The ‘PACE’ Reits that protect you from AI disruption

By Hugh Moorhead

Investors’ Chronicle

The past year has been a blockbuster one for fans of financial market acronyms. Taco, which stands for ‘Trump always chickens out’ and dominated much of 2025, continues to cause investors whiplash as they follow developments in the Middle East.

More recently, Halo (‘heavy assets, low obsolescence’) emerged as a way to describe sectors that are less vulnerable to the perceived AI threat than those such as software.

A variation on this second theme is Pace (‘physical assets, compounding earnings’), which entails not just owning complex, tangible assets, but astutely operating them to consistently grow shareholder earnings and dividends.

“If Halo offers insulation from AI disruption, Pace may offer progression, and compounding,” says Matthew Norris, manager of the Gravis UK Listed Property fund, who coined the acronym.

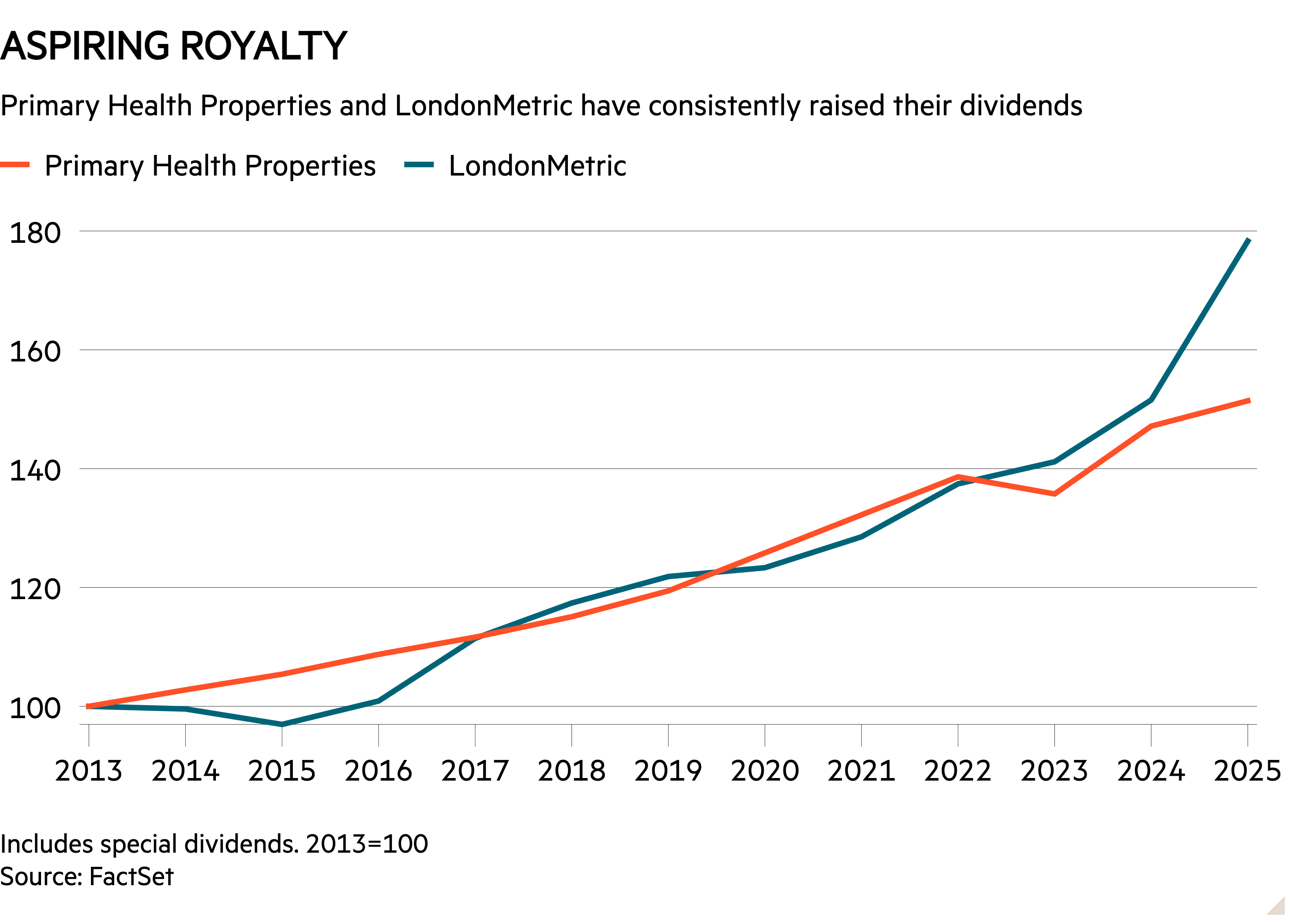

The UK’s listed real estate sector offers some pertinent examples. Primary Health Properties (PHP) operates a £6bn portfolio of GP surgeries and private hospitals in the UK and Ireland. These assets will remain essential infrastructure irrespective of what is happening in the broader global economy, and should be resilient to AI disruption, at least in the near term.

Two-fifths of PHP’s portfolio earns rents that are indexed to inflation or subject to fixed uplifts, albeit with many subject to ceilings as well as floors. The remainder are reviewed on an open-market basis, typically every third year, overseen by an independent district valuer.

The UK and Irish governments, unlikely to default on rents, account either directly or indirectly for three-quarters of PHP’s rental income.

“We have a very secure income stream and very stable asset class,” chief executive Mark Davies told Investors’ Chronicle on results day on 17 March.

The upshot of this security is that PHP is set to increase its ordinary dividend for the 30th consecutive year in 2026, and openly covets ‘dividend king’ status (50 consecutive rises).

Rents on smaller peer Target Healthcare Reit’s (THRL) £900mn portfolio of care homes are wholly indexed to inflation, again providing investors with protection should the conflict in the Middle East result in a persistent inflationary increase. This is also the case for Social Housing Reit’s (SOHO) £600mn portfolio of supported housing.

Target’s rental mix is far more weighted to the private sector. Yet the company argues that such tenants can more easily pass on rising costs, such as increases in the minimum wage, to customers.

In any case, its tenants’ rent cover – their ability to pay rents out of underlying operating profit – is very healthy, at just under two times.

A final example is LondonMetric (LMP). Its £7.4bn portfolio largely consists of ‘mission-critical’ assets, such as logistics premises, convenience stores and private hospitals.

Its tenants sign long-duration ‘triple-net’ leases, where the tenant takes responsibility for property taxes, insurance and maintenance costs. Two-thirds of its rental income comes from contracts indexed to inflation or with fixed uplifts. The company has doubled its ordinary dividend in just 13 years as a result.

Not all of its portfolio is as defensive, however, with 20 per cent comprising leisure assets such as hotels and theme parks. The company likes these because they are difficult to replicate and play into consumers’ growing preference for experiences over goods, but their tenants could still run into trouble if those consumers were to aggressively tighten their belts during an economic downturn.

While these companies’ physical assets and income streams should leave them well-placed to grow earnings regardless of any wider economic or technological disruption, investors should also bear in mind the outside risk of rising rates – and debt costs – impounding the compounders.

Leave a Reply