5 Small Stocks, 5 Super-Sized Payouts of Up To 11%

Brett Owens, Chief Investment Strategist

Updated: March 6, 2026

What’s better than getting to buy 6.6%-11% yields at discounted prices?

How about snapping those sweet dividend payers while momentum is on your side?

Late in 2025, I wrote about a “small-cap reawakening”—a bullish tailwind from retreating Federal Reserve rates that had begun to propel smaller companies forward and could continue well into 2026.

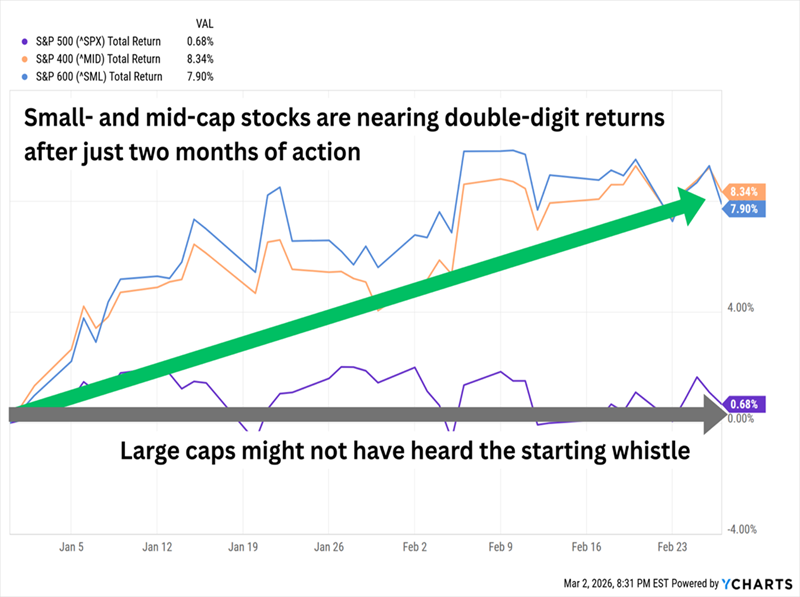

So far, so true. Small- and mid-cap stocks (or “SMIDs”) alike have been cruising full sail ahead while their larger cousins have been dead in the water.

2026 Has Been a Reversal of Longstanding Large-Cap Dominance

Better still for you if you haven’t yet taken the plunge into Wall Street’s more diminutive stocks: Small caps’ hot start has done little to drive up valuations. They still look like a screaming bargain compared to the market’s bigger names:

Broad-Market Forward P/Es:

- S&P 500: 21.2

- S&P MidCap 400: 17.0

- S&P SmallCap 600: 15.6

Fair warning: Economic turbulence is almost always tougher on smaller-cap equities, so we could always be a market scare away from a flight back into large caps.

The fuel driving smaller companies could run out in a few months, too. The Fed declined to move its target interest rate lower in late January, and the market is betting we don’t see another step lower until summer at the soonest.

But we’re all aware that a step into small caps means swallowing at least a spoonful of risk. Our best bet? Find the most advantageously positioned small caps… and get paid a truckload while we hold on for the ride.

Which is exactly what I see in these five small caps paying us between 6.6% and 11.0% right now.

Washington Trust Bancorp (WASH)

Dividend Yield: 6.6%

Financial firms as a group don’t deliver much more income than the broader market, but you can find some downright respectable yields in the sector’s smaller names: specifically, regional banks and credit unions.

Washington Trust Bancorp. (WASH), for instance, currently pays more than 6%.

This 225-year-old regional bank is neither in Washington, D.C., nor Washington State. Instead, it was named for the nation’s first president, and it proudly claims that it was “the first bank to print George Washington’s likeness on currency—69 years before President Washington appeared on the federally issued one-dollar bill and 132 years before the Washington quarter appeared.”

The operations are typical bank fare: personal and business banking offerings such as checking, savings, mortgages, financing and wealth management. The stock really hasn’t been noteworthy, either, delivering subpar performance relative to both the market and the financial sector for quite some time. WASH shares were barely above breakeven in 2025—and that’s only once we include its sizable dividend!—following a balance sheet repositioning near the end of 2024.

But Washington Trust is alive and well in 2026. In January, the company’s Street-beating results were helped by net interest margins that improved by 16 basis points YoY for the fourth quarter, and by 53 basis points YoY for the full year. The news sparked one of the biggest moves in WASH stock in years. Meanwhile, shares still trade for just 10 times earnings that are expected to jump by 27% in 2026 and offer one of the best yields in banking.

Though I’d Like to See Washington Trust Make a Move in Its Dividend, Too

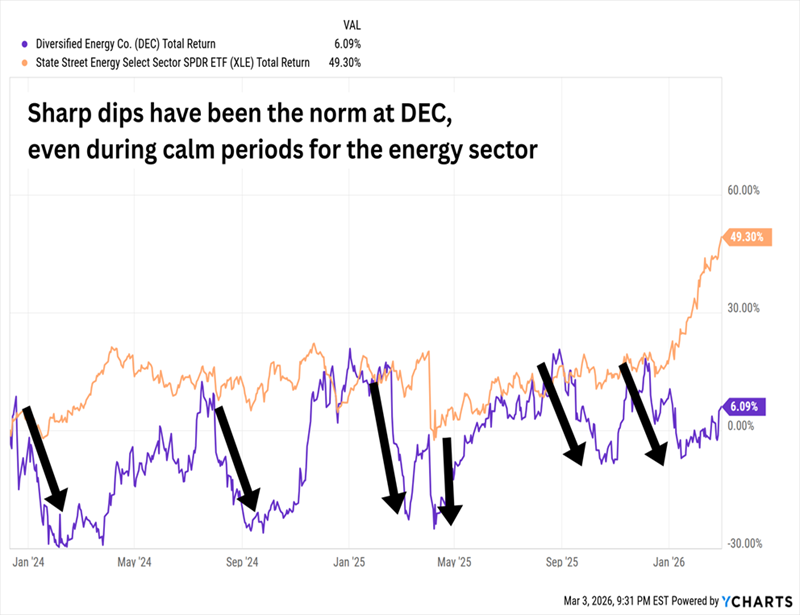

Diversified Energy Company (DEC)

Dividend Yield: 8.0%

When we think of “integrated” energy companies, we typically think of mega-cap titans like Exxon Mobil (XOM) and Chevron (CVX). But $1 billion Diversified Energy Company (DEC) checks off the right boxes, too.

It produces predominantly natural gas, but also some oil and natural gas liquids (NGLs), from the Appalachian (70% of production) and Central (30% of production) regions of the U.S. It also has about 17,000 miles of gathering and transportation lines, as well as compression stations, and it’s a top-25 North American gas marketer. It even has a well retirement service arm: Next LVL Energy.

It’s an odd stock with an odd history. The company started in the U.S. back in 2001, but it didn’t list publicly until 2017—on the London Stock Exchange. It only began trading in the U.S. in 2023, when it launched a secondary listing on the New York Stock Exchange; those NYSE shares became the company’s primary listing in 2025. Shares have delivered all the excitement of a small-cap company since then.

But They’ve Also Delivered Very Little Upside

That largely reflects the Diversified model—rather than undergoing capital-intensive drilling and development programs that can make splashy discoveries, DEC instead acquires long-life assets and tries to squeeze as much life out of them as possible.

Last year was no exception. The company completed the acquisition of “liquids-rich” Maverick Natural Resources in March 2025, then closed on a purchase of Oklahoma-based oil-and-gas E&P firm Canvas in November. The buying has continued this year; DEC recently announced it was buying natural gas properties in east Texas from Sheridan Production.

There’s admittedly not much room for breakneck growth in this model. But it does adequately fund a generous dividend yielding 8% right now, on a stock that trades at less than 8 times this year’s earnings estimates.

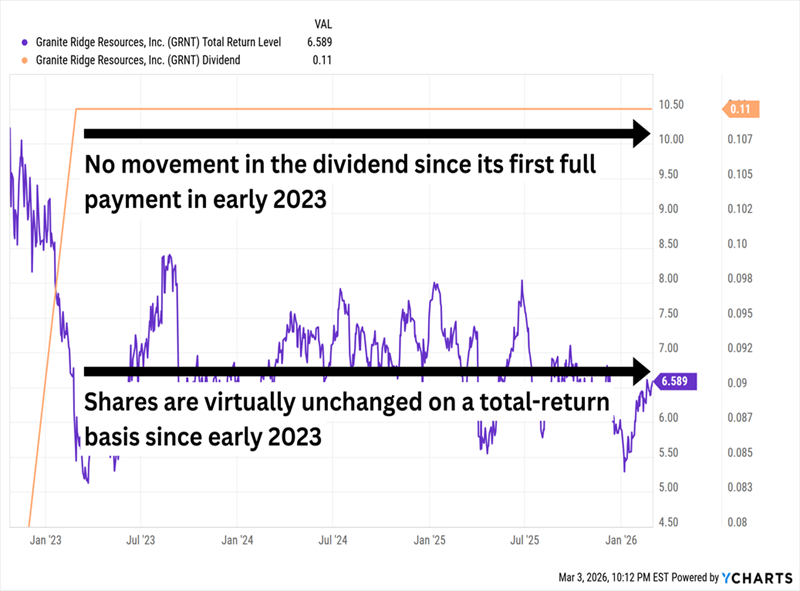

Granite Ridge Resources (GRNT)

Dividend Yield: 8.5%

Granite Ridge Resources (GRNT) is another energy name with an unorthodox business model. It says it “combines the agility of an investment firm with the expertise of an energy company.” In practice, it doesn’t operate anything—it simply holds oil and gas assets in the Permian, Eagle Ford, Bakken, Haynesville, DJ and Appalachian formations.

It’s almost fitting, then, that the company didn’t go public via a traditional IPO, but via special purpose acquisition company (SPAC). Investment firm Grey Rock Investment Partners merged in October 2022 with Executive Network Partnering Corporation (the SPAC).

GRNT hit the market with a thud, dropping like a rock over the first few months. Since then, it has delivered roughly breakeven returns (and that’s after factoring in the 8%+ dividend), which is right in line with its nonexistent dividend growth.

However, like DEC, Granite Ridge might have been building toward something in 2025, with the company projecting 28% production growth for the full year. That should allow the company and its roughly 3,200 wells to take better advantage of any improvements in price.

But unlike other small energy names, Granite Ridge appears to be a primarily steady cash flow and dividend producer first, and a growth prospect second.

Leave a Reply