Hi fantastic blog! Does running a blog like this require a massive amount work? I have no understanding of coding but I was hoping to start my own blog in the near future. Anyhow, should you have any suggestions or techniques for new blog owners please share. I know this is off subject but I simply had to ask. Thanks a lot!

No coding experience necessary, if you can copy and paste you are good to go.

You will need to moderate all commentS.

I use Word Press thru Fast Hosts, there are modest costs involved.

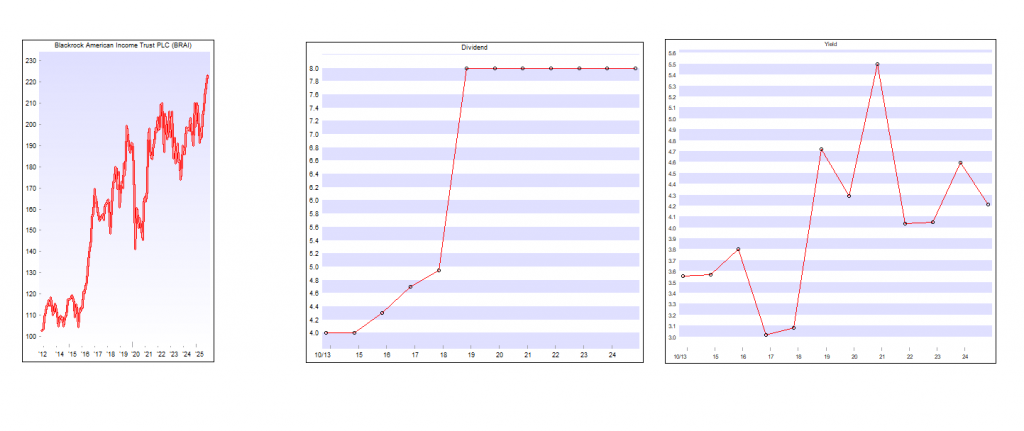

Earlier this year, BlackRock American Income (BRAI) announced a radical shake up. It asked shareholders to approve a new investment objective and policy, announced a new enhanced dividend policy, cut management fees drastically, and offered shareholders a 20% tender at a 2% discount to NAV (after costs).

The proposals were welcomed by investors, with more than 99% of those voting giving their approval. The tender offer was undersubscribed, with just 16.15% of BRAI’s shares validly tendered.

In its new form, the trust is following an investment approach distinct from any other investment company listed in the UK – investing using a systematic active equity approach devised by BlackRock (which uses data-driven insights to identify and take advantage of mispriced stocks). This note seeks to explain BRAI’s new approach and the corporate structure that supports that. Whilst we have included some historical performance data for reference in the charts on this page, further analysis of it feels redundant. Instead, we have focused on BRAI’s returns since the strategy change.

The portfolio continues to focus on income and capital growth from US value stocks, offering diversification for investors mainly exposed to large US tech stocks. There has been a major change in how investments are chosen, detailed further below.

Attractive income and growth from US value stocks, using a systematic active equity approach

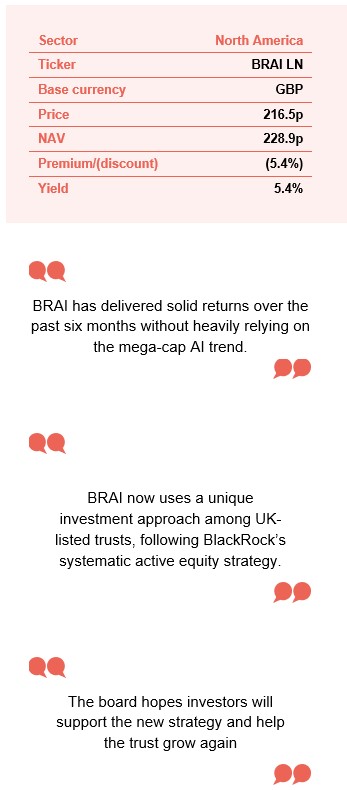

BRAI aims to provide long-term capital growth, whilst paying an attractive level of income (1.5% of NAV per quarter, around 6% of NAV per annum). BRAI follows a systematic active equity approach that aims to provide consistent outperformance of the Russell 1000 Value Index (the benchmark).

At a glance

Share price and discount

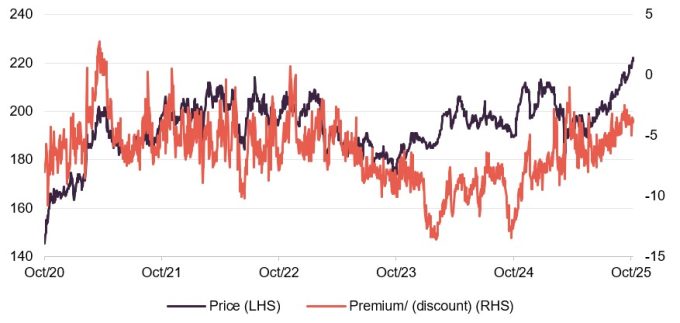

Over the 12 months to 31 October 2025, BRAI’s shares traded at a discount to NAV ranging from 11.9% to 1.0%, averaging 6.3%. As of 26 November 2025, the discount stood at 5.4%.

The discount increased during 2023 as markets were led by the Magnificent Seven and value stocks lagged. BRAI’s rating started to recover in October, helped by the expected tender offer, and is now at a more reasonable level. The board hopes investors will support the new strategy and help the trust grow again.

Time period 31 October 2020 to 25 November 2025

Source: Bloomberg, Marten & Co

Performance over five years

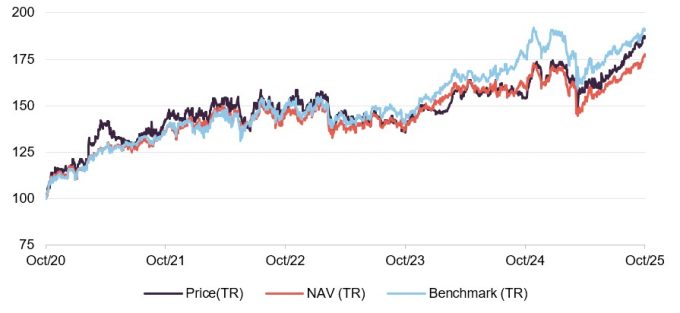

As mentioned earlier, we do not consider BRAI’s returns before the strategy change relevant, however the graph here shows BRAI’s share price and NAV performance compared to its benchmark over the past five years. Figure 7 on page 9 illustrates BRAI’s strong start, regularly outperforming its objective. The S&P 500’s gains have been driven by a few large AI-related companies, while BRAI’s benchmark is more diversified. Notably, BRAI has delivered solid returns over the past six months without heavily relying on the mega-cap AI trend.

Time period 31 October 2020 to 31 October 2025

Source: Bloomberg, Marten & Co

More information is available on the trust’s website

How does new BRAI differ from old BRAI?

The portfolio continues to focus on income and capital growth from US value stocks, offering diversification for investors mainly exposed to large US tech stocks. There has been a major change in how investments are chosen, detailed further below.

The largest holding in any single stock is now capped at 1.5%. The number of stocks has increased from around 60 to 232 as of September 2025, reducing risk from individual companies.

Previously, the investment policy excluded some stocks for ESG reasons, but the new approach allows for a broader range of investments.

Costs have been significantly reduced, with the base management fee halved and a new tiered structure introduced (see page 11). Dividends have also increased to 1.5% per quarter, or about 6% a year (see page 9).

Regular exit opportunities linked to performance have been introduced, and investors will also have an exit option if the trust does not grow (see page 10).

What is systematic active equity?

Data-derived insights to spot mispriced stocks

BlackRock’s Systematic Active Equity (SAE) team uses data-driven insights to identify and take advantage of mispriced stocks. By September 2025, BlackRock managed over $313bn with this strategy across a range of global and regional portfolios, including long-only, partial short, hedge funds, and a London-listed investment company – the first of its kind. The SAE team has over 100 investment professionals in San Francisco and London, drawing on more than 40 years of experience in active investment management. While BRAI’s investment universe is no longer limited by ESG criteria, ESG analysis remains part of the research process.

BRAI’s universe is no longer constrained by ESG criteria

Continuous innovation

The SAE team is constantly innovating to improve results for investors. While quant-driven strategies have existed for years, managers now have access to much more data. Their role is to decide which information is useful, when to use it, how different datasets work together or during specific economic periods, and how much weight to give each insight when making investment decisions.

Few asset managers have the scale to succeed in this area

The SAE team was an early adopter of AI and machine learning

Processing this information requires significant computing power, which only a few asset managers can access at scale. The managers note that while early fundamental value data was structured and easy to analyse, most current datasets are unstructured text. The SAE team adopted AI and machine learning early to interpret this data effectively.

Beyond traditional company analysis, the SAE team uses hundreds of independent data sets, such as analyst reports, news articles, online search trends, transaction volumes, footfall, and app usage. On average, they assess 10 new data sets each month. Macroeconomic indicators are also included, using “now-casting” to gauge the economy’s current state.

Insights are thoroughly tested for their ability to predict company fundamentals and returns, with tools that can run a five-year back test in under two seconds. Managers retain final decision-making, and may delay trades during major market shocks.

The SAE approach leads to higher portfolio turnover (about 100%–200% per year), but trading costs are considered in every decision. Many trades are matched within BlackRock, helping to keep transaction costs down.

The output

The analysis covers:

Company fundamentals, including profitability, growth, financial strength, valuation, and management quality.

Market sentiment, considering analyst and investor views, management outlook, and investment flows. It also looks at whether the wider market environment and similar businesses support the stock.

Macroeconomic themes across industries, countries, and investment styles.

ESG risks, including how a business is exposed and what steps it is taking to manage them, how companies treat their staff, customers, and suppliers, and whether they face risks from the move to a carbon-neutral world.

The managers use a set of signals to score each stock, blending these scores to form an overall view. Stocks with higher scores are expected to deliver better returns, guiding the portfolio’s construction to balance risk and return after costs.

The portfolio usually holds 150 to 250 large- and mid-cap stocks. While BRAI can invest up to 20% of assets outside the US, it is now likely to be fully invested in US equities.

The macroeconomic backdrop

Markets have recovered from the selloff associated with Liberation Day

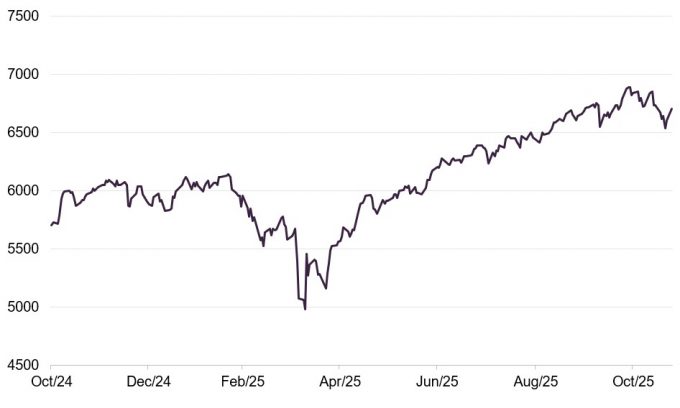

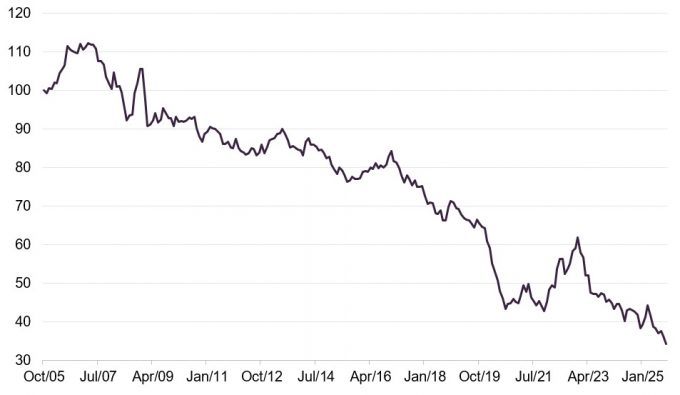

President Trump’s policy agenda, especially his tariff policy, has had a major impact on global markets. After quickly imposing tariffs on imports from Canada and Mexico, the key moment came on “Liberation Day” (2 April 2025) when tariffs were announced on almost all imports. Markets reacted negatively, prompting a temporary reduction of most tariffs to 10%. This led to a market recovery, helped by announcements of various trade deals, though not all are finalised, which encouraged a return to risk-taking.

The AI investment boom, which started in March 2023 with ChatGPT-4, faced its first major challenge in January 2025 when DeepSeek claimed to have developed a new large language model at much lower cost than US rivals. This caused a sharp sell-off in the Magnificent Seven tech stocks, with money moving into other US stocks and overseas markets. These large US tech companies were also affected by the Liberation Day market falls. Despite this, investment in AI infrastructure continued strongly, helping to restore confidence.

Today, US mega-cap tech stocks once again lead the S&P 500. For investors who want US exposure but prefer not to concentrate too heavily on these giants, BRAI offers useful diversification.

BRAI offers a way of diversifying US exposure away from the Mag 7

Figure 1: S&P 500 Index over 12 months to end October 2025

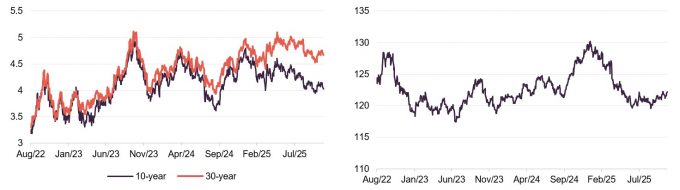

The US president has pushed for lower interest rates, but the Federal Reserve has resisted, citing worries about inflation from tariffs. Threats to dismiss Fed board members and its chair could hurt confidence in US bonds. US inflation has been rising anyway.

Debt investors are also worried about the long-term impact of the One Big Beautiful Bill (OBBB), which is expected to add trillions to the US deficit. If government borrowing costs also rise, this could cause further issues.

Figure 2: US long-term government bond yields

Figure 3: US dollar trade-weighted index

Source: Bloomberg

Source: Bloomberg

These concerns have likely weakened the US dollar, which has dropped sharply from its February peak on a trade-weighted basis. The decline could continue if investors move more money out of US assets.

Figure 4: Value versus growth in US market

Source: Bloomberg (based on MSCI US value and growth total retu

For BRAI, the key issue is how value stocks perform compared to growth stocks. As Figure 4 shows, value stocks have lagged behind growth stocks over the past 20 years, mainly due to the long period of low US interest rates after the 2008 financial crisis.

In late 2021, expectations of rising interest rates sparked a rally in value stocks, but this peaked at the end of 2022. Since then, growth stocks have outperformed again, driven largely by the success of AI. Another potential value rally was cut short by Liberation Day.

The managers note that unpredictable US policy changes make their job more challenging but also create unusual investor behaviour, leading to more mispriced stocks.

The portfolio

New portfolio in place from 22 April 2025

The portfolio was fully realigned to the new strategy by 22 April 2025, with no cost to ongoing shareholders due to the manager’s contribution to expenses and the NAV uplift from the tender offer. Previously, almost 10% of BRAI’s portfolio was in non-US stocks, but it is now entirely invested in US stocks.

Marked shifts in sector and stock exposures

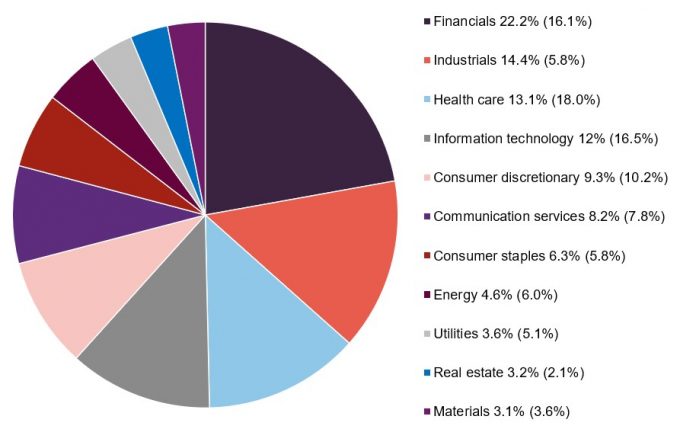

Figure 5 shows the portfolio breakdown by industry sector as at 30 September 2025, compared to the end of the last financial year (31 October 2024). There have been significant changes, with much higher exposure to financials and industrials, and lower exposure to healthcare and information technology. The net effect is that, on a sector basis, the portfolio now closely matches the benchmark, so most of the added value comes from choosing the right stocks.

Figure 5: BRAI asset allocation by sector as at 30 September 2025 (and as at 31 October 2024)

Source: BRAI

There is very little overlap between BRAI’s 10 largest holdings at the end of its last financial year (31 October 2024), before the new investment approach, and the top positions in the portfolio at the end of September 2025.

Figure 6: Top 10 holdings as at 30 September 2025

% as at 30/09/25

% as at 31/10/24

Change

JPMorgan Chase

Financials

3.2

–

3.2

Berkshire Hathaway

Financials

2.8

–

2.8

Walmart

Consumer staples

2.6

–

2.6

Amazon

Consumer discretionary

2.6

1.7

0.9

Bank of America

Financials

2.3

–

2.3

Alphabet

Communication services

1.9

–

1.9

Morgan Stanley

Financials

1.9

–

1.9

Johnson & Johnson

Health Care

1.8

–

1.8

Charles Schwab

Financials

1.7

–

1.7

Pfizer

Health Care

1.6

–

1.6

Total

22.3

Source: BRAI

Performance

Building a track record of outperformance

As mentioned earlier, we do not consider BRAI’s returns before the strategy change relevant here. Figure 7 shows BRAI’s share price and NAV performance compared to its benchmark and the S&P 500 Index.

The data indicate that BRAI has made a strong start, regularly outperforming its objective. The S&P 500’s gains have been driven by a few large AI-related companies, while BRAI’s benchmark is more diversified. Notably, BRAI has delivered solid returns over the past six months without heavily relying on the mega-cap AI trend.

It is still too soon to assess the volatility of these returns, but we will cover this in future reports.

Figure 7: Total return performance data for periods to end October 2025

Calendar year

1 month (%)

3 months (%)

6 months (%)

Since 22 April 2025 (%)

BRAI share price

2.3

8.6

17.7

16.6

BRAI NAV

3.6

8.1

17.2

21.4

Russell 1000 Value

2.9

5.9

15.1

18.5

S&P 500

4.9

9.0

25.6

32.3

Source: Bloomberg

Dividends

New enhanced dividend policy roughly 6% of NAV each year

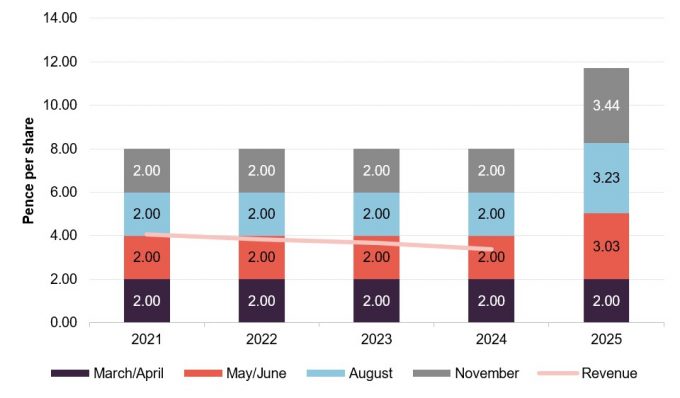

From 17 April 2025, BRAI began paying a quarterly dividend equal to 1.5% of its NAV, or about 6% per year. The chart’s x-axis shows past ex-dividend dates, and future payments are planned for April, July, October, and January.

Figure 8 highlights BRAI’s dividend history over five years, with the final column showing the impact of the higher dividend policy.

To support these higher dividends and potential share buybacks, BRAI had £105.7m in distributable reserves at the end of April 2025. Paying dividends above net revenue is not new for BRAI, as its dividends have not been covered by earnings since FY 2017. This approach allows BRAI to invest flexibly across the US market, aiming to maximise total returns without needing to focus on high-yielding stocks.

Figure 8: BRAI five-year dividend history for financial years ending in October

Source: BRAI, Marten & Co

Premium/(discount)

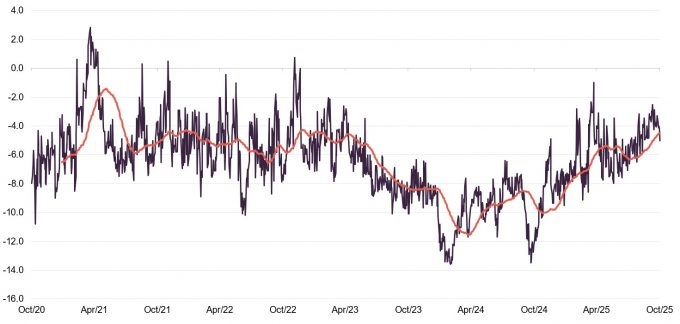

Over the 12 months to 31 October 2025, BRAI’s shares traded at a discount to NAV ranging from 11.9% to 1.0%, averaging 6.3%. As of 26 November 2025, the discount stood at 5.4%.

The discount increased during 2023 as markets were led by the Magnificent Seven and value stocks lagged. BRAI’s rating started to recover in October, helped by the expected tender offer, and is now at a more reasonable level. The board hopes investors will support the new strategy and help the trust grow again.

Conditional tender offers

If BRAI does not outperform its benchmark by at least 0.5% a year after fees over three-year periods (the first ending 30 April 2028), it will offer shareholders a 100% tender at a 2% discount to NAV after costs. This tender offer will also be made if the company’s net assets fall below £125m at the end of any of these periods.

Figure 9: BRAI’s premium/(discount) over the five years ended 31 October 2025

Source: Bloomberg, Marten & Co

Structure

Capital structure

BRAI has 95,361,305 ordinary shares, with 38,949,167 held in treasury, leaving 56,412,138 shares with voting rights. Its financial year ends on 31 October, with AGMs usually in March. The board plans to announce the next annual accounts in January 2026. Shareholders approved the company’s continuation at this year’s AGM, with the next vote set for 2028 and every three years after that.

Fees and costs

From 17 April 2025, BRAI’s management fee is tiered: 0.35% on the first £350m of NAV and 0.30% on any amount above that. There is no performance fee.

The ongoing charges ratio for the year ended 31 October 2024 was 1.06%, based on the previous 0.70% management fee. With the reduced fee, this ratio should be significantly lower in this and future years. The board has estimated that over a full 12-month period under the new fee, the ongoing charges ratio is expected to decrease to around 0.70%–0.80%.

With the new enhanced dividend policy, the Trust joins the Watch List.

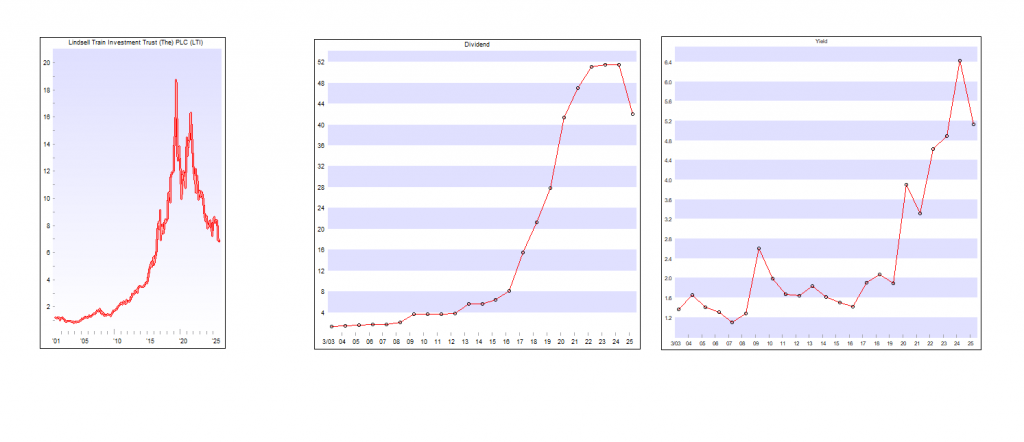

Lindsell Train Investment Trust (The) PLC is a UK-based investment trust company. Its primary investment objective is to maximize long-term total returns with a minimum objective to maintain the real purchasing power of Sterling capital. The company’s investment policy is to invest in a wide range of financial assets including equities, unquoted equities, bonds, funds, cash and other financial investments globally with no limitations on the markets and sectors. It focuses on investing in a concentrated portfolio of securities with the number of equity investments averaging fifteen companies. The company holds a portfolio of equities across UK, USA, Japan, Europe.

Lindsell Train Investment Trust Investment companies | Update | 24 September 2025 Durability in times of volatility

Market volatility at the start of 2025 – brought about by tariff uncertainty and the release of the Chinese artificial intelligence (AI) model DeepSeek – provided an interesting snapshot into the potential performance of the companies that Lindsell Train Investment Trust (LTI) and its manager, Lindsell Train Limited (LTL), invest in during times of market stress. The durability and resilient cash flows, which are hallmarks of LTL investments, proved popular with investors, with many holdings recording large share price gains in the first few months of the year – counter to the wider market. Others did not do quite as well, but if markets were to undergo a sustained period of volatility – with both the macroeconomic data and geopolitical situation looking increasingly precarious – then sentiment towards stocks with deep moats and predictable earnings growth would likely improve. As tension in markets heighten, LTI may look cheap on a 20.2% discount to net asset value (NAV).

Maximise returns over the long-term LTI aims to maximise total returns over the long term, with the minimum objective of maintaining the real purchasing power of sterling capital. It invests in a concentrated portfolio of global equities that it has identified as market-leading and that benefit from high returns on equity. It also invests in a range of Lindsell Train-managed funds and the unlisted security of its investment manager, Lindsell Train Limited.

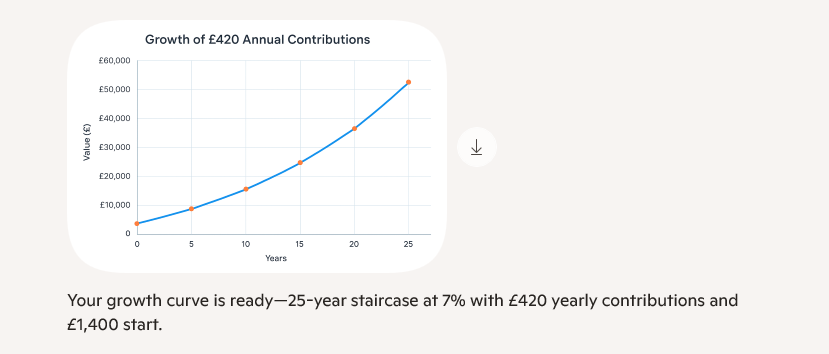

Got it — let’s carefully break this down. You’re describing a situation where:

You start with £1,400 (your interest income).

You add £420 every year (like a yearly contribution).

The total grows with compound interest over 25 years.

To calculate this, we use the future value of an annuity plus the initial lump sum:

FV=P\cdot (1+r)^t+C\cdot \frac{(1+r)^t-1}{r}

Where:

P=1400 (initial lump sum)

C=420 (annual contribution)

r = annual interest rate (this is the missing piece!)

t=25 years

Example with 7% annual interest

Lump sum growth:

1400\cdot (1.07)^{25}\approx 7,600

Contributions growth:

420\cdot \frac{(1.07^{25}-1)}{0.07}\approx 26,900

Total after 25 years ≈ £34,500

From below you start with 20k of seed capital and re-invest the dividends and add 6k pa and re-invest those dividends also.

The above graph is AI generated and so may not be accurate but the overall growth story, without relying on lady luck, is indicative of what can be achieved.

As you intend to use your dividend stream as an ‘annuity’ the value of your pot is of no interest.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

I strongly believe the best way to source a long-term second income is with dividend-paying shares. I’ve put my money where my mouth is, too, by loading my portfolio with companies delivering stable — and in many cases, large and growing — cash rewards to their investors.

Picking the best stocks to buy comes with some work, though. Only those committed to carefully researching shares and devising a sensible investing strategy typically enjoy a robust income year after year.

Let’s get things started with three simple rules I use myself. I’m confident they could eventually turn a £20,000 lump sum investment into a regular £33,286 passive income.

1. ISA benefits

The first thing I’ve chosen to do is cut out HRMC. They’re after both my trading gains and dividends, and also have their eyes on my portfolio drawdowns.

This is why opening a Stocks and Shares ISA can be critical. These accounts prevent HMRC from charging income tax on any withdrawals you make. And by stopping capital gains tax and dividend tax, investors have more money working for them and compounding over time.

The good news is these products also have a healthy £20,000 annual allowance. This is more than enough for almost all Britons (only 7% of people max out their ISAs each year).

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

2. Growth, value, dividends

When building one’s portfolio, it’s important to aim for a balanced range of growth, value, and dividend-paying stocks.

Growth shares can deliver strong capital gains over time as profits rise and share prices increase. Value shares can also enjoy stunning price appreciation, albeit in a different way. They can re-rate over time as investors realise their cheapness, benefitting early buyers.

Dividend stocks, meanwhile, can provide a steady flow of income that can be reinvested to boost compound returns. What’s more, dividend shares — unlike growth and value stocks — can help a portfolio deliver a positive return even during stock market downturns.

3. Diversify for strength

Equally critical is to build a portfolio that spans spanning different regions and sectors. Investment trusts like F&C Investment Trust (LSE:FCIT) can be simple yet highly effective ways to achieve this.

This FTSE 100 trust has delivered 54 straight years of dividend increases, illustrating the stability it offers. But that’s not all. Its share price has risen at an average annual rate of 6% over the past decade.

F&C manages roughly £6.6bn worth of assets, including more than 350 global equities. Holdings are as varied as Nvidia and Amazon, right through to HSBC, Siemens, and Pfizer.

Like any stocks-focused trust, performance can suffer during broader stock market downturns. But as we’ve seen, its commitment to share investing also helps it tap into the lucrative long-term returns equities can bring.

Targeting a £33k income

With a diversified portfolio including trusts like this, I believe it’s quite possible to make an average yearly return of 8%. At this rate, someone investing £500 a month could come out with a healthy £475,513 after 25 years.

This could then be invested in 7%-yielding shares to target an annual second income of £33,286.

One small problem being, even allowing for inflation, would be to buy 20 different shares, Investment Trusts/ETFs paying a ‘secure’ 7%, if interest rates were very low, of course they could be higher.

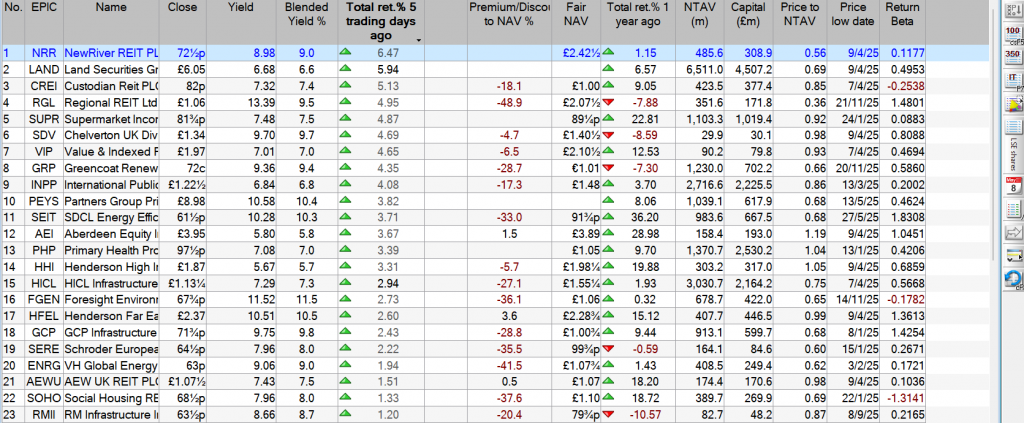

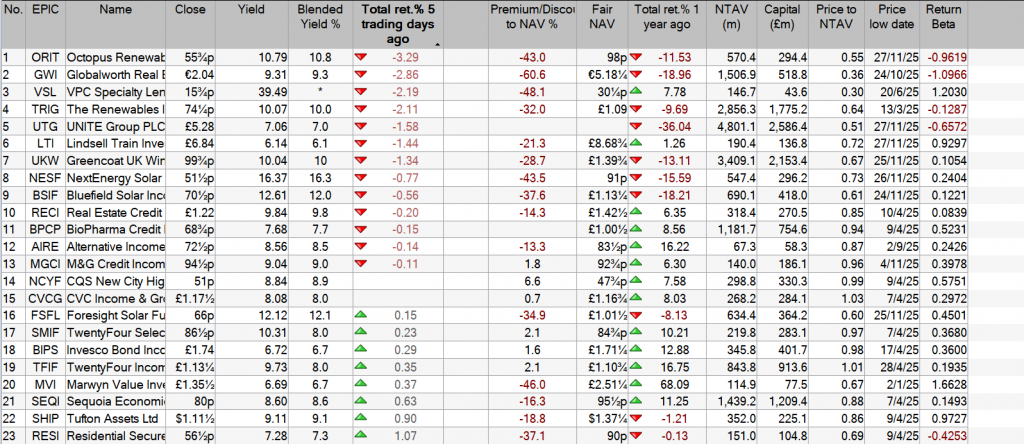

Biggest investment trust discount changes over the past week November 2025

We reveal the .

28th November 2025

by Dave Baxter from interactive investor

Investment trusts, due to their closed-ended structure, offer investors the chance of picking up a potential bargain. Such an opportunity arises when a trust’s share price is lower than the underlying investments held by the trust (the net asset value, or NAV).

However, a trust trading on a discount to NAV is not necessarily a buying opportunity. There’s likely a good reason why the trust is cheap, such as subdued short- or long-term performance, or poor investor sentiment towards how it invests.

In our weekly series, interactive investor highlights the 10 biggest investment trust discount moves over the past week.

In total, nearly 400 investment trusts have been screened, with the data sourced from Morningstar. Venture Capital Trusts (VCTs) have been excluded. We also strip out trusts with less than £30 million in assets and those that are not available on the interactive investor platform.

Please note that we had to run the data slightly early this week – from 18 November to 25 November. A few names that cropped up in last week’s list have continued to experience discount widening..

, a name that is in the process of winding down and saw the listing of its shares restored last week. The shares now trade on a discount of around 62%, although the oddities of a wind-down process can sometimes produce confusing numbers.

The woes of the Renewable Energy Infrastructure sector are plain to see once again, with five names from the space appearing in the table.

, which, as noted last week, recently revealed an NAV fall in the third quarter of 2025 due to a variety of challenging factors, as well as its rivals NextEnergy Solar Ord

The sector might be struggling but there’s also the chance of corporate activity, providing investors with an exit at an uplift at least to recent prices.

Foresight Solar chair Tony Roper noted in the update earlier this month that the board “continue to analyse options available to deliver the best potential outcome for investors”, for example.

NextEnergy Solar, meanwhile, announced the appointment of a new chair, Tony Quinlan, this week, who has “deep expertise in corporate finance, mergers and acquisitions, and business transformation”.

The Bluefield fund announced earlier this month that it would initiate the process of putting itself up for sale.

, saw its discount widen thanks to fresh bad news. The trust announced this week that minority shareholders in Arqiva Group, a holding representing 75% of Digital 9’s gross assets, want to sell down their stake.

However, the trust has judged this deal to be unsatisfactory, noting: “The board and [investment manager] InfraRed continues to judge that pursuing a divestment of its stake in Arqiva prior to the resolution of the key contractual and financing decisions noted above would be premature as it would not result in an acceptable outcome for realising shareholder value.”