Heya are using WordPress for your site platform? I’m new to the blog world but I’m trying to get started and create my own. Do you need any html coding expertise to make your own blog? Any help would be really appreciated! https://keslaser.com.ua/vodinnya-v-doshch-i-tuman-yake-svitlo.htm

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

The content of this article is provided for information purposes only and is not intended to be, nor does it constitute, any form of personal advice.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Turning excess savings into a second income can be a very good idea. Even for someone starting from scratch, it’s possible to earn some good returns with enough time.

As things stand, someone in the UK aged 30 has 38 years before becoming eligible for the State Pension. And that’s a long time to build up an investment portfolio.

Should you buy Supermarket Income REIT plc shares today?

Property

Historically, property has been a very good source of extra income for UK investors. But higher taxes and greater regulation have made things more complicated in recent years.

Enter real estate investment trusts (REITs). These are companies that own and lease properties (which might be hospitals, offices, warehouses, or other buildings) to tenants.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

In exchange for tax exemptions, REITs return 90% of their income to shareholders as dividends. And this gives investors a different way to earn income by investing in property.

There’s been a lot of interest in the UK REIT sector recently in terms of takeovers and acquisitions. But I think there are still some opportunities that are worth checking out.

Supermarkets

When it comes to leasing buildings, supermarkets probably aren’t the first type of property that people think of. But Supermarket Income REIT (LSE:SUPR) is worth a closer look.

As its name suggests, the company leases a portfolio of around 55 supermarkets across the UK. And its largest tenants include Aldi and Lidl as well as Tesco and Sainsbury.

The nature of the grocery market means the firm’s tenant base is relatively concentrated. While its rent collection metrics are impressive, investors shouldn’t overlook this risk.

A 7.85% dividend yield, however, goes some way to offsetting the risk. And investing regularly at that rate of return for 38 years can have some impressive results.

Regular investing

Investing £100 each month for 38 years and earning a 7.85% annual return results in a portfolio that generates £19,293 a year. Starting from nothing, I think that’s a strong result.

The situation with Supermarket Income REIT might be even better. Since the majority of its leases are linked to inflation, investors might expect an extra 2% in annual rent increases.

There is, however, no guarantee the stock will trade with a 7.85% dividend yield every month for the next 38 years. If the share price rises, the equation could look very different.

In that case, investors aiming to turn £100 a month into something that eventually returns £19,293 a year would need to look elsewhere. But that might not be such a bad thing.

Diversification

One of the benefits of regular investing is it allows for gradual diversification. Over time, different stocks come in and out of fashion for various reasons.

Buying each month should give an investor a chance to take advantage of different opportunities as they present themselves. And this creates a diversified portfolio over time.

For someone starting from scratch, buying shares and reinvesting dividends could be a good long-term strategy. And I think REITs are a good place to start looking for opportunities.

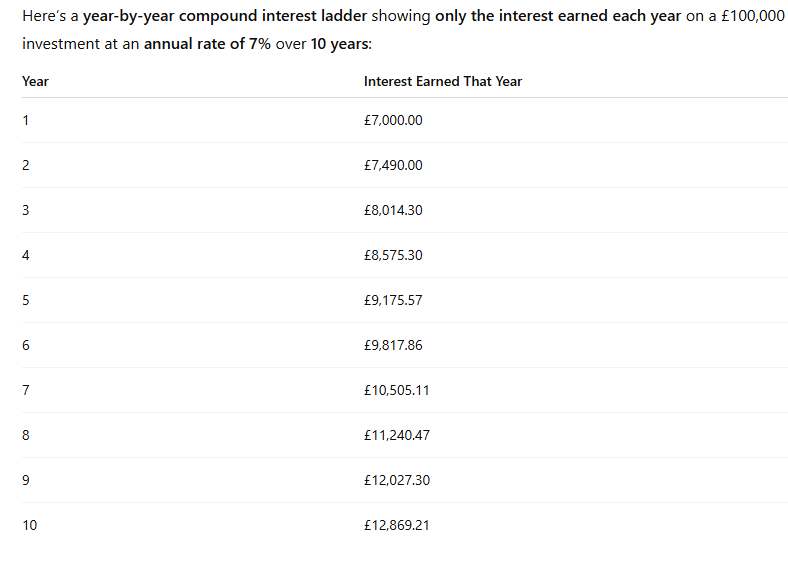

Investing £100 monthly for 38 years at a 7.85% annual return builds into something quite powerful thanks to compound interest. Let’s break it down: 📈 Investment Summary

Monthly contribution: £100

Duration: 38 years

Annual return: 7.85% (compounded monthly) 💰 Final Value Estimate Using monthly compounding, your investment would grow to approximately: £291,000

Equity markets could make investors nothing in the next 10 years, warn managers

19 September 2025

Downing’s Simon Evan-Cook and Orbis’ Alec Cutler explain why investors should be wary of a downturn.

By Patrick Sanders

Reporter, Trustnet

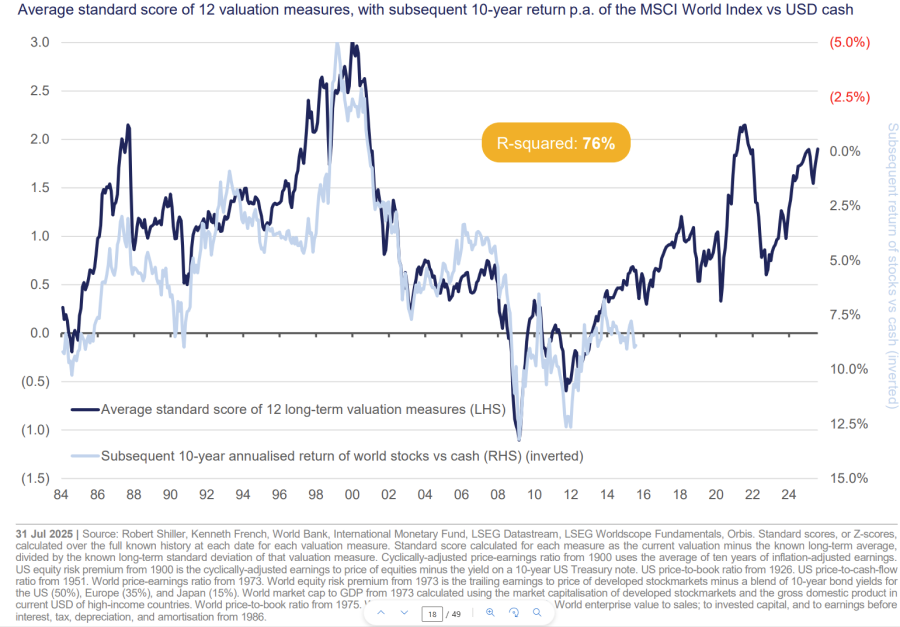

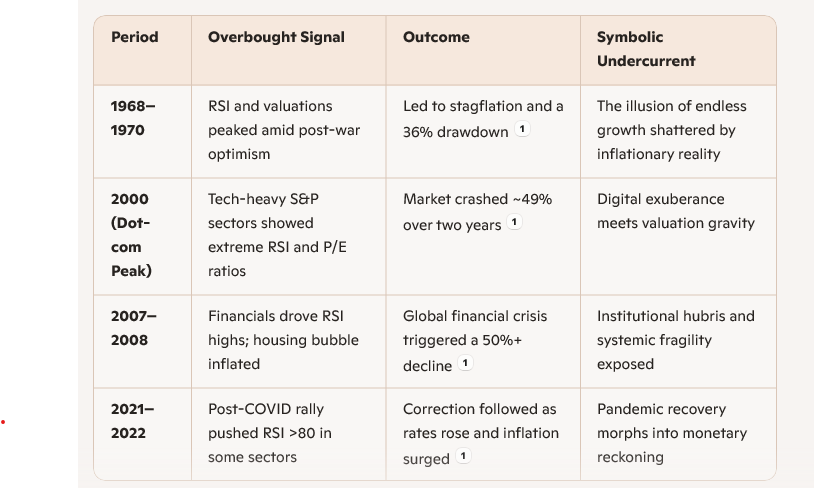

Equity markets have posted stellar returns over the past decade but extreme valuations and historical precedent indicate that this could be about to reverse, according to managers.

“People seem to think that equities are guaranteed a positive return. They aren’t. They could absolutely make zero in the next 10 years,” he said.

It seems “realistic” that equity markets deliver nothing or even lose money, thanks to the dominance of US stocks, which make up roughly 70% of the MSCI World index.

Since 2011, the S&P 500 has delivered a “spectacular” average yearly return of 14%, but this is based on unsustainable expectations, according to Cutler.

“To produce 14% again, you need valuations to go from already extreme 24x [price-to-] earnings to almost 40x earnings. You need corporate earnings, profit margins and valuations, which are near record highs, to increase further,” Cutler concluded.

The far more likely outcome is that the US equity market corrects and drags the rest of the global market down with it, he said. The average annual return of the S&P 500 is around 7%, so to return to that level, equity markets would post an average return of zero for “at least the next 10 years”.

This may sound absurd, he noted, but it has happened before. The chart below shows the average expected return on equities over 10 years, from different market valuations.

Source: Orbis Investments

“If you look back in history as far as you can get, whenever we’ve been at this level of valuation, markets returned zero over the next 10 years,” the Orbis manager explained.

On top of this, the US government’s “financial mismanagement” in relation to escalating debt levels and investors pulling out of American markets (both bonds and equities) could lead to a weaker dollar. This in turn could fuel further capital exodus from the country, sparking a US downturn.

“I would not be shocked if you get a 0% return from the global equity market from here,” he concluded.

Simon Evan-Cook, fund of funds manager at VT Downing Fox, agreed that this is a realistic concern. “There’s no God-given right that equity markets will go up every year, let alone to go up for another 15 years in a row,” he said.

While the past decade has been “mostly sunshine and rainbows” for global equities, strong performance is causing investors to develop “worrying” assumptions.

For example, many investors have concluded that active funds are no longer needed due to their underperformance compared to a surging global equity tracker.

“I completely understand why some people are asking themselves if they need an active fund, given that any attempt to do anything different has underperformed,” the Downing Fox manager said.

However, he warned that these assumptions were also around in the 1990s and backfired on investors as, in the following decade, the average global equity tracker “made you nothing”, Evan-Cook explained.

Performance of funds post 2000

Source: Downing Fox. Total return in sterling

The tech bubble collapse in 2000 was due to the high concentration of US equities, which had outperformed and become overvalued. When they corrected, they represented 50% of the global market and so dragged most portfolios down.

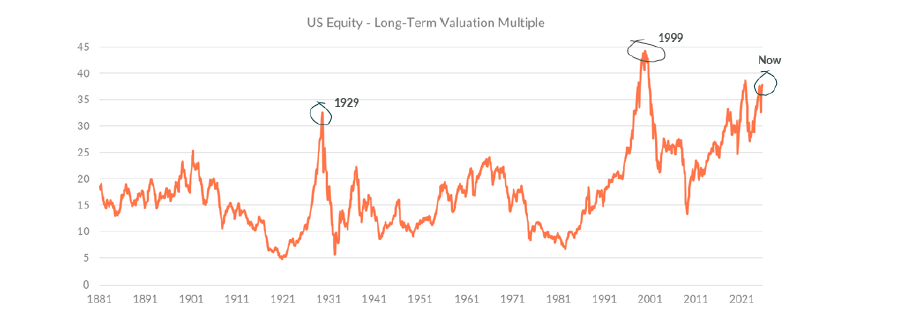

As Evan-Cook noted, while current valuations are not at the 1999 peak, they are approaching it. And global markets have become even more dominated by the US than they were 25 years ago.

If North America stocks re-rate, the resulting crash might look closer to the Nifty 50 downturn in the 70s, he suggested.

Long-term valuations of US Equities

Source: Downing Fox. CAPE Ratio, January 1881 to August 2025.

“Hence why it’s not outrageous to suggest that something as apparently reliable as a global tracker could go a long time without making money,” he said.

Not even the most popular stocks on the market would be immune. For example, in 2000, some investors thought Amazon would thrive due to the emergence of the internet, while others thought it was overvalued and heading for a fall. “Both investors would have been absolutely correct,” Evan-Cook noted.

Amazon shed almost 92% of its value between 2000 and 2005, but those that sold missed the rebound, he explained. This could happen again to some of the biggest stocks in the index, “despite how transformative things like artificial intelligence are”.

“Broadly, equity markets do go up over time”, Evan-Cook said “, but they can spend long periods of time that matter to investors going sideways or down. That’s a real risk right now.”

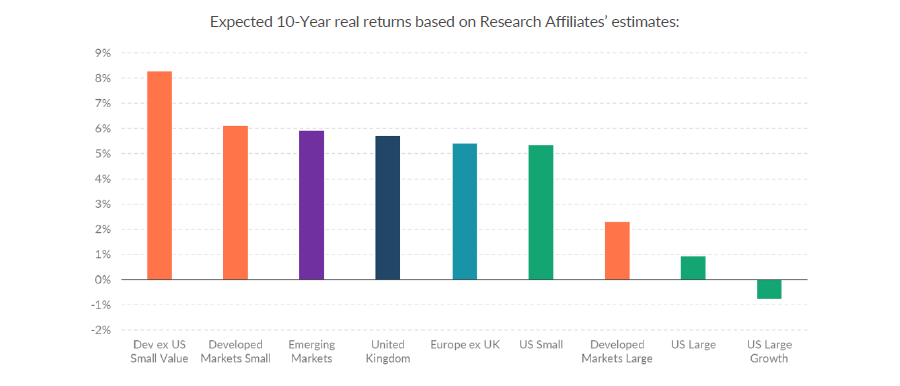

However, he said this is mostly a risk for global equity trackers and US mega-caps, with the outlook outside of US blue-chips being much more positive, as seen in the chart below.

Expected 10-year returns of equity markets

Source: Downing Fox. Research Affiliates.

Maybe prudent to have part of your portfolio in dividend paying shares ?

Here’s a 7-share passive income portfolio investors should consider over cash savings

Discover how holding a diversified range of UK dividend shares could generate a strong and stable passive income over time.

Posted by Royston Wild

Published 20 September

Image source: Getty Images

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

The content of this article is provided for information purposes only and is not intended to be, nor does it constitute, any form of personal advice. Investments in a currency other than sterling are exposed to currency exchange risk. Currency exchange rates are constantly changing, which may affect the value of the investment in sterling terms. You could lose money in sterling even if the stock price rises in the currency of origin. Stocks listed on overseas exchanges may be subject to additional dealing and exchange rate charges, and may have other tax implications, and may not provide the same, or any, regulatory protection as in the UK.

By some distance, Brits still prefer to hold cash on account for a passive income than to put their money in shares. To prove my point, latest data showed that 7.9m adults currently hold a Cash ISA, more than double the number that have a Stocks and Shares ISA (3.8m).

Given the spike in interest rates after 2021, it’s not a shock to see cash accounts have gained popularity. But with the Bank of England slashing their lending rates, continuing to prioritise savings over investing in the stock market could be an expensive mistake.

Should you buy Chelverton UK Dividend Trust PLC shares today?

Better returns

Investors have to balance risk and reward when deciding where to put their cash. And there’s no right or wrong answer, as it depends on each individual’s investment goals and risk tolerance.

But I prefer to put the lion’s share of my capital in dividend-paying stocks. By investing in a wide range of companies, too, I can mitigate the riskier nature of share investing versus saving, and chase a strong return without putting my money in too much danger.

Even if rates remain unchanged at 4%, the superior passive income that’s on offer from UK shares make stock market investing a ‘no brainer’ for me.

Seven dividend stars

Here’s a mini-portfolio of seven UK stocks investors could consider putting their spare cash in:

Dividend share

Sector

Dividend yield

M&G

Financial services

7.9%

Greencoat UK Wind

Renewable energy

9.8%

HSBC

Banking

4.8%

Persimmon

Housebuilding

5.5%

Target Healthcare REIT

Real estate investment trusts (REITs)

6.2%

Pennon Group

Utilities

6.6%

Chelverton UK Dividend Trust

Investment trusts

8.6%

The average dividend yield across these shares is 7.1%, which is triple the average interest rate of 2.3% that savers currently enjoy. Dividends aren’t guaranteed, but assuming these companies meet brokers’ forecasts — and can print a 3% average share price rise, too — I could enjoy a total annual shareholder return north of 10%.

Spread across 73 different companies, this mini portfolio could help protect investors against regional-, industry-, or company-specific shocks. The Chelverton UK Dividend Trust is especially effective in delivering this diversification.

The trust’s objective is “to deliver a high and growing income through investments in mid to small-cap companies exclusively outside the largest 100 UK stocks“. Concentrating on non-FTSE 100 stocks comes with greater risk, but it also provides the potential for superior rewards.

Besides, with investment in 66 different businesses across 20 different sectors, risk is still pretty well spread, in my opinion. Chelverton’s record of 14 straight years of dividend increases illustrates this robustness.

My plan

I’m not saying that investors should consider avoiding cash accounts altogether. I myself hold money in savings to diversify my broader portfolio and provide access to emergency cash.

But, for me, the best way to target a life-changing passive income is by putting most of my spare capital in dividend shares.

Whenever the stock market hits a rough patch, investors often start nervously eyeing their portfolios. After all, there’s nothing more unpleasant than seeing investments crash in value.

So capitalising on these can propel portfolios to new heights, potentially opening the door to an earlier retirement.

The power of a crash

Let’s take a trip down memory lane and explore the stock market at the height of the pandemic. When lockdowns were put in place, shares around the world tumbled. And here in the UK, even the FTSE 100, which has historically been quite resilient, dropped sharply by around 30% in March.

Yet those with their eye on the long term could have used this sudden drop to start snapping up shares at a massive discount. And even when relying on passive index funds, the results would have been tremendous.

The extra gains generated from investing during a volatile market environment have made a massive difference, even for investors following a strategy as simple as drip-feeding £500 into an index fund each month.

If you buy an index tracker and as long as you can choose when to sell, you will not lose any of your hard earned, it could be multi years though.

To buy when markets are week, you either need a safe part of your Snowball that you can sell, new funds to add to your Snowball, or dividends to re-invest at sale prices.

The Market is the only place where customers run out of the Store when there is a sale on.

Gilts are bonds issued by the UK government. In recent years, they have become increasingly attractive to individual investors due to increasing interest rates and tax efficiency.

What are gilts?

Gilts are a type of government bond. When you buy a gilt, you effectively lend money to the UK government in exchange for periodic interest payments (coupons) and the return of your initial investment (the principal) when the bond matures.

UK government bonds are known as ‘gilts’ because their past paper certificates had gilded (golden) edges. The name also reflects their security and reliability, as the UK Government has never failed to make repayments.

Key features of gilts:

Issued by the UK government – Issued by the UK government, gilts are generally considered safe investments. The UK government has solid investment grade credit ratings of Aa3, AA-, and AA from Moody’s, Fitch, and S&P respectively.

Fixed interest payments – gilts pay a fixed rate of interest that is set at the inception of the bonds. These payments are known as ‘coupons’. The interest payments are typically made every 6 months.

Different maturities – Maturity is the time when the bond has come to the end of its life and the investor receives their money back. This ranges from a few years to several decades.

Traded in the market – meaning their prices can go up or down.

Return of principal at maturity – the issuer (HM Treasury) issues gilts with a promise to return your capital at maturity.

Low risk: Since they are issued by the UK government, gilts are considered very safe.

Tax benefits: Capital gains from gilts are not taxed, making them attractive for investors.

Predictable returns: You know how much you will receive at maturity, and can see a schedule of period interest (coupon) payments.

Liquidity: Gilts can be easily bought and sold in the market.

Cons:

Low returns: Compared to stocks or corporate bonds, gilts usually offer lower potential profits.

Interest rate risk: Buying a gilt at a 3.75% yield may seem attractive now, however, if interest rates were to rise you would be locked into a lower rate. This causes investors to sell legacy gilts with lower rates and can lead to their prices falling.

Inflation risk: Like all investments, inflation will eat away at the real value of returns. For example, if a gilt is yielding 4%, and inflation is 2%, the real return is 2%.

Why is now a good time to buy gilts?

This presents an opportunity for individual investors to buy them at a discount, and benefit from their tax-free capital gains when they mature.

For example, take a gilt maturing in 2026 with a low coupon of 0.125%:

It is currently trading at a discount (<100).

The taxable income component of its return (0.125%) is negligible.

When it matures, the price will return to its full value (100), giving you a capital gain.

Since this gain is considered capital rather than income, the bulk of the yield is tax-free, making it very tax-efficient.

This tax advantage makes low coupon gilts an efficient way to earn returns, especially for higher-rate taxpayers.

Comparing gilts to other investments

Gilts vs. Corporate Bonds: Corporate bonds often offer higher yields, but they come with more risk as companies can default. Generally speaking, corporate bonds will have higher coupons, as such they are more commonly held within ISA wrappers.

Gilts vs. Stocks: Stocks are more volatile than gilts, and provide less capital protection. However, they have higher expected returns, which minimises the risk of not receiving a required return target. Stock market index trackers can be a solid choice for investors looking to maximise long-run returns, especially if held within an ISA wrapper.

Gilts vs. Cash Savings: Cash savings provide the greatest protection of capital (providing for the FSCS limit). Further, flex savings accounts can be accessed on demand without needing to sell a bond at the prevailing market price. However, cash savings are income products (taxed at your income tax rate), making the rates available less competitive if held outside a tax wrapper.

Who should invest in gilts?

Gilts may be suitable for you if:

You want a safe and predictable investment.

You are looking for tax-efficient ways to invest, especially outside of a tax wrapper such as an ISA

You need to preserve capital.

You prefer stability over risk.

You are looking for a hedge against stock market volatility.

How to invest in gilts

You can buy gilts through a broker, most investment platforms will offer gilts. You can also gain exposure to gilts through pooled products such as ETFs, however, pooled products will not be subject to the same tax treatment (free of capital gains tax).

Steps to buying gilts:

Determine your investment objectives – Why are you investing? Will you need your money back in a year, or a few years? How much will you need to earn to meet your objective? Your investment objectives will help you narrow down a suitable range of gilts.

Choose a platform – Open an account with an investment platform or broker.

Review tenors and yields – Check the current market yields for gilts with different tenors (the length of time until they are repaid). Choose a gilt that matches your investment goals.

Place an order – Buy directly through your chosen platform.

Conclusion

Gilts have become an attractive investment for individuals due to recent economic changes and their tax efficiency. While they may not offer the highest returns, they provide a safe and predictable way to grow your money, especially in uncertain times.

Key takeaways:

Gilts are low-risk government bonds suitable for conservative investors.

They offer tax benefits, making them efficient, especially for higher-rate taxpayers.

The current market environment makes discounted gilts a unique opportunity.

While they are safer than stocks or corporate bonds, they have lower return potential.

Gilts are easy to buy through brokers, such as WiseAlpha.

If you are a higher or additional rate tax-payer looking for a low-risk investment that can help preserve and grow your wealth with high levels of tax efficiency, gilts might be worth considering.

Before investing, always review your financial goals and consult a professional if needed.

How Does the Stock Market React to Interest Rate Cuts?

Below, we show how the S&P 500 has performed after the first rate cut over the last five decades:

Year of first rate cut

Three months

Six months

One year after

1973

-10.2%

-6.2%

-36.0%

1974

-14.7%

-15.3%

+7.5%

1980

+15.0%

+28.9%

+30.3%

1981

-11.0%

-7.9%

-17.8%

1982

-4.8%

+17.4%

+36.5%

1984

-1.2%

+7.2%

+10.5%

1987

+0.1%

+1.7%

+7.5%

1989

+7.4%

+7.5%

+11.9%

1995

+5.1%

+8.0%

+13.4%

1998

+17.2%

+26.5%

+27.3%

2001

-16.3%

-12.4%

-14.9%

2007

-4.4%

-11.8%

-27.2%

2019

+3.8%

+13.3%

+14.5%

Average

-1.1%

+4.4%

+4.9%

Historically, the S&P 500 returns 4.9% on average one year after the first interest rate cut, seeing positive returns nearly 70% of the time.

In the three months following a rate cut, the market often dips, but typically rebounds by the six-month mark. This aligns with conventional wisdom that lower interest rates stimulate economic activity by reducing borrowing costs for businesses and consumers, which tends to benefit the stock market.

However, S&P 500 performance following rate cut cycles can vary significantly. For instance, U.S. equities saw double-digit declines after the first rate cuts in 1973, 1981, 2001, and 2007. On the other hand, the S&P 500 surged 36.5% one year after the 1982 rate cut cycle. In the most recent rate cut cycle, the S&P 500 jumped by 14.5% in the following year.

In this way, interest rate cuts don’t show the whole picture. Instead, positive earnings growth may offer a more reliable indicator of S&P 500 performance in the following year. When earnings growth is positive, the market averages 14% returns one year after. In contrast, when earnings decline during periods of falling interest rates, the S&P 500 increased by 7%, on average.

Veroni App

📈 Yes, the S&P 500 is showing signs of being overbought as of mid-September 2025. Here’s what’s happening:

14-day RSI peaked at 76 in July, which is well above the typical overbought threshold of 70.

Market breadth is narrowing—only a small group of large-cap stocks (especially the “Magnificent Seven”) are driving the rally, while broader participation has faded.

Volatility risks are rising, with technical analysts warning of a potential correction due to systemic overvaluation and divergence from equal-weighted indices. Even though the index is hovering near all-time highs, the underlying structure looks fragile. It’s a classic setup where enthusiasm can quickly flip to caution. If you’re tracking this for historical parallels or symbolic storytelling, it’s a textbook case of exuberance masking imbalance.

Narrowing Market Breadth and Rising Overbought Conditions in the S&P 500: A Warning Signal for Investors?

Henry RiversTuesday, Sep 9, 2025

– S&P 500’s recent gains show growing divergence from broader market breadth, with 80% of stocks above 50-day averages in May 2025 but narrowing participation by September.

– Overbought conditions intensified as 20% of S&P 500 stocks entered overbought territory, with RSI peaking at 76 and WealthUmbrella Margin Risk hitting extreme 13-level readings.

– Persistent divergence between index performance and equal-weighted indices/small-cap laggards signals structural fragility, historically preceding market corrections.

– Magnificent Seven dominance and systemic overvaluation create volatility risks, urging investors to adopt defensive strategies amid mixed economic signals and Fed policy uncertainty.

The S&P 500 has long been a barometer of U.S. equity health, but recent data suggests a growing disconnect between the index’s performance and the broader market. Investors are increasingly scrutinizing narrowing market breadth and systemic overbought conditions, which together may signal a heightened risk of a near-term correction.

Market Breadth: A Tale of Two Rallies

Market breadth, as measured by the Advance/Decline Line (AD Line), has been a mixed bag in 2025. In late 2024, the AD Line plummeted despite the S&P 500’s resilience, a classic bearish divergence that signalled weak participation and reliance on a narrow group of large-cap stocks, particularly the “Magnificent Seven” S&P 500 Forecast: Correction Signs & 2025 Buy Levels[2]. This trend persisted into early 2025, with high uncertainty over policy shifts like tariffs exacerbating the imbalance S&P 500 Forecast: Correction Signs & 2025 Buy Levels[2].

However, a more recent rebound in mid-2025 offered a glimmer of hope. By April–June 2025, the AD Line surged to a 2-year high, outpacing the S&P 500’s recovery and suggesting broader participation as stocks rebounded from oversold conditions S&P 500 Nears Record Highs: Key Market Drivers Explained[3]. By late May, 80% of S&P 500 stocks were trading above their 50-day moving averages, a robust sign of sector-wide strength US Stocks Watchlist – 5 September 2025[4]. Yet, this optimism has since dimmed. As of September 2025, the AD Line has flattened while the S&P 500 continues to climb, raising concerns about sustainability S&P 500 Forecast: Correction Signs & 2025 Buy Levels[2].

Overbought Conditions: A Volatility Time Bomb

The S&P 500’s recent rally has pushed it into overbought territory, with its 14-day RSI peaking at 76 in July 2025 US Stocks Watchlist – 5 September 2025[4]. While the index has since retreated slightly, technical analysts warn that the market remains vulnerable. The WealthUmbrella Margin Risk Indicator, a rare tool for gauging systemic overbought/oversold levels, hit an extreme reading of 13 in late 2025—a level historically associated with trend reversals Is the S&P 500 Overdue for a Correction? 2025 Forecast & …[1].

The most alarming signal is the persistent divergence between the S&P 500 and breadth indicators. While the index hit record highs in September 2025, the Equal-Weighted S&P 500, small-cap indices, and semiconductors lagged behind Is the S&P 500 Overdue for a Correction? 2025 Forecast & …[6]. This lack of confirmation from key sectors is statistically rare and historically precedes corrections S&P 500 Forecast: Correction Signs & 2025 Buy Levels[2].

The S&P 500’s current trajectory is a double-edged sword. On one hand, the mid-2025 rally demonstrated broad-based strength, with 67.87% of stocks trading above their 50-day averages in September US Stocks Watchlist – 5 September 2025[4]. On the other, the reliance on a handful of mega-cap stocks and systemic overbought conditions paints a cautionary picture.

Investors should remain vigilant. While the market’s technical setup does not guarantee a correction, the combination of narrowing breadth, overbought momentum, and divergent sector performance warrants a defensive stance. As the Federal Reserve pauses monetary policy and economic signals remain mixed, the coming months will test whether this rally is a durable recovery or a prelude to a pullback.