We look at the dos and don’ts when picking trusts and suggest a starter portfolio to get you going

Published on April 15, 2026

by Val Cipriani

The dos and don’ts of picking a trust.

Portfolio upkeep.

A model portfolio to get you started

Can you build a whole portfolio using only investment trusts? To an extent, that depends on your needs, but for most investors, the answer would be ‘absolutely’. Indeed, at a time of high global uncertainty and market volatility, there’s something very reassuring about active management – and about an independent board keeping an eye on what those managers are doing.

Regardless of which type of fund you use, the key principles of portfolio construction remain the same: think about your time horizon and objectives, consider your risk appetite, then decide on a strategy and pick the investments to match it. You can gain access to a broad range of geographies and asset classes via investment trusts; if anything, the problem is that there is almost too much choice.

The dos and don’ts of picking a trust

The investment trust structure does, however, have some specific features that you need to keep in mind when constructing your portfolio.

Trusts trade as shares, so their size and liquidity matter. A trust that is too small can become difficult to sell. And there’s a lot of merger and acquisition activity in the sector at the moment, so a small trust is also more likely to disappear – either because it is absorbed by another trust or because the portfolio receives a cash offer from a third party.

The complete guide to buying investment trusts

If your goal is building a long-term buy-and-hold portfolio, you arguably shouldn’t obsess over discounts. Don’t ignore them, but you shouldn’t pick a trust just because it looks cheap, or just because you have reasons to hope the discount will close. This would be a nice-to-have boost, but ultimately the characteristics of the underlying portfolio are a lot more important in the long run.

On the other hand, you should be wary of buying a trust at a premium, especially at a time when most are discounted. Even a slight worsening of the portfolio performance can erase that premium very quickly, and turn the best-performing trust into a poor investment.

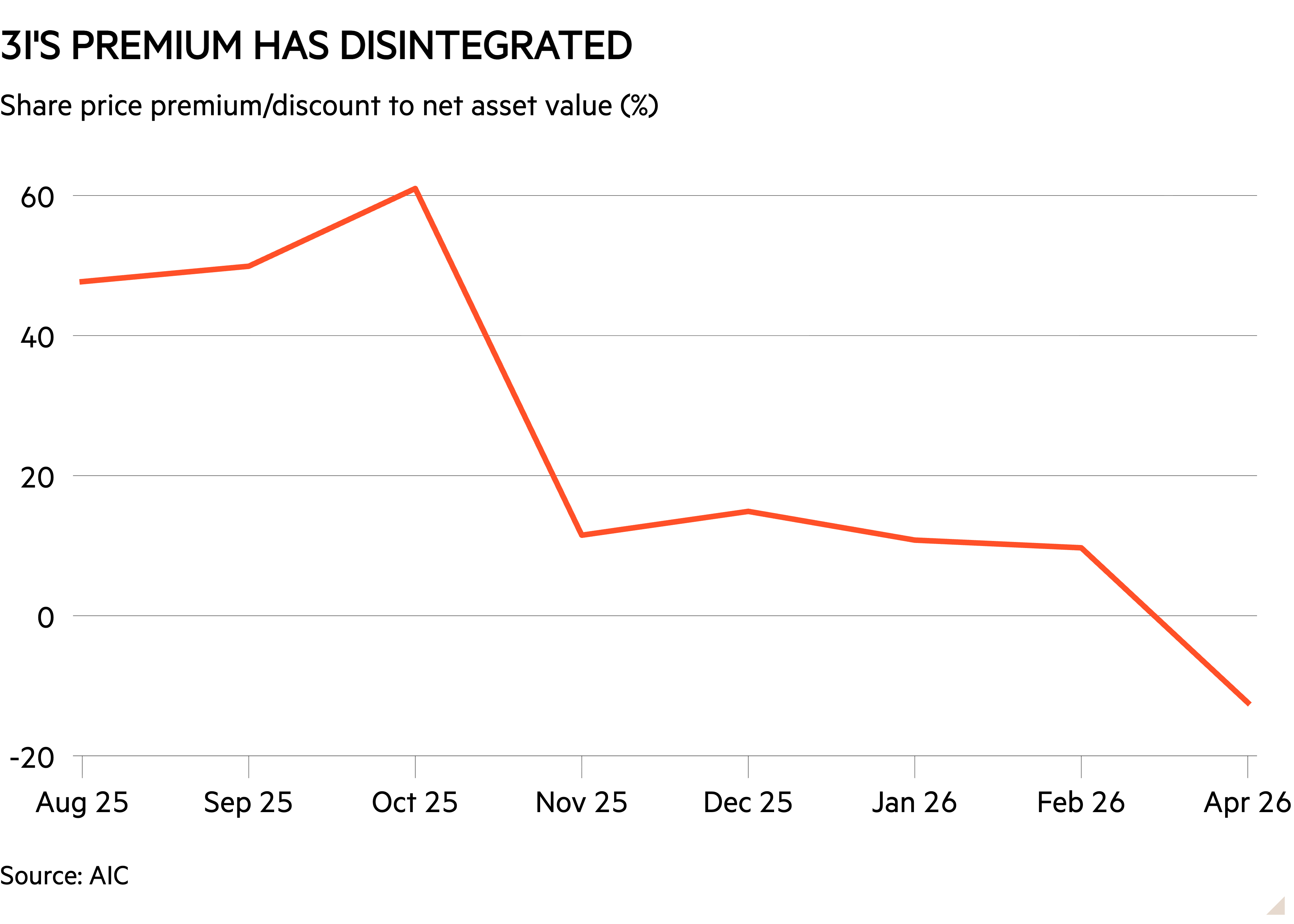

At the end of October 2025, private equity trust 3i Group (III) was trading at an eye-watering premium of 61 per cent. Then the outlook for its main holding, Dutch discount retailer Action, darkened a little. Fast-forward to the present day, and the trust is trading at a discount of about 12 per cent; investors who bought at the top of the market will be sitting on heavy losses.

“Trusts that move to trade on big premiums usually ring alarm bells for me,” says James Carthew, head of investment companies at QuotedData. However, he adds that it is worth checking whether the premium exists because the net asset value is out of date, which can happen when a trust holds unquoted underlying assets that are priced less frequently.

It is also worth thinking about how you can best exploit the investment trust structure for your investment goals. Do you need regular income that rises with inflation? You could pick a ‘dividend hero’, or one of the trusts with a long record of increasing its payout every year regardless of circumstances – City of London (CTY) is one example. Are you feeling especially bullish towards a certain sector or geography? Then pick a trust that deploys gearing for a more high-conviction approach.

Portfolio upkeep

Once your portfolio is up and running, the rule of thumb is to review it every six months, give or take. You are relatively safe just letting it be for the rest of the time. As Carthew puts it: “In theory, investment trusts are the ultimate ‘buy and forget’ investments – not that you should neglect to keep an eye on your portfolio, but you should at least be able to take comfort that if something is going wrong, the board (whether encouraged by activists or not) should step in and fix things, by changing the manager, for example.”

Of course, that doesn’t mean that you never sell. “Be very wary of attempts to force a change of remit or investment style on you,” he says. “If I have deliberately bought a ‘value’ trust and the board is trying to shift towards a ‘growth’ style because that is what is working currently, I’d most likely end up selling.”

And you can use your regular review to trim holdings that have done well, rebalancing your portfolio back to the original strategy. Carthew says: “A lot has been written over the years about the futility of trying to time markets, but I am a great believer in top-slicing things that have done really well, or at least thinking very hard about how large a percentage of your portfolio you want this trust to be, and looking for bargains among the trusts that everybody seems to hate.

“In momentum-driven markets that can feel like poor advice, but then circumstances change and you get to feel smug about selling something close to the top of its trading range.” He recently had this experience with Golden Prospect Precious Metals (GPM). The trust’s shares dropped about 11 per cent between the start of the war in Iran at the beginning of March and 8 April, as the gold price fell and its investment managers resigned.

A model portfolio to get you started

There are countless ways to build a portfolio of investment trusts, depending on your goals, needs and preferences.

We asked Ben Yearsley, investment director at Fairview Investing, to put together a basic trust portfolio that investors could use as a starting point.

The ideal investor for this portfolio is someone who has some knowledge of investing but is not yet a trust expert, and wants to keep things relatively simple. The goal is long-term growth, with a time horizon of 10 to 15 years, so investors need not be concerned about short-term volatility. Keeping trading costs low is an important consideration, so Yearsley has opted for just six trusts.

This portfolio blends various types of equity exposure, including a couple of pretty aggressive options, with two lower-risk holdings: Personal Assets (PNL) and International Public Partnerships (INPP).

Personal Assets is one of the so-called ‘wealth preservation’ trusts. It aims to protect your capital first, and grow it second, using a mixture of stocks, gold and bonds. Its equity exposure of 39 per cent as at the end of January was a little higher than that of competitors Ruffer (RICA) and Capital Gearing (CGT), and indeed Personal Assets has tended to offer a little more growth than the other two in recent years. But it remains a prudent choice.

INPP invests in a range of unlisted infrastructure assets, many of which offer regular, government-backed revenue. It’s a fairly vanilla investment with a decent yield (6.7 per cent at the time of writing) and should be able to keep up with inflation without being too volatile.

For the global equity part of the portfolio, Yearsley pairs the aggressive growth play that is Scottish Mortgage (SMT) with the more sedate Brunner (BUT), whose portfolio he describes as “a good mix of quality value and growth”.

For investors with a long time horizon, it makes sense to have exposure to Asia and emerging markets, which have higher potential for growth in the long term. Yearsley adds that he would have suggested a China, India or Vietnam trust for a higher-risk portfolio, but that Schroder AsiaPacific Fund (SDP) is a good option for beginners. The trust’s managers look for “quality but undervalued” companies. Note that it has a giant position in the biggest company in the region, chipmaker TSMC (TW:2330), which accounted for nearly 17 per cent of the portfolio at the end of February. Samsung Electronics (KR:005930) accounts for just shy of 12 per cent, meaning that this trust has a lot of AI-related exposure.

Yearsley’s portfolio can then be personalised to match your specific needs. Six trusts is a relatively low number, but as well as keeping trading fees low, this means it is easy to keep on top of if you don’t have much time to dedicate to it. Once you become more experienced and the portfolio grows, you can add more specialist and sophisticated options. When you are a little more advanced, experts usually suggest having between 10 and 15 funds in your portfolio.

You can also tweak Yearsley’s portfolio to modify the level of risk, depending on your personal attitude, time horizon and goals.

If you want to stick to investment trusts alone, increasing or decreasing the position in Personal Assets is an easy way of modifying overall risk exposure, because it (like other wealth preservation trusts) has significant exposure to bonds. Otherwise, you can add some more fixed income by buying bonds directly or using a bond fund. The investment trust sector does have a handful of fixed income plays, but they are arguably somewhat complicated – open-ended funds offer more straightforward options in this area.

If you are a more adventurous investor and want to build a more nuanced portfolio, high-growth sectors you can add exposure to include private equity, smaller companies, technology and emerging markets. If you need more income you can look at using income trusts that go beyond the UK – examples include Murray International (MYI) globally and Invesco Asia Dragon (IAD) for Asia.

This article helped me, thank you