7%, better if higher. In 60 years that would equate to income of £46,844 pa which would have to be adjusted for inflation.

Better if you can add more funds to buy more Investment Trusts that pay a dividend. GL my friend.

Here, in 5 steps, is how Warren Buffett turned £100 into £3,787,464 !

Our writer learns a handful of lessons from the masterful investing career of Warren Buffett and his phenomenal long-term performance.

Posted by

Christopher Ruane

Image source: The Motley Fool

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

Investing in some shares and seeing their value grow by 24,708% would be very rewarding. That is what happened to the US S&P 500 index between 1964 and 2022 (with dividends reinvested: compounding can really help build wealth!). Impressive though that is, Warren Buffett’s performance left it in the dust.

His company Berkshire Hathaway does not pay dividends. But during that period, its per-share market value grew 3,787,464%.

In other words (excluding currency movements), £100 put into Berkshire shares back in 1964 would have turned into almost £3.8m by the end of 2022.

Know what you’re aiming to do

Warren Buffett has learnt on the job. His strategy today is different to how it was in the 1960s (or even a few years ago).

But the broad principles have stayed the same: he has tried to accumulate wealth by paying less for stakes in businesses (or whole businesses) than he thinks they are worth.

Look at value creation potential, not just balance sheet value

Early on, Buffett saw value buying shares for less than their net asset value.

It used to be more common than now, but some shares do still trade below net asset value. FTSE 100 member Pershing Square Holdings had a net asset value of £59.70 per share on Tuesday (28 January), yet its shares could be picked up this week for around £42 apiece.

Warren Buffett moved from a focus on current net asset value to look instead at what assets a company had that might help it create recurring value in future.

Buy to hold (but be prepared to sell)

An example is his stake in Coca-Cola

Thanks to its brands, proprietary formula, and distribution network, the drinks maker has been a massive cash generator over the decades. It faces risks like shifting tastes and health trends. But the cash has kept coming!

Berkshire bought shares between 1987 and 1994 and has simply held onto them.

It could have sold along the way for a quick buck. But buying to hold means that Warren Buffett now gets more than half as much as the stake originally cost every year in dividends – and the shares themselves have ballooned in value.

But, while he buys to hold, Buffett does sell on occasion. When an accounting scandal hit Tesco in 2014, he dumped his remaining shares in the supermarket at a sizeable loss.

Stick to what you understand

Tesco was one of Buffett’s few forays into the UK market. His main focus has always been his native US – and industries he understands, like insurance and banking.

Warren Buffett is a firm believer in sticking to one’s own circle of competence, whatever it is.

It takes money to make money

Obvious as it may sound, to turn £100 into over £3.7m requires £100 in the first place!

Warren Buffett’s success shows that it is possible to start investing on a small budget: he began buying shares as a schoolboy. But, even if the budget is small, it needs to be something.

Here’s how to start earning a second income with dividend shares

Story by Zaven Boyrazian, MSc

Here’s how to start earning a second income with dividend shares

With the cost-of-living crisis increasing pressure on households, the importance of earning a second income’s rising rapidly. Luckily, dividend shares offer a potential solution to this problem, allowing focused investors to earn impressive long-term passive income.

Dividends explained

Not all businesses are high-flying enterprises. The London Stock Exchange is to many mature businesses whose explosive growth days are now in the rear-view mirror. However, with the strong demand for their products and services, their cash flows remain robust. As such, with no other use of capital internally, management teams are returning a large chunk of this cash back to shareholders – the owners.

Typically, dividend payments come every quarter, although this frequency can be different depending on the business and its cash flow timings. However, most companies like to keep payment timing relatively consistent. And investors can leverage that to establish a reliable and predictable income stream.

If cash flows become disrupted, dividends can often find themselves under pressure. And if market conditions become too adverse, shareholders may see their payouts get cut or even outright cancelled. As such, the second income generated by an investment portfolio can take a hit on relatively short notice.

Luckily, such risks can be managed with prudent market monitoring and portfolio diversification.

Best income stocks to buy now?

There are a lot of UK dividend shares to pick from. However, not all of them offer the best value or long-term income potential. And depending on the risk tolerance and time horizon of an investor, the best dividend shares to buy can vary, depending on the individual

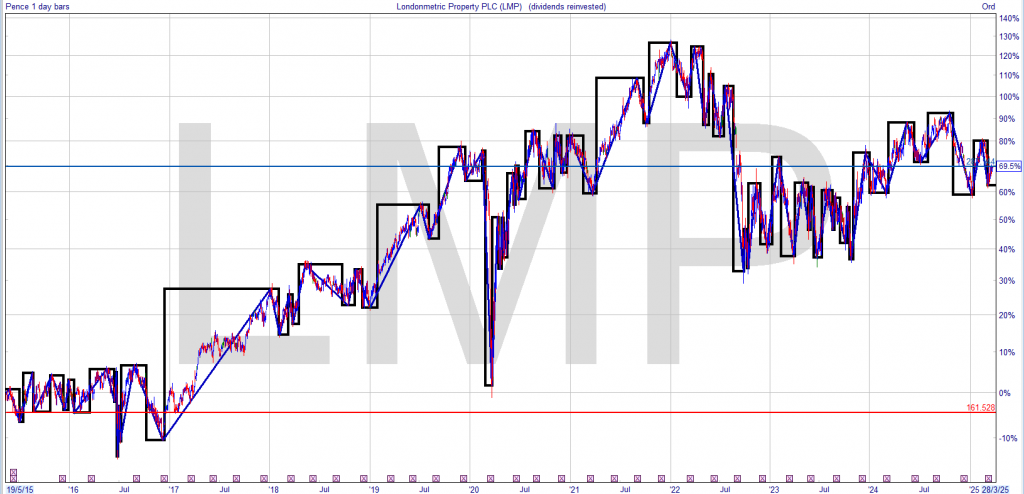

Higher interest rates have wreaked havoc on property prices, even in the commercial sector where LondonMetric operates. And with the book value of its assets marked down, shares are still trading at a forward price-to-earnings ratio of 13.9.

To be fair, weakened asset prices can be problematic. Suppose management suddenly needs to sell properties to raise capital. In that case, it will likely have to do it at a discount, given the weakness in the commercial real estate market. And the group’s £2.2bn of debt does add pressure to the bottom line, due to higher interest rates.

However, despite these handicaps, demand from tenants and occupancy remains strong, as do cash flows. That’s why LondonMetric Property’s already in my income portfolio, and I feel other investors may want to consider it for theirs.

The post Here’s how to start earning a second income with dividend shares appeared first on The Motley Fool UK.

How investors can combine a best-of-both income and growth mandate…

Jo Groves and David Brenchley

Disclaimer

This is a non-independent marketing communication commissioned by Schroder Investment Management. The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

The outlook for income-focused investors is ever-changing. Looking back 15 years, the standard 60/40 portfolio provided benefits: the 60% equity portion gave good growth and a decent income, while the 40% bond portion gave predictable income and protected your capital when stock markets fell.

Fast-forward to the post-financial crisis period and while bonds provided protection, they generally failed on the income side due to low interest rates, moving investors up the risk curve with equities and alternatives taking up the slack.

Coming full circle, bonds again offer attractive income, with the 10-year gilt yielding c. 4.7%, so have a role to play in an income portfolio. As seen during 2022, though, they have become more correlated with equities: UK government bonds’ correlation with global equities has been low over 10 years, at 0.28, but over three years it’s risen to 0.65.

With the potential for more inflationary episodes moving forward, this could be a running trend. Cash, meanwhile, might look attractive on the face of it, but interest rates are now on a downward trend, so you’re leaving yourself open to reinvestment risk: if you’d put cash into a one-year fixed-term bond paying 5.5% at the start of 2024, you’d only be able to get c. 4.7% if you wanted to reinvest.

Bonds and cash also offer little to no prospect of capital growth, as opposed to more productive assets such as equities, property and infrastructure. Schroders’ forecasts suggest that gilts will return c. 4.8% per year for the next decade – well below stock markets.

One asset class that has maintained its negative or low correlation to global equity markets is property. UK commercial property’s correlation with global stocks has been 0 over 10 years and 0.07 over three years.

The higher-yielding stock markets today look to have better potential future returns, too. As shown in the graph below, that’s particularly true of the UK, emerging markets and Japan, with Schroders forecasting annual returns of 10.5%, 10% and 7.9% respectively, while the lower-yielding US market has expected returns of 6.6% over the next decade.

Looking beyond the US for growth

Source: Schroders (December 2024)

The anatomy of an income portfolio

Bonds remain a key component of any income portfolio, with their current high and attractive yields at c. 4.7% for the 10-year gilt. However, diversifying across other sectors could enhance the growth potential of a portfolio.

Property

Real estate investment trusts (REITs) have a history of delivering consistent and growing dividends, with yields in the AIC: Property – UK Commercial sector of between c. 5.4% and 8.7% attractive, given the 10-year UK gilt yield of c. 4.7%.

Those gilts have little to no prospect of capital growth; property’s positive supply and demand dynamics and potential for sustainability improvement offer good income and capital growth prospects.

The economic backdrop looks to have become more constructive, too. The MSCI UK Monthly Property Index clocked up a 1% gain in the three months to November 2024. That’s stemmed the tide, after a two-year bear market where capital values fell by c. 25%. Encouragingly, rents, in aggregate, actually grew by a solid 7.5% during that two-year period. Further reductions in the interest rate should also be positive for REITs.

Looking to the UK can pay dividends

The UK stock market ranks highly versus most other countries and is on a par with what’s available from gilts and savings accounts, as you can see from the table below.

The UK’s income advantage

Source: MSCI

The FTSE 100’s c. 3.5% yield provides a solid base, but the FTSE 250’s c. 3.3% yield looks attractive, too, and gives you the potential for more of a total return. Mid-cap stocks have outperformed their large-cap counterparts by c. 190 percentage points over the past 30 years.

UK plc’s dividend cover is the healthiest it’s been for over 10 years, too, and share buybacks are becoming more prevalent in the UK market. Adding together dividends, buybacks and takeovers, the FTSE 350 has an estimated cash yield of 8.3%, according to the investment platform AJ Bell.

Don’t overlook Asia for yields…

Asia offers compelling income opportunities with higher yields than some of the traditional equity income markets in the UK and Europe. Its income credentials are underpinned by a diverse set of drivers due to the heterogenous nature of its universe, including Taiwan and South Korea’s dominance in semiconductors, corporate governance reforms in Japan and financialisation in Indonesia.

Asia is also the epitome of a growth story, having recently reached the pivotal milestone of generating more GDP than the rest of the world combined. The next wave of expansion will be driven by a surging domestic consumer class, with the World Data Lab reporting that Asia added 90 million consumers in 2024 alone. With the tailwinds of favourable demographics and strong economic growth, its global influence looks set to increase further in coming decades.

The best of both worlds in biotech

While biotech isn’t traditionally an income sector, the high level of M&A in the biotech sector generates cash that can be reinvested or distributed as dividends to investors. As a result, a small number of investment trusts have adopted an enhanced dividend policy with a NAV-linked payout to provide both income and capital growth for investors.

Turning to the potential for capital growth, healthcare is a substantial and growing market, with the World Economic Forum reporting that global spending hit $10 trillion, or 10% of GDP, in 2022 and spending is forecast to outpace GDP growth in the coming years. Due to its high level of innovation, the global biotech sector is forecast to enjoy significant growth of 12% to surpass $4 trillion by 2033, according to Precedence Research.

How investment trusts provide an advantage

Investment trusts offer several benefits for income-focused investors. A key benefit is their ability to provide stable and sustainable dividends by retaining up to 15% of annual income in reserves, allowing them to maintain dividend payments during periods of market downturns or economic uncertainty.

The AIC list of dividend heroes is testament to the income-generating advantages of the investment trust structure, with Schroder Income Growth (SCF)having increased its dividends for the last 29 years. In contrast, open-ended funds must distribute annual income received, leading to a more variable income stream.

The closed-ended nature of investment trusts also provides the flexibility to invest in less liquid assets, including property and small-cap companies. This includes access to unquoted companies which can offer strong returns, particularly in sectors like biotech, where private firms are increasingly opting for strategic acquisitions over an IPO.

By holding a mix of liquid and illiquid assets, investment trusts can enhance diversification, supporting long-term capital appreciation alongside income generation.

How to improve diversification without sacrificing income

Investing across a range of income-generating sectors improves diversification, preventing a portfolio from being overly reliant on one single source of income such as the FTSE 100.

As illustrated in the graph below, the FTSE 100 Index, commonly used as a benchmark for the UK equity income sector, demonstrates a high positive correlation with the S&P 500 and MSCI World indices. In contrast, it shows a much lower correlation with Asian and biotech indices, while the UK property sector remains largely uncorrelated to the FTSE 100.

How sector diversification can reduce correlation

Source: FE Analytics, correlation of 5-year total returns in GBP, UK property based on FE UK Property Proxy (as at 24/02/2025)

Harnessing the green premium

The fact that commercial property rents increased during a tough backdrop of rising interest rates and, consequently, falling capital values, shows that the income side holds up.

The self-help factor can cement REITs’ income advantage, as demand grows for environmentally friendly buildings. The managers of Schroder Real Estate (SREI) believe that tenants are increasingly willing to pay a premium for energy-efficient buildings and for a good environment for employees. This could have a triple impact by boosting rents, improving vacancy rates and raising capital values.

SREI’s unique strategy of turning brown buildings green should help it deliver on its dual mandate of providing income and capital growth while achieving meaningful and measurable improvements in its sustainability profile.

SREI’s 6.4% dividend is well covered (c. 104%) by earnings and backed up by a reversionary yield of 8.4%, hinting that its already impressive five-year record of c. 5.6% per annum dividend increases can continue.

In addition, a 4% NAV total return in the three months to 31/12/2024 was the company’s strongest quarterly performance since June 2022, suggesting that while it’s early days, managers Nick Montgomery and Bradley Biggins seem to be harnessing that green premium.

Securing a total return from the UK

The high yields on offer from UK equities already gives our domestic market an income advantage. Yet, there’s an argument that the UK is a fertile hunting ground for total return investors. It’s rare that the FTSE 250 has a yield on a par with the FTSE 100 and provides the potential for higher income and capital growth than ordinarily might be the case.

Active management can harness this most effectively, as yields in small- and mid-cap land are high for a reason, with plenty of value traps out there.

Step forward SCF, where managers Sue Noffke and Matt Bennison look for businesses with healthy cash flows and solid balance sheets, giving them firepower to pay healthy and growing dividends, invest for growth and engage in share buybacks where appropriate.

In addition, Sue and Matt can call on the deep resources within Schroders’ UK equities team, allowing them to fish from a bigger pool that includes the whole market-cap spectrum, a pond from which many of its peers are unable to fish.

The benefits of this approach shine through. SCF’s unbroken record of dividend increases is impressive, while 60% of its portfolio holdings conducted buybacks in its most recent financial year, up from 38% in the previous year.

Tapping into Asia’s growth story

Asia offers diversification for a UK equity income strategy by offering a unique mix of growth and income drivers. The region offers a compelling blend of high-growth economies such as Vietnam and the Philippines, alongside mature yet dynamic markets like Singapore and Australia (which still boast higher GDP growth forecasts than most G7 nations).

Given its diversity, Asia is arguably best suited to an active strategy and Schroder Oriental Income (SOI) is well-positioned to capitalise on the unique growth drivers across the region. Manager Richard Sennitt, supported by Abbas Barkhordar, together have a combined five decades of experience and leverage extensive on-the-ground resources to identify the most attractive opportunities.

SOI’s portfolio balances export-led industries with domestic consumption plays. Around a quarter of its holdings are in Taiwan, where TSMC has delivered impressive returns thanks to its partnership with NVIDIA. Meanwhile, rising financial inclusion across Asia is fuelling demand for banking, insurance and real estate services, with SOI overweight in these sectors.

Rather than simply chasing high yields, Richard and Abbas focus on companies offering both income and growth potential. SOI currently offers a 4.4% dividend yield, comfortably above the 2.7% and 3.5% for the MSCI AC Pacific ex-Japan and UK indices respectively (as at 28/02/2025).

It’s also delivered a ten-year share price return of 104%, compared to 85% for the FTSE 100, compensating investors for the extra risk of investing in Asia.

Why Japan looks set to shine

Not only is Japan the fourth largest economy, it’s also home to a number of world-leading companies such as Toyota, Sony and Mitsubishi. As mentioned earlier, it’s also projected to deliver an impressive annual return of 8% over the next decade, above both global and US markets. And Japanese equites have the ultimate seal of approval from Warren Buffett, who plans to increase his stake in five major Japanese trading houses.

Japan is strategically positioned to benefit from Asia’s growth story, supported by an improving macroeconomic environment. Inflation has returned, restoring corporate pricing power for the first time in decades and supporting a positive cycle of wage growth and increased corporate earnings. Japan also offers a diversified range of sectors that should benefit from the China+1 strategy as well as smaller, innovative companies capitalising on megatrends such as robotics, artificial intelligence and decarbonisation.

Schroder Japan (SJG) is the highest-yielding trust within the AIC Japan sector, offering an enhanced dividend policy that distributes 4% of NAV, resulting in a current dividend yield of 4.6%.

Managed by Masaki Taketsume, SJG focuses on high-quality companies with the potential for a re-rating in valuation driven by company-specific factors. This has provided the foundation for the trust outperforming the TOPIX index with a share price total return of over 110% over the past decade.

Japan’s commitment to corporate reform has made it an attractive income alternative, with dividend payments soaring in recent years. That said, low payout ratios and the number of companies in a net cash position provides the potential for further yield improvement.

Riding the biotech tailwinds

Biotech is a high growth sector, driven by strong structural and idiosyncratic tailwinds from an ‘older, richer and sicker’ global population.

One of the most significant growth drivers is a demographic ‘time bomb’, with the United Nations forecasting a doubling of the over-65s within the next 30 years, increasing the incidence of age-related chronic diseases such as heart disease and cancer.

Global healthcare spending is also forecast to rise, fuelled by increasing expenditure from developing nations. According to the OECD, healthcare expenditure in India and China remains below $1,000 per capita compared to over $6,000 in most G7 economies.

The biotech industry has also seen record numbers of clinical trials, with breakthroughs in gene, RNA, and cell-based therapies for previously untreatable conditions, as well as game-changing anti-obesity drugs.

The biotech sector is best suited to active management with the specialist expertise to optimise returns while managing downside risk. One such example is International Biotechnology Trust (IBT), which has outperformed its benchmark with a 10-year share price return of over 110% compared to 70% for the Nasdaq Biotechnology Index (as at 17/02/2025).

M&A activity has been a key driver of returns, with large pharmaceutical companies turning to acquisitions to plug the projected $200 billion ‘patent cliff’ by 2030. Since 2020, the acquisition of 21 quoted and 5 unquoted companies from the IBT portfolio has highlighted the stock-picking prowess of Ailsa Craig and Marek Poszepczynski.

IBT offers a highly differentiated source of income by offering a dividend (based on 4% of NAV), providing both income and growth potential for investors. Paying dividends from capital ensures a more secure stream than relying on dividends received from underlying companies.

Final thoughts

While cash and bonds are popular choices for income-seeking investors, other asset classes offer the potential for a reliable income stream without sacrificing capital growth. Although income-focused investors have traditionally focused on the UK equity income sector, this overlooks some of the high-yielding opportunities in other sectors.

Diversifying across a broad range of asset classes provides exposure to a range of unique growth drivers, from the burgeoning middle-class consumer base in Asia to the green premium in the commercial property sector. Combined with the benefits of an investment trust structure, these diverse opportunities offer the potential for both sustainable income and long-term capital growth.

Many people dream of earning passive income while sleeping but few understand the specific strategies to reach that goal.

There’s actually a wide range of options, some that are fairly easy and others extremely difficult. Setting up a business, for example, can be lucrative, but it’s risky and takes a lot of initial time and effort.

Investing in dividend stocks is much easier but still involves time, money and a side order of risk.

Right now, the UK market looks like a great place to get started. For a rare moment in history, the FTSE 100 is outperforming the S&P 500 over a 12-month period.

Created on TradingView.com

Yet there are still many high-yield dividend stocks selling at discount prices.

Grab your calculator

Ok, so £15,000 a year — that’s a hefty chunk of passive income. How many dividend stocks are needed to achieve that? Well, dividends differ from stock to stock but we can get an idea of their value from the yield. This is the percentage each one pays on the share price.

A few quick calculations tell me that about £214,000 is needed to return £15,000 a year.

That’s a lot of dividend stocks!

Which stocks might be best?

In my portfolio, I try to aim for stocks with yields between 5% and 9% so that my average yield is around 7%. I think this is a realistic target for the average investor.

Take Legal & General, for example, with its 9% yield. It’s quite possibly the most popular dividend stock in the UK — and for good reason. It has a very long history of proving its dedication to shareholders by consistently increasing dividends.

For income investors, this is usually the most important factor. When a company cuts or reduces dividends, it can devastate a passive income strategy. L&G never misses a beat, raising dividends by around 5% to 20% every year.

To help counter this, it regularly buys back its own shares to boost the stock’s value. Currently, it’s planning a further £500m on top of a previous £1bn.

But it’s just one stock worth considering. Other good examples include Aviva, HSBC and Imperial Brands. Building a portfolio of 10 to 20 similar high-quality dividend stocks is the first step in this strategy.

But what about the £214,000?

That’s the slow part. To reach that goal requires regular investment, patience and compounding returns.

Say an investor puts £300 a month in a 7% portfolio with moderate 4% price appreciation. Even with dividends reinvested, it’s going to take over 20 years to reach £214k.

But as they say — time is money. So get started as soon as possible and who knows, maybe one day both time and money will be available in abundance !

The best closed-end funds will significantly boost your portfolio income and allow you to buy their underlying stocks and bonds at a discount.

(Image credit: Getty Images)

By Charles Lewis Sizemore, CFA

If someone offered to sell you a dollar for 90 cents . . . well, you’d probably think it was too good to be true. Yet these are exactly the kinds of opportunities that arise in the market’s best closed-end funds (CEFs).

CEFs are a type of investment fund, and in fact, they are older than mutual funds. The very first closed-end fund was launched in 1893 – more than 30 years before the first traditional mutual funds (like those you might find in your 401(k) plan) were created.

As with their mutual fund cousins, CEFs are pooled investment vehicles that hold portfolios of stocks, bonds or other assets. But that’s where the similarities stop.

Mutual funds are open-ended. When you want to invest, you or your broker sends cash to the fund, and the manager takes that fresh cash and uses it to buy assets. When you want to sell, the manager will sell a small amount of assets to cash you out. Money is always coming and going, and there’s no hypothetical limit to the amount of new money a popular fund can take in and invest.

Kiplinger

Closed-end funds are different. CEFs have initial public offerings (IPOs) like stocks, and there is a fixed number of shares that then trade on the stock market. If you want to buy shares, you buy them the same way you’d buy a stock.

And here’s where the fun starts. CEF prices are set by the market the same way a share of Apple (AAPL) or Amazon.com (AMZN) would be, but that price can vary wildly from the value of the assets the fund holds. It’s not uncommon to see CEFs trading at a premium to the value of the assets they own. But just as you’d never pay $1.10 for a dollar, you’re generally better off avoiding CEFs trading a premium.

Discounts, however, are another story. Closed-end funds often sell at massive discounts to net asset value (NAV). In these cases, they’re effectively worth more dead than alive!

Another nice aspect of CEFs is that, unlike mutual funds, they can use debt leverage to juice their returns. That same leverage also allows closed-end funds to sport some of the highest yields you’re likely to find.

Today, we’re going to take a look at some of the best CEFs on the market. Each of these funds trades at a reasonable discount to NAV and offers a yield that’s at least competitive, if not downright extravagant.

Data is as of November 24. Distribution rate is an annualized reflection of the most recent payout and is a standard measure for CEFs. Distributions can be a combination of dividends, interest income, realized capital gains and return of capital.

Nuveen Real Estate Income Fund

Market value: $284.0 million

Distribution rate: 7.2%

Discount to NAV: -4.3%

Expenses: 3.64%*

It’s been a rough stretch for real estate investment trusts (REITs). Because REITs have always had a major emphasis on income, investors came to view them as a bond substitute over the past two decades. But when bond yields surged in 2023 – and bond prices collapsed – REIT prices also fell in sympathy.

But now that prices in the sector have reset, investors have a chance to buy quality real estate assets on the cheap. And there’s an inflation angle as well. Land and building prices tend to at least keep pace with inflation over time, and commercial rental contracts will generally have rent escalators that will rise.

REITs are a fine way to get exposure to real estate. But why pay retail for them if you don’t have to?

The Nuveen Real Estate Income Fund (JRS, $7.67) is one of the best closed-end funds that invests in REITs. It owns essentially the same collection of REITs you’d expect to find in any mutual fund or exchange-traded fund (ETF), such as logistics REIT Prologis (PLD), data center REIT Equinix (EQIX) or self-storage operator Public Storage (PSA), but it has the added benefit of owning them at a discount.

At current prices, JRS trades at a 4.2% discount to NAV, which is wide given this CEF’s history. It also yields a very juicy 1.5%.

The Fed might be successful in bringing inflation to heel. Or we might see several more quarters of sticky inflation. Only time will tell. But either way, it makes sense to own a little real estate, and JRS is a smart way to do so.