This Major Market Rotation Just Handed Dividend Investors A Huge Gift

Feb. 23, 2026

Samuel Smith

Summary

- Capital is rotating aggressively, and most investors are reacting emotionally instead of strategically.

- Some sectors look unstoppable… others look broken. The truth may surprise you.

- Here’s how I’m taking advantage of this massive market rotation to target 7-8% yields with below-market volatility.

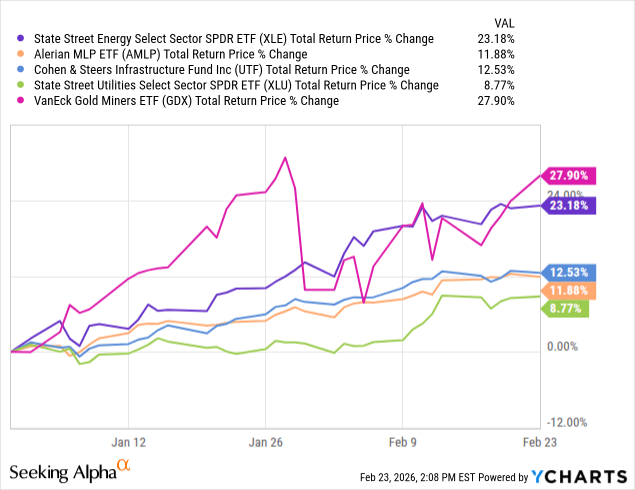

So far in 2026, there is sharp dispersion going on in various sectors with the dividend stock universe (SCHD). On the one hand, you have energy stocks (XLE), MLPs (AMLP), infrastructure (UTF), utilities (XLU), and precious metals (GDX) related stocks that are soaring higher.

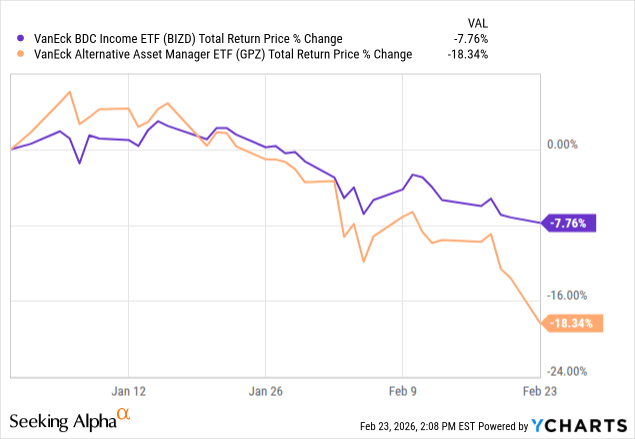

At the same time, BDCs (BIZD) and alternative asset managers (GPZ) are getting crushed.

While this is causing many investors who own shares in BDCs and/or alternative asset managers to panic, for me, it is an ideal investing environment. This is because volatility and dispersion of performance of these income-generating sectors is the very fuel that powers my strategy and my long-term total return outperformance, rather than threatening it. When capital rotates aggressively from one sector to another, valuation multiples tend to become detached from fundamentals, both on the upside and on the downside. This enables me to implement disciplined value investing principles and to recycle capital to produce outsized total returns over the long term. In this article, I will detail why.

When Volatility Becomes a Gift for Income Investors

Put simply, when markets get very volatile and some sectors soar while others plunge, it allows a disciplined value investor to harvest gains from fully valued or overvalued positions and recycle that capital into deeply undervalued opportunities. This enables me to both accelerate my passive income growth by trimming stocks whose dividend yields have become suppressed from soaring stock prices and recycle the capital into stocks whose dividend yields have soared due to their stock price getting beaten down, as well as accelerate my long-term total return compounding because it enables me to arbitrage fluctuations in valuation multiples on top of the compounding already being generated by dividend payouts and growth. By pursuing this strategy while still maintaining some portfolio diversification, it enables me to allow volatility to serve me rather than the other way around.

Why Sector-Level Sell-Offs Are Even Better Than Market Crashes

While a general market sell-off is typically something that I appreciate as an investor who has earned income coming in because it enables me to deploy capital at lower valuations than I would have otherwise, I actually like sector-level volatility far more. Such volatility enables me to not only deploy new capital at attractive yields and valuations into the out-of-favor sectors, but it also enables me to recycle some capital out of in-favor sectors into these out-of-favor sectors, thus further amplifying the amount at which I am able to take advantage of these sell-offs. This is especially true when these dislocations are far more substantial than the underlying changes in fundamentals.

Today, BDCs and alternative asset managers are being hammered by negative headlines, causing leading BDCs like Blackstone Secured Lending (BXSL), Hercules Capital (HTGC), Ares Capital Corporation (ARCC), Blue Owl Capital Corporation (OBDC), and many others to sell off aggressively, while alternative asset managers like Blackstone (BX), Ares Management (ARES), Apollo Global Management (APO), KKR & Co. (KKR), and others are also getting hammered. At the same time, however, these companies all continue to post solid underlying fundamentals, are growing their assets under management and their dividends (in the case of alternative asset managers), and (in the case of BDCs) are keeping their non-accruals fairly low while continuing to pay out attractive dividends. Thus, I think that the sell-off presents a compelling buying opportunity.

Meanwhile, midstream companies generate fairly stable cash flows regardless of the commodity price environment, but they have been soaring higher recently, as have utilities and other infrastructure plays. Precious metals miners have also been soaring higher. Yes, the fundamentals are solid in these businesses, but I think that, in some cases, the run-up has been excessive relative to changing fundamentals. Thus, I am finding increasing opportunities to trim or even sell my holdings in the energy, infrastructure, and precious metals sectors and recycle the capital into higher-yielding and deeply undervalued yet still high-quality alternative asset managers and BDCs that are posting solid fundamentals yet are deeply undervalued.

My Three Unshakable Pillars for Navigating Market Rotations

So how exactly am I doing this, and what principles do I follow as I decide where and how much to trim from positions that are soaring and reallocate to positions that have been oversold by the market?

First of all, value investing discipline guides all of my trades. What that means is I try as much as possible to block out market sentiment and not allow stocks rising rapidly to color my view of fair value, nor a plunging stock to color my view of fair value. Instead, I look at the fundamentals, the conservative outlook for future growth for that business, and determine what a fair value is for that stock.

Another pillar is maintaining portfolio diversification. What this means is that even if one sector is very much in favor and another one is very much out of favor, I seldom would ever go fully into the out-of-favor sector, even if I think it offers much better value, because ultimately I realize that I am not omniscient and that the market could be seeing something that I am not. Therefore, I try to maintain at least some portfolio diversification to guard against a major macro shift completely obliterating my portfolio.

At the same time, though, I implement opportunistic capital recycling. So when fundamentals and value diverge, I tend to rotate capital as guided by my valuation principles, while at the same time somewhat limited by my diversification framework into rotating capital from overvalued positions into undervalued positions.

In so doing, I still maintain diversification, which helps keep my risk-adjusted returns attractive, while also accelerating the compounding process of both my passive income stream as well as my total returns over the long term. It can definitely feel painful in the short term, especially if I sell a position and it continues to soar higher, or I buy a stock, and it continues to plunge lower. In fact, more often than not, this seems to be the case. However, over the long term, this strategy has paid off richly for me, and I expect it to continue doing so moving forward, especially if I can maintain proper diversification so that, at the times when I do get it wrong, it does not completely set me back.

Positioning for AI Disruption Without Overreaching

Another major risk to the strategy in the current market is that AI disruption has the potential to be very significant in the coming years. Therefore, if the market is selling off a stock because of concerns that AI is going to disrupt industries such as the software-as-a-service industry, as I recently detailed here, I need to take extra precautions to make sure that I am not betting heavily against future disruption. I think one way to do this is to either steer clear of sectors altogether or, if I feel like I have a degree of understanding of how the disruption is going to impact it, try to position myself conservatively in the capital stack such that it will likely weather the disruption just fine and, due to the large margin of safety in the valuation that I am buying at, will end up generating attractive total returns over time. This is what I am doing with my investments in senior secured software loans in diversified, actively managed portfolios with skilled managers like HTGC, rather than simply buying the dip in software common equities.

Why This is the Most Important Market Rotation Nobody is Talking About

While chasing hot stocks can be fun and even easy in the near term and lead to strong short-term results, you also run the risk of buying near the top and then getting hammered on the inevitable correction. Instead, if you can be guided by valuation and fundamentals and invest where those are disconnected, while still tempering that opportunistic capital recycling approach with proper portfolio diversification principles, you can view periods of market volatility like this as incredible gifts, as they enable you to allow valuation multiple expansion and contraction to work alongside dividends and per-share growth to accelerate your compounding process over time.

Leave a Reply