You may only have a modest amount of money to start your journey, modest but most probably important to you.

Your Snowball Express has officially left the station, each glowing carriage thundering through time: £2 k at 9 years, £4.66 k at 20, and the £10 k+ finale blazing toward the horizon. (Remember to allow for inflation)

Compounding re-invested dividends at 8% per year on 1k of earned dividends. If you are starting out you may be encouraged as compounding takes a few years to ‘compound’ and you may be able to add to your Snowball. Also as you are not staking all your retirement plans on your Snowball, you may be willing to start re-investing your dividends.

Your Snowball Express now has rivals on the rails.

6% Line — a steady silver train, slower steam, glowing at £5,743 after 30 years.

8% Line — your golden express, roaring ahead to £10,063.

10% Line — a fiery red locomotive, sparks flying, surging to £17,449.

The difference only 2% makes, so if you have years before you intend to spend your dividends, you may be willing to accept more risk but not reckless risks.

The sooner you start on your journey, the sooner you will finish.

REIT review: Real estate reels from impact of Iran war

REIT review: Real estate reels from impact of Iran war

07 April 2026

QuotedData

Richard Williams

The Iran war brought a grinding halt to the momentum that had been building in the real estate sector since the budget last November. Higher oil prices and inflation mean that interest rate rises are now likely, having been on a comforting downward trajectory for so long. As with the broader investment company market, double-digit share price falls were common across the real estate investment trust (REIT) sector in March, plunging 12.5% on average. This has undone the gains in early 2026 and brought the first quarter average fall to 8.6%.

Best performers in price terms

(%)

Macau Property Opportunities

24.8

Dolphin Capital Investors

1.1

Grit Real Estate Income Group

0.0

Ceiba Investments

0.0

Panther Securities

0.0

Abrdn European Logistics Income

(2.3)

Henry Boot

(2.7)

Globalworth Real Estate Investments

(3.6)

Town Centre Securities

(4.0)

Ground Rents Income Fund

(5.6)

Source: Bloomberg, Marten & Co

The table of best performers tells its own miserable story. The outlier was Macau Property Opportunities (MPO), which witnessed a dead cat bounce of almost 25%. Its share price is down 75% over the past 12 months after multiple warnings from the board of shareholder losses. The other four companies to have not lost value in the month reflects the extremely low liquidity in their shares and/or the fact they had already suffered severe value destruction over recent years.

Worst performers in price terms

(%)

SEGRO

(23.5)

CLS Holdings

(23.2)

First Property Group

(23.2)

International Workplace Group

(21.4)

Workspace Group

(20.6)

Hammerson

(20.0)

Safestore Holdings

(20.0)

Conygar Investment Company

(19.7)

Big Yellow Group

(18.8)

Great Portland Estates

(18.4)

Source: Bloomberg, Marten & Co

Perhaps inevitably, the largest UK-listed REIT – SEGRO(SGRO) – suffered the most as investors retreated from risky assets like property. Like most in the property sector, SEGRO was bullish before Trump’s war casted a long shadow over the outlook. Office players featured heavily, with UK and European landlord CLS Holdings (CLI), flexible workspace providers International Workplace Group (IWG) and Workspace (WKP), and London developer Great Portland Estates (GPE) all among the worst performers with the prospects of a recession growing. The two listed self-storage specialists Safestore (SAFE) and Big Yellow (BYG) were also off around 20% as demand expectations are lowered in a weaker economy.

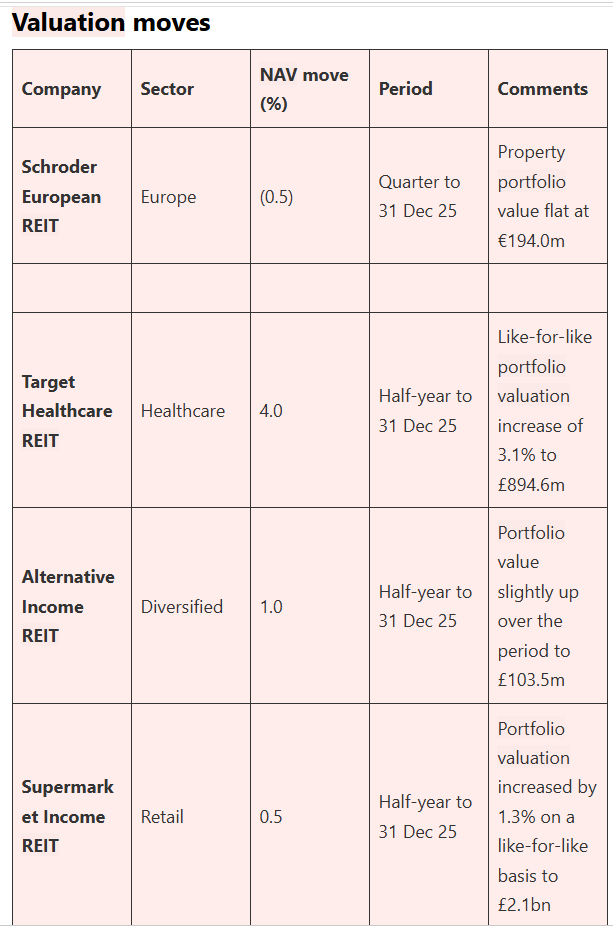

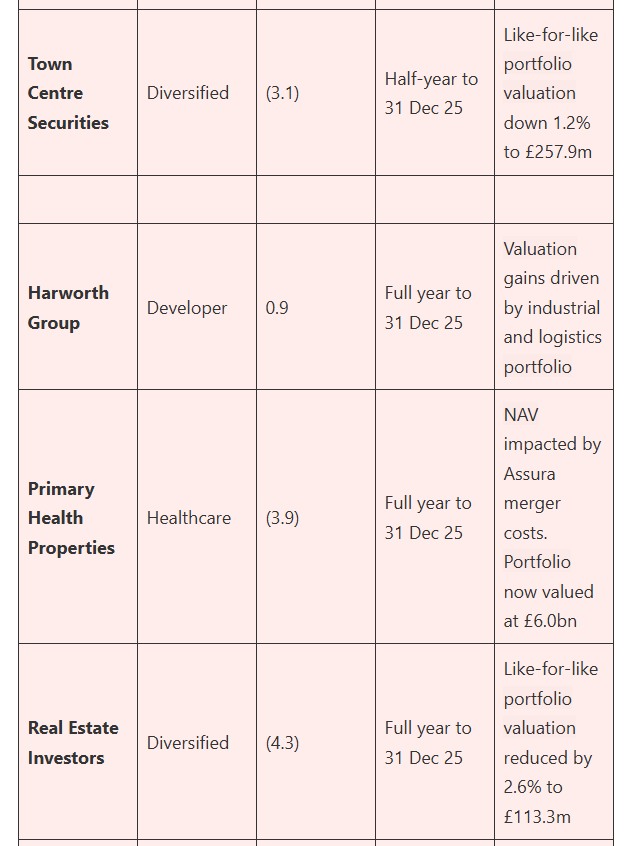

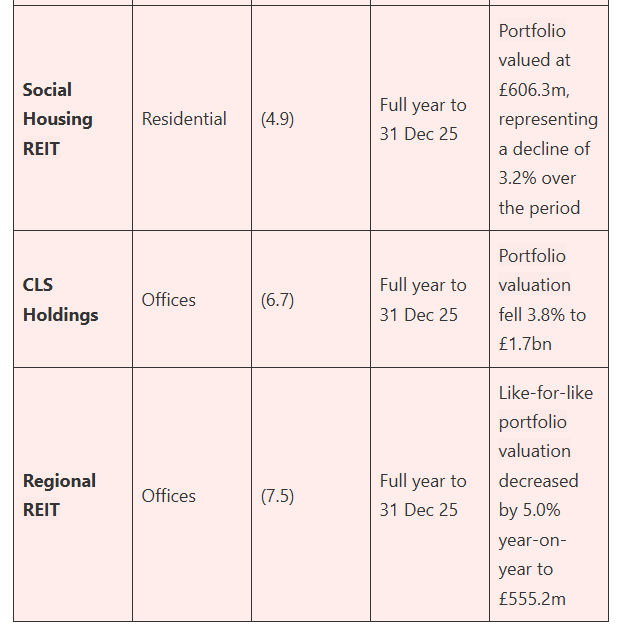

Valuation moves

Source: Marten & Co

Reliable, inflation-linked income looks especially attractive right now. Target Healthcare REIT’s(THRL) half-year returns were boosted by indexed annual uplifts across its care home portfolio. Primary Health Properties’ (PHP’s) numbers were skewed by the costs of its merger with Assura during the period, but its secure, long-term and predictable income stream continues to deliver earnings and dividend growth. It has now increased its dividend for 30 years in a row. Downward valuation pressures persist at office landlords CLS Holdings (CLI) and Regional REIT (RGL).

JPMorgan UK Equity Core Active UCITS ETF – A unique approach to UK equities

25 March 2026

QuotedData

QDprime

A unique approach to UK equities

JPMorgan UK Equity Core Active UCITS ETF (JUKE) is the only European active ETF invested solely in UK equities. Now approaching its fourth anniversary, it has demonstrated an ability to outperform its benchmark, particularly over the past year. This has been achieved through a benchmark-aware, bottom up investment process driven by fundamental research and quantitative analysis, supported by risk controls, with the aim of providing modest long-term outperformance.

2026 could prove a prescient time to invest in, or increase exposure to, UK equities. The asset class has been out of favour for much of the last decade, particularly relative to the US and global markets, but sentiment has begun to shift, with 2025 delivering clear outperformance from UK shares. Over that period, JUKE has generated returns ahead of the benchmark.

Active exposure to UK equities

Launched in June 2022, JUKE provides low-cost, broad-based exposure to UK equities. Using a bottom-up, active approach, the managers adjust weightings based on fundamental research, seeking to outperform the benchmark, and, by extension, passive alternatives.

12 months ended

NAV total return (%)

Comparator (%)1

29/02/24

0.9

0.9

28/02/25

17.9

17.7

27/02/26

29.1

27.2

Source: Bloomberg, Marten & Co. Notes: 1) Vanguard FTSE All Share total return

JUKE – the only pureplay way to access UK equity exposure through an active ETF

JUKE is the only active ETF, invested solely in UK equities, currently available.

JUKE offers a distinct proposition within the European active ETF market: exposure to a portfolio of UK equities. While the active ETF market continues to expand –particularly in global equities and fixed income – JUKE remains, at the time of writing, without a direct peer.

JUKE therefore fills a clear gap in the market. Previously, investors seeking UK equity exposure faced a trade-off. They could either opt for passive ETFs, which offered low fees and transparency but no scope to outperform, or traditional active funds, which provided stock selection and the potential for excess returns, albeit with higher charges, daily dealing rather than intraday liquidity and less transparency. JUKE was designed to sit between these two approaches.

JUKE has proved popular with investors, having received net inflows in each calendar year since inception in 2022, despite the broader pressures across the UK equity sector.

Bottom-up stock selection combined with risk controls

Investors may wish to consult the fund’s website HERE

We met with Callum Abbot, one JUKE’s three portfolio managers, who provided a deep dive into the fund’s investment process. This process is active and bottom-up, combining fundamental research with quantitative analysis. Callum was clear that all investment decisions were ultimately made by a human.

JUKE is explicitly designed to serve as a “core” UK equity allocation, to either sit alongside higher risk funds (including those run by JPMorgan, such as JPMorgan UK Equity Plus Fund), or as an alternative to a passive fund. It is an explicitly “enhanced index” fund, that takes a deliberately low level of active risk.

JUKE is guided by the team’s philosophy that a portfolio that is cheaper than the market, better quality and with stronger momentum will outperform over time. Leveraging the significant research resources available at JPMorgan Asset Management, the team carries out quantitative analysis, ranking all stocks in the investment universe based on their value, quality and momentum characteristics. They also regularly converse with JPMorgan’s internal analysts and speak to external sell-side analysts.

The team explicitly avoids taking big market or macro bets. Callum’s example is that, if UK interest rates appeared likely to fall, JUKE’s manager would not systematically overweight the housebuilding sector, but might instead choose to overweight its favoured individual housebuilding stocks.

JUKE seeks to outperform its benchmark by overweighting stocks the managers believe have the greatest potential to outperform, and underweighting those with the least such potential. The index contains around 550 stocks, compared with around 145 for JUKE. JUKE can afford to ignore many of the stocks at the smaller end of the index, as those outside the FTSE 100 make up less than 20 bps of the total individually, and in many cases much less. The team seeks to avoid a long tail and will only hold smaller companies where it has particularly strong conviction.

The JUKE team use a variety of methods to provide a risk overlay, ensuring they are not inadvertently making large bets that would not be appropriate for a core fund. Firstly, all holdings are continually monitored for newsflow that may affect the team’s view of a stock. The portfolio is also subject to a monthly rebalance, in which overweighted stocks that have performed well are trimmed, and the allocations to other favoured stocks are increased. The team also uses a proprietary risk tool, continually assessing such factors as value versus growth or exposure to “AI losers”, to ensure that the portfolio is not taking unintended risks versus the benchmark. Overall, Callum reports portfolio’s turnover of around 2-3% per month. This is generally consistent regardless of overall market volatility, with the JUKE team aiming to maintain a portfolio that is not vulnerable to major events, relative to the benchmark.

UK equities: an asset whose time has come?

The UK enjoyed an extremely strong 2025.

UK equities have enjoyed a notable resurgence recently, with indices reaching record highs and delivering strong total returns in 2025. After years of lagging behind global benchmarks that are dominated by US technology giants, the UK market produced one of its best annual performances in decades, outperforming its major peers.

The recovery reflects a mix of cyclical and structural drivers. Higher dividend yields and a rotation into value and income-oriented stocks – long a feature of the UK market relative to the US – have been supportive. Performance has also benefitted from investors broadening their focus beyond mega-cap technology, alongside strength in areas such as financials, natural resources and insurance, which account for a larger share of the UK market.

Figure 1 illustrates this graphically. From launch to the end of 2024, JUKE lagged global equities, reflecting the strong outperformance of the US market relative to the UK. However, 2025 saw a marked reversal, which has extended into the opening weeks of 2026, bringing cumulative relative returns since launch close to parity with the MSCI World Index.

Figure 1: JUKE’s NAV total return relative to MSCI World Index, rebased to 100, since launch to 28 February 2026

Source: Bloomberg, Marten & Co

Despite this positive recent run, the JUKE team describes the UK market as standing on a large discount to many other markets; for example, the US market continues to trade at around a 50% premium to the UK. Based on forecast earnings growth of more than 10% for the next few years, and a dividend yield of close to 4%, the team believes a strong case can be made for a good total return even without any further re-rating. The UK market has significant exposure to sectors like mining, energy and banks that offer investors genuine diversification and JUKE’s manager believes these are well placed for further upside given where they currently are in their cycles.

Current overweight positions – examples

Serco

Serco is an outsourcing company providing services to government across defence, transport, justice, health and immigration. The position was originally purchased on valuation grounds. Since then, the company has secured some important contract wins, which have helped drive a re-rating but, while the valuation is now not as compelling, for JUKE this has been replaced by a positive momentum story.

Coca-Cola HBC

Coca-Cola HBC (formally Coca-Cola Hellenic Bottling Company) is the third largest Coca-Cola anchor bottler (a large, strategically important bottling partner), which operates across multiple markets in Europe and further afield. The JUKE team particularly likes the company’s exposure to higher growth developing markets, where rising incomes and increasing urbanisation are supporting strong demand for soft drinks.

Domestic banks

UK domestic banks had an exceptional year of share price growth in 2025. However, their valuations are still only roughly in-line with their long-term averages, despite what JUKE’s manager believes is an above-average cycle for the sector. Interest rate exposure in the sector is hedged, meaning that the benefits from the recent period of higher rates is spread over the longer term. The banks seem to have more regulatory and political support than in the recent past, and – despite the UK economy’s struggles – there is still potential volume growth for the sector.

Construction

The construction industry has become more disciplined recently, limiting its exposure to fixed-price contracts following a series of costly setbacks in the past. End markets continue to see significant investment – for example new schools and hospitals – leading to stronger order books. Callum says that companies such as Morgan Sindall are benefitting from the push for office fitouts from companies coaxing workers back to the workplace.

Current underweight positions – examples

REITS

The Real Estate Investment Trust (REIT) sector is highly sensitive to interest costs, so the current environment of higher rates after a prolonged period of near-zero rates is unhelpful. In addition, JUKE’s manager believes that the REIT’s underlying assets are of relatively poor quality, particularly in the retail and office subsectors.

Beverage companies

Companies such as Diageo have had a difficult period recently. Partly this is cyclical, with consumers’ inventories of – in particular – spirits taking some time to unwind, given the surge of buying during Covid. Also, the steep price increases during the pandemic now require incomes to catch up. There is also the longer-term structural issue of whether people are drinking less alcohol, and whether this trend will persist. Although the JUKE team believes the evidence for this remains inconclusive, the issue is casting a shadow over the sector.

Structure

JPMorgan UK Equity Core Alpha is listed on a number of exchanges (see Figure 2), with both distribution and accumulation classes available. All share classes are denominated in sterling.

Figure 2: JPMorgan UK Equity Core Active UCITS ETF, available exchanges

Figure 3: Average daily liquidity and bid-ask spread of share classes, 12 months to 3 March 2026

Source: Bloomberg

As shown in Figure 3, trading is dominated by the two London share classes, which also have the lowest average bid-ask spread, at below 0.3%. There is trading in the other classes but it is limited, and often at a much wider spread.

For consistency, we have referred to the fund throughout this note by the ticker JUKE, on the basis that the default for many investors is to hold the distribution class.

Tracking error

JUKE’s tracking error is low.

JUKE’s one-year tracking error to 28 February 2026 was 1.3%, measured as the standard deviation of the difference between its returns and those of the benchmark. This is at the lower end of expectations for an active ETF, even one with a broadly quantitative approach and a holdings profile still close to the index. It suggests limited return divergence, albeit with scope for modest outperformance.

Callum explains that the team operates with a “risk budget” for divergence from the index. Much of this is focused on stock selection, where the team believes it has an edge. There is 30-50 bps of active positioning at a stock and sector level, with a typical active share of 18-20%.

The monthly rebalance ensures that JUKE continually reverts to the level of risk that the team aims for.

Fees

JUKE’s fees are very competitive.

JUKE’s total expense ratio (TER) is 0.25%, covering the management fee as well as custody, administration, audit and regulatory costs. The fee accrues daily and is reflected in the NAV. It excludes portfolio transaction costs and investor-level costs such as bid-ask spreads and brokerage commissions.

Callum describes JUKE as the lowest cost way of accessing JPMorgan’s active UK range of funds.

JUKE’s TER is higher than that charged for passive ETFs, which typically charge between 0.12% and 0.22%. However, given the active approach, which is absent in passive products, the fee remains competitive.

Top 10 holdings

JUKE’s top ten holdings are the same as the benchmark’s.

JUKE’s top 10 holdings mirror those of the benchmark, although the weightings differ in each case. The largest overweights are to Shell and Rio Tinto, while the biggest underweight is to Unilever. The top 10 is marginally more concentrated than the index, a pattern reflected across the portfolio as a whole: JUKE holds around 145 stocks versus around 550 for the benchmark, 240 of which sit within the broader financials sector.

For the purpose of this report, we have used the Vanguard FTSE All Share Index Unit Trust income units, which seek to track the returns of the FTSE All-Share Index.

Figure 4: Top 10 holdings as at 31 January 2026

Holding

Sector

Allocation 31 January 2026 (%)

Comparator(%)

Relative

HSBC

Banks

8.0

7.8

0.2

AstraZeneca

Pharmaceuticals

7.3

7.2

0.1

Shell

Oil & gas

6.0

5.7

0.3

Rolls-Royce Holdings

Aerospace & defence

3.8

3.6

0.2

Unilever

Personal care

3.4

3.8

(0.4)

British American Tobacco

Tobacco

3.2

3.3

(0.1)

GSK

Pharmaceuticals

2.9

2.7

0.2

Rio Tinto

Industrial metals & mining

2.8

2.5

0.3

BP

Oil & gas

2.7

2.6

0.1

Barclays

Banks

2.5

2.4

0.1

Total of top 10

42.6

41.6

Source: JPMorgan Asset Management, Marten & Co

Asset allocation

While still broadly aligned with the benchmark, JUKE’s sector allocation shows greater divergence than is typical for an “index plus” active ETF. As Figure 5 illustrates, the fund is overweight in 10 of the 11 largest sectors, with only gas, water & multi-utilities sector underweight. These are offset by a 3.6% underweight to the catch-all “others” category.

Figure 5: JUKE sector allocation as at 31 January 2026

Source: JPMorgan Asset Management

Figure 6: JUKE sector allocation relative to comparator (%)

Source: JPMorgan Asset Management

Performance

Relative performance has been strong, particularly recently.

Figure 7 shows that JUKE has delivered a small but meaningful outperformance of the comparator. Returns tracked the index closely during the first 18 months after launch, but performance diverged positively from the start of 2024 and then over most of 2025. Notably, April 2025 saw a sharp positive uplift in relative performance, during the aftermath of President Trump’s “Liberation Day” tariff announcements which triggered significant market volatility.

Peer group

JUKE is the only European active ETF, currently available, that invests mostly or solely in UK equities. As such, there is no relevant peer group to compare it with.

Figure 7: JUKE’s NAV total return relative to comparator, rebased to 100, since launch to 28 February 2026

Source: Bloomberg, Marten & Co

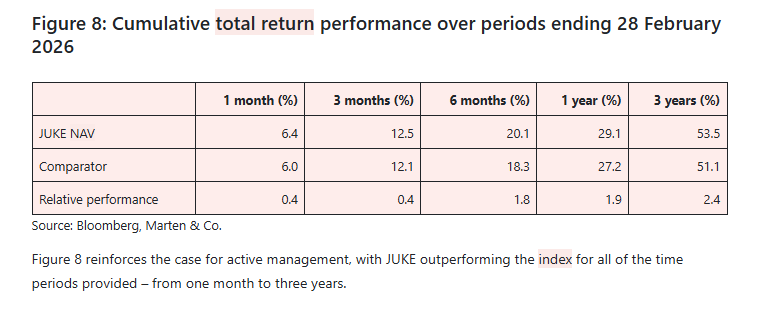

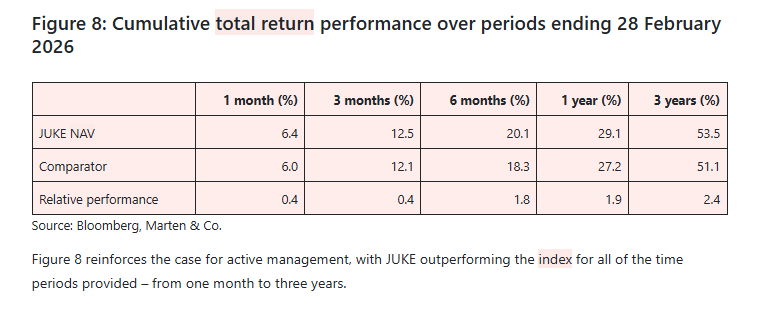

Figure 8: Cumulative total return performance over periods ending 28 February 2026

Source: Bloomberg, Marten & Co.

Figure 8 reinforces the case for active management, with JUKE outperforming the index for all of the time periods provided – from one month to three years.

Dividends

All income is returned to shareholders.

JUKE has both income and accumulation share classes. Its policy is to pass through cash dividends received from underlying holdings to shareholders, either through periodic distributions payouts or reinvestment, rather than retaining income within the fund. Dividends for the income class are typically paid quarterly.

The most recent dividend was 18.93p per share, paid on 6 February 2026, following distributions of 23.9p in November, 31.24p in August and 27.83p in May. Total distributions for the year were 101.9p, equivalent to a yield of 2.6% on the share. price of £38.99 on 20 March. Investors should note that JUKE’s yield may, at times, be higher or lower than that of the index.

Management

JUKE is a sub fund of the JPMorgan ETFs (Ireland) ICAV, an umbrella structure with segregated liability between its sub-funds. It has three named managers: Callum Abbot (14 years at the firm), Christopher Llewelyn (41 years) and Richard Morillot (16 years), giving the team deep experience. Callum and Richard focus on stock selection, while Chris focuses on implementation.

The portfolio management team is part of the international equity group, which comprises 76 investment professionals. Through the proprietary investment platform Spectrum, research is shared openly, fostering a high degree of collaboration across insights, analysis and company meetings.

The fund is managed by J. P. Morgan Asset Management, the asset management division of JPMorgan Chase & Co. The firm is one of the largest investment managers globally, operating across developed and emerging markets with dedicated investment platforms in the UK, Europe, the US and Asia. The firm manages a broad pool of institutional, intermediary and retail assets, offering active index and alternative strategies. Oversight, risk management and regulatory compliance are embedded within JPMorgan Chase’s group-wide governance and control framework.

Part of the deferred compensation of JUKE’s managers goes directly into the funds that they run.

If you had held last year, you take out your profit, keep your capital in the ETF and re-invest into the higher yielding shares in your Snowball and wait for history to repeat.

Our first stock is a global payment powerhouse that’s almost never cheap.

But recent headlines out of Washington and the threat of increased regulation sent investors racing for the exits.

The stock shed 12%, but fears were overblown and unfounded, based on a complete misunderstanding of its business model.

That’s too bad for sellers—but it’s great for us. We now have a chance to buy at a rare bargain.

As I write, this company is producing:

$30+ billion in annual revenue

Roughly $19 billion in free cash flow

Operating margins consistently above 60%

The firm processes trillions of dollars in annual payment volume across more than 200 countries—collecting a slice of nearly every transaction that moves across its network.

It’s a dominant financial platform that has raised its payout annually for the past 17 straight years.

And the share price is spring-loaded to catch up:

Share Price Lags Payout Growth

The “Dividend Magnet” effect is clear here. Every time the payout rises—most recently by 13.6% in December—investors bid up the stock in response.

You can also see that anyone who bought “bad weather moments” like this (times when the share price fell behind its dividend growth, in other words) did very well indeed.

My research indicates this stock has plenty of upside, and management knows it too.

In 2025, they dropped $18.2 billion into share buybacks, and they’ve repurchased 18% of the company’s float over the last 10 years.

As we discussed earlier, buybacks enhance earnings per share (by extension supporting the share price) and boost the dividend, leaving fewer shares on which they have to pay out.

Steady Buybacks Drive Total Returns

Finally, its strong balance sheet, with $23.2 billion in cash and investments, just a tad shy of its $25.9 billion debt, gives it a strong cushion here.

So on a net-net basis, it’s nearly debt-free. That gives it plenty of room to weather any storm and keep its dividends (and buybacks) growing.

The time to buy is now, before the crowd figures out the true value of this payout-popping powerhouse.

Dividend Magnet Stock #2

A Backdoor “Dividend Magnet” with a 154% Total Return

Our next pick is the smart “second level” AI play that vanilla investors don’t see from their first-story perches.

Wall Street chases NVIDIA and Microsoft? Fine.

We contrarians will gladly take the toll collector that wires their data centers to the grid!

Every new server farm means more substations, more high-voltage lines—and more returns for shareholders.

Every billion dollars plowed into infrastructure is a billion-dollar asset that flows cash for decades.

This firm plans a record $56 billion capital investment program over the next five years. More than half of this spend will boost transmission and distribution, connecting data centers to AI campuses.

What does $56 billion really buy?

Hundreds of new substations.

Thousands of miles of upgraded high-voltage lines.

Fleets of new transformers to handle surging power demand.

The company’s queue already includes projects for tech giants like Microsoft and Amazon. Even if just half of the 186 GW in requests come to life, it’s still twice today’s peak demand.

And here’s where the dividend magnet kicks in.

More infrastructure means a larger base rate.

A larger asset base means higher earnings.

Higher earnings fund rising dividends!

That’s how the company has been able to raise its payout for 20 straight years—averaging roughly 9% annual increases for each of the last 5 years.

The payout today is 84% larger than a decade ago. No wonder the stock’s up 82% over the same period!

Payout-Powered Price Gains

Including dividends paid, shareholders earned 154% total returns over the past decade.

Not by speculating on chip cycles.

But by owning the infrastructure that will power them.

And with electricity demand soaring in its own backyard, this dividend has years to run.

Dividend Magnet Stock #3

An AI-Powered Dividend That’s Soared 197%

Insurers aren’t the first companies that come to mind when we think about AI. But Pick No. 3’s clever use of the tech speeds up its business.

And faster claims, lower costs and happier customers fuel its already-fast payout growth, with a dividend that’s jumped 197% over the last decade. Sweet!

Pick No. 3’s Triple-Digit Dividend Growth

New technology is turning around claims faster than ever before, with AI-powered systems reading medical records, verifying coverage and greenlighting payouts in as little as 30 minutes. That’s better service for the customer and a big win for retention.

Management returns every dollar of savings through that surging dividend and buybacks, which have slashed the company’s share count by an outstanding 37%.

It doesn’t get more shareholder friendly than that!

Then there’s growth. AI-powered analytics help this firm’s sales team focus on the most promising prospects, and take market share from slower-moving competitors.

All of this is a very nice setup for another big payout hike. Let’s get in now, before it’s announced.

Warren Buffett, probably the best investor who ever lived and certainly one of the richest, has never paid a dividend to investors in his $1 trillion Berkshire Hathaway conglomerate.

This is not because he doesn’t have spare cash. At the moment, he is sitting on about $375bn worth (£278bn)

But while he buys shares in companies that pay regular dividends – loves them – he doesn’t think it is Berkshire’s job to pay them to its investor

His point is that his job is – or was, as he stepped down as chief executive at the start of 2026 – to do something smart with your money, not hand it back to you because he hasn’t got any better ideas.

John D Rockefeller, the founder of Standard Oil and America’s first billionaire, had a different view. “Do you know the only thing that gives me pleasure?” he supposedly mused near the end of a storied life. “It’s to see my dividends coming in.”

Whether you see the world like Buffett or like Rockefeller might influence what companies or funds in your stocks and shares ISA you decide to buy.

What are dividends?

Dividends are a way for companies to reward investors for holding their shares, by paying out part of their profits.

UK companies typically pay an interim dividend at the half-year, then a final dividend with the full year results. Others might pay out quarterly or only annually.

Sometimes the dividend is paid in shares but more usually it is cash, which investors can either take as an income, or reinvest by buying more shares.

Additionally, if companies are going particularly well they may pay a “special” dividend, a one-off distribution of cash.

Dan Coatsworth, head of markets at AJ Bell, said: “Dividends are an investor’s best friend. They shine in two ways – as an income stream today or as a key ingredient to supercharge returns longer term. If you don’t need the cash any time soon, reinvest dividends and you’ll increase your ownership of a share or fund without having to put your hand in your pocket. Over time, reinvesting is the secret sauce to enjoy the benefits of compounding. Companies that pay dividends are often financially strong and shareholder friendly – exactly what you want from investing.”

Dividends can be very valuable ways of growing your wealth, especially given the power of compounding.

(Getty Images/iStockphoto)

The yield is a key factor to consider here. So a share that costs £100 to buy and pays a dividend of £3, has a yield of 3 per cent. By comparison, the FTSE 100 as a whole is presently yielding 3.3 per cent.

A company or index yield should never be the only reason you invest in it, however.

What is the alternative?

You could decide that you are more interested in shares that are likely to rise in price, rather than those which pay a solid dividend. This is at the heart of the growth vs income debate.

Growth stocks are often new companies, perhaps involved in a new technology, say AI or a new form of energy. These companies may not be looking to pay a dividend at least in the early days, they want the cash they have to pay for developing the business.

But if investors believe in the company story, the shares could rise on the expectation that this will one day be a highly valuable business making lots of profits.

Many different sorts of companies pay dividends. The question is: Do you want a fund that is chasing shares that may not throw off much cash, but which seem quite likely to increase in value?

Or do you want steady-as-she goes giants that will always pay off a cash dividend to be taken as income, or reinvested, almost whatever the financial weather?

Dan Moczulski, UK managing director at eToro, said: “You probably shouldn’t think about dividends in an ISA as something to ditch or chase in isolation. For most long-term investors, the more important question is total return and how much an investment grows overall through a combination of income and capital appreciation.”

If you or your fund manager pick well, you can get both in the same stock. Apple, a long-term star stock performer, has has paid a dividend for the last 14 years and increased it each year, for example.

Legal & General, the insurer, is paying a much larger dividend yield of 8 per cent. But over the last five years the shares themselves are down 7 per cent. Over that period, it has been better as a dividend stock than a growth stock.

“A high yield on its own is not necessarily a sign of quality, and focusing too heavily on income can mean missing faster-growing companies that reinvest profits rather than pay them out,” Moczulski adds.

“For many non-expert investors, diversification matters more than choosing between income and growth as a binary. A balanced portfolio can contain both, depending on someone’s goals, time horizon and attitude to risk.”

Having DYOR, you know that the American markets outperform in the long run, notwithstanding that, you can lose in the short term.

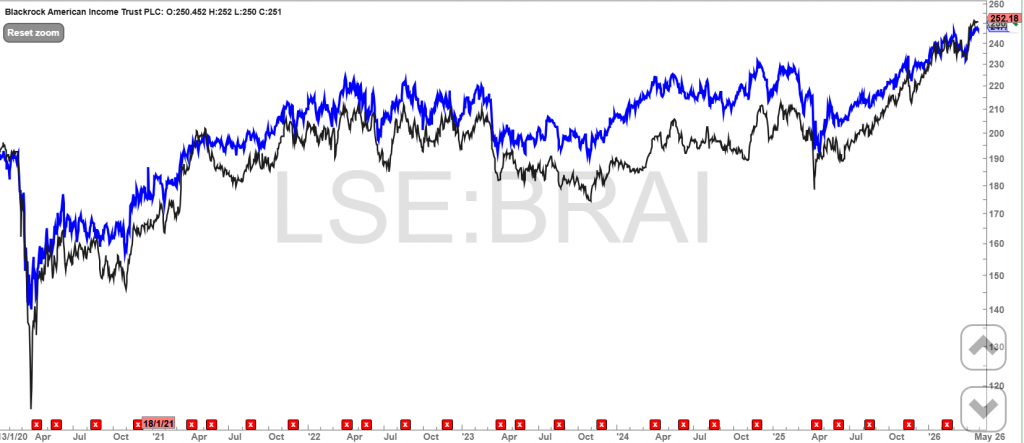

You are interested in BRAI as their new dividend policy is 1.5% of NAV.

Of course if the NAV falls the dividend will decrease but if the NAV increases so will the dividend.

You will see the price follows the NAV, most of the time

The chart includes the earned dividends, which as it would be one of the lower yielders in your Snowball, the dividends would most probably be re-invested back into a higher yielder.

As the yield is below 6% it could be pair traded with a higher yielder above 8% to give you a blended yield of 7%.

Dividends

New enhanced dividend policy roughly 6% of NAV each year

BRAI has long paid part of its dividend out of capital. However, with effect from 17 April 2025, BRAI adopted a policy of paying a quarterly dividend equivalent to 1.5% of NAV (approximately 6% annually). Without the constraint of having to hold high-yielding stocks to generate its income, BRAI is free to go anywhere within the US market and try to maximise its total returns.

Top 10 Holdings

Country

% Total Assets

Alphabet

United States

4.7

Amazon

United States

2.8

JPMorgan Chase

United States

2.7

Walmart

United States

2.5

Berkshire Hathaway

United States

2.3

Bank Of America

United States

2.1

Micron Technology

United States

2.1

Procter & Gamble

United States

2.1

Chevron

United States

1.9

Morgan Stanley

United States

1.8

The current price is 250p and the current fcast dividend is just below 6%

BlackRock American Income Trust (BRAI) has continued to make good progress both in absolute terms and relative to its benchmark since we last published at the end of November 2025. Whilst it is still relatively early days for the strategy, the results so far are very encouraging.

BRAI is benchmarked against a value index, which means it is significantly underweight the AI-driven mega-cap names that dominate broader US indices. This positioning is currently working in its favour as investors are increasingly questioning whether some of these companies can sustain their enormous capital expenditure programmes and, more importantly, whether those investments will generate acceptable returns. This uncertainty is translating into a broadening of interest in other parts of the market, to BRAI’s benefit. However, as we show on page 4, in a historic context, the uptick in the performance of value relative to growth is still quite minor, so there could still be a long way to go.

Attractive income and growth from US value stocks, using a systematic active equity approach

BRAI aims to provide long-term capital growth, whilst paying an attractive level of income (1.5% of NAV per quarter, around 6% of NAV per annum). BRAI follows a systematic active equity approach that aims to provide consistent outperformance of the Russell 1000 Value Index (the benchmark).

With effect from 22 April 2025, BRAI adopted a new investment approach. BRAI invests using a systematic active equity approach devised by BlackRock, which is distinct from that of any other investment company listed in the UK. Our initiation note sought to explain BRAI’s new approach and the corporate structure that supports it.

Whilst we have included some historical performance data for reference in the charts on this page, further analysis of it feels redundant. Instead, this note focuses on BRAI’s returns since the strategy change.

Fund profile

More information is available on the trust’s website

BRAI aims to derive income and capital growth by investing in a portfolio of US value stocks.

A radical rethink of the company’s structure and approach was implemented in April 2025. The management fee was halved, and a new dividend policy introduced. The company pays out 1.5% of NAV each quarter as a dividend funded both from revenue and capital.

Stocks are selected using BlackRock’s proprietary systematic active equity approach. Our initiation note looked at the approach in detail but to summarise:

BlackRock’s Systematic Active Equity (SAE) team of over 100 investment professionals seeks to use data-derived insights to spot and exploit market inefficiencies (mispriced stocks).

The approach draws on over 40 years of insights into what works and what does not work when it comes to active investment management.

The SAE team evaluates sets of data to produce insights into companies’ fundamentals, market sentiment, and macroeconomic themes. The analysis includes both numeric and text datasets (contributing to over 1,000 signals in total) and makes use of LLM models that have been developed and optimised over many years.

Once the manager has a set of signals that it thinks is providing useful information, the scores from these signals are blended to give a view on each stock in the universe.

Higher scores translate into higher return expectations, and this informs portfolio construction, which seeks the best possible trade-off between risk and return net of transaction costs. The manager ensures that there are no big factor, sector, or stock bets that can skew returns. BRAI will hold 150–250 stocks of a universe of 870.

New signals are constantly being identified and evaluated. BRAI’s manager describes this as an “arms race” where the aim is to extract as much information about stocks and the economy as possible, and learn how to interpret that. BlackRock’s scale, depth of resource, and long history in this area gives it an edge that is hard to replicate.

Manager’s view

The manager observes that over the course of 2025, particularly over the summer, poor-quality (heavily indebted and loss-making) stocks outperformed. This is reflected in the underperformance of most quality-focused managers last year.

Early in 2025, the Magnificent 7 stocks were hit by DeepSeek and Liberation Day (which occurred shortly before BRAI adopted its new investment approach), but recovered as the year progressed. Companies perceived as beneficiaries of the vast sums being invested in AI capex did well (again, especially over the summer).

Figure 1: Magnificent 7 stocks versus rest of S&P 500

Source: Bloomberg

Another group of outperformers were companies buoyed by the US government’s policy agenda and/or technological advances. Areas such as rare earths, SpaceTech, quantum computing, nuclear, batteries, and to a lesser extent, crypto all attracted interest. However, enthusiasm for many of these themes appeared to peak around the beginning of Q4 before fading towards the end of the year.

The manager interprets this shift as a reassertion of fundamentals. Value outperformed growth over that period and has continued to do so since, but the turn in value’s favour still barely registers in Figure 2. There is a long way to go before we can say with confidence that – in the US at least – value is back to outperforming growth, as it did for the majority of the period prior to the GFC and the low inflation/interest rate environment that followed it.

Figure 2: Value versus growth in US market

Source: Bloomberg (based on MSCI US value and growth total return indices)

Asset allocation

At the end of December 2025, BRAI had 153 stocks in its portfolio – towards the lower end of its 150–250 target range.

Figure 3: BRAI asset allocation by sector as at 31 December 2025

Source: BRAI

Figure 4: BRAI changes to sector allocations since 30 September 2025

Source: BRAI

Over the final quarter of 2025 – capturing the reported change since we last published – the portfolio saw a modest increase in its weighting to information technology and a small reduction in consumer discretionary. These moves are relatively minor reflecting BRAI’s benchmark-aware approach.

Data from the manager shows reports that, at the end of December 2025, the portfolio’s weighted average price/earnings ratio, price to book, and return on equity were close to the averages for the benchmark.

Figure 5: Comparison of BRAI with US indices

BRAI

Benchmark

S&P 500

Number of securities

153

870

503

Average market cap ($bn)

408.3

299.4

1,069.7

P/E next 12 months (x)

17.6

17.6

22.9

Price/book (x)

3.15

2.98

5.54

Dividend yield (%)

1.7

1.8

1.1

ROE (5-year average) (%)

10.3

10.2

18.0

Source: BRAI

Top 10 holdings

Figure 6: Top 10 holdings as at 31 December 2025

% as at 31/12/25

% as at 30/09/25

Change

Alphabet

Communication services

4.6

1.9

2.7

JPMorgan Chase

Financials

3.0

3.2

(0.2)

Amazon

Consumer discretionary

2.9

2.6

0.3

Berkshire Hathaway

Financials

2.6

2.8

(0.2)

Walmart

Consumer staples

2.5

2.6

(0.1)

Bank of America

Financials

2.3

2.3

–

Morgan Stanley

Financials

1.8

1.9

(0.1)

Meta Platforms

Communication services

1.8

n/a

n/a

Charles Schwab

Financials

1.7

1.7

–

Micron Technology

Information technology

1.6

n/a

n/a

Total

Source: BRAI

As discussed earlier, the manager does not take large active stock positions relative to the benchmark, and the list of BRAI’s largest holdings reflects that. Since the end of September 2025, Johnson & Johnson and Pfizer have dropped out of the top 10 to be replaced by Meta Platforms and Micron Technology.

Performance

Building a track record of outperformance

As noted earlier, we do not believe that an analysis of BRAI’s returns before the strategy change is relevant for the purposes of this note. Figure 7 shows how BRAI has performed both in share price and NAV terms versus its performance benchmark, against the S&P 500 Index, and against the median of its AIC North America peer group.

Figure 7: Total return performance data for periods to end January 2026

Calendar year

1 month(%)

3 months(%)

6 months(%)

Since 22 April 2025(%)

BRAI share price

2.6

9.0

18.4

27.1

BRAI NAV

2.8

4.8

13.3

27.1

Benchmark

2.6

3.5

9.6

22.7

S&P 500

(0.5)

(2.5)

6.2

28.9

Peer group median

(0.4)

(3.1)

4.0

27.1

Source: Bloomberg

Figure 8 shows BRAI’s month-by-month relative returns and highlights the strong run of outperformance achieved over the past six months.

Figure 8: BRAI NAV total return relative performance by month

Source: Bloomberg, Marten & Co

The trust has clearly got off to a great start under its new investment approach, delivering outperformance of its benchmark and ahead of its peers. In 2025 it was the top performing North American equity trust in the peer group, and it continues to be the top performer over last 12 months. This may reflect the shift back towards a more fundamentally driven market that the manager has noted.

Figure 9: Attribution by sector

Source: BRAI

Figure 10: Attribution by signal

Source: BRAI

The manager highlights that the portfolio has done well in periods of volatile markets, when dislocations have created mispricing opportunities. We observe that BRAI’s returns are also less volatile than those of its benchmark, with a standard deviation of 9.9% since the strategy change versus 10.3% for the index.

In Figure 9, the yellow dots represent BRAI’s average active overweight and underweights relative to the benchmark and the bars illustrate the contributions by sector to BRAI’s returns over this period.

Figure 10 breaks down the source of relative return by signal. Helpfully, all three made positive contributions, but market sentiment driven stock selection signals had the greatest impact. Here the manager stresses the importance of being aware of where retail money was flowing (a lesson learned from the meme stock phenomenon over 2024 and into 2025). These flows do not necessarily identify the best long-term performers, but can materially distort short-term returns.

Dividends

New enhanced dividend policy roughly 6% of NAV each year

BRAI has long paid part of its dividend out of capital. However, with effect from 17 April 2025, BRAI adopted a policy of paying a quarterly dividend equivalent to 1.5% of NAV (approximately 6% annually). Without the constraint of having to hold high-yielding stocks to generate its income, BRAI is free to go anywhere within the US market and try to maximise its total returns.

The x-axis labels show historic ex dates for BRAI’s dividends. Going forward, the intention is to pay the dividends in April, July, October, and January.

Figure 11 shows BRAI’s dividend history over the last five years. We now have 12 months of dividends declared under the new system totalling 13.25p.

Figure 11: BRAI five-year dividend history for financial years ending in October

Source: BRAI, Marten & Co

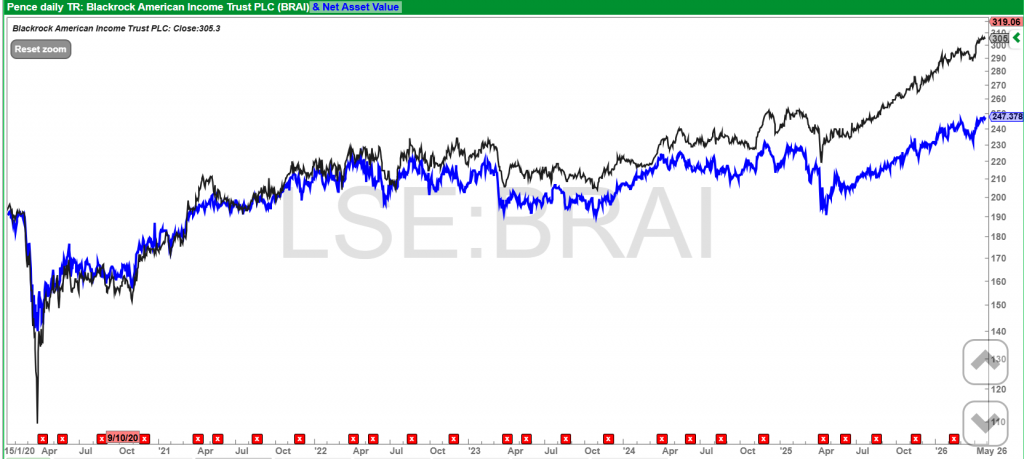

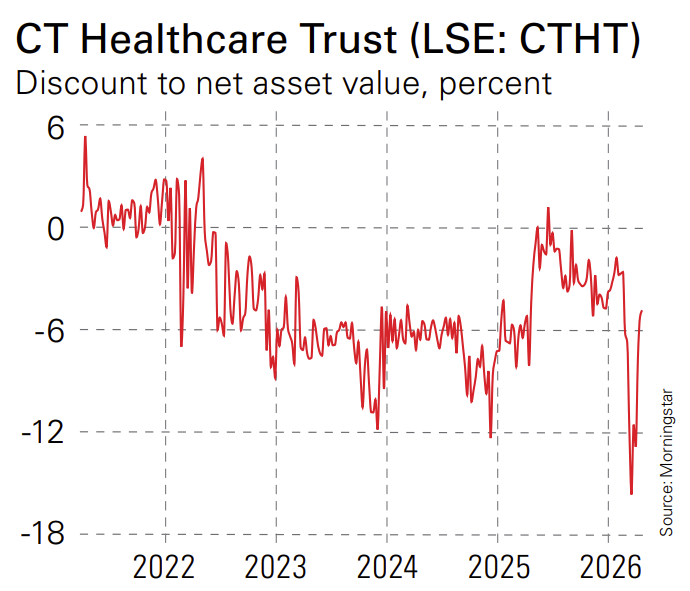

Premium/(discount)

Over the 12 months ended 31 January 2026, BRAI’s shares traded between 9.1% discount to NAV and a 1.2% premium and averaged a discount of 4.8%. By25 February 2026, the discount had been eliminated.

Figure 12: BRAI’s premium/(discount) over the five years ended 31 January 2026

Source: Bloomberg, Marten & Co

As we explained in our previous note, the widening discount over 2023 came as the Magnificent Seven dominated markets and value stocks underperformed. BRAI’s rating began to improve in October 2024, initially in anticipation of a tender offer. Since then, it has continued to narrow and is currently trading close to asset value or at a premium. The board is keen for the trust to re-expand and has powers to issue stock at a premium to NAV, which would enhance the NAV for existing shareholders and improve liquidity in the shares. It would also have the effect of spreading BRAI’s fixed overheads over a wider base, lowering its average running costs.

Conditional tender offers

If BRAI fails to beat its benchmark net of fees by an average of 0.5% per annum over three-year periods, the first of which ends on 30 April 2028, the company has committed to offering shareholders a 100% tender offer at a 2% discount to NAV less costs. In addition, the 100% tender offer may also be triggered if the net assets of the company are less than £125m at the end of those three-year periods.

SWOT and bull vs. bear analysis

Figure 13: SWOT analysis

Strengths

Weaknesses

Differentiated investment proposition

Investors need to get comfortable with the investment approach

Enhanced income whilst maintaining risk-controlled exposure to US equities

Encouraging early performance

Relatively low market cap restricts attraction for wealth managers

Considerable backing of BlackRock

Opportunities

Threats

Discount has been eliminated, potential for a re-expansion of the trust

Persistent US dollar weakness undermines attractions for UK investors

Recent market moves mean that US investors are thinking more about diversification

AI could continue to dominate the investment agenda, perpetuating the outperformance of growth stocks

Value is overdue a return to favour

Source: Marten & Co

Figure 14: Bull versus bear case

Bull

Bear

Performance

Off to a great start with fairly consistent outperformance and lower volatility

AI resurgence could depress value stocks further

Dividends

Dividend policy results in attractive yield

If markets fell for an extended period, the dividend policy would shrink the capital base of the company

Outlook

Value is picking up and a more decisive shift in sentiment could help extend BRAI’s run of good relative performance

Weak dollar and return to outperformance by growth stocks are both possibilities

Discount

Appears to be under control

Small size reduces the impact of buybacks as liquidity worsens

Source: Marten & Co

Important Information

This marketing communication has been prepared for BlackRock American Income Trust Plc by Marten & Co (which is authorised and regulated by the Financial Conduct Authority) and is non-independent research as defined under Article 36 of the Commission Delegated Regulation (EU) 2017/565 of 25 April 2016 supplementing the Markets in Financial Instruments Directive (MIFID).

The SNOWBALL will earn repeatable income this year of around £11,000 on invested capital of 100k, no new funds will be added to the SNOWBALL, only the income earned. The actual income figure will be higher as it includes some special dividends. Whilst no dividend is 100% secure, some dividends are more ‘secure’ than others.

Annuity

Option take out an annuity currently yielding 7% but you have to surrender your capital. A huge gamble as you are relying on a known unknown, interest rates at the time your retire.

Canada Life figures show the 65-year-old with a £100,000 pension pot could buy an annuity linked to the retail price index (RPI) that would generate a starting annual income of £3,896. That’s up from £2,195 in the New Year following a 77% spike in rates this year.

Oct 22

The 4% rule.

If interest rates are low at your retirement date you could use the 4% rule.

The SNOWBALL has a comparison share VWRP, where 100k of capital invested on the same date as the SNOWBALL is valued at £158,963. Not too shabby, so could be an option for the tax free part of your pension retirement plan. Not advice DYOR as buying near the end of a major bull run could be very expensive.

The equivalent income would be £6,358.00.

Let’s jump forward ten years to a retirement date.

The SNOWBALL will have income of 20k plus, the amount is predictable, the time scale may vary. Once you have achieved the income in your plan, you could re-invest your dividends into ‘safer’ Trusts, like Dividend Heroes especially when Mr. Market is helpful, or higher coupons Gilts where the income is risk free, if you hold to maturity. Or invest in REIT’s where the values fluctuate but the income is ‘secure’.

A pension of 20%.

To receive the same income using Rule4 VWRP’s value would have to be £500k. GL with that gamble.

If you invest for the long term, hopefully you will have one or two Trusts that you can withdraw your capital from, re-invest that capital in higher yielders, it may have to be ETF’s and continue to receive income from at a cost of zero, zilch, nothing.

Remember no dividend is completely ‘secure’ but some dividends are more secure than others. The more shares you own the bigger the risk of owning a clunker but that risk is even bigger if you own only a couple of shares.

The SNOWBALL aims to own around ten positions but as the SNOWBALL matures the number of positions could increase.

Managing your money in retirement comes with significant challenges, including the risk of overspending and running out of funds in old age. Cost-of-living pressures have only made things more difficult in recent years.

A comfortable retirement now costs a single person £43,900 per year, according to figures from trade association Pensions UK. This has risen from £33,000 in 2019, before the pandemic sparked the highest level of inflation in a generation.

These figures do not include housing costs, so anyone still renting or paying a mortgage in retirement could face even higher outgoings.

With this in mind, it is unsurprising that one in five adults worry their pension won’t provide enough income in retirement, according to research from Nottingham Building Society. This rises to more than one in four among over-60s (28%).

Some use their pension savings to buy an annuity, giving them a guaranteed income for life (depending on the product you buy). However, the amount you qualify for depends on the size of your pension pot.

Others opt for pension drawdown in the hope it will give them better value for money – but the risk is that they could outlive their savings.

“If you aren’t sure how to go about this, it’s worth considering employing a regulated financial adviser to help you navigate what can be complex choices.”

The lottery effect – overspending early on in retirement

Poor financial planning can create problems for those who opt for drawdown, with some retirees overspending early on in retirement and leaving themselves short towards the end – a time when outgoings can shoot up thanks to care costs.

Last year, a study by Legal & General (L&G) found that some retirees were at risk of emptying their pension pot a decade early, after taking large cash lump sums and withdrawing too much in monthly income.

Savers generally expect their pension pot to last 22 years from age 60, according to L&G’s analysis, taking them to around 82. But for those who may not have other sources of income, such as property wealth or a defined benefit pension, it typically runs out by age 77. Both fall short of the average life expectancy, which is 86 for those who are currently age 60.

“For most people, their pension pot is the largest sum of money they’ll have access to, and after decades of hard work and saving, it’s natural to view it as a well-deserved reward,” said Katharine Photiou, managing director of workplace savings at L&G.

“However, our research shows the sudden financial freedom can trigger ‘The Lottery Effect’ for some savers, which can lead to unsustainable spending.”

Golden rules to avoid retirement shortfall

1. Make a plan before taking your tax-free cash

Once you turn 55, you can access your pension and are entitled to take 25% of your savings as tax-free cash. Some rush to withdraw this straightaway as one lump sum, but that can be a mistake.

When you withdraw money from your pension, you take it out of a tax-efficient environment and move it into one where a tax bill may be generated – for example on savings interest, or dividends and capital gains if you decide to reinvest the money

Withdrawing your tax-free cash and sticking it in a savings account also means you miss out on the potential for future investment growth.

It is better to have a plan for what you are going to do with the money. Some use it to pay off their mortgage, for example, so they can retire debt-free. Everyone’s personal circumstances are different, so it is worth seeking financial guidance or advice.

Remember: you don’t need to take all of your tax-free cash in one go. You can take it in instalments if you prefer. This means the money remains invested for longer and can hopefully continue to grow.

2. Build up your emergency savings

Everyone should have an emergency savings pot to cover unforeseen costs. Those who are working should have enough to cover one-to-three months’ worth of essential expenses, but this rises to one-to-three years among retirees. It is generally advisable to keep this in an easy-access account.

If you haven’t got enough in emergency cash savings as you head into retirement, should you use your pension tax-free cash to top it up? Helen Morrissey, head of retirement analysis at investment platform Hargreaves Lansdown, says it depends on your circumstances.

She told MoneyWeek: “If someone is in drawdown and needs a buffer to help them maintain income during periods of market volatility, then they could look at having 1-3 years’ worth of emergency savings.”

If they also have income from an annuity or a defined benefit pension, they might be able to keep less in their emergency cash reserve, leaving more invested in their pension.

“The decision to take tax-free cash to top up emergency funds will also depend on wider issues such as access to other assets, size of estate given the upcoming inclusion of pensions as part of people’s estate for inheritance tax, as well as wider planning issues,” Morrissey said. “If in doubt, people should seek financial advice.”

3. Think about how much income you need

A cash management strategy is important. How much income do you need to live on, and is your pension pot big enough to sustain you for as long as you might live? Some people adopt the 4% pension rule – a guideline that can be used to help you draw a sustainable retirement income for around 30 years.

This rule suggests you can withdraw 4% of your pension in your first year of retirement. In all subsequent years, you can withdraw the same amount but adjust for inflation. If you had a £500,000 pension, this would mean taking £20,000 in the first year. If inflation was around 2%, you would then take £20,400 out the second year, £20,808 out the third year, and so on.

There are pros and cons to the rule, as we explore in a separate piece. If you are in a position to seek tailored financial advice, that is usually the best approach, as a financial adviser will be able to help with cash-flow modelling.

4. Consider combining drawdown with an annuity

Pension drawdown is a more popular option than buying an annuity, based on FCA data. While the idea of guaranteed income is appealing, many dislike the idea that an insurer will profit from their life’s savings if they die shortly after purchasing the annuity contract. Meanwhile, your loved ones can inherit any unused pension savings.

That said, annuity rates currently look attractive and can give you peace of mind, offering guaranteed income until you die. Recent data from Hargreaves Lansdown’s annuity search engine shows a 65-year-old with a £100,000 pension can get up to £7,793 per year from a single-life level annuity with a five-year guarantee.

Savers don’t need to choose between the two approaches. A combination of the two can be a good strategy. “This mix and match approach means you can secure the income you absolutely need from an annuity, and also keep some invested for growth in a drawdown plan which provides a more variable, flexible income,” said Laith Khalaf, head of investment analysis at AJ Bell.

Investment trusts with wide discounts can use tenders and buybacks to close the gap. But these aren’t a sustainable solution and don’t produce the best outcome for investors.

By Cris Sholto Heaton

(Image credit: Getty Images)

Many investment trusts have become very rattled by the threat of activist investors and are concerned about reducing their discount to net asset value (NAV). This is mostly good: some boards had become too dozy about putting the interests of their investors first and more attention to structural discounts was overdue.

Still, it is also clear that many investment trust boards are convincing themselves that regular share buybacks and tender offers (an offer to buy shareholders’ shares) are the best way to keep discounts down. As a shareholder in a number of investment trusts, I am far from convinced that this always produces the best outcome for investors like me.

The rules for investment trusts with wide discounts

Wide discounts can reflect a range of factors, including poor performance, doubts about the reported NAV, being in a sector that’s out of favour, or the investment trust being too small and/or illiquid. Tenders and buybacks can do nothing for the first three: if the problem persists, you may need to change manager, change strategy, find ways to prove the NAV, or just wait for your market to become popular again.

Get 6 free issues + a free water bottle

Stay ahead of the curve with MoneyWeek magazine and enjoy the latest financial news and expert analysis, plus 58% off after your trial.

Meanwhile, the fourth scenario is why too many buybacks and tenders can even be actively harmful. They shrink the size of the fund, which will make it less attractive to many investors. Even an investment trust that starts at a healthy size can shrink itself into irrelevance if it gets hooked on buybacks and tenders in a vain attempt to control a discount driven by other factors. Consider Bellevue Healthcare (now CT Healthcare), which peaked at around £1 billion in 2021, but had dwindled to under £300 million by 2025, without really reducing the discount.

Who benefits the most from buybacks and tenders?

The other question is who benefits most from buybacks and tenders. Buybacks are at least accretive to remaining shareholders if the price is genuinely below net asset value. Still, I am cautious about trusts that decide to sell illiquid assets in weak markets to fund buybacks, because they may be selling the best assets and leaving the fund with the junk that is less likely to be worth its carrying value.

Since tenders typically happen near NAV, they are not directly accretive. True, long-term investors could take up each tender offer to the limit allowed, take the proceeds, and use them to buy shares more cheaply in the open market again – but many won’t. So the beneficiaries here are often influential shareholders – activists or institutions – who want a chance to exit at a preferential price. If the discount does not then shrink and the trust becomes smaller and less viable, long-term holders have been left worse off by the whole process.

This does not mean that tenders and buybacks are always bad – but they need to be structured in a way that limits these disadvantages. A large exit opportunity every five years, perhaps triggered only if the fund underperforms, is fairer to all investors – not just those who want to cash out – than constantly shrinking the assets.

The Independent

The Independent