5 Small Stocks, 5 Super-Sized Payouts of Up To 11%

Perrigo (PRGO)

Dividend Yield: 10.2%

Perrigo (PRGO) is an over-the-counter health and wellness company with a wide range of products we’re all used to seeing on Walgreens and CVS shelves: sinus and allergy relief, antacids, sleep aids, pain relievers, toothbrushes, skin care, vitamins, contraceptives and more.

It’s also a long, long, long way removed from its heyday of roughly a decade ago.

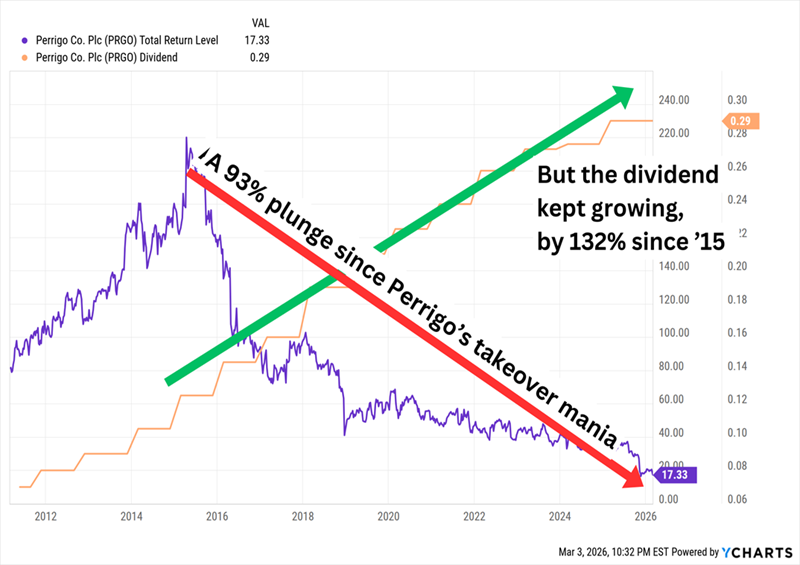

In 2015, Perrigo was a large cap on the rise—so much so that it attracted the advances of global generics specialist Mylan. PRGO rebuffed Mylan several times, most notably in April 2015 when it turned down a $205-per-share offer, then a $232-per-share offer shortly thereafter. Perrigo’s board, then its shareholders, turned back a hostile bid later in the year.

After That, It Was Likely Nothing But Regrets

The top and bottom lines have stagnated or declined in most years since 2015. Generics margins suffered amid growing competition, and FDA approvals tapered off. The company has since undergone multiple restructuring plans and pivoted to lean harder into self-care products. But it’s still sliding; during its Q4 2025 report, it said sales would be down 1.5% to 5.5% in 2026, and adjusted diluted earnings per share would fall by 16% to 27%.

A few days earlier, it also announced that it would keep its dividend level—maybe not surprising given its continued weakness, but perhaps another warning sign given that PRGO is currently riding a 22-year streak of annual dividend growth.

Perrigo is very much a stock to watch just given the potential to pick up a double-digit yielder on the cheap—it currently trades at a skinny 5 times 2026 earnings estimates. But we need to see some signs of operational stabilization first; otherwise, this small cap will just keep getting smaller.

Insperity (NSP)

Dividend Yield: 11.0%

Insperity (NSP) is a human resources (HR) and business solutions provider to small- and medium-sized businesses. That’s payroll, benefits, HR, employee onboarding, time and attendance, performance and more, provided through multiple Insperity-branded platforms.

This is a name that has only recently started to ping my high-yield radar, which usually means one of two things has happened:

- A massive dividend increase, say, double or more (rare)

- The stock has plunged into the earth’s core (common)

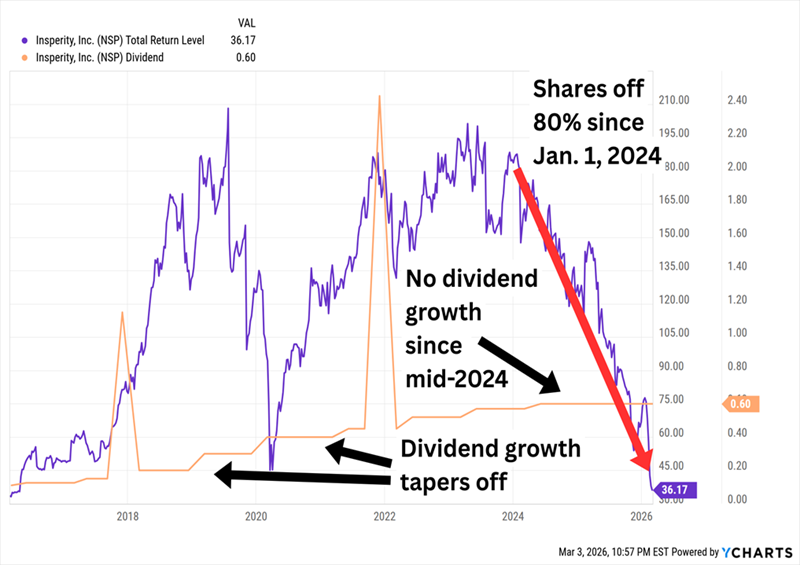

It’s Pretty Clear What We Have on Our Hands

The stock is unsurprisingly cheap as a result, trading at 10 times this year’s earnings estimates.

The question is whether NSP is a generational value play or a falling knife.

The plunge was due to a complete erosion of Insperity’s bottom line, as well as sentiment for both small- and midsized businesses and the labor market. The company earned $171.4 million in 2023, then $91 million in 2024, then suffered a $7 million net loss in 2025. Health care costs have been a major factor here, chewing into Insperity’s margins.

But the top line hasn’t flinched. Revenues have climbed in all but one year over the past decade, and they’re expected to keep rising by single digits in each of the next two years. A renegotiated contract with UnitedHealth Group (UNH) could relieve some of its cost pressures. And there’s potential in its new Insperity HRScale—an HR platform built in partnership with Workday (WDAY) that promises “faster deployment and simpler setup” and that the company expects will host 6,000 to 8,000 paid worksite employees (WSEEs) by year’s end.

It might be enough for a turnaround, but even if it is, we have to consider whether the dividend will still be there. The $2.40 per share that Insperity pays across the year was more than twice NSP’s adjusted earnings in 2025, and it’s projected to overshoot 2026 profits, too.

This 11% Dividend Is Overlooked, Too—But in Much Better Position

I don’t want to have to pinch my nose and pray before buying a double-digit dividend.

So I won’t. And you shouldn’t, either.

Right now, one of my favorite home-run dividends pays every bit as much as NSP. But it’s not a down-on-its-luck HR play hoping for a rebound in the economy and job market—it’s a heavily diversified, brilliantly built bond portfolio that is also set up to rise in price if interest rates keep falling.

This fund checks off just about every income box I can think of:

- It pays a whopping 11% in annual income!

- It has increased its dividend over time

- It has paid out multiple special dividends

- And it pays its dividends each and every month!

That’s a resume few income investors could resist … and why would we?

This fund pays us $1,100 for every $10K we invest. All we need to do is sit back, relax, and let a skilled manager call the shots.

Leave a Reply