Young Caucasian girl showing and pointing up with fingers number three against yellow background© Provided by The Motley Fool

Story by John Fieldsend 1 Year ago

How much more money would I have if I’d avoided every ISA mistake I made? Probably a fair bit, sadly. I can’t have my time again, but I can share what I have learnt here.

No early bird

The first time I had a bit of cash to spare was at 16, thanks to an unglamorous role at the local Kentucky Fried Chicken. Many hours assembling Zinger burgers and salting french fries netted me a few hundred quid a month. What did I spend it on ? I can’t even remember.

Perfectly balanced

My second ISA mistake was thinking that stocks and markets would even out. The US and other Western countries had been dominant, so why not look at China and developing countries instead? Why not look at stagnating companies over high-flying ones? They were bound to catch up, weren’t they?

Billionaire investor Warren Buffett would have had a field day with me. One of his most famous quips is: “For 240 years, it’s been a terrible mistake to bet against America.”

He could also point out that thriving stocks and stock markets stay near all-time highs. The FTSE 100 hit an all-time high this May. It’s still only a hair’s breadth away. The S&P 500 just hit an all-time high five minutes ago (as I write)!

Interest rates

My third ISA mistake was choosing the wrong type of account. I realised with a very visceral feeling how the first month returned around 40p, or so. Although modest, my life savings were in there. That I was getting nothing back for it felt like a gut punch.

Of course, I had opened a Cash ISA at near 0% interest rates. Had I known that these types of savings accounts don’t beat inflation by much – by design – then I might have looked elsewhere.

If I could roll back the years then the first step would be opening a Stocks and Shares ISA instead, and the second step would be going for an income stock like National Grid (LSE: NG). It’s a reliable dividend payer, yielding 5.24% at present. A steady and sizable stream of cash would be nice on its own but would also provide reassurance that my money was working for me.

Reliable really is the key word here too. The company has a monopoly on its UK operations which offer very stable cash flows. This allows the company to slowly increase dividends with its current 10-year growth rate at 2.9%.

The firm does face large capital expenditure as the country moves towards net zero obligations. Another downside is it’s a stock that will likely produce more income than growth in the years ahead. These are the main reasons it’s not in my portfolio today. But for the right kind of investor, this stock’s one to consider.

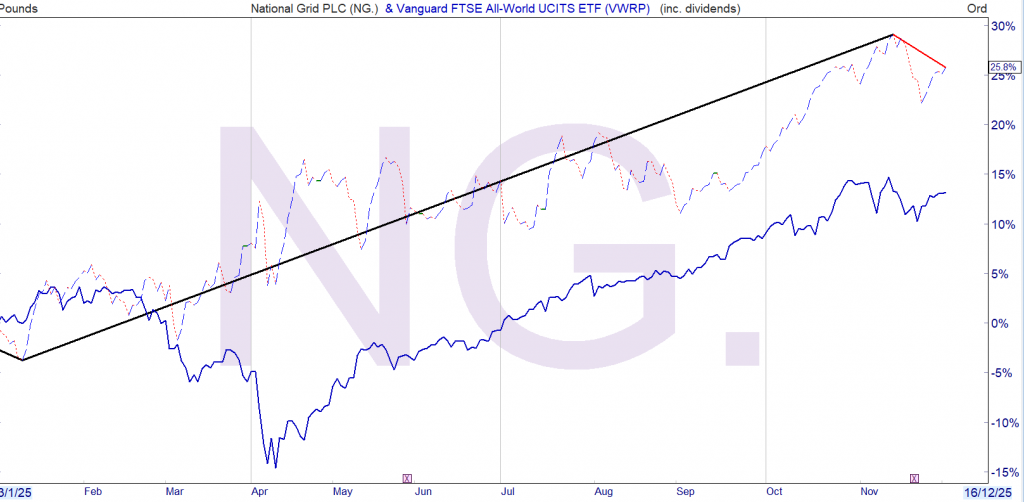

Note the date of the above article, NG has outperformed VWRP.

Leave a Reply