Big Dividend Smackdown: This 6.4% Payer Crushes Its 12% Rival

by Michael Foster, Investment Strategist

Think back three months: The market was in the throes of the “tariff terror.” Us ? We were doing what we always do: sifting out overly beaten down closed-end funds (CEFs) with huge yields.

Today, the stock market is doing the opposite of what it was back then – levitating from all-time high to all-time high. And we’re still finding bargain-priced dividends. Right now, some of the best ones are in corporate-bond CEFs.

Let’s keep at it now by zeroing on two corporate-bond CEFs that are still undervalued – though one much more than the other. On average, they yield north of 9%.

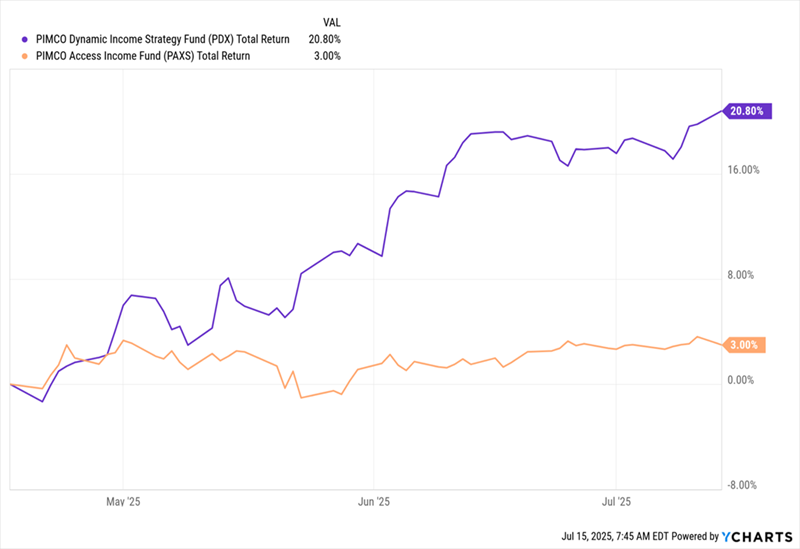

I mention the April tariff crash for a reason: In an April 17 article (published as trade confusion reigned), I focused on two oversold PIMCO corporate-bond funds that, at the time, yielded 10.1% between them. Those were the PIMCO Dynamic Income Strategy Fund (PDX) – currently a holding in our CEF Insider service – and the PIMCO Access Income Fund (PAXS).

Since April 17, PAXS (in orange below) and PDX (in purple) have bounced, posting a nearly 12% average total return, based on their market prices. But the gains have been lopsided.

PIMCO Funds Surge (With PDX Leading) We’ll talk about that gap more in a second. First, let’s dig into the dividends, since they’re usually investors’ No. 1 reason for buying CEFs.

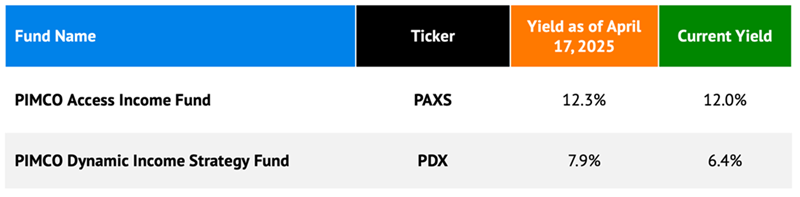

If you’d bought these CEFs on April 17, you’d have gotten a 10.1% average yield. Here too, the gap was quite big between the funds, with PAXS yielding over 12% at the time.

Note that these funds’ average yield has fallen due to price gains (as prices and yields move in opposite directions), though PAXS’s yield is still near where it was in April, at 12%. In other words, the fund’s smaller market-price gains mean it still offers a lot of income.

This is takeaway No. 1 in CEF investing: The higher yielder isn’t always the bigger short-term winner. In fact, it’s often the opposite: Many investors fear all big yields – even many CEF investors. (There’s really no excuse for that, since many CEFs have offered 10%+ yields for years without major payout cuts).

As a result of that fear, lower-yielding CEFs tend to bounce higher than bigger payers after a market panic. So PDX’s outperformance is no surprise. But there’s something else going on with these funds’ net asset values (NAVs).

NAV is a measure of a CEF’s portfolio performance: Since CEFs have fixed share counts, their NAV and market-price performance usually differ. A market price below NAV results in the “discount to NAV” that we CEF buyers covet.

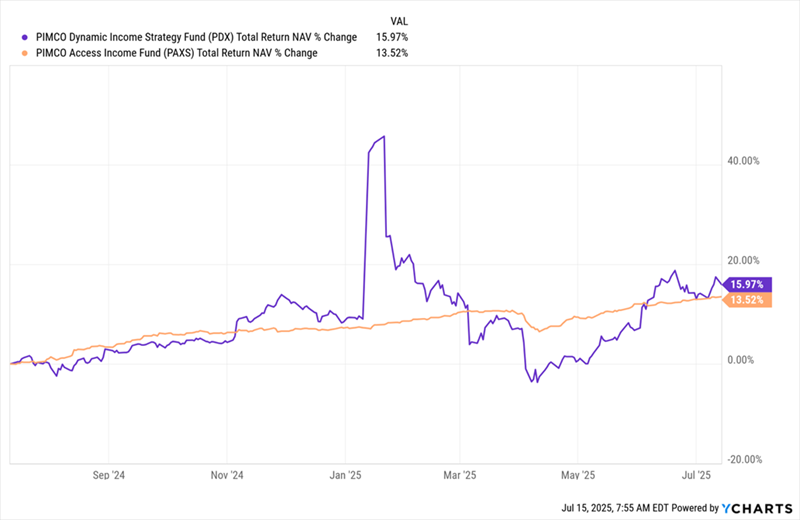

PDX’s Portfolio Edges Out PAXS Over the past year, PAXS (in orange above) and PDX (in purple) have posted similar total NAV returns, with PDX edging ahead. That’s not too surprising, as both funds invest in a mix of credit assets and have overlapping management teams.

However, some aspects of PDX’s portfolio, like a focus on energy and oversold floating-rate credit, drove its outperformance (including that spike in early 2025) at different times over the last 12 months. In the future, we can expect both funds to keep recovering, mainly because of their discounts to NAV.

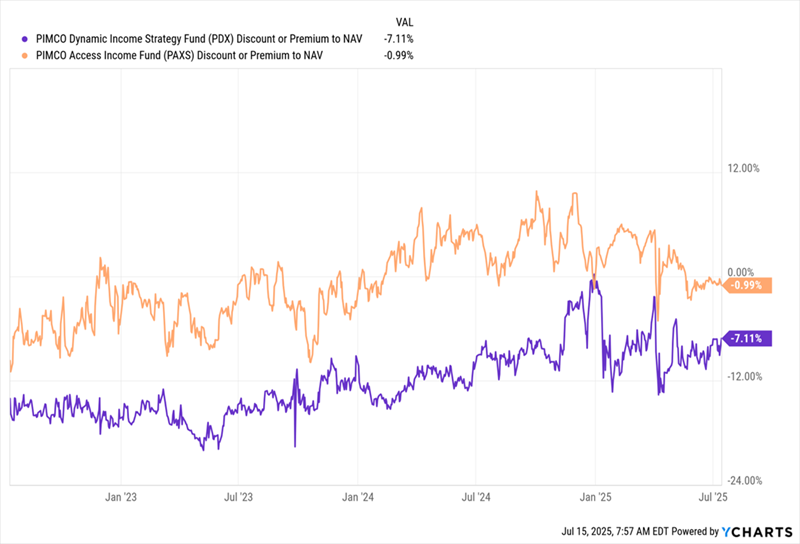

PDX, PAXS Discounts Bubble Away Both funds trade at discounts as I write this, with PDX’s markdown being much bigger, at 7.1%. That makes the fund the more appealing choice between these two, even with its lower yield.

I expect PDX’s closing discount to result in a bigger total return than we’d get from PAXS in the long term, even if that discount is rangebound today. However, PAXS isn’t a bad fund, with the market’s continued gains spurring a bigger appetite for risk and income. As more investors look to CEFs, we should see more demand for those with the highest yields, and 12%-paying PAXS is nicely set up to benefit from that.

PAXS’s portfolio mix of leveraged-credit investments should allow its NAV to keep climbing in a rising market. That, in turn, would attract more investors and bring the fund’s tiny discount to a premium. This wouldn’t be unprecedented, since PAXS was trading at a double-digit premium less than a year ago.

In fact, a premium is likely for both funds in the longer term, since they both operate under the PIMCO name, and PIMCO CEFs tend to trade at large premiums.

There are lots of reasons for this, including the fact that investors generally don’t like to sell PIMCO funds because they often do outperform, and the company aggressively courts the ultra-rich in California via wealth managers.

As a result, many shares of these funds sit in accounts and aren’t traded very much. In the past, in fact, I’ve seen premiums on PIMCO funds shoot as high as 40%!

Could PAXS or PDX see that type of premium? It’s possible, though it will likely take years – though these funds’ current high payouts would make the wait a pleasant one.

Earlier this year, Warren Buffett announced he would be stepping down as chief executive of investment conglomerate Berkshire Hathaway (US:BRK.B). For more than 60 years, he has championed the importance of buying stocks based on their valuation rather the hype surrounding them. It was an approach that promoted discipline over speculation, and made him one of the richest people in the world.

The numbers are remarkable. Since 1965, Berkshire Hathaway has returned a compound annual gain of 19.9 per cent. This resulted in a total gain of over 5mn per cent, compared with 39,000 per cent for the S&P 500.

However, these total returns don’t tell the whole story. Berkshire Hathaway’s most successful years came in the 1970s, 1980s and 1990s. In the past decade, the business struggled to outperform a market that’s been driven by megacap technology stocks.

As a value investor, Buffett has never wanted to pay up for stocks he believed to be overvalued. Most recently that has meant not owning artificial intelligence (AI) company Nvidia (US:NVDA), which this month became the first business to be valued at $4tn (£3tn). As a result, in 2023 Berkshire Hathaway’s 15.8 per cent returns lagged the S&P 500’s 26.3 per cent growth.

It’s been a similar story of underperformance for most of the value fund managers who see themselves as Buffett’s disciples.

In the 2010s, a well-established market theme said that low interest rates favoured high-growth stocks. The logic went that these companies, whose cash flows were further out in the future, were more vulnerable to higher rates. The longer an investor must wait for a stock to generate cash flows, the more risk-free returns (such as those offered by government bonds) they sacrifice.

Low rates meant that, when people questioned increasingly expensive stock valuations, the rationale was usually ‘Tina’: ‘there is no alternative’. In other words, with bond yields so low, the only place to invest was shares – including fast-growing but lossmaking technology companies.

Goodbye value investing

Value investors were one of the main victims of this investment regime. The concept of value investing was popularised by Benjamin Graham’s book The Intelligent Investor. In short, Graham’s philosophy was that investors should buy stocks that were cheap relative to their earnings and then hold them for a long time. For Graham, a shrewd investor is “one who bought in a bear market when everyone was selling and sold out in a bull market when everyone was buying”.

This is the opposite of a momentum investor, who buys stocks that are rising in value in the hope that other investors will also do so. “People talk about value versus growth [investing], but really it is value versus momentum,” says Ariel Investments fund manager Timothy Fidler. “Value is by definition a negative momentum expression, and momentum has definitely been the dominant force in the market.”

Investors’ Chronicle

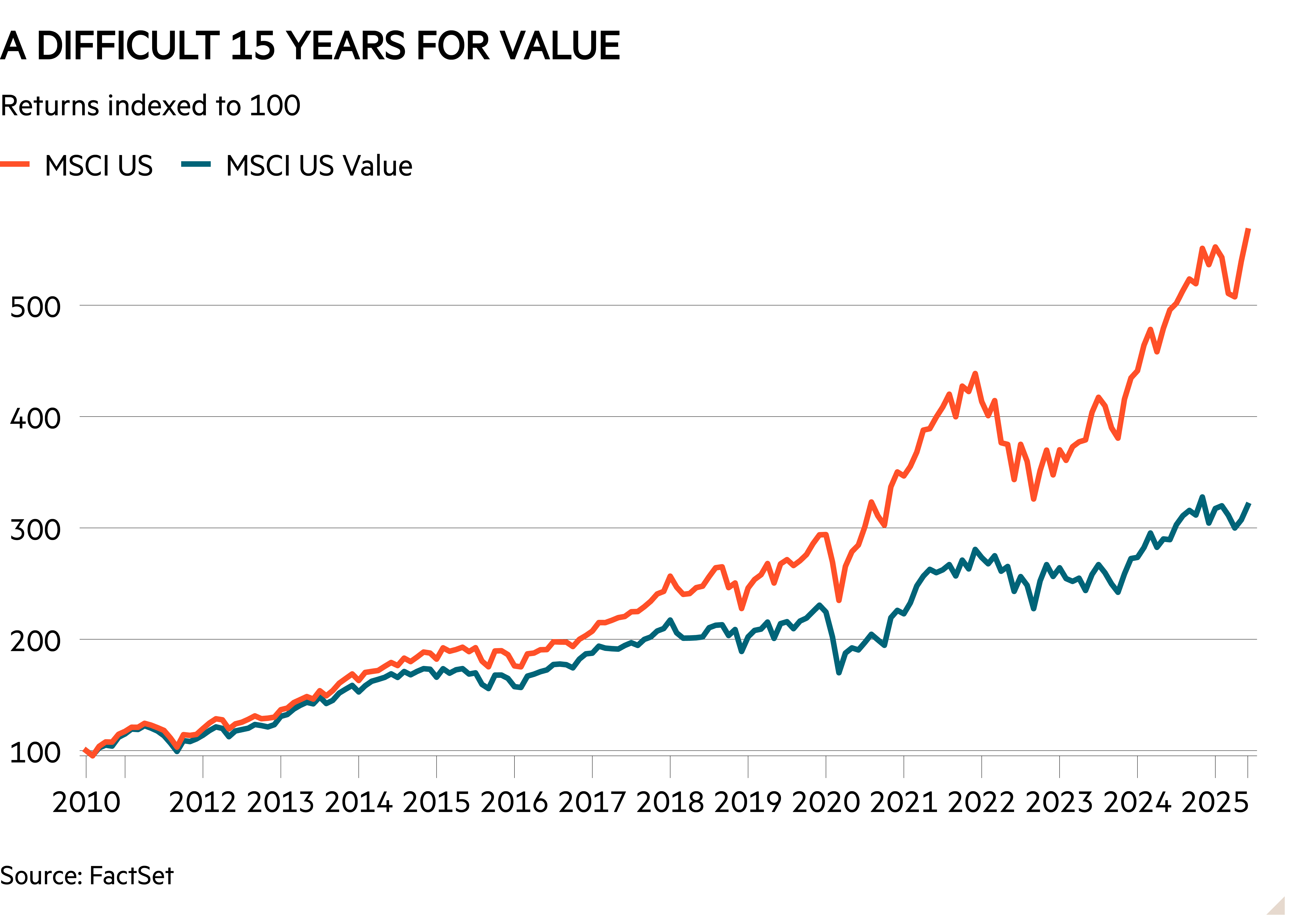

For value investors, the hope was that when interest rates started to rise, stock fundamentals would become more important again. However, this hasn’t quite happened – at least in the world’s biggest market. While value shares have consistently outperformed growth in the UK since the rate-hiking cycle began, in the US the opposite is the case. US value indices produced far superior performance in 2022, coupled with a marginal outperformance so far this year. Cumulatively, however, the MSCI USA Growth Index’s 45 per cent return since the start of 2022 is almost double that of the value index.

The upshot is that stock market valuations have remained at record highs. The S&P 500’s consensus forward price/earnings ratio is 22, higher than it was at the start of the rate-hiking cycle.

The market continues to rise, as do valuations. The new rationale is that AI will shift earnings growth higher, but the outcome of that bet is still uncertain. This is either the beginning of a new era, where this time things really are different, or we are nearing the end of a years-long bull market.

On some metrics, the stock market is now as expensive as it’s ever been. “Equity valuations in the US have always been high, but rising interest rates make it obvious quite how high,” says Third Avenue portfolio manager Matthew Fine. “The equity risk premium is now negative, which means the anticipated earnings yield is expected to be lower than Treasury yields.”

Professional investors refer to the “equity risk premium” as the additional return that they demand for holding stocks instead of risk-free assets, such as Treasury bonds.

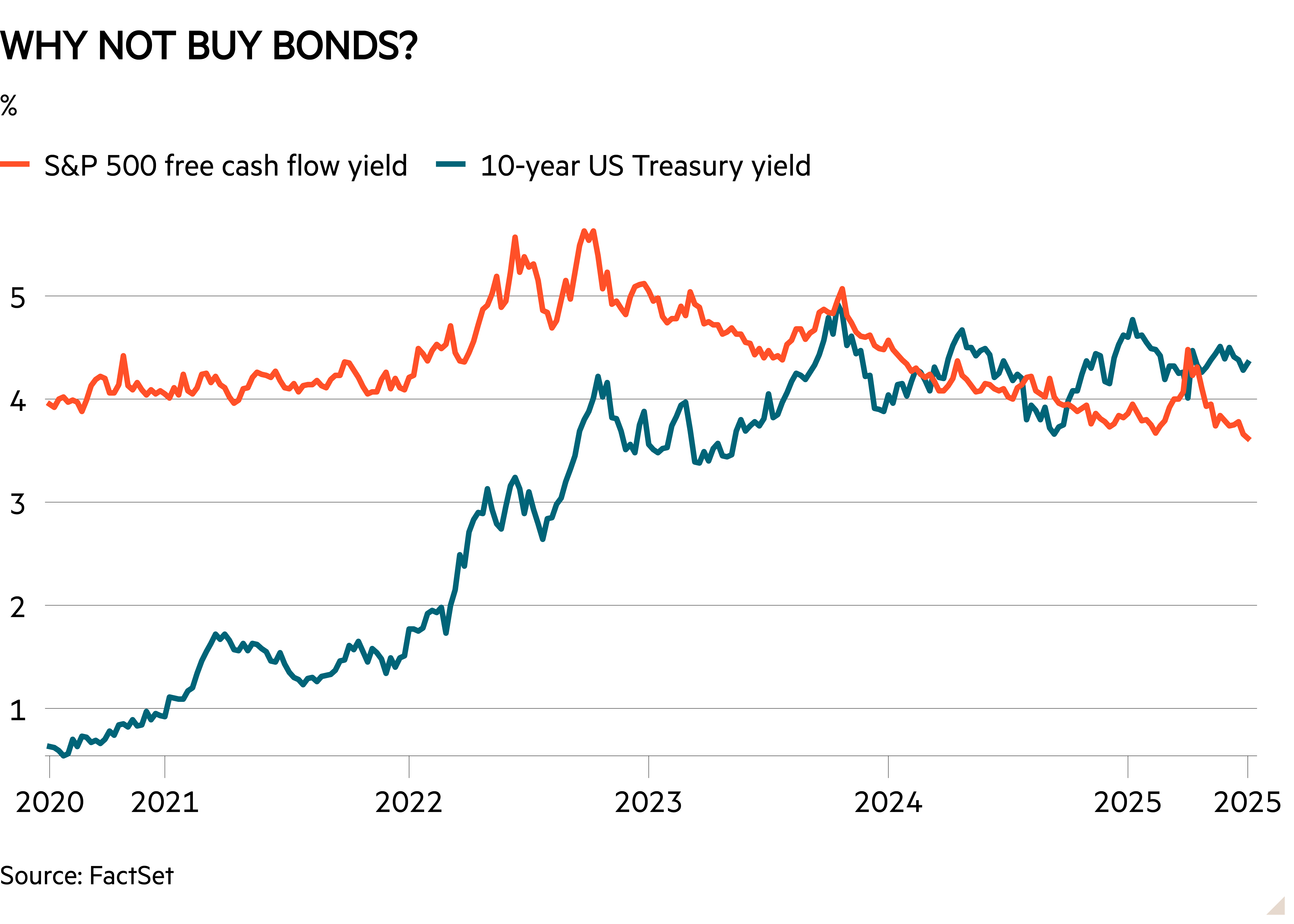

One way to estimate a stock’s expected return is to look at free cash flow yields. As the chart shows, at the start of 2020 the S&P forward free cash flow yield was 3.5 percentage points higher than the 10-year Treasury yield. This gap is expected: investors should be compensated for stocks’ greater risk with higher returns. The odd thing in the past few years is that the gap closed rapidly and, as with the gap between earnings yields and bonds, is now in negative territory.

Too much crowding?

The reason for the exceptionally high stock valuations has been the concentration of the stock market around a few megacap companies: the Magnificent Seven and a few others such as semiconductor designer Broadcom (US:AVGO). In total, the 10 largest companies make up over 40 per cent of the S&P 500.

This has made it a very difficult market for active managers, who pride themselves on picking lesser-known stocks, to outperform the market. “All of that has essentially created a ‘bear market in diversification’ because every manager that has de-emphasised the Mag Seven has created negative relative performance,” notes Fine. “The valuation spread between large and small caps has exploded to 40-year highs.”

Graham, who believed in the cyclical nature of markets, would have been sceptical of those who say AI’s potential to structurally increase earnings over the coming decades means “this time is different”. In his view, all bull markets had “a number of well-defined characteristics in common”. These included a historically high price level, high price/earnings ratios, low dividend yields compared to bond yields and much speculation on margin. All of these could be applied to today, suggesting the top of the market is not too far away.

Don’t time the market

Market bubbles have formed around technology narratives in the past, such as the ‘Nifty Fifty’ enthusiasm for IBM (US:IBM) in the 1970s and the dotcom bubble at the turn of the century. For many investors, it took years to recoup losses.

Timing is less of an issue for value investors, because they plan to hold their positions for the long term. “When I invest in a business, I do this with the assumption that there is no exit in sight; it has nothing to do with how much it will re-rate”, says Fine.

To find ‘cheap’ stocks, value investors need to be contrarian. This often means looking for businesses where something has recently gone wrong. To protect against the risk of a company going bankrupt, they can limit the downside by seeking out companies with strong balance sheets.

There is a strategy known as ‘deep value’, which involves buying an extremely cheap stock on the brink of bankruptcy. However, most fund managers look for businesses that still have strong business models but might have gone temporarily astray for some reason. “We try not to overpay, but we still want stocks with a strong balance sheet, good free cash flow and growth prospects,” says Janus Henderson value portfolio manager Justin Tugman.

Graham suggested buying stocks that trade at “a reasonably close approximation to their tangible asset value – say, at not more than one-third above that figure”. This advice is a little dated, given the rise of software and the increasing confidence the market has in these intangible assets. But the spirit of the suggestions – to compare the valuation relative to the balance sheet as well as earnings – still holds.

Fine has invested in carmakers BMW (DE:BMW) and Subaru (JP:7270), which are under pressure from tariffs and increased competition from low-cost Chinese manufacturers such as BYD (HK:1211) yet still have strong balance sheets and impressive cash flow generation. After recent share price falls, both their free cash flow yields sit at around 10 per cent.

As this suggests, Fine is increasingly looking outside the US for stocks that meet his “value” demands. “Japan looks like one of the most attractive areas and most notably there are a bunch of really well run and good businesses to own in a market where valuations have been beaten down,” he says.

As well as Subaru, his Japanese investments include semiconductor equipment manufacturer JEOL (JP:6951). Its electron beam lithography machines create the photomasks needed to etch semiconductors. The company is essential to the manufacturing process, but trades on a forward price/earnings ratio of just 11, significantly below many of its European and American peers.

But while value investors are confident in the stocks they own, many can’t say how long it will take for them to rebound.

“We have gone through 10 years of zero-interest rate policy. Then it looked like we would be in a more normal environment and then we decided we were going to enter this trade war, which has thrown everything into the mixer,” says Ariel Investments’ Fidler.

How long can this go on?

The AI story could continue to drive market concentration, while many of Trump’s economic policies favour larger international companies. In the case of tariffs, if nothing else the biggest companies can more easily lobby for exemptions. On top of this, the recent US spending bill is regressive, with a historically large cut to government healthcare insurance spending. This will take money away from low-income households with higher marginal rates of consumption; not good for domestic consumer stocks.

Although Fidler is confident that value investing will be profitable in the long term, he admits that “in the short run anything can happen”. One strategy is to pick stocks that have the negative impact of the trade war already priced in. The largest position in the Ariel Mid Cap Value fund is toy maker Mattel (US:MAT). The owner of brands such as Barbie and Hot Wheels sold off in the wake of “liberation day” because it manufactures many of its toys in China, as well as Indonesia, Malaysia, Mexico and Thailand.

Mattel had previously “lost its way”, in Fidler’s words, but now it is concentrating on diversifying its supply chain and managing its costs. It is also successfully monetising its brands, most famously with the box office success of the 2023 Barbie movie. “We feel that Mattel has been unfairly penalised, but now it has found a way to utilise its brands in the digital age,” says Fidler.

A company does not always require negative news to be weighing on it to qualify as a value stock. Madison Square Garden Entertainment (US:MSGE) is the owner of the famous Madison Square Garden and has a long-term lease on Radio City Music Hall, both in Manhattan. Importantly, its free cash flow yield is 8 per cent. “The density of tourists means Billy Joel can play 40 Madison Square Garden shows in a row… there is an enormous margin of safety because of the valuation,” Fidler says.

Definitions of ‘value’ differ notably, to the extent that the Russell indices in the US allow stocks to sit in both growth and value benchmarks. Last month even saw Meta (US:META), Amazon (US:AMZN) and Alphabet (US:GOOGL) enter the Russell 1000 Value index, partly because their expected growth rates have fallen by more than that of the wider index this year. Even so, Russell continues to view all three as predominately growth stocks.

Many traditional value stocks are simply “not sexy”, notes Fidler, which nowadays also means they are often overlooked by the retail investors who make up an increasing portion of the market. In the first half of the year, retail flows into US shares and ETFs surged to a new high, reaching $155bn – the strongest first half on record, according to Vanda Research. Unsurprisingly, it was Nvidia and Tesla (US:TSLA) that were the most favoured stocks.

As a result, Janus Henderson’s Tugman says he often has to look for companies that operate in the “real economy” to find good value. One of his oldest and most successful holdings is Casey’s General Stores (US:CASY). It owns a chain of convenience stores, primarily serving rural and small-town communities in the Midwest, and has recently expanded into Texas. The business has been acquisitive, which has helped it generate roughly double-digit earnings growth in the recent past. “There has been a lot of consolidation in the US convenience store market, so it’s becoming a scarce asset,” he explains.

Is it the end of beginning?

The most famous value investors can’t always find opportunities, however. In recent years, Buffett has struggled to find “good businesses” at the right price. Berkshire Hathaway has grown so large that the only companies it can invest in to move the needle are other big businesses, which today are often trading at expensive multiples.

Instead, Berkshire Hathaway has increased its cash holding further in the past year.

However, Buffett, inspired by the lessons he learnt from Benjamin Graham, is still strongly supportive of the methods that grew Berkshire Hathaway to the position it has today and believes investors should always be looking for ways to deploy their cash.

This year saw the publication of Buffett’s final shareholder letter as chief executive, in which he continued to promote the importance of taking a long-term perspective. In 2024, Berkshire Hathaway made operating earnings of $47bn, but it chooses to exclude all capital gains on the stocks and bonds it owns, because the “year-by-year numbers will swing wildly and unpredictably”. Buffett reminded investors that his “thinking involves decades” and that “Berkshire almost never sells controlled businesses unless we face what we believe to be unending problems”.

If you take a long-term view, timing the market becomes irrelevant. It doesn’t matter about short-term fluctuations; to hold cash waiting for the right moment would mean giving up dividend returns. This is a point made by Graham in The Intelligent Investor, where he encourages readers to continue to invest whenever they have spare cash. Similarly, despite Berkshire’s growing cash pile, Buffett wrote that it would “never prefer ownership of cash-equivalent assets over the ownership of good businesses” because “paper money can see its value evaporate if fiscal folly prevails”.

Buffett has been a figurehead for value investing. He has argued that the only way to be successful is to research businesses in detail, understand them deeply and have the patience to resist market fluctuations.

With every year where momentum stocks outperform, the case for value stocks paradoxically strengthens. At some point, there must be a limit to the mindless growth of passive investing. The efficient market hypothesis argues that all markets are “informationally efficient” – meaning asset prices fully reflect all available information at any given time. But this is only true if people – or machines – are actively trying to process that information, rather than just following the crowd.

For Buffett, investors have an almost moral calling to try to allocate their capital efficiently. “One way or another, the sensible – better yet imaginative – deployment of savings by citizens is required to propel an ever-growing societal output of desired goods and services,” he wrote earlier this year.

In 2022, we were granted a peek into what could lie ahead – prior to the release of ChatGPT, the stock market sold off as interest rates started rising. In that year, the S&P 500 fell 18 per cent, whereas Berkshire Hathaway delivered 4 per cent returns.

There was once the belief that higher interest rates would force more discipline on the market. Whether by luck or design, the rise of AI has obscured that thesis. Value investors continue to wait for their time in the sun. They always knew they would have to be patient, but the surprise is quite how long the wait has been

Buying infrastructure funds – ‘cheap is not always cheerful’

Well-balanced infrastructure funds offer better prospects than high-yielding renewables funds, says Max King

(Image credit: Getty Images)

By Max King

The performance of the UK’s listed infrastructure funds continues to be dismal. The average dividend yield of the renewable energy sector is 8.9%, having spiked to an all-time high of 10.6% on 7 April, according to the Association of Investment Companies (AIC). The average yield of the infrastructure sector is 6.1%, having reached a record 6.8%. Weighted average discounts to net asset value (NAV) are 24% and 17.5% respectively.

Surely these are the sort of companies that investors should be buying as the market rotates away from growth to value investing, and from the US to the rest of the world? “Analysts believe that the pessimism is overdone,” said Annabel Brodie-Smith of the AIC. “There has been some corporate activity, shares are being bought back and assets realised.” Her view has since been partially vindicated with the higher-risk, higher-reward infrastructure funds prospering. Still, the lower-risk infrastructure funds continue to languish, as do renewables.

The subsidy trap of renewables

Renewables may not be as much of a bargain as they seem. While the companies claim the economic lives of their projects are up to 40 years, “many funds will see their subsidy revenues expire in 2032-2035, and these mechanisms are typically 60% of a fund’s annual income”, points out Iain Scouller at brokers Stifel. “Once the subsidies end, the revenues will be more volatile, as a higher proportion of revenues will be subject to market prices and the funds will lose the inflation linkage provided by current support schemes.”

Get 6 issues for £1 + a free notebook

Stay ahead of the curve with MoneyWeek magazine and enjoy the latest financial news and expert analysis.

The drop-off in subsidies is taken into account in asset valuations, but dividends are likely to be squeezed. These shares may prove a good investment for those who want to collect the high dividends, but the market is unlikely to favour companies with a visible sword of Damocles hanging over them. There are other risks as well. Power prices could fall. New technology could make existing projects obsolete. Costs of maintaining equipment could rise. A future government could recoup the subsidies via tax. So Scouller’s lukewarm recommendation is probably fair.

Better prospects in the infrastructure sector

Sentiment in the general infrastructure sector was given a boost in February by the all-cash bid for BBGI Global Infrastructure at a premium of 3% to NAV (and 21% to the prevailing share price). The share prices of HICL Infrastructure (LSE: HICL), InternationalPublic Partnerships (LSE: INPP), 3i Infrastructure (LSE: 3IN)and Pantheon Infrastructure (LSE: PINT)have since revived.

BBGI invested in low-risk public-private partnership (PPP) concessions of limited life. The rest of the sector has moved steadily away into demand-based assets – these are higher risk, but also offer higher returns. The share prices of INPP and HICL, still with significant PPP exposure, offer a slowly rising dividend yield of more than 7%, plus the promise of modest capital growth.

3IN and PINT offer a lower yield of roughly 4%, but target total returns of 8%-10%. PINT returned a remarkable 14% last year from a portfolio invested 44% in digital infrastructure, 29% in power and utilities and 16% in renewables and energy efficiency. However, 3IN returned a lesser 5.1% in the six months to 30 September, held back by adverse currency movements. Its portfolio is 42% in energy transition, 22% digitalisation, 22% essential infrastructure, 8% demographic change and 6% oil storage.

So while investors may be tempted by the high yields and high discounts to NAV of the renewable-energy funds, the opposite end of the spectrum looks more attractive. PINT and 3IN, which are still on discounts of over 10%, offer better long-term prospects. As so often in investment, cheap is not cheerful.

This trust’s dividend has beaten inflation for a decade – but its share price needs a boost

Schroder has been in our portfolio since 2016, and we’d buy it all over again

Robert Stephens 18 July 2025

Questor is The Telegraph’s stock-picking column, helping you decode the markets and offering insights on where to invest.

The FTSE 100 is in the midst of a record-breaking year. After posting desperately poor returns for what felt like an eternity, it has made several new all-time highs during 2025.

Indeed, it appears as though investors are finally beginning to realise that a globally-focused index that trades at a discount to its peers is likely to be a worthwhile prospect.

Of course, the chances of the FTSE 100 posting further record highs may seem somewhat distant amid an ongoing global trade war that could yet heat up after an extended pause.

This may prompt many investors, particularly those seeking a reliable income, to determine that now is an opportune moment to exit UK large-cap shares while they trade at more generous price levels vis-à-vis their recent past.

In Questor’s view, though, long-term income investors are being more than fully compensated for the heightened risk of elevated volatility over the coming months. The index, for example, offers a dividend yield of 3.4pc – this is 2.8 times that of the S&P 500.

The FTSE 100 also remains cheap relative to other major large-cap indices, with many of its members offering significant long-term capital growth potential, as well as dividend growth, amid the current era of monetary policy easing that is taking place across several developed economies.

Therefore, sticking with UK-focused investment trusts such as Schroder Income Growth could prove to be a sound long-term move. It has an excellent track record of dividend growth, with shareholder payouts having risen in each of the past 29 years.

Given the scale and variety of geopolitical challenges experienced in that time, it seems to be well versed in overcoming periods of heightened uncertainty.

The company’s dividends, furthermore, have increased at an annualised rate of 11.3pc over the past decade. This is 50 basis points ahead of annual inflation over the same period, thereby meaning the trust has met its aim to provide positive real-terms dividend growth. And with a dividend yield of 8pc, it offers a substantially higher income return than the FTSE 100 at present.

The company also has a solid long-term track record of capital growth, thereby meeting the other part of its aim. Its net asset value (Nav) per share has risen at an annualised rate of 11.3pc over the past five years.

This is 50 basis points ahead of the FTSE All-Share index, which is the company’s benchmark. Given that its shares currently trade at an 8pc discount to Nav, they appear to offer good value for money and scope for further capital gains over the long run.

Of course, a gearing ratio of around 11pc means the trust’s share price is likely to be relatively volatile, especially given the aforementioned elevated geopolitical risks.

However, given Questor is highly optimistic about the stock market’s long-term growth potential, leverage is likely to prove beneficial to overall returns in the coming years.

A glance at the weightings of the trust’s major holdings may also suggest relatively high share price volatility lies ahead. After all, its five largest positions account for 28pc of total assets, with its portfolio amounting to a relatively limited 45 holdings.

However, given the FTSE 100’s five largest members account for 31pc of its market capitalisation, this column is not overly concerned about the trust’s concentration risk.

Moreover, well-known FTSE 100 stocks that are fundamentally sound dominate its major holdings. They include AstraZeneca, Shell and National Grid, with the trust adopting a bottom-up approach that seeks to identify market mispricings when selecting stocks.

Since being added to our income portfolio all the way back in December 2016, Schroder Income Growth has produced a capital gain of 18pc.

Although this is four percentage points behind the FTSE 100’s rise over the same period, which is undoubtedly disappointing, there is scope for index-beating performance as its current discount to Nav likely narrows, the benefits from sizeable gearing in a rising market become more apparent and its focus on fundamentally sound firms catalyses its performance.

As well as offering capital return potential, the trust remains a worthwhile income purchase. Its relatively high yield, potential to deliver inflation-beating dividend growth and excellent track record of consistently rising shareholder payouts more than compensate investors for what could yet prove to be a highly volatile and uncertain second half of 2025.

Questor says: buy Ticker: SCF Share price at close: £3.12

Broke Britain: what it means for investors The Office for Budget Responsibility’s latest fiscal risks report makes for bleak reading – and investors shouldn’t ignore it.

Higher gilt yields beckon, along with higher taxes.

The argument for overseas investing has grown stronger – despite the government’s protestations that it wants to see more people invest in UK shares. Wednesday, 16th July 2025

Dear Fellow Fools,

Macroeconomics is a dry subject. With two degrees in economics – or three, depending on how you’re counting – I can truthfully say that macroeconomics is the branch of economics that I liked least.

But sometimes, even the driest subject comes alive. And right now, we’re unfortunate enough to be living in a macroeconomic experiment which is making for very interesting times indeed.

All of which I mention because what’s going on has a direct impact on all of us as investors.

Bleak assessment July 8 saw the publication of the Office for Budget Responsibility’s latest fiscal risks report. It didn’t pull any punches

The general thrust (and here I’m quoting pretty much verbatim from the report):

The UK’s public finances have emerged from a series of major global economic shocks in a relatively vulnerable position.

The UK now has the sixth highest debt, fifth highest budget deficit, and the third highest borrowing costs among 36 advanced economies.

Efforts to put the UK’s public finances on a more sustainable footing have met with only limited and temporary success in recent years.

The result has been a substantial erosion of the UK’s capacity to respond to future shocks and growing pressures on the public finances.

Against this more challenging domestic and global backdrop, the scale and array of risks to the UK fiscal outlook remains daunting.

How we got here Now, bodies such as the Office for Budget Responsibility don’t use words like ‘daunting’ and ‘vulnerable’ lightly. Nor does it lightly warn of ‘a substantial erosion of the UK’s capacity to respond to future shocks’. This is serious stuff.

George Osborne’s and David Cameron’s era of austerity was unpopular. But it did keep a fairly tight rein on the public finances. And successive governments since have failed to replicate anything like that. Public sector debt has ballooned.

And the present government – which is of a very different political hue, remember – so far appears to be keeping even less of a grip on the public finances. It talks tough, but caves when pressed.

Look at the facts. It has foresworn tax rises. Made massive new spending commitments in areas such as defense and healthcare. Failed to get much-needed spending cuts through parliament, as we saw with the latest welfare climbdown, and the climbdown over the Winter Fuel Allowance. And refused to tackle expensive liabilities such as the so-called ‘triple lock’ on the state pension.

To stress, I’m not making a political point here, but an economic one. Once, the government might have hoped for GDP growth or improvements in productivity to help it out of its hole. But productivity growth is anaemic, and economic growth has been negative for the last two quarters – and this with a government that placed economic growth at the top of its priorities.

Things simply don’t add up.

Threats and opportunities So where are we heading? And what does it mean for investors? Here’s my take on it.

First, the already-nervous bond market is going to become even more nervous, unless things change – which, as the Office for Budget Responsibility points out, they’ve shown no sign of doing. Worse, the Office for Budget Responsibility is forecasting that pension funds will sharply reduce their gilt holdings in the years ahead, and so gilt yields will have to rise in order to entice foreigners to hold them. UK long-term gilt yields are already higher than they’ve been in the last 25 years, but expect them to climb higher.

That’s good news for income investors, of course, but it also raises the cost of the government’s debt interest. And to the extent that gilt rates drive interest rates in the broader economy, things don’t auger well for business sectors that do best in low interest rate environments. Which is quite a chunk of the economy, when you think about it.

But other countries – and other economies – may, and probably will, have different interest rate environments, and very different GDP growth and productivity environments. Right now, UK shares are cheap on a price-earnings basis, but overseas shares may offer better growth prospects. Not to mention better relative asset prices, going forward, if sterling depreciates. Should you buy UK – or look elsewhere? It’s a very valid question. The government has a view – but isn’t delivering the economic backdrop to support it.

What about taxes? Well, the Labour party campaigned on a pledge not to raise taxes for working people, and Rachel Reeves stated firmly in the autumn that there would be no more tax rises. But how about imposing a tax that doesn’t already exist? Hence the talk of a wealth tax. It won’t be politically popular – but relatively few voters will be affected, unlike continuing the present freeze on tax thresholds.

Raising Capital Gains Tax rates is a distinct possibility, too. Unpopular again, but only with relatively fewer voters – and critically, arguably not ostensibly raising taxes for ‘working people’.

What to do in such a taxation regime? ISAs and pensions offer some relief, and you could always move abroad – as, apparently, people are. But talk to advisers to the wealthy, and you’ll also hear plenty of talk of trusts, family investment companies, gifting assets early to beat inheritance tax, and tax shelters such as Venture Capital Trusts. Sangria in the sun sounds attractive it, but there are alternatives.

We have been warned So there we have it. I’m aware that this is a Collective column that is a little out of the ordinary, but so too was the report from the Office for Budget Responsibility. And so too, it must be said, is the state of the nation’s finances.

Again, to stress, I’m not making a political point here, but an economic one – and the assessment isn’t mine, but that of the Office for Budget Responsibility.

But the takeaway is clear: hard times, and tough choices, lie ahead. And building wealth – and, critically, keeping hold of it – has rarely been more important.

Until next time,

Malcolm Wheatley Investing Columnist, The Motley Fool UK

Dr James Fox takes a closer look at an alarming trend in the Far East that could have consequences for investors around the world.

Posted by Dr. James Fox

Published 17 July

Image source: Getty Images

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Japan’s bond market is making headlines again and it could have major implications for stock market investors worldwide.

Bond yields have surged to multi-year highs as the Bank of Japan (BOJ) winds down years of ultra-loose monetary policy.

Once known for rock-bottom yields, Japanese government bonds (JGBs) suddenly offer competitive returns.

As I write, here are the yields and changes (in basis points) in JGB. Rising yields indicates less demand for government debt and will mean government debt becomes more expensive to service.

Bond maturity

Yield (%)

Change (1 month, bp)

Change (1 year, bp)

2-year

0.79

+3.4

+47.7

5-year

1.09

+7.1

+52.3

10-year

1.59

+13.9

+56.8

20-year

2.63

+24.7

+77.5

30-year

3.17

+26.2

+100.5

Why should investors care?

So, why should investors in the UK care? Because the consequences of a Japanese debt crisis could be global. And that may hit stock markets right where it hurts.

For decades, Japan’s low rates powered the ‘yen carry trade’, fuelling equity rallies abroad — including in US tech stocks — as investors borrowed cheaply in yen and ploughed the proceeds into riskier, higher-yielding assets overseas.

But as Japanese yields spike, those investors may start repatriating huge sums back to Japan as the equation shifts. That could mean dramatic outflows from global stock markets, especially in areas most exposed to foreign capital.

What’s more, Japan’s debt burden is now exceptionally high, with its debt-to-GDP ratio above 260%, the highest in the developed world (although Japanese net debt is lower).

Confidence in the stability of Japanese government bonds is being tested and that could spread to other nations with increasingly unsustainable debt… like the UK.

If a crisis of confidence erupts, that could roil not only Japan’s economy but send shockwaves through equity markets globally.

Should investors panic? No. But it’s certainly a concern. Investors with heavy holdings in markets like the US or global tech should keep a watchful eye on Japanese bond developments.

As previously guided, the Company is transitioning to a dividend aligned with project cash flows and EBITDA. Based on the latest analysis, which reflects the 6-month delay in several new assets coming online and no increase in base merchant revenues from the last 12 months, the Board’s dividend guidance is:

§ 3p special dividend.

§ 0.75p per share per quarter commencing with the quarter ending 30 September 2025 and continuing through FY26/27, with potential for higher dividends during that period if merchant revenue improves.

The fcast yield falls to around 5%, so GSF leaves the Watch List today. If you hold you may wish to hold until the special dividend of 3p, paid in two tranches this year is paid, or you may not.

Hey there would you mind sharing which blog platform you’re working with? I’m looking to start my own blog in the near future but I’m having a difficult time selecting between BlogEngine/Wordpress/B2evolution and Drupal. The reason I ask is because your layout seems different then most blogs and I’m looking for something unique. P.S Sorry for being off-topic but I had to ask!