SEIT; go on say it

Proof-point Clues and Clueless Views

The Oak Bloke

Apr 12

Dear reader

Last week down -17% since its inclusion in the OB25 for 25, I declared I’m going to go in large here with proceeds from my imaginary “25 for 25” portfolio. 20% of the 25 for 25 makes it the largest single idea. A bold move. Or brash too?

Brash? £1k bought at 50p in 2025 and £10.3k added at 42p in 2026 means I’m in at a 42.6p average buy. I’m pretty happy with that.

Days later SEIT declares it’s going into wind down.

Readers have asked what do you think about that OB?

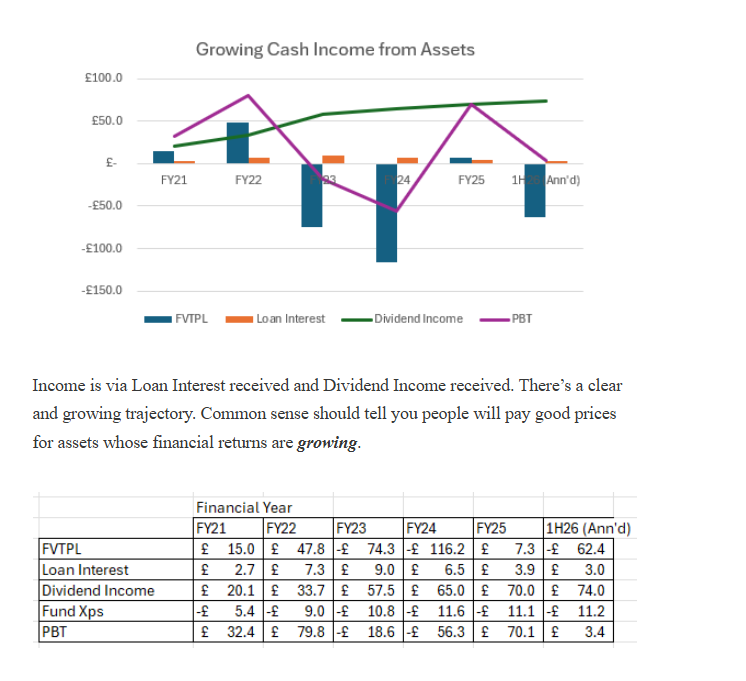

Beyond the obvious disappointment that it has come to this, the present reality is still that it is a share you can buy for 42p which is yielding a 6.36p dividend per year, so delivering a 15% yield 92% covered by actual earnings (topped up by capital returns) and is delivering a growing cash income where the “fair value” noise (in blue below) is blinding people to the growing income stream. If inflation rises, as seems likely, these energy assets generate inflation-linked income. Debt is fixed.

Meanwhile the negative “fair value” has essentially been driven by a growing discount rate taking this trust to a levered discount rate of 9.7% far beyond that of its peers. Hiding about £300m or 28p per share of NAV if the trust was valued at its discount rate in 2021 (while the assets are broadly identical to those of five years ago).

Five years ago 20% of the world’s Oil wasn’t cut off in the Persian Gulf. Energy is arguably far more valuable in a world where Oil and energy is on the cusp of a massive rise – in my opinion.

But we also now need to consider the wind down and the inevitable question:

How Easy will it be to Sell?

1 Red Rochester £246m or 23p a share

Proof Points:

Enwave is a district energy system which sold for a huge premium to NAV in 2021 (at the height of the market) for $2.8bn to Brookfield.

Vicinity Energy another district energy sold in October 2022 for 12X EBITDA

Vauban Infrastructure acquired Coriance in France in June 2023 at 15X EBITDA.

Antin acquired Veolia’s district energy business this month April 2026 for $1.25bn so at a 12.5X EBITDA.

According to Finerva valuations are rising, EBITDA multiple are rising.

EV/Multiples for green energy are back at 16X EV/EBITDA according to Finerva research.

Consider the growing EBITDA at Red-Rochester where even a 12X EBITDA implies a $500m price tag so a 50% premium to the gross portfolio value of $330m (as at 30/09/25).

Yet the market values Red Rochester at a 50% discount so at $114m + $102m debt = $216m

And $216m/$43.5m is a 5X EV/EBITDA.

Wait what?

Moving to views in the chattersphere where even getting 42p back is said to be “very difficult” and instead “we are going to have a fire sale”. Any evidence to that? No, just a haha.

2 Onyx £222.2m or 20p a share

We should consider Onyx as a developer-owner-operator so as three elements for sale.

2.1. The “YieldCo” (The Operational Portfolio)

This is the “safe” part of Onyx: 1,300+ operational projects across 30+ US states.

Primarily rooftop solar and carports for “Blue Chip” names like Walmart, Amazon, and Primo Brands. These have 15–20 year contracted Power Purchase Agreements (PPAs) with inflation-linked escalators.

Portfolio GAV Value $580m, project debt -$346m; NAV $233.8m or £187m

The portfolio is 211MW with 50% energised at the prior update September 2025, so an average value of $2.75m GAV per MW.

2.2 The “DevCo” (The Pipeline & Platform)

The Asset: Onyx has a ~500MW+ pipeline of projects in various stages of sign off and commercial business development.

Valuation: £35.2m or $47m.

Market Proof: In June 2025, Onyx secured a $260M financing facility (expandable to $350M). You don’t get a quarter-billion-dollar credit line from major banks unless your pipeline and platform have real, audited value.

2.3. The “New Frontiers” (Storage & EV Charging)

Onyx is no longer just “Solar Onyx.” It has moved heavily into BESS (Battery Energy Storage Systems) and EV Fleet Charging.

The Opportunity: Solar-plus-storage projects have higher EBITDA margins (often 10–15% higher) than standalone solar because they can “shift” energy to peak-price periods.

The Proof: The Maine project energised in Feb 2026 explicitly highlighted its “behind-the-meter” non-export design, which is the high-value sweet spot for industrial users.

2.4. Reduction (-$83m/-£63m/-5.8p)

Arguably you could say that with SEIT in wind down, Onyx will be unable to fund any development after 2027. This is described as -5.8p a share for SEIT (the -2.5p is part of the -5.8p before you let detractors double count).

It’s not necessarily a foregone conclusion when Onyx can (and has) borrowed from other parties, potentially extend facilities (keeping debt to EBITDA in proportion) and also can recycle cashflow into new projects theoretically but let’s assume it can’t and that its owner SEIT shall suck all cash flow out. We are in wind down now.

So Onyx is worth only 14.2p or £159m net of the -5.8p per share development platform aspect and boasting a 211MW portfolio the PPA’s are valued at £0.75m NAV each MW and £2.4m ($3.2m) per MW GAV.

The US C&I (Commercial & Industrial) solar market is currently seeing a wave of consolidation. Big “aggregators” are buying smaller portfolios to get scale. C&I are very lucrative containing SREC (solar renewable energy certificates – which are State level subsidies – nothing to do with Trump) selling energy at a retail price $90/MW not wholesale price ($30/MW).

Notice the vast difference in revenue per MWh for retail solar vs utility solar which this detractor invested heavily in making “substantial loses”. As I said 12 months ago Ecofin is not a good proof point to Onyx. It’s a very different business model – even if both are “solar”.

Better – and recent – examples of C&I/retail deals are Altus Power December 2025 buying 234MW at $2.8m per MW, TPG in April 2025 buying 1.3GW at $3m per MW

So ironically, the above values suggest that while the development platform might wipe -5.8p from the NAV the current portfolio if it sells for $3m per MW (net of costs) would be worth $633m. Minus paying off the -$346m debt such a deal leaves SEIT with $287m or £215m which is an overall -2.9% haircut vs today’s NAV.

So the operating portfolio is worth MORE than its NAV on a read across basis.

That further assumes the Onyx development platform really is worth zero and essentially ceases trading in April 2026.

2.5 The Counter View

Of course the alternative explanation from that “heavy loses” detractor is that Onyx is a “landmine waiting to explode”.

How do energised solar panels and battery storage on a 20 year PPA which generate contracted returns explode? The detractor doesn’t explain his peculiar view. Just that EBITDA is “tiny” and the business is capital hungry. The business is building capital equipment and providing those at a retail rate below that of retail grid power (Solar Energy Assets and Power Storage). Surely that person understands that assets under construction do not generate EBITDA – which is the majority as at the 1H26 results.

So yes, there is initial capex, and a delay to seeing EBITDA results, it’s true. But once energised how capital hungry are solar and BESS assets? About $15 per KW per year consisting of monitoring, inspections, panel cleaning, inverter replacement and corrective repairs so for a 100KW rooftop system that’s $30k over two decades per MW.

Assuming 1500 MWh generation per MW and $100 per MWh that’s $150k per year or $3m. SREC adds $10 per MWh so $15k or $0.3m on top over 20 years. EBITDA is highly attractive at those rates.

Does a post-construction capex spend equal to 1% of revenue make Onyx’ operational portfolio “capital hungry”?! Remember we’re assuming no development at Onyx wiping -5.8p per share for no new development.

So as projects in construction are energised capex reduces to a tiny 1% trickle and yes it pays its own way. So the “landmine” is a little box that flaps up a little boom flag. Onyx becomes more boon than boom.

Why do you think Infrastructure Funds buy up these energised portfolios? They are hugely cash generative and you can apply leverage to generate substantial returns. Go and read the $ trillion dollar accounts of those large funds – I have.

3 Primary £222m or 20% of NAV

Nippon Steel has undertaken to invest $3bn into US Steel, Primary’s customer. Nippon is wholly reliant on the continuation of Primary to operate its US mill in Indiana. It is an essential asset.

We already established district heating is valued at 12X EBITDA+ and EBITDA is $40m implying a $480m GAV minus -$150m project debt implies $330m or £250m. So about 10% higher than the NAV.

At a -50% discount the market is valuing Primary as being worth £110m + £110m debt so 6.8X EV/EBITDA

That valuation makes no sense.

4 Driva £82m or 6% of NAV

There are several comparatives we can use.

4.1.Solör Bioenergy / E.ON Vallentuna (July 2025) – In mid-2025, Solör Bioenergy (a major Nordic aggregator) acquired the district heating network in Vallentuna (just north of Stockholm) from E.ON. This is ~67 GWh network serving 240+ customers. M&A Insights cited an implied EV/EBITDA multiple of 12.0x.

Vallentuna is geographically adjacent to Driva’s Stockholm-centric assets and shares the same “alternative pricing” model where prices are benchmarked against electricity costs.

4.2.Strängnäs Municipality (Solör Acquisition) – Though older (2021), this remains the anchor for municipal-to-private transactions in the Stockholm region. The deal was at EV/EBITDA Multiple: 11.4x.

Why Driva is Higher: Driva is a private platform (not a single municipality utility), which carries a “Private Ownership Premium.” As highlighted in the Lundin (2025) study on Swedish heating pricing, private firms charge roughly 7% more on average than municipal ones, leading to higher margins and, consequently, higher valuation multiples (12x–14x).

4.3. Stockholm Exergi (March 2026) is the “Giant” of the region (80% market share). Its 2025 Year-End Report (published March 2026) provides the secondary market data used to value Driva.

Projected EBITDA (2026): SEK 3.3bn – 3.5bn.

Enterprise Value (Market Derived): Based on recent private stake valuations (AP6/Ancala), the implied multiple for a premium Stockholm asset is 14.5x – 16.0x EBITDA.

BECCS Premium: A portion of this multiple is driven by Bio-CCS (Carbon Capture). Since Driva is smaller and more localized, it trades at a 2-3 turn discount to Exergi, placing Driva firmly in the 12.5x – 13x range.

Driva generated SEK84m in 2025 (annualising the 1H25 result). That’s £6.7m. Taking £82m NAV and £54m debt that’s a £136m GAV so a 21.9X EBITDA valuation.

Typically for regulated assets valuation is at 1.2x to 1.5x its regulated asset value.

But let’s assume 12X EBITDA and that EBITDA cannot grow from the £3.35m result in 1H25. That implies a -68% haircut and again assumes zero growth and zero valuation to the growth which we see at Driva’s website such as new wins in 2026 like Nordquist’s coffee facility

5 Oliva

Oliva’s EBITDA profits have varied between $6.2m (1H25 annualised) and $68.8m (FY23) and its base-load power is sought after in the current market. The £35m valuation implies a 0.7X to 7X EV/EBITDA.

It will be good to see the FY26 results to March 2026 to understand the outcome of the turnaround at Oliva.

6 Other Holdings (the Non-Top 5)

LEDs provided under a PPA to large corporates, co-gen, solar, BESS, EPCs, biomethane, energy saving – these aren’t unusual assets that are difficult to sell.

They are all valuable assets particularly in a world of higher energy prices. Year on year electricity is 20%-30% higher across most of Europe. With Data Centers and AI electricity is no longer dirt cheap in the USA either.

£250.7m NAV and £18m non-big 5 project level debt means an EV of £268.7m and £19.1m EBITDA is a 14X EV/EBITDA. Based upon read across from the recent sale of similar assets this is “about right”.

At a 50% discount £125m +£18m debt the market values this at £143m EV/EBITDA so at an EV/EBITDA of 7.5X.

7 Conclusion

Yes, you could potentially point to certain assets where a slight haircut to NAV is possible. And yes, there are going to be sale costs of a few percent, and yes perhaps in the interests of winding things up speed vs return will be balanced.

But there are plenty of proof points backing the majority of assets and clearly we are in a world in 2026 where energy has grown in importance.

There are plenty of asset realisation examples valued at at least 12X EV/EBITDA. Reasons to think more than 12X is possible too. Show me where sales are going through at 6X EV/EBITDA? You can’t, because they aren’t any.

Landmines? Fire Sales? Give me a break. Try putting together a serious case that backs up your view.

Sales may not materialise overnight and SEIT have not been able to rapidly sell assets until now, but deals are being done out there for assets not dissimilar to those held by SEIT. To describe them as having “no strategic value” reflects more on such people’s understanding of strategy than on the assets.

Do I regret picking SEIT shortly before the news of the wind down? Not at all. Bring it on. Meanwhile SEIT can continue to deliver a strong dividend although if they announce they are focusing on paying down the RCF I for one, won’t be displeased. Once the RCF is gone they could engage in vast buy backs and those or tenders will be hugely accretive given the 50% discount – or the 65% discount if you agree with the harshness of SEIT’s 9.7% discount rate.

Regards

The Oak Bloke

Disclaimers:

This is not advice – you make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as “blue chip”

Disclosures:

I have no commercial connection nor receive any remuneration from any company I write about.

Thanks for reading! Subscribe for free to receive new posts and support my work.

© 2026 The Oak Bloke

548 Market Street PMB 72296, San Francisco, CA 94104

Leave a Reply