3 Quant Growth And Income Stocks

Jun 17, 2026, 9:00 AM ETRLJ, EPR, XOM, XOM:CA

Steven Cress, Quant Team

SA Quant Strategies

Summary

- While a pending U.S.-Iran peace deal may temporarily cool headline commodity volatility, a stellar quarter of surprise jobs growth and an entrenched 3% Core CPI indicate that structural inflation will remain sticky.

- Thriving in a high-employment, sticky-inflation environment requires a strategic pivot toward stocks that leverage immediate daily pricing power, experiential consumer demand, and deep operational cost insulation.

- Discover three Quant Growth & Income stocks, supported by strong Quant Ratings, that offer inflation insurance in an increasingly unpredictable market.

- I am Steven Cress, Head of Quantitative Strategies at Seeking Alpha. I manage the quant ratings and factor grades on stocks and ETFs in Seeking Alpha Premium. I also lead Quant Growth and Income, which is a model portfolio for dividend investors interested in capital appreciation and income.

Sticky Inflation

President Donald Trump has announced a tentative peace deal between the U.S. and Iran that would cease military actions and reopen the Strait of Hormuz. The agreement is set to be signed this Friday in Geneva during the current G-7 Summit.

The market’s immediate response was a textbook relief rally. As markets opened on Monday, indexes surged higher, crude oil prices fell, and the overall angst of the market seemed to cool.

While the pending peace deal would eliminate a massive geopolitical wildcard for markets to navigate, assuming that it’s also an overnight fix for inflation would likely be a miscalculation.

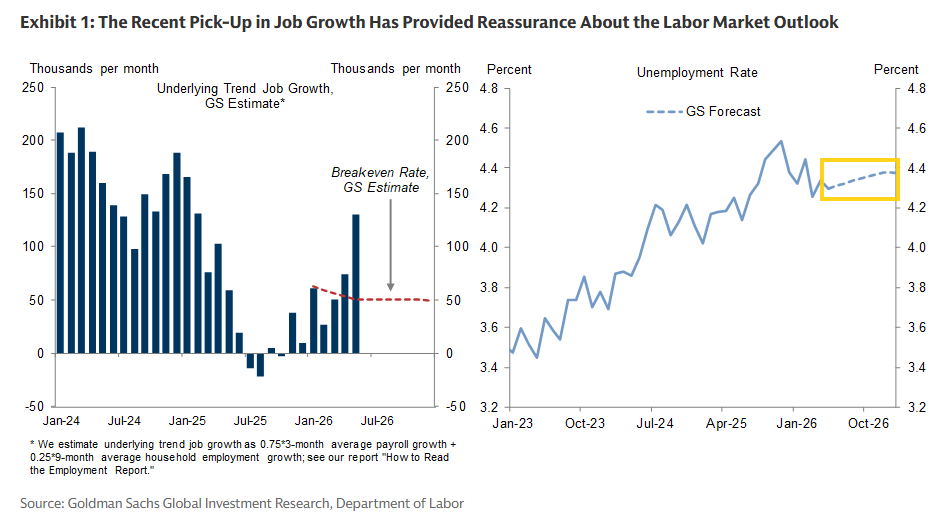

Energy inflation driven by the blockade of the Strait of Hormuz certainly shocked the financial system, but today’s sticky inflationary environment isn’t a one-trick pony. A stellar quarter of surprise jobs growth has suddenly revived a labor market that had been stagnant for the better part of a year. And regardless of energy-driven inflation, Core CPI has remained range-bound to the 3% mark and has shown few signs of deviation.

The Labor Market is Strengthening

May’s jobs report reinforced the complex macro backdrop, supporting the case for higher-for-longer rates while underscoring the economy’s resilience. The labor market has recorded its strongest quarterly growth trend since mid-2024, with payroll growth continuing to exceed expectations. Goldman Sachs Global Investment Research forecasts a stabilization of the unemployment rate through the end of the year.

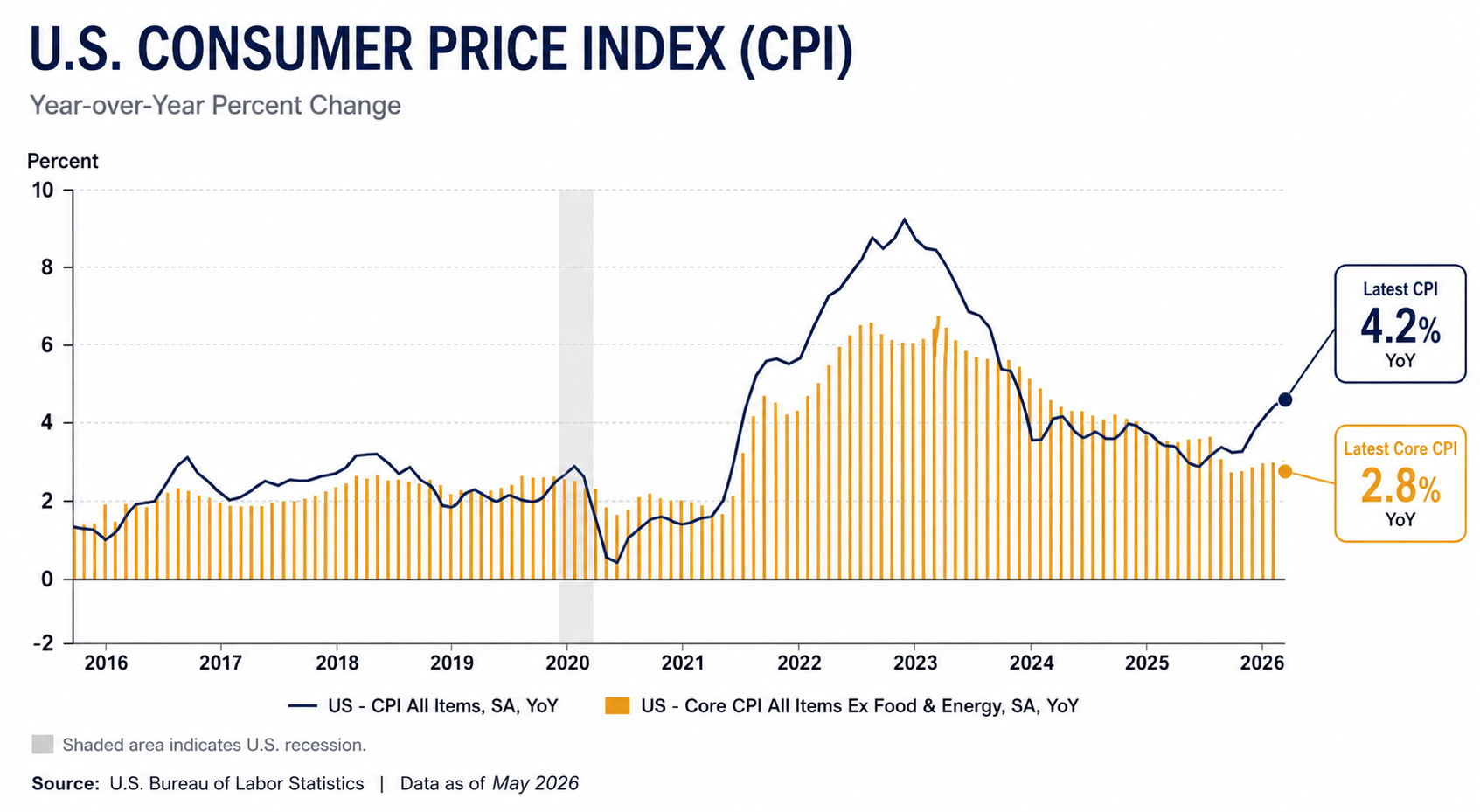

Core CPI Remains at 3%

Inflation data released last week provided further support for the higher-for-longer narrative. Headline CPI accelerated to 4.2% YoY, while Core CPI (ex. Food and Energy) increased to 2.8%. While headline inflation could see a pullback if oil prices continue to drift closer to pre-war levels, the underlying pricing pressures that have kept Core CPI close to 3% are showing no signs of a slowdown.

Although inflation remains well below the peaks reached in 2022, the recent uptrend illustrates that the disinflationary process has become increasingly uneven and arguably unreliable. Combined with resilient labor market conditions and continued capital spending tied to reshoring initiatives and AI-related investment, the latest data reinforces the view that economic activity remains sufficiently firm to keep inflation pressures elevated.

With Federal Reserve Chair Kevin Warsh leading his first FOMC meeting this week, all eyes will be on the committee’s Summary of Economic Projections (‘SEP’) for any signs of when a potential rate hike will occur.

Robert Kaplan, Goldman Sachs vice chairman and former president of the Dallas Fed, believes that the potential end to the Iran War would likely buy Warsh and the Fed more time before deciding on any rate movements. For the Federal Reserve, the combination of solid employment growth and persistent inflation could result in interest rates remaining restrictive for the long term.

Top Quant Growth and Income Stocks

This backdrop continues to favor safe-haven businesses with durable cash flows, strong pricing power, and resilient demand characteristics, qualities that are captured by Seeking Alpha’s Quant Growth & Income Portfolio. To give you an idea of what the QG&I strategy looks like in action, we’ve selected three featured holdings from the portfolio that exhibit characteristics needed to inflation-proof your portfolio. These selections serve as an example of how our quantitative framework can cut through the volatility of headlines and personal emotional bias to systematically target growth and income stocks that neutralize uncertain macro conditions.

RLJ Lodging Trust (RLJ)

- Market Capitalization: $1.67B

- Quant Rating: Buy

- Sector: Real Estate

- Industry: Hotel & Resort REITs

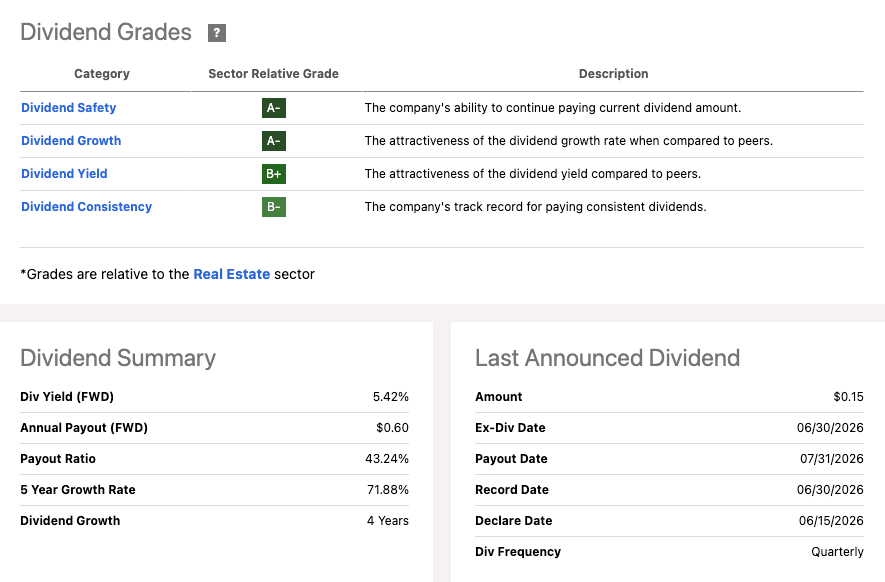

- Dividend Yield (“FWD”): 5.42%

RLJ Lodging Trust is a hotel REIT that owns a portfolio of 92 premium-branded properties concentrated in urban, convention, and high-demand leisure markets across the United States. RLJ holds a unique advantage in a sticky inflationary environment due to its pricing agility. While a sustained higher-for-longer rate environment can eat away at traditional commercial REITs through long-term lease obligations, RLJ’s business model maintains a safety buffer through its 24-hour pricing loop. Because hotel room bookings are re-priced daily through real-time price monitoring, RLJ’s price agility can absorb prolonged periods of high interest rates.

RLJ’s attractive combination of dividend income and improving cash flows was evident in its strong first quarter results. The company was able to improve operating momentum through pricing power and demand normalization across its portfolio. RevPAR increased 4.8% year-over-year, while non-room revenues grew 8.2%, significantly outpacing room revenue growth.

Management raised its full-year adjusted FFO guidance to a range of $1.29 to $1.45 per share as the company’s portfolio remains strategically positioned in major urban and business-centric markets that stand to benefit from continued normalization in corporate travel, convention activity, and group bookings.

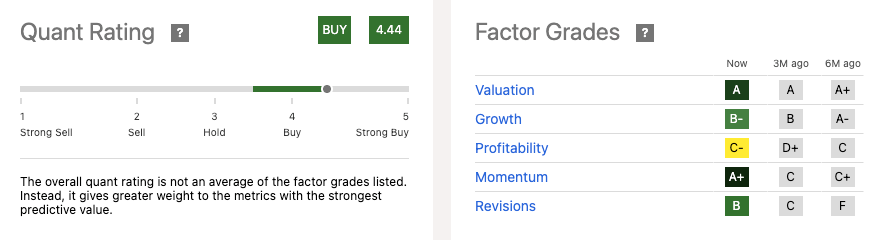

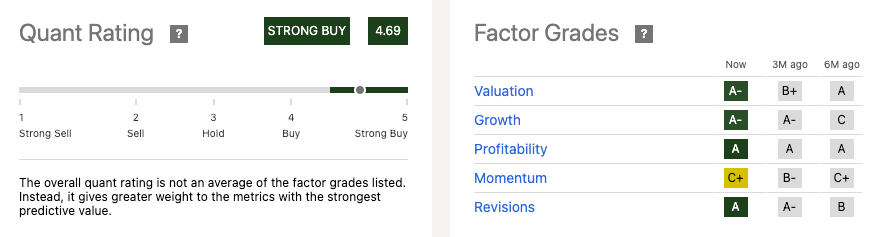

RLJ Lodging Trust is currently rated as a Buy according to Seeking Alpha’s Quant System, backed by strong Factor Grades.

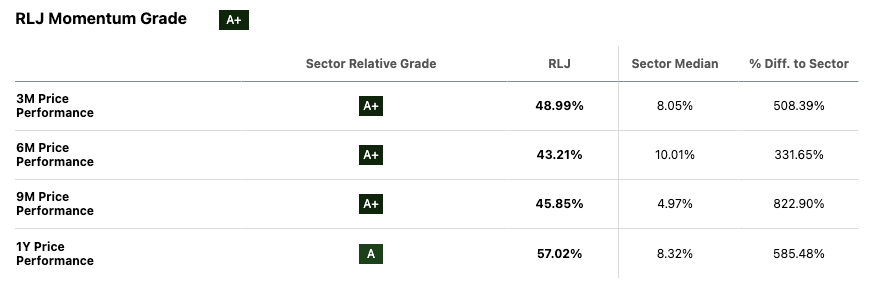

Our Quant System currently highlights RLJ’s rapid Momentum Grade increases over the last six months. Specifically, RLJ scores a rare A+ Momentum Grade, with straight ‘A’s across the board in price performance over the past year.

A key component of the bull thesis is RLJ’s strengthened balance sheet. During the first quarter, management refinanced all debt maturities through 2028, extending its maturity profile and reducing refinancing risk. The company ended the quarter with more than $950 million of liquidity, including approximately $353 million in cash and a fully available revolving credit facility.

RLJ’s forward P/AFFO (“FWD”) of 8.43 vs. the sector median of 16.37 is more than a 48% discount.

The company has maintained an exceptional dividend profile, with a current 5.42% FWD dividend yield, providing investors with a reliable income highlighted by its consecutively paid dividend for 14 years. Management’s willingness to aggressively repurchase shares suggests confidence that the stock remains undervalued relative to its underlying real estate portfolio and future cash flow potential. This is also supported by its AFFO Payout Ratio of 45.71%, representing a 38% discount to the sector.

EPR Properties (EPR)

- Market Capitalization: $4.46B

- Quant Rating: Strong Buy

- Sector: Real Estate

- Industry: Other Specialized REITs

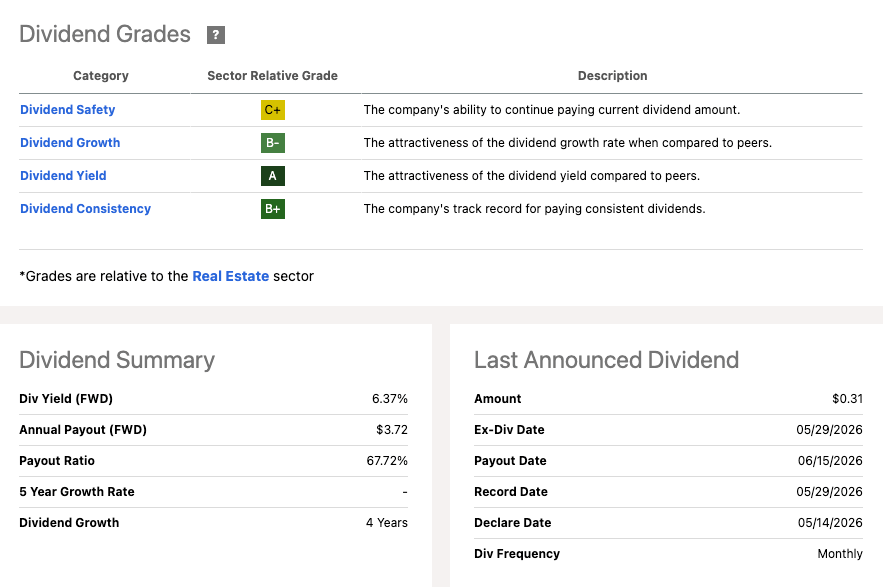

- Dividend Yield (“FWD”): 6.37%

EPR Properties is a premier player in experiential real estate, out-of-home leisure, and entertainment venues. EPR’s portfolio spans across high-traffic destinations such as golf complexes, ski and winter resorts, theme parks, and theaters. Consumers have grown wary of goods inflation and have increasingly migrated to spending on services and experiences. EPR is positioned well to capitalize on this consumer trend even in a sticky inflation environment.

EPR is experiencing a strong tailwind driven by its $7.1 billion gross investment across 335 properties, which currently holds a 99% occupancy rate. This foundation is supported by an expanding market and a strategic 94% portfolio concentration in experiential properties.

EPR Properties is currently rated as a Strong Buy according to Seeking Alpha’s Quant System, backed by an exceptional suite of underlying Factor Grades.

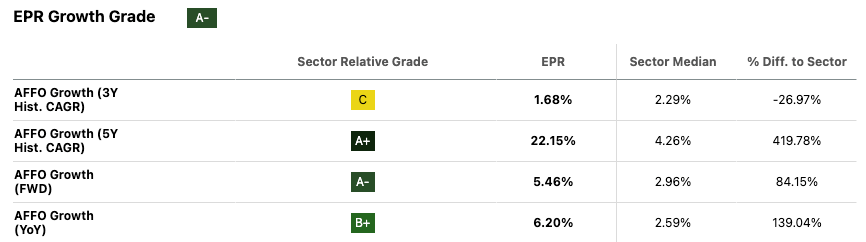

Our Quant System currently highlights EPR’s rapid Growth Grade increase—currently an ‘A-‘, when only six months ago it was rated a ‘C.’ Investors should consider capturing this momentum heading into the summer. As shown below, EPR scores strongly on its AFFO Growth (5Y CAGR and FWD) scores, with its AFFO Growth (“FWD”) nearly doubling the sector median figure at 5.46%.

In a traditional commercial real estate setup, high interest rates have the potential to erode cash flow as maintenance management costs rise. However, EPR’s triple net lease structure (“NNN”) protects them from rising inflationary pressures on margins.

Under long-term agreements, tenants are legally obligated to pay for 100% of the property-level costs that are subject to rising input costs. This includes taxes, insurance, and utility costs. This structure has provided an exceptionally strong buffer for AFFO growth.

Additionally, EPR includes annual rent escalators, which are usually tied to the Consumer Price Index (“CPI”). This helps to insulate the company’s cash flow from internal cost pressures. And ultimately, providing the basis for a phenomenal dividend profile.

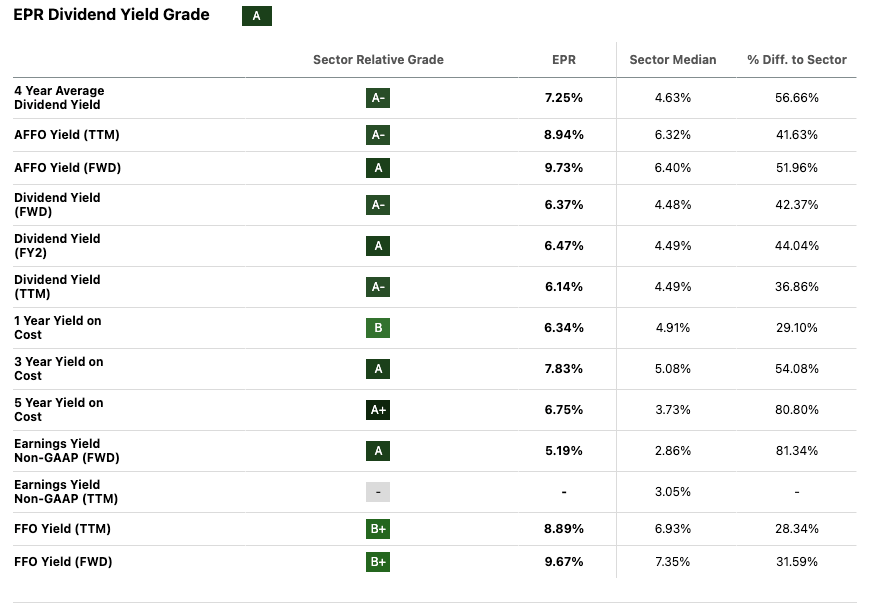

EPR’s balance sheet strength passes through to its incredible ‘A’ Dividend Yield Grade. The income profile is headlined by its 6.37% dividend yield (“FWD”), outperforming the sector median by 42%. More importantly, its 9.73% AFFO yield (“FWD”) is nearly 52% higher than the sector median and provides a profitable yield gap of 3.36%, anchoring the company for strong growth ahead while protecting its payout.

Exxon Mobil Corporation (XOM)

- Market Capitalization: $584.04B

- Quant Rating: Strong Buy

- Sector: Energy

- Industry: Integrated Oil & Gas

- Dividend Yield (“FWD”): 2.92%

Founded in 1870 and headquartered in Spring, Texas, Exxon Mobil is one of the world’s largest integrated oil and gas companies that engages in the exploration and production of crude oil and natural gas internationally, operating through four segments: Upstream, Energy Products, Chemical Products, and Specialty Products.

On the surface, you may question the inclusion of an oil giant amidst the notion of falling oil prices. While high oil costs can benefit energy companies like Exxon Mobil in the near term, eventually the rising costs of operation and exploration catch up. A more balanced energy environment is actually where Exxon is built to thrive and where its competitive advantages really stand out.

Selling products under the Exxon, Esso, and Mobil brands with a total refining capacity of 4.1 million barrels of oil per day, Exxon Mobil holds a strong internal hedge against oil volatility. When oil prices normalize, input costs for its downstream units drop significantly. This reduces expenses and unlocks expanded profit margins within these segments, offsetting the reduction in revenue from upstream pricing.

Meanwhile, Exxon Mobil’s upstream unit is targeting $25 billion in earnings growth by 2030 through a combination of growth and cost reductions. Management has specifically pursued high-performing capital projects with a focus on the Permian Basin and Guyana regions, which are expected to be primary drivers of new production volumes over the next five years.

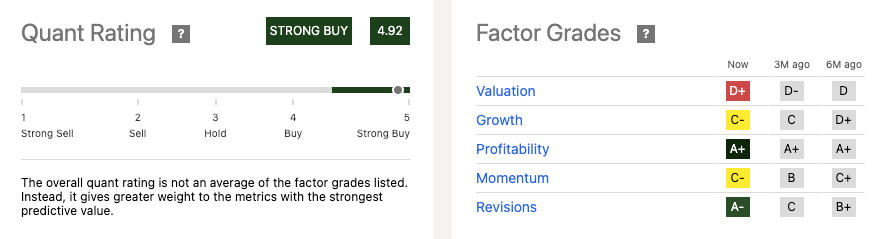

Exxon Mobil is currently rated as a Strong Buy according to Seeking Alpha’s Quant System, backed by impressive Profitability and Revisions Factor Grades.

XOM’s ‘A+’ Profitability Grade is supported by a fortress balance sheet and $47.72B cash from operations position, driving its 29.77% gross profit margin and 9.79% return on common equity.

FY1 earnings and revenue revisions saw near-unanimous upward movement in both, boosting its Revisions Factor Grade from a C to an A- over the past quarter. This underscores Wall Street’s confidence in XOM’s mature and highly integrated operations. Even with energy market volatility stemming from the Middle East, analysts believe the company possesses the operational expertise and capacity to navigate short-term challenges.

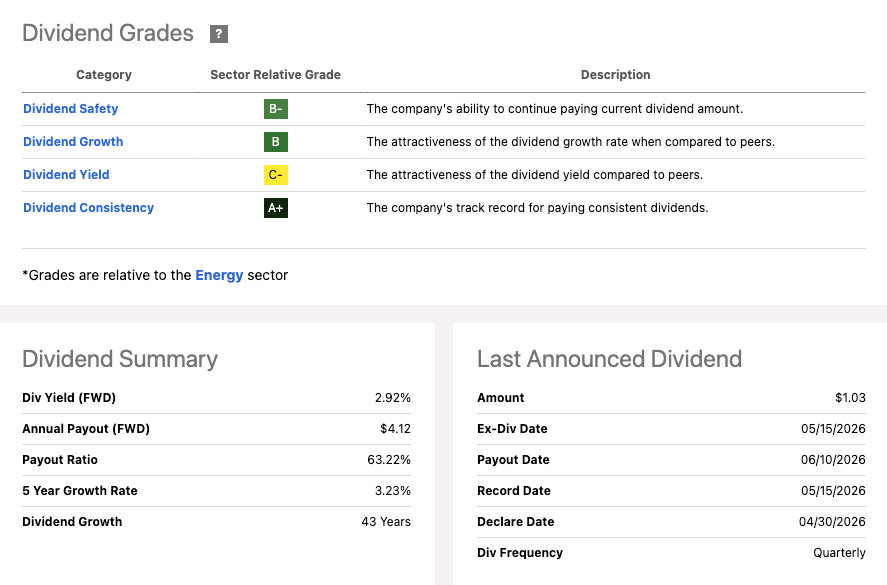

Exxon Mobil’s strong cash position and commitment to reducing debt levels have fortified its reliability with shareholder return, earning it an ‘A+’ Dividend Consistency Grade.

With 43 consecutive years of dividend growth and 43 consecutive years of dividend payments, a 2.92% forward dividend yield, and a “Strong Buy” Quant Rating, XOM demonstrates both income reliability and sector leadership.

Looking Ahead: Secure Growth and Income

There’s a lot of uncertainty in the months ahead. Sticky inflation continues to prove it’s not going to leave without a proverbial fight. Investor sentiment remains fragile amidst persistent inflation, soaring interest rates, volatile energy prices, a rebounding labor market, and upcoming midterm elections. Income investors are facing headwinds, and achieving benchmark-beating results in this higher-for-longer rate environment might require owning stocks with strong fundamentals that can survive a prolonged inflationary environment.

If the months ahead are defined by sticky inflation and potential rate hikes, it could be difficult for growth and value opportunities that lack income-generating payments. Ultimately, RLJ, EPR, and XOM highlight income opportunities that have a natural defense against today’s macro backdrop.

If you’re looking for a data-driven income strategy, explore our new Quant Growth & Income Portfolio – a systematic model built to outperform dividend ETFs by focusing on yield, growth, and safety. Seeking Alpha’s quant ratings and investment research tools help to ensure you are furnished with the best resources to make informed investment decisions while taking the emotion out of investing.

More on my IG service

- I am Steven Cress, Head of Quantitative Strategies at Seeking Alpha. I manage the quant ratings and factor grades on stocks and ETFs in Seeking Alpha Premium. I also lead Alpha Picks, which selects the two most attractive stocks to buy each month, and also determines when to sell them.

This article was written by

Steven Cress, Quant Team

Steven Cress is VP of Quantitative Strategy and Market Data at Seeking Alpha. Steve is also the creator of the platform’s quantitative stock rating system and many of the analytical tools on Seeking Alpha. His contributions form the cornerstone of the Seeking Alpha Quant Rating system, designed to interpret data for investors and offer insights on investment directions, thereby saving valuable time for users. He is also the Founder and Co-Manager of Alpha Picks, a systematic stock recommendation tool designed to help long-term investors create a best-in-class portfolio.Steve is passionate and dedicated to removing emotional biases from investment decisions. Utilizing a data-driven approach, he leverages sophisticated algorithms and technologies to simplify complex, laborious investment research, creating an easy-to-follow, daily updated grading system for stock trading recommendations.Steve was previously the Founder and CEO of CressCap Investment Research until its acquisition by Seeking Alpha in 2018 for its unparalleled quant analysis and market data capabilities. Prior to that, he had also founded the quant hedge fund Cress Capital Management, after spending most of his career running a proprietary trading desk at Morgan Stanley and leading international business development at Northern Trust.With over 30 years of experience in equity research, quantitative strategies, and portfolio management, Steve is well-positioned to speak on a wide range of investment topics.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given that any particular security, portfolio, transaction or investment strategy is suitable for any specific person. The author is not advising you personally concerning the nature, potential, value or suitability of any particular security or other matter. You alone are solely responsible for determining whether any investment, security or strategy, or any product or service, is appropriate or suitable for you based on your investment objectives and personal and financial situation. Steven Cress is the Head of Quantitative Strategy at Seeking Alpha. Any views or opinions expressed herein may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank.

Leave a Reply