From a global recession to stagflation, we offer dynamic and robust portfolios to cover all eventualities

Published on May 14, 2026

by Julian Hofmann

Table of contents

Why scenarios beat predictions

What to do with your portfolio at a time of uncertainty is the hardest question in investing, and the honest answer is that it depends on which world you find yourself in. Pretending otherwise at a time when a single social media post can erase (or restore) billions of market value in an afternoon would be wilfully blind.

The current period of rapidly changing market conditions would tax the portfolio management skills of even the most experienced investor. The core problem is that markets are not really pricing in a single outcome in which investors can have much confidence.

Instead, they are oscillating between several incompatible ones: a negotiated de-escalation of trade tariffs; a protracted stand-off in the Middle East; a potential escalation in eastern Europe; a US dollar decline; and a higher-for-longer interest rate environment that punishes long-term positions. Each of these outcomes is possible, but we cannot anticipate them all at once. For retail investors, this is a paralysing problem, and it is tempting to do nothing and hope the fog lifts.

But sitting still may not prove foolproof, either. The past three years have been characterised by higher interest rates, an AI-driven US stock market boom and a general assumption that inflation would stay at manageable levels. A portfolio that worked well through that period is, by default, a bet on the specific combination of economic and investment conditions that prevailed during that time. Can anyone now champion these assumptions with confidence?

If not, the uncomfortable question is: what is your current portfolio relying on, and would you have consciously chosen this stance at the outset? The useful response to elevated uncertainty is not to attempt predictions, but to understand which scenario your existing allocation is implicitly positioned for, and to ask whether one or two modest adjustments might improve its resilience.

Why scenarios beat predictions

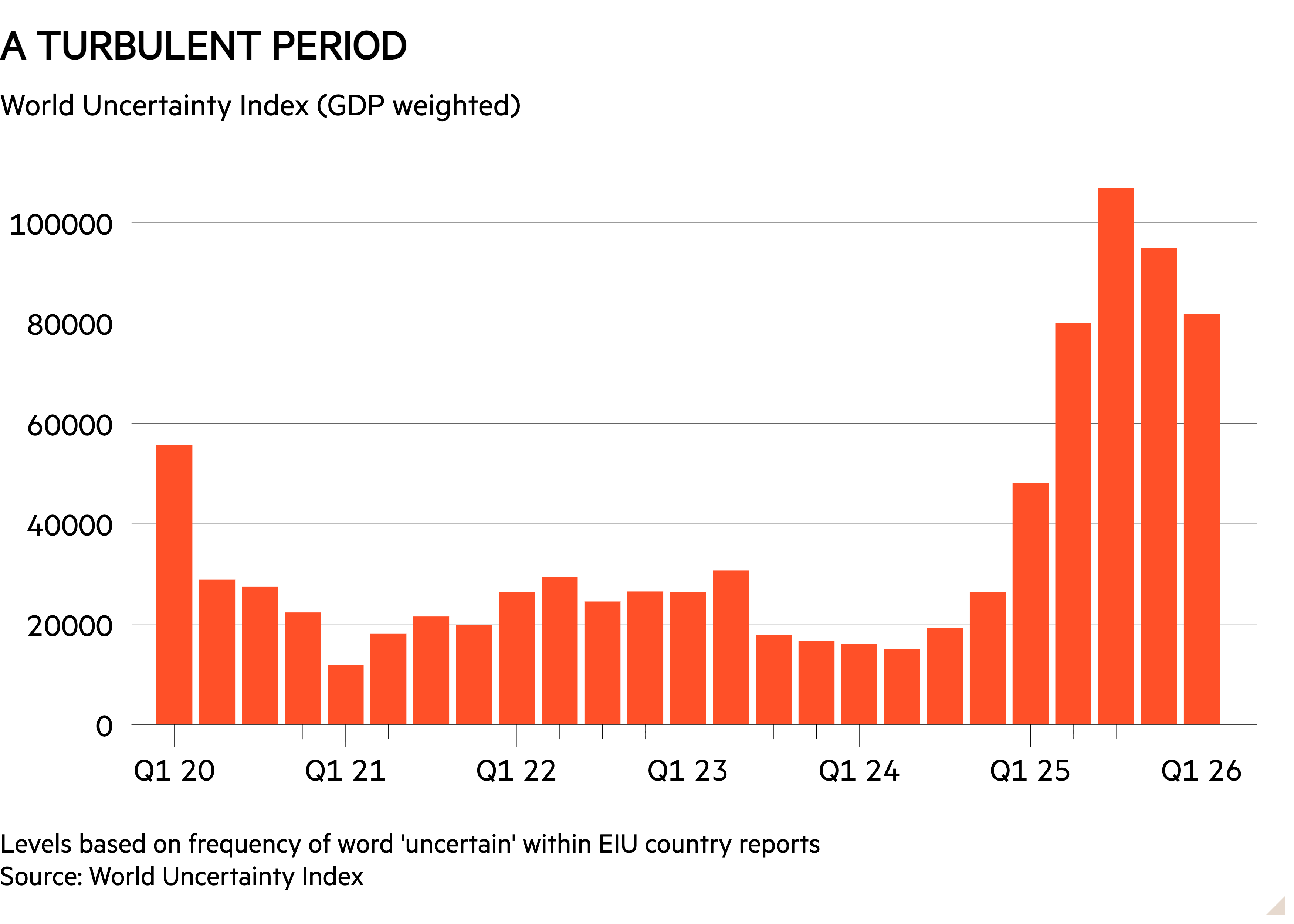

Volatility is an unavoidable part of investing, but the current backdrop feels more destabilised than at any time since the end of the cold war.

The World Uncertainty Index, constructed by Hites Ahir and Davide Furceri of the IMF together with Stanford’s Nicholas Bloom, demonstrates the turbulence of the past decade, with major spikes around Brexit, the Covid-19 pandemic and the second Donald Trump presidency (see chart below).

In fact, it is entirely possible that the so-called ‘Great Moderation’ from 1990 to 2008 was the exception to the rule, and that a permanent state of uncertainty and instability is in fact the new ‘normal’. In which case, preparing conceptually for several different scenarios should be a key mental discipline for investors.

Achieving sustained insight means assessing risk dispassionately. Investors have traditionally relied on smoke signals from the bond market to forecast trouble ahead. However, part of the current problem is that this market may no longer be transmitting reliable information, due to surging sovereign debt loads pushing yields higher for structural, rather than purely economic, reasons.

For example, in its latest Fiscal Monitor report, the IMF estimates that global public debt was just under 94 per cent of world GDP in 2025 and is on course to reach 100 per cent by 2029, with the accumulation driven largely by the world’s major economies.

Indeed, the market historian Russell Napier argues that investors cannot rely on the signals from bond yields for the next 15 years or so. His reasoning is that government debt levels are now so high that they require inflation to erode them. He thinks the ‘financial repression’ investors experienced after 2008, whereby interest rates were kept lower than the rate of inflation, is now an embedded part of the financial system.

Investors do not need to accept every implication that Napier draws to take the underlying point seriously: if sovereign bond yields no longer transmit a reliable price signal, a portfolio built on assumptions to the contrary is taking a position that is not consciously chosen.

This reinforces the theoretical point that is less often stated but still important. A portfolio built for one economic outcome is, by definition, an unhedged bet on that outcome materialising.

Generally, the assumed correlations between asset classes bear weight: equities rise, bonds cushion, the ‘60/40’ equity/bond portfolio works as envisioned. However, in abnormal times, those correlations invert without warning and investors discover, usually too late, that they were never really diversified at all.

Investors’ Chronicle

The Five Portfolio Scenarios

Portfolio one: Stagflation

Inflation is sticky, growth stalls, and the two halves of a balanced portfolio fail

This is the scenario that often arrives in the wake of an external crisis (such as an oil shock that does not easily unwind). It leads to rising wage demands at the same time as output stumbles. What is so damaging about stagflation is that inflation does not need to return to double-digit levels to do serious damage: it simply needs to stay above target while activity weakens.

When inflation is high and rising, the negative correlation between equities and government bonds turns positive, meaning both suffer and the 60/40 portfolio no longer works.

In this scenario, inflation-linked gilts provide more ballast than conventional gilts, although they too can be caught out if base rates rise faster than markets expect. Another option would be selectively chosen infrastructure and resources funds. Indeed, this is when energy and broad commodities exposure earns its keep, despite being uncomfortable to hold in any other scenario.

On the equities side, the choice narrows to those companies that can pass cost inflation on to customers without losing them, which is a far smaller universe than generally advertised. This increases the case for holding stalwarts such as AstraZeneca (AZN) or Unilever (ULVR) that anchor a portfolio, precisely because these companies can still increase earnings when turnover is flat.

The history of the 1970s stagflationary period shows that it was brutal, but not uniformly so. The pain was certainly concentrated: the FT30 (the precursor to the FTSE 100) lost roughly three-quarters of its value between May 1972 and December 1974, a worse absolute fall than the UK market suffered during either world war or the Great Depression.

Gilts suffered in real terms, with UK inflation hitting 25 per cent in 1975 and savers watching the purchasing power of fixed coupons evaporate. The winners were the assets the typical British investor of the time either could not access or actively distrusted.

Gold rose from $35 an ounce when the US abandoned the gold peg in 1971 to around $850 by January 1980, comfortably outpacing inflation. Broad commodity baskets, as measured by the S&P GSCI index, returned more than 580 per cent over the decade.

Portfolio two: Soft landing

The Federal Reserve cuts rates once or twice, tariff damage is absorbed, earnings hold up

This was the consensus scenario at the start of 2026, so by definition the one most open to disappointment. A soft landing would require consumer prices not to climb too much due to tariffs or supply shocks and trade negotiations to grind their way to bilateral deals, while central banks deliver two or three more base rate cuts.

The temptation in this scenario is to assume that what worked over the past three years will continue to work. The main weakness in this assumption is that returns have been driven by a handful of US megacap technology shares trading at high multiples.

For example, the S&P 500 is on a forward price/earnings (PE) ratio of roughly 21 times, according to FactSet, above its 10-year average of around 19, and that headline figure flatters the picture as the largest constituents trade considerably higher.

A soft landing may not mark the return to an indiscriminate risk-on environment; instead it may mean the conditions under which neglected value shares come back into focus. Currently, that points towards European equities, where the Stoxx Europe 600 trades on a more forgiving forward multiple of around 14.5, according to FactSet.

The case for holding the UK in a soft-landing scenario is sharper still. The FTSE 100, on a forward PE ratio of 12.6 with a dividend yield over 3 per cent, has trailed the S&P 500 consistently over the past decade. The gap has narrowed over the past 18 months, but is still wide enough that even a modest mean reversion would have a material effect.

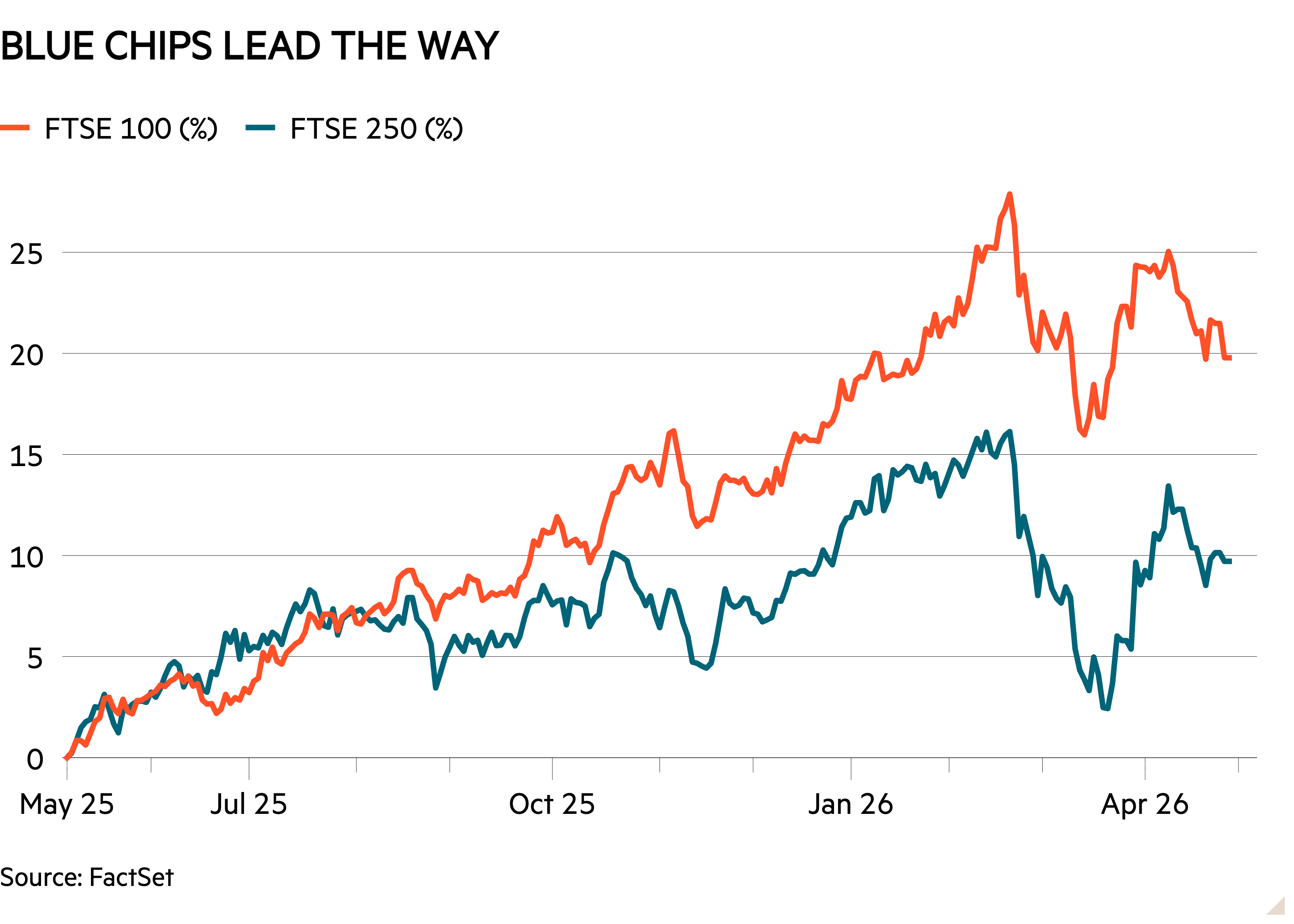

The FTSE 250 is the more interesting prospect for those willing to take domestic risk. The mid-cap index continued to lag its larger counterpart last year (see chart below), and on a FactSet forward PE ratio of around 12 against a long-run average closer to 15, it sits at a relative discount to its own performance.

The bond side of the portfolio benefits gently rather than dramatically in this scenario. Central bank policy that delivers modest rate cuts will pull gilt prices up by enough to deliver a respectable total return.

Investment-grade corporate bonds benefit from the same dynamic, with spreads relative to government debt compressing as recession risk fades. The running yields on offer at the start of 2026 – sterling corporate bond funds were distributing around 5 per cent – provide a cushion that did not exist for most of the past decade.

Cash is the loser here in this scenario, in relative terms. The 4 per cent cash yield that competes credibly with equity risk in a ‘higher-for-longer’ interest rate scenario starts drifting back towards 3 per cent as the rate-cutting cycle proceeds; the common investor mistake is to stay too long in cash on the way down.

The structural hedge worth carrying is a deliberate tilt away from the US. Tracker fund drift (global benchmarks now have 60-70 per cent of assets in the US) has left most UK retail portfolios more US-exposed than the holders would consciously choose if asked, and a soft landing is not a reason to stay there by accident.

Portfolio three: Recession

Tariffs and the Strait of Hormuz closure bite, consumer confidence slumps, earnings disappoint

A recessionary scenario is unusual in that it requires two portfolios at once – a defensive one for the next 18 months and an opportunistic one for the period after. The investors who do badly in recessions are not those who fail to predict them, but those who treat the defensive phase and the subsequent deployment phase as the same problem.

Capital preservation dominates the first phase. Short-duration fixed income earns its keep again, after a decade in which it was barely worth owning. Cash finally pays and defensive sectors, such as consumer staples, utilities and parts of healthcare, do the income work that the textbooks promise they will, with the caveat that valuations within them are now uneven enough to require genuine stockpicking. This is also where conventional gilts become a genuine income option again, as their negative correlation with equities reasserts itself.

Understanding the deployment phase

Recessions produce bargain prices that make 20-year compounding possible, but only for investors with the cash, the discipline and the time horizon to act on them. Holding 10 per cent of your portfolio in instruments that can be deployed quickly is not dramatically strategic, but it allows the next decade’s returns to be earned at sensible prices.

It is worth noting that two assets behave less obviously than the textbooks suggest in a recession scenario.

Gold’s recession record is more mixed than its reputation implies. The metal has tended to perform strongly in inflationary recessions and crisis periods but can drift sideways or fall in conventional downturns, when real yields rise and the US dollar strengthens as a haven asset. A modest position is defensible as a tail-risk hedge, but should not be confused with the recession-proofing role that conventional gilts can perform in its place.

Non-US equities are the other consideration that deserves attention. The most vulnerable market at the start of a sell-off will depend on which sectors are at the centre of the shock in question. But as a general rule, other markets tend to start from cheaper valuations and recover faster.

This makes them the natural home for capital being deployed in the second phase. UK and European mid-caps have historically been among the most rewarding hunting grounds for investors who have the patience to buy throughout the bottom, rather than waiting for confirmation that a recovery has arrived.

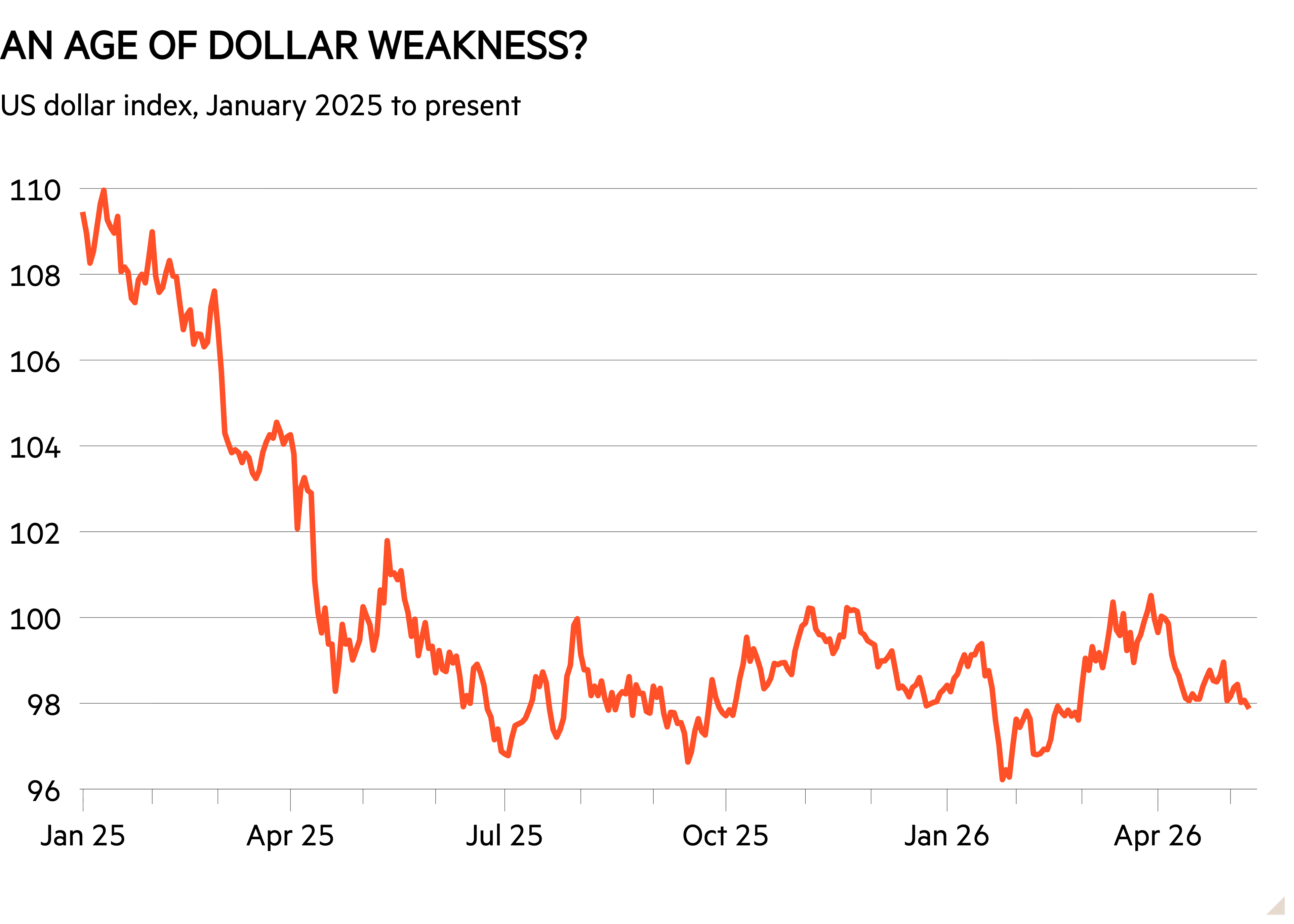

Portfolio four: Dollar decline

A structurally weaker dollar changes the total returns on offer from US assets, without anything happening to underlying businesses

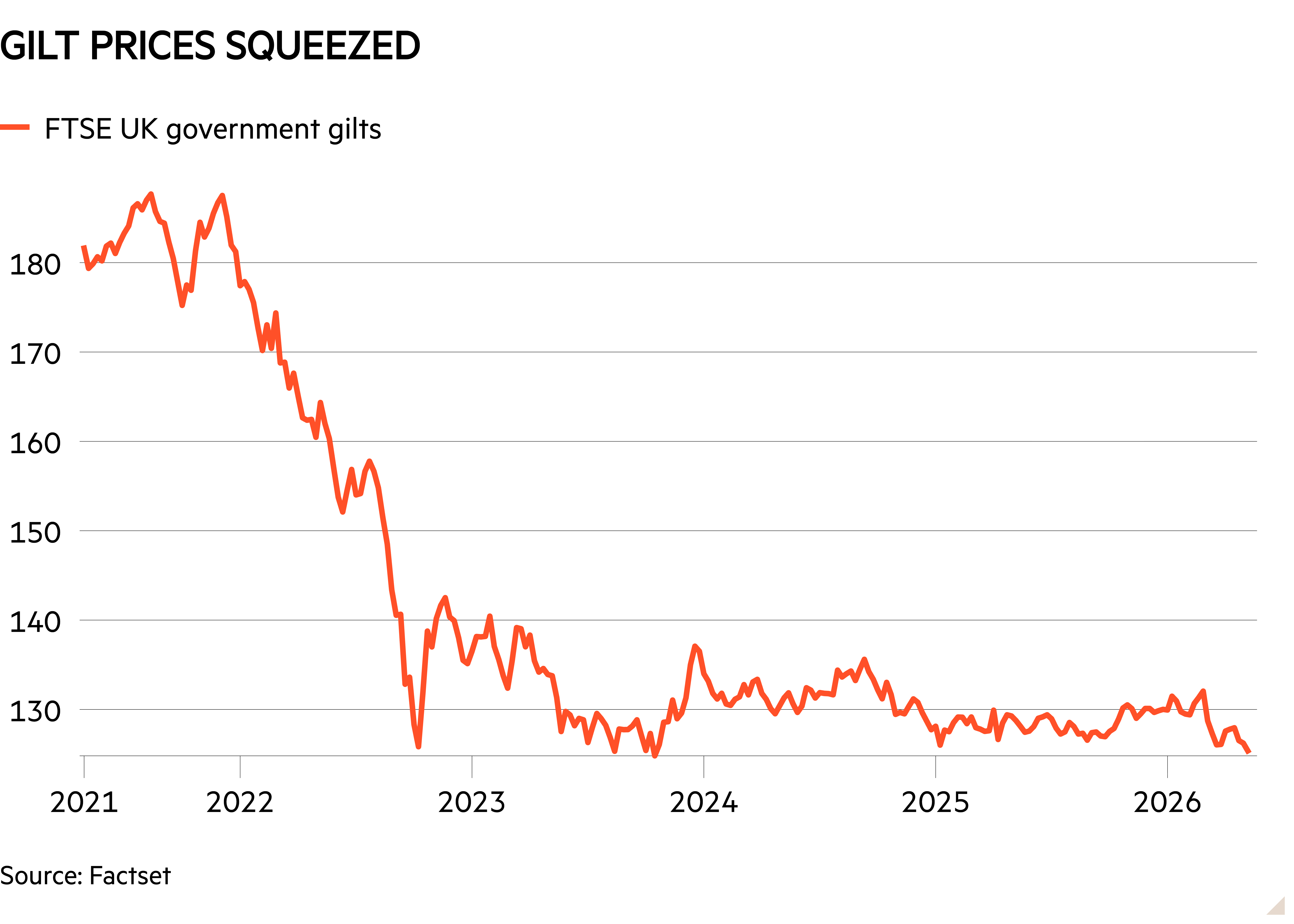

This scenario is already partially under way, although less dramatically than much news coverage suggests. The US dollar is meaningfully softer than the 2022-23 cycle, but talk of collapse mistakes a multiyear drift for a rout (see chart below).

The structural point matters more than the precise level of the dollar. As mentioned, UK retail portfolios have become more US-exposed than many holders would consciously choose. This is due to the simple mathematics of letting Wall Street’s outperformance compound inside a default global index allocation.

However, the Investment Association’s full-year 2025 data, published in February, shows the picture beginning to shift. UK retail investors pulled £4.8bn from global equity funds in 2025, with North American equities suffering £2bn of redemptions in the second half alone, while European equity funds attracted net inflows of £761mn, in what could be the first signs of conscious geographical reallocation rather than a passive drift.

The response to the dollar problem takes different forms. Gold has historically been negatively correlated with the currency. But the metal’s soaring price – last year was its strongest annual performance since 1979, driven by sustained central bank buying and sovereign debt anxiety – raises the risk of a reversal even in a scenario where the dollar keeps weakening.

For income investors who want to reduce their currency risk, sterling-denominated bonds now offer a genuine alternative in this scenario. Ten-year gilt yields are above 5 per cent, the highest level this century, and sterling investment-grade corporate bond funds are typically paying around this level, too.

Portfolio five: Interest rates stay higher for longer

Rates remain elevated, the cutting cycle is shallow, long bonds are a trap

This is the scenario in which cash genuinely competes with equity risk, which inverts the past decade of investor experience. It does not require a rebound in inflation, just for it to persist above target, leaving central banks unable to cut for fear of stoking further price growth.

It is in this context that the Bank of England and the Federal Reserve have both signalled that the floor for rates during the current cycle may be higher than during the post-2008 period.

The portfolio implications are uncomfortable for anyone whose mental model was set between 2009 and 2021. Cash and money market instruments are a changed asset class because, with a yield of 4 per cent or more, they compensate for a corresponding underperformance in equities, as the discounted rate of future cash flows suffers from higher-for-longer interest rates. Short-duration bonds can also play a role.

The other important asset class in this scenario is long-duration bonds, but only in the sense that investors should be wary of them as long as rates remain higher. These will remain a value trap until a sharp fall in interest rates raises their prices.

The structural hedge here is a modest gold allocation, not because gold competes with cash on yield, but because the higher-for-longer scenario is arguably also the one in which the institutional framework supporting those cash interest rates comes under the most strain. If political pressure for rates to ease increases and central bank credibility starts to fray, inflation expectations can rise, and cash is the asset that suffers first.

The five scenarios are not equally probable, but the test of a portfolio is not whether it passes the most likely scenario, but if it survives all of them at an acceptable cost.

Looking across the framework, two assets earn their place in three of the five future scenarios. Gold works in stagflation, dollar decline and higher-for-longer rates scenarios, and serves as tail-risk insurance in a fourth. Short-duration fixed income does well in recessions, dollar decline and higher-for-longer rates. Neither asset is particularly glamorous. But equities, and their unrivalled potential for long-term compounding, should not be forgotten. The possibility of geographical exposure outside the US market is also a serious option for investors looking for stockpicking options during downturns.

The honest answer to what investors should do remains: it depends on which world emerges. By organising according to scenarios, at least the portfolio that arises is the result of conscious decisions.

Recessions produce bargain prices that make 20-year compounding possible, but only for investors with the cash, the discipline and the time horizon to act on them. Holding 10 per cent of your portfolio in instruments that can be deployed quickly is not dramatically strategic, but it allows the next decade’s returns to be earned at sensible prices.

Leave a Reply