GPIQ: Goldman Sachs Built The Income ETF I Wish Existed 5 Years Ago

Apr 10, 2026, 8:30 AM ETGoldman Sachs Nasdaq-100 Premium Income ETF (GPIQ)NVDA, AAPL, JEPQ, QQQ

Steven Fiorillo

Summary

- The Goldman Sachs Nasdaq-100 Premium Income ETF offers a dynamic covered call strategy, delivering a 10.42% yield and strong total returns since inception.

- GPIQ’s flexible overwrite approach allows active adjustment of call coverage, capturing elevated option premiums during volatility while retaining upside exposure.

- Tax-advantaged distributions and a tech-heavy portfolio position GPIQ as a compelling income vehicle, particularly in uncertain or volatile markets.

- I remain bullish on GPIQ, adding to my position as its structure thrives amid elevated volatility and upcoming earnings uncertainty.

I have been investing in and writing about income-producing assets for a long time now. I have an entire segment of the portfolio structured around generating cash flow from equities. I spend quite a bit of time tracking and analyzing my income producing assets and I believe that the current market environment is an attractive entry point for long-term investors into income producing assets. The big thing about covered call strategy ETFs that people trend to glance over is that they are not conservative vehicles for people afraid of stocks just because they have a large distribution yield. They are structured to pay out a large amount of income for capping some of your upside during periods when nobody knows what is coming next.

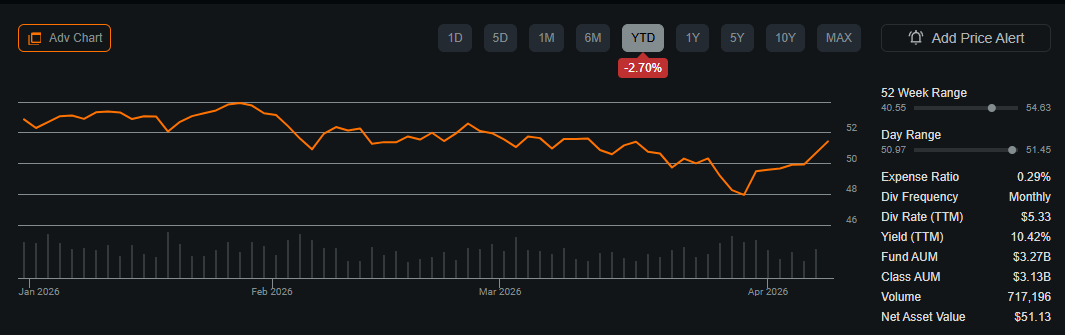

I believe that the Goldman Sachs Nasdaq-100 Premium Income ETF (GPIQ) is built for this exact moment. The Iranian conflict has caused the flow of roughly 20% of global oil supply to become constricted as the Strait of Hormuz has become the most important global choke point. We’re headed into the heart of Q1 2026 earnings with big banks setting the stage for big tech later in the month. The market is going to demand proof that Big Tech AI spending is translating into real revenue causing uncertainty which could translate to increased options premiums. GPIQ is paying a distribution of $5.33 which is a yield of roughly 10.42% at a time when GPIQ is only down -2.7% for the year. I think that GPIQ will continue to generate low double digit or high single digit yields while returning positive appreciation throughout the year.

Following up on my previous article about GPIQ

Back in November I had written an article on GPIQ (can be read here) and since then the total return is 2.82% due to the large distribution compared to the S”&P 500 gaining 1.69%. I felt that GPIQ offered a compelling blend of capital appreciation and double-digit yield as the dynamic covered call strategy left the upside partially uncapped. This allowed GPIQ to benefit from market appreciation while producing a large recurring income stream for investors. Despite the evolving Fed policy GPIQ’s distribution rate has been stable and I felt it had become more attractive in a failing rate environment. I am following up with a new article on GPIQ because I feel the current environment is creating opportunities for covered call ETFs especially with how uncertain the geopolitical landscape has been. In my opinion, GPIQ is built for periods like this as it can generate large amounts of recurring income when the market falls and follow the market higher on green days since a portion of the portfolio is uncapped.

What GPIQ Actually Is And How It Works

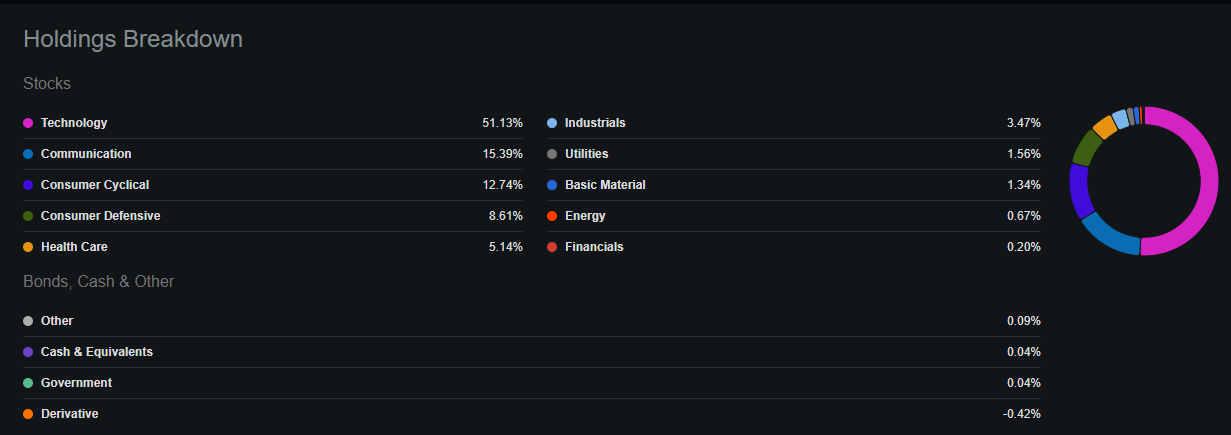

GPIQ launched in October 2023, so it does not have as long of a track record as some of the other covered call ETFs such as the Global X Nasdaq 100 Covered Call ETF (QYLD). While this isn’t a long enough timeframe for some investors what GPIQ does have is a clear and well executed strategy backed by Goldman Sachs Asset Management, and results that speak for themselves. GPIQ has constructed an equity portfolio that mirrors the Nasdaq-100 index. The top holdings look exactly like what you would expect with Nvidia Corporation (NVDA) representing 8.74% of the portfolio and Apple (AAPL) coming in at 7.67%. The tech sector makes up roughly 51% of the portfolio, with communication services at about 15% and 104 positions.

Where GPIQ gets interesting is the overlay segment of its strategy. It sells call options on anywhere between 25% and 75% of the underlying holdings which is the key differentiator. This is what Goldman calls a dynamic overwrite strategy which is significantly different than covered call ETFs operating at fixed percentages. QYLD writes calls on 100% of its portfolio every month while the JPMorgan Nasdaq Equity Premium Income ETF (JEPQ) utilizes equity-linked notes which have their own structural limitations. GPIQ can actively adjust how much of the portfolio is being overwritten based on market conditions which is what I like about it.

When volatility spikes and premiums expand, GPIQ has the ability to overwrite a larger portion of the portfolio. This allows them to collect larger premiums and deliver more income to shareholders. When the market trends higher GPIQ has the ability to reduce the overwrite percentage and let more of the underlying equity appreciation drive the share price higher. That flexibility is why GPIQ has managed to deliver both a double-digit yield and better total returns than most of its peers. GPIQ also utilizes FLEX options through the CBOE which are customizable exchange-traded option contracts. This gives the portfolio managers the ability to tailor strike prices and expiration dates in ways that standard listed options cannot match.

The taxed advantaged income profile is a benefit for income investors

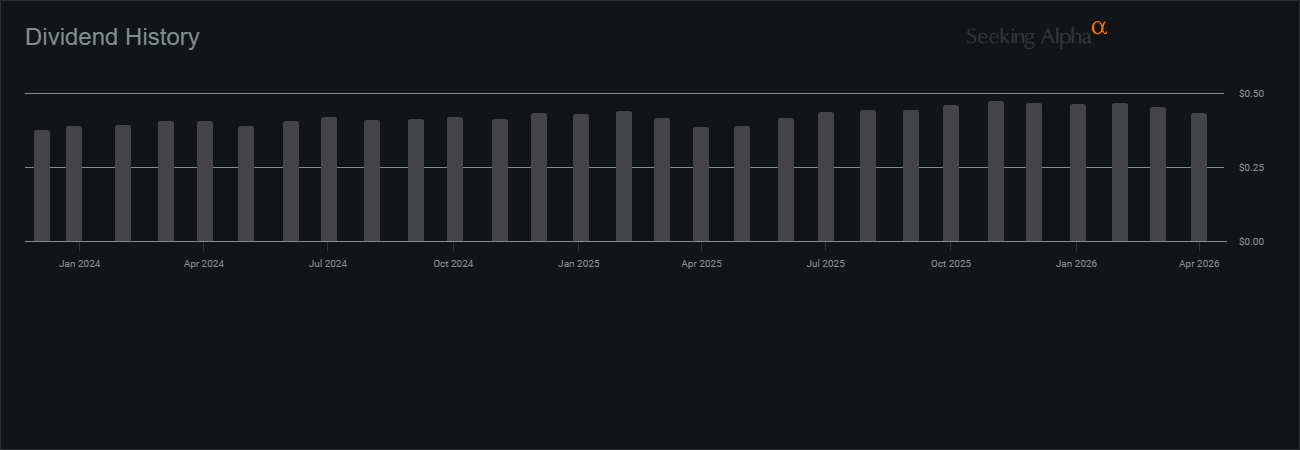

GPIQ has paid $5.33 in distributions over the trailing twelve months (TTM) which is a 10.42% yield. The part that doesn’t get enough attention is the tax treatment of these distributions. A large portion of the distributions get treated as return of capital because GPIQ uses index options that qualify for Section 1256 tax treatment. The gains are split on a 60/40 basis between long-term and short-term regardless of holding period. When I considered this against ETFs that are taxed as ordinary income GPIQ looks increasingly favorable especially at the end of the year when Uncle Same gets is fair share. For some investors this aspect can become extremely favorable especially when you have larger amounts of income being generated from the underlying investment.

Since the end of 2023 GPIQ has paid 29 monthly distributions which have amounted to $12.26 of income. GPIQ opened at $38.78 and since 2023 has appreciated by 32.70% while producing another 31.71% in monthly distributions. Since it went public GPIQ has generated a total return of 64.32%. When I look at the characteristics of GPIQ the dynamic income approach looks very appealing as the monthly distribution has averaged $0.42 over the past 29 months which is a monthly yield of 0.82% based on the current share price. From an income perspective this works in my portfolio and I am very bullish on GPIQ going forward because its structure will benefit when the geopolitical tensions finally get sorted out while maintaining an attractive yield compared to the risk free rate of return.

Why Earnings Season Makes The GPIQ idea Timely

Q1 2026 earnings season is about to get started as JPMorgan Chase (JPQ) will set the tone on Tuesday 4/14. Big tech will come right as we have the April FOMC meeting at the end of the month. The consensus expectations for the S&P 500 are about 13.2% YoY earnings growth for Q1. Technology has seen its YoY earnings growth rate increase to 45.1% from 34.3% on December 31st. The market is looking for another strong quarter from the names that dominate the Nasdaq-100 which would be beneficial for GPIQ. The March washout shook out a lot of the speculative froth causing a repricing of mega-cap tech. It looks like there has been a lot of AI fatigue and the market wants proof that the amount of capital being spent on CapEx is going to pay off. I think were setting up for a scenario where the companies that deliver strong results are going to get rewarded and we’re going back to good news is good news and bad news is bad news. This kind of dispersion would be beneficial for GPIQ’s covered calls strategy because it keeps implied volatility elevated across the index.

If the Magnificent 7 come in and report strong Q1 numbers, GPIQ would participate meaningfully in the upside because it can dial back its overwrite percentage. If earnings come in mixed and the market chops sideways or pulls back further it still has the ability to generate that 10% plus yield that everyone loves collecting. This is a setup where the fund gets paid either way and the only question is how much capital appreciation comes along with it. The reality is that nobody except the management teams know what these companies are going to produce and more importantly what they will guide for. What we do know is that the implied volatility embedded in Nasdaq-100 options right now is elevated relative to where it was for most of 2024 and early 2025. This has become a direct input as to how much income GPIQ can generate. When the VIX was sitting at 13 or 14, covered call funds had to work harder for their yield and now with the Vix over 20 the premiums are significantly larger.

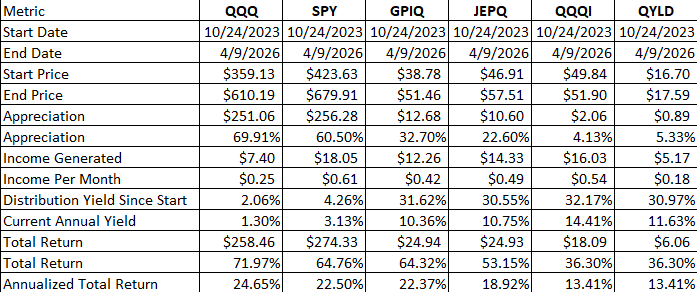

GPIQ is outperforming it’s peers since inception and it’s not even close

I compared GPIQ to the Invesco QQQ Trust (QQQ), the SPDR S&P 500 Trust (SPY), QYLD, JEPQ, and the Neos Nasdaq 100 High Income ETF (QQQI) since it’s first day of trading and the results were overwhelmingly bullish. The metrics that I track are the starting price, todays price, how much appreciation was generated, the amount of income produced, and what the total return was. All of the data is in the table below. I am not as shocked as some may be to learn that GPIQ has almost doubled the total return of QYLD and been able to maintain a total annualized return that has almost matched the market.

Since inception GPIQ has generated $12.68 of capital appreciation while producing $12.68 in distribution income. This has led to a total return of 64.32% from a combination of 32.70% appreciation and 31.62% in distribution yield. The annualized return on GPIQ has been 22.37%. SPY which is the benchmark has a total return of 64.76% over this period with a 22.50% annualized return. GPIQ’s performance is within a half of percent of SPY. QQQ which is the benchmark for the Nasdaq 100 has a total return of 71.97% with an annualized return of 24.65%. When I look at JEPQ, QQQI, and QYLD there is a huge drop off in total return since GPIQ hit the market. JEPQ has a total return of 53.18% while QQQI and QYLD both have the same total return at 36.30%. The data is clear and GPIQ is holding its own against the market and currently superior to its peers.

The risks to investing in GPIQ

Even though I am bullish on GPIQ there are several risks to consider. The first risk is concentration considering over 50% of this fund is in technology. If the Tech sector doesn’t perform this earnings season we could experience a multi-quarter bear market in tech which will impact GPIQ’s share price. The premium income provides a cushion but it’s not going to save investors from a large step down in Nasdaq 100. . During the April 2025 tariff shock, GPIQ fell roughly 25% peak to trough before recovering. Next, if we get a ripping bull market due to the geopolitical tensions easing then GPIQ will underperform QQQ as the The covered call overlay inherently caps some upside. That is the trade-off as investors are trading some capital appreciation potential for current income. If your goal is pure growth maximization GPIQ isn’t the right investment for you. The reality is that GPIQ has only been in existence for 2.5 years and we have not seen it navigate a prolonged recession or a sustained bear market. The dynamic overwrite strategy looks great in a volatile but ultimately recovering market but there is no data as to how its overwrite strategy will perform during a genuine downturn. Investors should do their own due diligence and make sure this strategy is right for them.

Conclusion

One of the things I think about is if I was going to build building an income-focused portfolio from scratch today would I want a vehicle that gives me exposure to the best companies while paying a double-digit yield that is tax-advantaged? The answer is yes and GPIQ checks off all the boxes especially in this market environment. We are in a market where volatility is elevated and earnings season is about to inject a fresh round of uncertainty. The Fed is not likely to cut rates and the geopolitical landscape is a mess. All of those factors push implied volatility higher which pushes option premiums higher and positively impacts GPIQ’s distribution income. GPIQ doesn’t need optimal conditions or a rising market to work and it’s built for the types of uncertain environments we’re living through. I am still bullish on GPIQ and adding to my position.

This article was written by

Steven Fiorillo

I am focused on growth and dividend income. My personal strategy revolves around setting myself up for an easy retirement by creating a portfolio which focuses on compounding dividend income and growth. Dividends are an intricate part of my strategy as I have structured my portfolio to have monthly dividend income which grows through dividend reinvestment and yearly increases.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of GPIQ, QYLD, JEPQ, QQQI, NVDA, AAPL either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Disclaimer: I am not an investment advisor or professional. This article is my own personal opinion and is not meant to be a recommendation of the purchase or sale of stock. The investments and strategies discussed within this article are solely my personal opinions and commentary on the subject. This article has been written for research and educational purposes only. Anything written in this article does not take into account the reader’s particular investment objectives, financial situation, needs, or personal circumstances and is not intended to be specific to you. Investors should conduct their own research before investing to see if the companies discussed in this article fit into their portfolio parameters. Just because something may be an enticing investment for myself or someone else, it may not be the correct investment for you.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Comments

Thanks @Steven Fiorillo for this article. I manage my portfolio a little differently than I used to as I now maintain at least one year of personal distributions (sometimes 2 years) in SGOV/JAAA. Then I set my investments to DRIP and mostly leave them alone. Sometimes, I’ll trim some of my CEFs to harvest a discount-premium swing and I’ll put those monies into my savings bucket.

For 2025 I invested in QQQI QDVO and SPYI. They did well and I had some nice gains but for 2026 I changed it up and exited QQQI QDVO entirely and put everything into GPIQ and SPYI.

So far GPIQ has been doing just as well as my previous split. SPYI is lagging a little YTD but I turned DRIP off in January for this fund to help add to my SGOV bucket since I took a distribution

Leave a Reply