Investment Trust Dividends

UKW’s dividend remains resilient.

Updated 30 Jan 2026

Disclosure – Non-Independent Marketing Communication

This is a non-independent marketing communication commissioned by Greencoat UK Wind (UKW). The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

The UK government has announced the result of its consultation into changes to the inflation indexation used in the Renewables Obligation (RO) scheme. The RO scheme will, from 01/04/2026, be indexed at the consumer price index (CPI), instead of the retail price index (RPI).

Greencoat UK Wind (UKW) had released its factsheet for 31/12/2025 on the day of the announcement and made some changes to its net asset value (NAV) and dividend policy as a result of this news on 29/01/2026.

While neither of the two possible changes to the RO scheme that were being consulted on were ideal,this is clearly the least-worst outcome and removes a key piece of uncertainty that had been hanging over renewable energy infrastructure investment companies. Accordingly, UKW’s shares initially rose as much as 4.5%, before settling c. 0.7% higher by the end of the day (28/01/2026).

Considering the result of the consultation, it makes sense to us that UKW would change the inflation linkage in its dividend policy from RPI to CPI to ensure that dividend cover remains strong and does not compromise future dividend growth nor dividend cover.

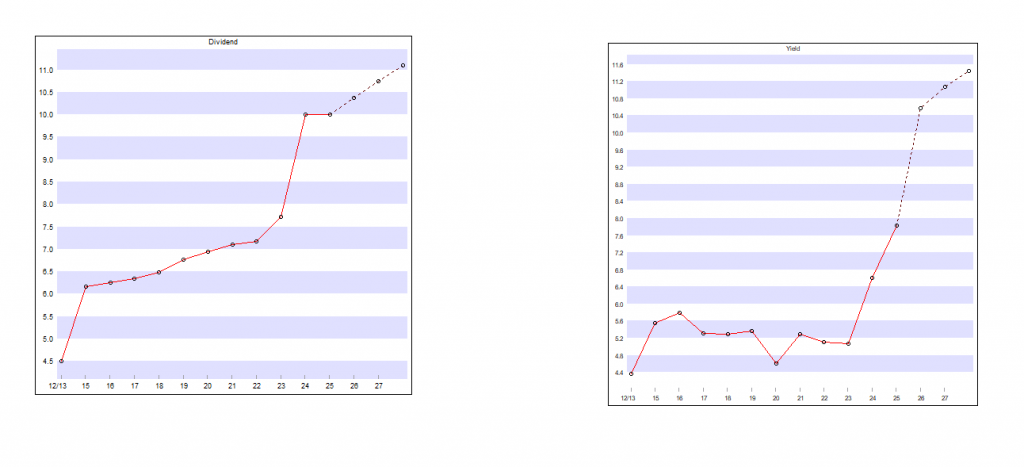

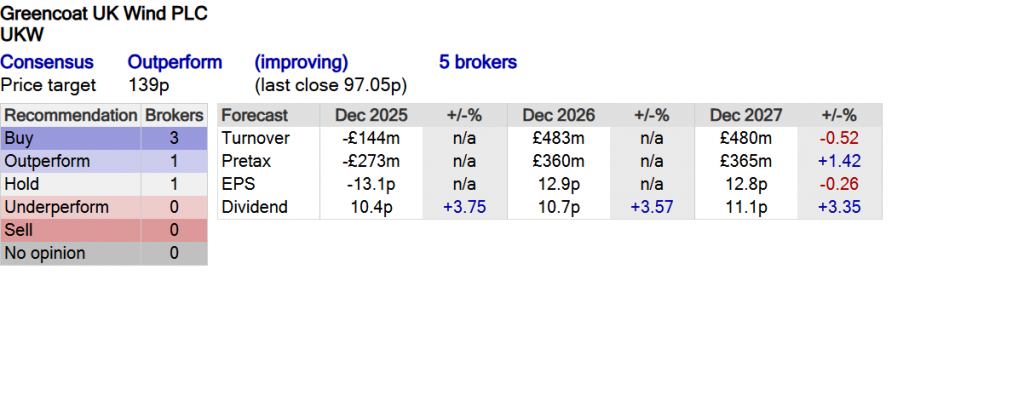

Indeed, UKW has increased its dividend by RPI or better for each of the 12 years it has been a listed company. The dividend has grown from 6p per share at IPO to 10.35p by 2025, a cumulative increase of 72.5%, and the target is to increase this further to 10.70p in 2026. This dividend progression has been underpinned by strong cashflow generation since IPO.

The company’s forward-looking dividend cover and cashflow generation expectations remain robust and the former is substantially unchanged. This leaves UKW with one of the most robust dividends in the sector and unique in that the dividend is still linked to inflation.

With shares trading at 98p at the time of writing (on 29/01/2026), the forecast yield based on UKW’s 2026 dividend target is 10.9%. That’s extremely attractive, at almost two-and-a-half times the 4.5% yield offered by a 10-year UK government bond.

In addition, UKW’s structurally higher dividend cover means that it still has options to deploy surplus cashflows towards new investments, buybacks or reducing debt. We note that UKW continues to buy shares back, illustrating the confidence the board has in strength of the balance sheet.

As discussed in our recent feature, the fundamentals of the renewable energy sector appear to remain as strong as ever, and UKW has delivered impressive NAV total returns of 185% since launch 12 years ago, yet shares currently trade below their IPO price, suggesting, on a discount of c. 27%, there remains latent value, in our view.

With a dividend re-investment plan, you fail by the month, not by the year.

Remember a bad plan as long as it has an end destination is better than no plan.

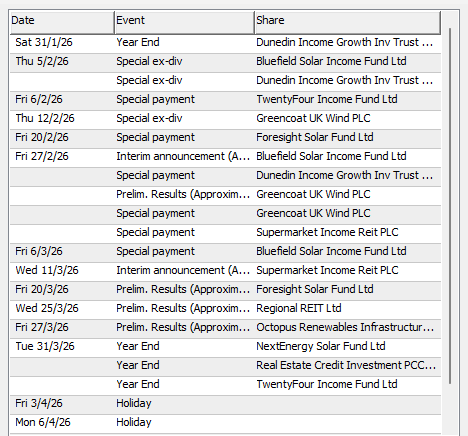

The current best month for dividends is February

Then (January) April

and the worst month is March where currently only one dividend is due, although some February dividends could be slip into March.

The February dividends when invested should earn another 3 dividends for the year.

Greencoat UK Wind PLC is pleased to announce that the Company has been named winner of the Renewables – Active category in the AJ Bell Investment Awards 2025.

AI Overview

Greencoat UK Wind (UKW) is considered by some analysts to be an interesting investment due to its attractive dividend yield (around 10%), strong cash flows, inflation-linked revenue, and a discount to its Net Asset Value (NAV), potentially offering significant upside if rates fall and discounts narrow; however, recent performance has been hit by lower wind speeds and higher interest rates impacting sector valuations, though its long-term strategy focuses on outperformance through asset management and accretive investments, with recent refinancing showing resilience.

Potential Positives (Bull Case):

Potential Risks (Bear Case):

Analyst Sentiment (Recent):

Conclusion:

Greencoat UK Wind presents a compelling case for income-focused investors seeking inflation-linked returns, but it’s not without risks tied to macro-economic factors and weather. Its valuation discount and strong cash flows make it interesting, but investors should be prepared for volatility, as highlighted by recent performance.

CANACCORD STARTS GREENCOAT UK WIND WITH ‘HOLD’

Dividend Policy and 2026 Dividend Target

The Company also announces a quarterly interim dividend of 2.59 pence per share with respect to the quarter ended 31 December 2025.

Dividend Timetable

Ex-dividend date 12 February 2026

Record date 13 February 2026

Payment date 27 February 2026

The Company has been reviewing its dividend policy in line with the range of potential outcomes from the RO Indexation Consultation. The Company has, for 12 consecutive years, increased its dividend by RPI or better, from a 6 pence dividend per share at IPO to 10.35 pence in respect of 2025. Dividend progression has been underpinned by strong cashflow generation.

The principal instrument from which the Company derives explicit RPI cashflow linkage is the RO scheme, which will now be indexed to CPI. The Company’s Contracts for Differences instruments also have explicit CPI linkage. The Board has therefore determined that its dividend policy will now be to aim to provide shareholders with an annual dividend that increases in line with CPI inflation.

Accordingly, the Company announces an increase in the target dividend for 2026 to 10.7 pence per share in line with CPI for December 2025 of 3.4%. The Company’s forward looking dividend cover expectations remain robust and are substantially unchanged.

For the avoidance of doubt, the quarterly interim dividend of 2.59 pence per share with respect to the quarter ended 31 December 2025 remains unchanged.

CT Global Mgd – CMPI – Half Year Report to 30 November

Unaudited Half-Year Results for the Six Months ended 30 November 2025

The Board of CT Global Managed Portfolio Trust PLC (the ‘Company’) announces the unaudited half-year results of the Company for the six months ended 30 November 2025.

Income Shares – Financial Highlights and Performance Summary for the Six Months

· Dividend yield(1) of 6.2% at 30 November 2025, compared to the yield on the FTSE All-Share Index of 3.2%. Dividends are paid quarterly.

· Net asset value total return(1) per Income share of +12.0% for the six months, outperforming the total return of the FTSE All-Share Index of +11.8% by +0.2 percentage points.

Growth Shares – Financial Highlights and Performance Summary for the Six Months

· Net asset value total return(1) per Growth share of +11.9% for the six months, outperforming the total return of the FTSE All-Share Index of +11.8% by +0.1 percentage points.

· Net asset value total return per Growth share of +208.8% in the 15 years to 30 November 2025, the equivalent of +7.8% compound(1) per year. This compares with the total return of the FTSE All-Share Index of +213.5%, the equivalent of +7.9% compound per year.

The Chairman, David Warnock, said:

“The Board and Manager continue to believe the Portfolios comprise high class investment companies, diversified across geography and investment style and are well set to deliver future shareholder returns”.

Notes:

(1) Yield, total return and compound annual NAV total return – See Alternative Performance Measures.

Chairman’s Statement

Highlights

• Net asset value (‘NAV‘) total return for the six months of +12.0% for the Income shares and +11.9% for the Growth shares as compared to the total return for the FTSE All-Share Index of +11.8%

• Income shares dividend yield of 6.2% at 30 November 2025

Investment performance

For the six months to 30 November 2025, the NAV total return was +12.0% for the Income shares and +11.9% for the Growth shares. The total return for the benchmark index for both share classes, the FTSE All-Share Index, was +11.8%. Of relevance and for interest, the FTSE All-Share Closed End Investments Index total return was +13.1% for the period.

These six months saw strong returns across equity and bond markets as worries over a global trade war dissipated. This is mostly thanks to the initial level of tariffs announced by President Trump back in April being watered down and a number of ‘trade deals’ being announced between the US and its trading partners. Economic data remained generally positive, with falling – yet still above central bank target – inflation, allowing central banks to further cut interest rates. In the UK, the long-awaited budget brought some relief in respect of keeping financial markets and Labour backbenches satisfied but failed to deliver policies to boost the UK economic growth outlook.

UK equities posted solid returns over the six-month period, with a +12.4% total return for the FTSE 100 and a +7.4% total return for the FTSE 250. Elsewhere, in sterling terms, US equities continued their recovery from the ‘Liberation Day’ selloff, with a +18.6% total return for the S&P 500, while in Europe the total return for the MSCI Europe ex UK Index was +9.4%. The strongest returns included South Korea, with a total return of +52.6% from the MSCI Korea Index. Global government bonds, as referenced by the FTSE World Government Bond Index (GBP Hedged) were up +2.5% and the gold price continued its ascent, up +28.1%.

From 1 June 2025, the beginning of the Company’s current financial year, the investment portfolios have been managed by Investment Managers Adam Norris and Paul Green, supported by the Manager’s broader EMEA Multi-Asset Solutions team (of which they are members). The previous longstanding Investment Manager, Peter Hewitt, has retired and the Board wishes him a long and happy retirement, while thanking him for his years of service.

The Investment Managers’ Review follows, and it is pleasing to see that, in their first six month period, the NAV total return of both Portfolios was strong and also marginally ahead of the benchmark index. The Investment Managers have been repositioning between sectors and regions and highlights of their recent investment activity are set out in their review.

Dividends

As I referenced in the 2025 Annual Report and Financial Statements, in the absence of unforeseen circumstances, it was (and remains) the Board’s intention to pay four quarterly interim dividends, each of at least 1.90p per Income share so that the aggregate dividends for the financial year to 31 May 2026 will be at least 7.60p per Income share (2025: 7.60p per Income share).

To date, first and second interim dividends in respect of the year to 31 May 2026 have been announced and paid, each at a rate of 1.90p per Income share (1.85p per Income share in the corresponding periods in the year to 31 May 2025).

The minimum intended total dividend for the financial year of 7.60p per Income share represents a yield on the Income share price at 30 November 2025 of 6.2% which was materially higher than the yield of 3.2% on the FTSE All-Share Index at the same date.

Borrowing

At 30 November 2025 the Income Portfolio had total borrowings drawn down of £7 million (9.2% of gross assets), unchanged over the period, the investment of which helps to boost net income after allowing for the interest cost. The Growth Portfolio had no borrowings, also unchanged.

Management of share price premium and discount to NAV

In normal circumstances the Board aims to limit the discount to NAV at which the Company’s shares might trade to not more than 5%. During the six months to 30 November 2025 the Income shares traded at an average discount to NAV of -0.4% and the Growth shares traded at an average discount of -3.5%. At 30 November 2025, the Income shares and Growth shares stood at a premium to NAV of +0.6% and +0.9% respectively.

The Company is active in issuing shares to meet demand and equally in buying back when this is appropriate. During the six months to 30 November 2025, 200,000 Income shares were bought back for treasury at an average discount of -3.6% to NAV and then subsequently resold from treasury at an average premium of +1.5% to NAV. In addition, 2,430,000 new Income shares were issued from the Company’s block listing facilities at an average premium to NAV of +1.6%. 1,578,000 Growth shares were also bought back to be held in treasury at an average discount to NAV of -3.8% and 450,000 Growth shares were resold from treasury at an average premium to NAV of +1.6%.

Since the end of the period, a further 3,095,000 new Income shares have been issued and a further 765,000 Growth shares have been resold from treasury. To facilitate this demand, at the start of December 2025, the Company obtained a further block listing of 8,000,000 Income shares, which can be allotted, when there is demand. The Income shares were issued and the Growth shares resold from treasury at average premiums to NAV of 1.6% and 1.5% respectively. Much of this recent demand has come from former shareholders in European Assets Trust which underwent a corporate transaction with The European Smaller Companies Trust (‘ESCT‘) in the autumn. Shares in ESCT are not eligible to be held through the Manager’s savings plans and we welcome those investors who have decided to invest instead in CT Global Managed Portfolio Trust.

Last year was one to remember for dividend hunters and followers of this column, generating more income than expected and a record capital gain.

Lee Wild explains how it happened.

29th January 2026

by Lee Wild from interactive investor

It seems difficult to believe that so much was packed into 2025. Events that might otherwise have condemned global financial markets to a miserable time after back-to-back winning years, turned out to be a trigger for a third consecutive prosperous 12-month period for investor

US President Donald Trump continued to have an outsized impact on stock performance. His radical Liberation Day tariffs caused one of the biggest stock market corrections in decades. However, some serious backpedalling on the scale of import duties gave birth to the amusingly named TACO trade, or Trump Always Chickens Out.

Equity markets recovered almost as quickly as they had fallen, and every major global stock index ended 2025 ahead. For UK investors, it was thrilling to see the FTSE 100 register a 21.5% gain, its biggest annual increase since 2009 and better than anything Wall Street could muster.

Falling interest rates have played a significant role in the spectacular rebound and UK stock market revival, as inflation washed through the system. Investors have also been excited by major themes such as artificial intelligence (AI) on which tech giants have been spending hundreds of billions of dollars. Now the pressure is on to make it work, and big profits are needed to justify spending and sky-high valuations.

New themes such as quantum computing grabbed headlines, although momentum has been lost more recently. It was the same for crypto, where bitcoin raced to a new high at $126,000, dragging related assets with it, before a swift pullback. Enthusiasm for precious metals amid geopolitical uncertainty has seen prices for gold and silver regularly make record highs. And there seems no obvious end to the mining sector boom.

Trump proved again that he has the power to move markets in either direction, when he gave a massive boost to the global defence sector. Bullying other countries into spending more on their militaries propelled UK operators such as BAE Systems

BA.

and Rolls-Royce Holdings

RR.

to record highs.

And the ongoing precious metals rally reflects investor fears about the president’s unique approach to domestic and foreign policy. Both the metals and defence sectors are key reasons why the FTSE 100 just broke above the psychologically important 10,000 level.

And geopolitics remain a major talking point in 2026. Already this year we’ve had the seizing of Venezuela’s leader by American forces and the threat of repercussions for European countries opposing his annexation of Greenland. It’ll be interesting to see how the land lies when Trump faces mid-term elections in November. Before then, we’ve got any number of potential flashpoints and concerns to navigate. It’ll be another interesting year for sure.

Income portfolio performance in 2025

A year ago, I expected the 10 stocks in this income portfolio to generate £10,338. I like to go for a little bit more than the round £10,000 as a kind of insurance policy should anything go wrong with one or more of the choices. I needn’t have worried. I ended up with £10,680, a chunk of which is attributed to an unexpected special dividend from Sainsbury (J)

SBRY

Apart from a small shortfall from Rio Tinto Ordinary Shares

RIO

other constituents delivered pretty much the income I expected. As well as the £1,452 from Sainsbury’s, the portfolio banked £1,483 from my favourite income play M&G Ordinary Shares

MNG

.But the biggest income generator in 2025 was Legal & General Group

LGEN

where the 9.2% yield I locked in a year ago dropped £1,653 into the coffers.

Targeting a 6.8% yield, the portfolio delivered 7%. But there was a fantastic capital return this time, too. In fact, it was the biggest profit generated by any of my equity income portfolios.

By the end of the 12 months, the £152,000 it cost to buy the 10 stocks had turned into £189,963. Both HSBC Holdings

HSBA

and M&G were up almost 50% and GSK

GSK

,Rio Tinto and British American Tobacco

BATS

all rose 30% or more. Only Taylor Wimpey

TW.

fell, dropping 9%, although the income was welcome. Combined, the income and 25% capital gain generated by the entire portfolio gave a total return of 32%.

As always at this point, I issue a reminder that investors don’t typically revamp an entire portfolio at the beginning of a calendar year. The reason I make changes to this income portfolio is to ensure the exercise remains relevant whether you’re an existing investor or coming to the portfolio for the first time. This year there are four changes.

The shares that stay in 2026

Rising stock markets means it has cost a bit more to put together this year’s portfolio. To achieve the targeted £10,000 of annual income, I’ve had to spend £168,000, the same as in 2024, but £16,000 more than in 2025. The prospective yield is 6%.

With share prices significantly higher than they were this time last year, there are fewer eye-catching yields out there, especially in the blue-chip index. However, I’ve been able to stick with a few of the same high yielders in 2026 and some of last year’s other stocks for diversification.

I’m remaining faithful to the pair of star income plays of 2025 – L&G and M&G – both yielding well over 9% and between them generating over £3,000 of income. This time they yield 8.4% and 6.9% respectively, and their consistency over the years would be foolish to reject this time.

The tariff playbook: why I’m sticking with UK markets in 2026

Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

While I don’t expect Sainsbury’s to return anything like the 9.7% it generated last year – it’ll likely be about half that – it remains the best income option in the grocery sector. It’s also working hard on growing market share, battling the discounters such as Aldi and Lidl while offering premium alternatives to Waitrose and Marks & Spencer Group

MKS

In the blue-chip oil sector, it’s BP

BP.

that keeps its spot in this income portfolio. At around 5.5%, it yields about 160 basis points more than Shell

SHEL

and, while it’s slightly more expensive, it outperformed its rival too in terms of share price performance. There’s seems little reason to switch sides.

Utilities are rarely exciting, which can be great for an income portfolio like this. However, last year National Grid

NG.

generated a dividend yield of 4.8% for us plus a 21% capital return. And despite a more modest 3.9% predicted yield in 2026, I’m keeping this diversifier for its defensive appeal, inflation-linked dividend and attractive forecast earnings growth.

I’ve given this final stock a lot of thought, and the decision to keep it was not an easy one. I want a housebuilder in the portfolio, and the sector still screens as cheap, trading on 0.8x price to book, according to Morgan Stanley. Taylor Wimpey might not be the analysts’ favourite, perhaps exposed more than others to slower house price growth, but it has an eye-catching 8.3% dividend yield and is similarly valued to sector peers. That’s impossible to ignore.

Heading for the exit

British American Tobacco yielded 7.5% in dividends last year plus a 32% capital return, outperforming sector peer Imperial Brands

IMB

But this year may be harder, with weaker cigarette fundamentals and growth in so-called New Category sales. I’m looking for better value and a more compelling investment case.

I’m grateful to GSK for three years of strong dividend income, including last year’s 4.7% yield and 30% share price gain. But the shares now trade at the top of their 13-year range of roughly 1,300p to 1,800p, and a forecast dividend yield of 3.5% doesn’t cut it. Time to let another stock have a go.

HSBC was the second-biggest riser in the 2025 portfolio with a 48% rally, but it also delivered the 6% dividend yield I’d picked it for. Of course, I still want to own a bank stock here, but a sector-wide rally has made it less attractive for income seekers, yielding a more modest 4%.

Rio Tinto is a fantastic company, and it has provided valuable dividend income over the years. However, the shares are up 46% in the past six months at a record high, and the yield has dropped to almost 4% from nearly 6% in 2025. A potential mega-merger with Glencore

GLEN

also carries with it risk, so I’m going without a miner in the portfolio this time.

New holdings for 2026

Despite a 56% surge in the past 12 months, NatWest Group

NWG

is the cheapest UK bank and yields 5%, much more than its high street rivals. Yes, it is a little more sensitive to interest rates, but it’s both a fitting replacement for HSBC and gives us exposure to a sector which should benefit from an improving UK economy.

Land Securities Group

LAND

makes its debut in this income portfolio series, which tells you all you need to know about the parlous state of the property sector in recent years. However, the ship has steadied and LandSec offers one of the best yields in the sector at around 6.4% plus an attractive valuation.

Pennon Group

PNN

is the second utility in this year’s portfolio. The water company had underperformed peers in recent years but has staged a recovery, now offering a sector-leading 6% yield. As utilities are minded to, the company set out its five-year dividend policy to 2030 which will see the payout grow in line with the Consumer Price Index including Owner Occupiers’ Housing Costs (CPIH).

My rationale for ejecting BATS this year was to find “better value and a more compelling investment case”. There’s not much choice in the UK tobacco sector, but Imperial Brands and its 5.5% prospective dividend yield is a worthy replacement. The valuation is undemanding – it’s much cheaper than BATS – and the view in the City is that earnings visibility and moderate leverage should guarantee superior capital returns.

So only general advice not trading advice.

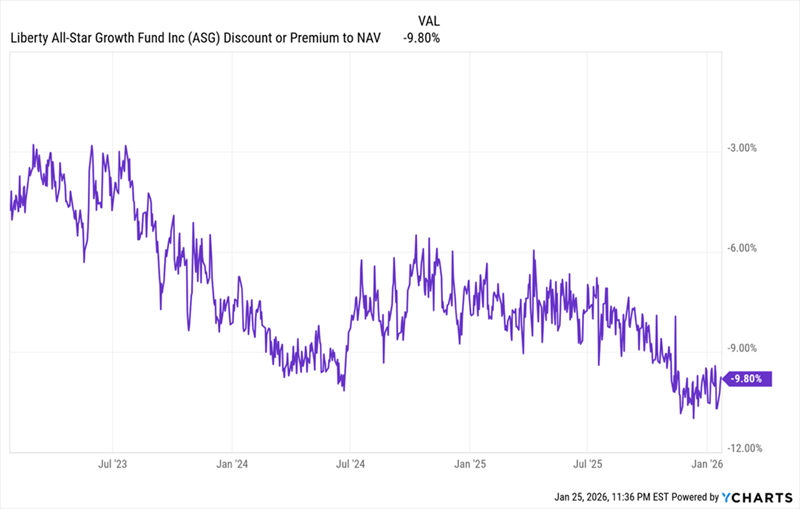

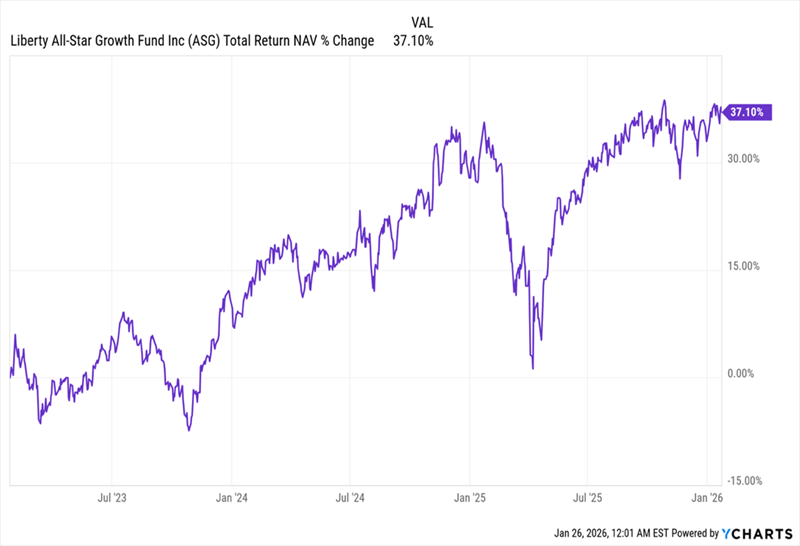

Recession in 2026? Here’s My Take (and a 9% Payer to Profit) by Michael Foster, Investment Strategist My prediction for 2026? Strange as it may sound, given the wild headlines we’re seeing pretty much daily, I’m calling for more of the same. As I said a couple weeks ago, I expect around 12% returns from the S&P 500 this year. That’s why we’ve been adding to the equity CEFs in the portfolio of our CEF Insider service. Today I want to talk about one of our holdings, in particular: a 9%-payer called the Liberty All-Star Growth Fund (ASG). We’re zeroing in on this one because its discount to net asset value (NAV, or the value of its underlying portfolio) is the biggest it’s been in three years. As a result, we can buy ASG, and its portfolio of US blue chips, for around 90 cents on the dollar. That markdown helps reduce any worries around valuation as the market keeps rising higher. Bubble Worries Are a Plus for Us (and This 9%-Paying Fund) Remember that recession we were told had a 100% chance of happening back in 2022? Well, we’re still waiting for it. Meantime, US GDP rose 4.4% at the last reading for the third quarter, and our most up-to-date estimate, the Atlanta Fed’s GDPNow indicator is showing over 5% growth for Q4. These are strong numbers, especially with average annual growth around 3%. Then there’s AI, which continues to spread through the economy, boosting productivity as it does. When you account for the AI effect, the 13.4% return the S&P 500 has put up over the last 12 months (versus its long-term average of 10.6% annualized) makes sense. The market is simply telling us that it’s pricing in a bit of extra juice from this new tech. So we’re going to go ahead and let the mainstream crowd fret. The truth is, the numbers don’t support the idea of a bubble right now. That’s one reason for the 9.8% discount on ASG, which sports a high-quality portfolio of US blue chips like NVIDIA (NVDA), Microsoft (MSFT) and Apple (AAPL), as well as domestic-focused midcaps like property manager FirstService (FSV) and Pennsylvania retailer Ollie’s Bargain Outlet Holdings (OLLI). ASG Drops Into the Bargain Bin  That 9.8% discount makes ASG particularly compelling when you consider that its NAV has gained 11.5% annualized over the last decade. Something else many CEF investors don’t realize is that a discount like this helps keep a fund’s dividend stable. That’s because, when you calculate ASG’s yearly payout based on NAV, not the discounted market price, you get 8.1%. This is significantly below ASG’s yield on market price and an easier figure for management to cover. That said, the point is pretty much moot when you consider that the fund’s 11.5% annualized NAV return over the last 10 years means it has been out-earning that payout for a long time. Now, we do need to bear in mind that ASG’s management ties its dividend to NAV, with the stated goal of paying 8% of NAV as dividends a year, so the payout does float around some. But given ASG’s strong NAV performance, the dividend has been pretty stable for the last three years. Steady Payouts at a Healthy Discount Source: Income Calendar But all that said, there is a question we need to ask: After three years of the discount getting steeper, should we worry it will never go back to where it used to be? To answer that, we need to look at where ASG’s total NAV return has gone in that three-year span. And it’s been nowhere but up: ASG’s Short-Term Performance: Strong  Over the last three years, ASG has delivered about a 12% total NAV return, a bit above the 11.5% it’s posted over the last decade. Over the long haul, discounts like this tend to narrow in the face of such persistent strong gains. That makes this discount a sign that ASG is ripe for buying: The market will eventually reward this strong performance (and dividend). But if we buy today, we’ll get in at a discount before that happens. |

ACTION REQUIRED: The deadline to be on the list for the next payment is February 3rd.

That’s the date you need to focus on to be eligible for your first payment on February 5th.

Fellow Investor,

Starting on February 3rd you can fundamentally transform your income stream from a string of near misses to a steady, reliable flow of income right to your bank account.

And it all starts with a simple to use, yet powerful calendar, like the one below, only with more details. Kind of like the one you might have on your desk, only this one tells you when you’ll get paid and how much you’ll receive each and every month.

No more guesswork, no more confusion, no more worrying if you did the right thing… just steady paychecks coming like clockwork.

With the monthly dividend paycheck calendar, you’ll stop worrying about the market’s ups and downs because they won’t matter anymore.

Your payday is already on the calendar.

In this urgent briefing, I’m going to share with you all of details on how the monthly dividend paycheck calendar works, how easy it is to use for investors of any level, and real life examples of the kinds of paychecks investors are getting right now.

Before I do that however, I’ll take just one minute to tell you who I am and why you should listen to what I have to say.

I’m Tim Plaehn, lead income analyst and editor of The Dividend Hunter.

I launched the Monthly Dividend Paycheck Calendar as part of my Dividend Hunter service over 10 years ago when we were in a near zero interest rate environment.

Many investors – particularly retirement focused investors – who had been told all their lives to put their money in 5% and 6% CDs and live off the interest were finding CDs at those rates no longer existed. Not even close. They were starving for yield and just as importantly, a plan.

In my previous career I’d been an F-16 fighter pilot and instructor in the United States Air Force. I’d also been a stock broker and certified financial planner. In all of those endeavors I was a meticulous planner.

So it seemed natural that I’d develop the Monthly Dividend Paycheck Calendar as part of my then newly launched Dividend Hunter. Now, 10 years later and tens of thousands of subscribers I’m still guiding our plan.

In order to receive your first paycheck on February 5th, you must be a shareholder of record by February 3rd. That means you must own the stock by this date.

This date is critical and clearly marked on the monthly dividend paycheck calendar.

The way the calendar is structured you can expect between 11 and 29 paychecks per month. By starting with the Monthly Dividend Paycheck Calendar today, you will have the opportunity to earn a growing cash income stream in perpetuity.

That’s the way the calendar is set up: you’ll have a base of 11 paychecks every month and then in some months you’ll get a bonus paycheck and in others you’ll receive two bonus paychecks all the way up to 29 per month several times a year.

The peace of mind you’ll get from knowing that every month you’re going to get at least 11 paychecks is invaluable.

No more worrying about the market’s gyrations.

No more keeping tabs on how much you’re spending and how much you’re taking in, pinching every penny along the way.

No more worry at the end of the month that you might not be able to pay all of the bills.

The income derived from the monthly dividend paycheck calendar is like getting a bonus every month.

Whether you sock it away for the future, re-invest it, or treat yourself to something nice, it’s your call. After all, it’s your money. And in this letter, I’ll tell you how to get it.

To create the Monthly Dividend Paycheck Calendar I first had to find the very best dividend investments for individual investors.

Sure, some folks out there just chase down the highest yield, buy a bunch of shares, and expect money to just flow into their account. And for some, this works. At least for a while.

But the problem is that solely chasing down yield leaves you exposed. Sadly, there are many companies out there paying eye-popping yields that are just one bad management decision or one market pull-back away from bust. They cut their dividend and the results are calamitous for investors.

You see, the share price of stocks for companies that cut dividends always crashes. And hard.

For example, in August 2024 Intel Corp. announced a suspension to its dividend payments amid a cost-cutting program. The share price fell 38% in the seven days following the announcement and has only partially recovered though it still trades at a 26% loss from before the announcement.

Plus, any investors still holding onto shares of Intel are out of luck when it comes to dividends. Ouch!

Or take Walgreens, the big drug store chain. It seems there’s a store on practically every street corner in the U.S. and they should be printing money.

Instead, Walgreens cut its dividend earlier in 2024 with an announcement just after the beginning of the new year. Until then the dividend had been 48 cents per share.

Shareholders had enjoyed well over a decade of modest but consistent dividend increases from Walgreens.

That all changed with the announcement that the next quarterly dividend payment would be a mere 25 cents per share. That’s a 48% overnight haircut for income investors relying on those dividends to help pay bills and fund retirement.

And the share price has continued to tumble during the year, coming into it at over $26 a share and now trading for $11 the last time I checked… a 73% drop in price.

Do the mental math… 48% dividend cut and a 73% share price drop, an absolute catastrophe for investors.

Investors, many of them depending on that income for retirement money, watched helplessly as their income was cut by 48% and the principal by 73%.

They were counting on that money.

Imagine for a second how devastated they were. Could your portfolio stand that big of a hit? Could your lifestyle handle an 73% cut?

That’s why it’s important to me that we select the right dividend stocks for the monthly dividend paycheck calendar. And for me the right dividend stocks are those with a history and commitment to increasing their dividend payments.

It’s not enough that a company is paying dividends. Why? Because a company without a history of increasing dividends is 9 times more likely to cut their dividends than a company that has a solid track record of raising dividends.

And you saw from just the few examples above the devastation that just one dividend cut can cause for your portfolio. Imagine a string of them in your portfolio.

Now, I spend the better part of 60 hours a week sorting through the data, the SEC filings, the analyst reports, the company releases and annual reports, listening in on company conferences calls and dialing up management on the phone when I need to… all in an effort to find that core group of consistent dividend raising companies.

Even then most won’t make the cut. But the few that do make it get consideration for the monthly dividend paycheck calendar.

And then I look for a good spread of payment dates so all the paychecks aren’t lumped into a handful of months while the rest of the year has no cash coming in.

I don’t know about you but there’s something reassuring knowing that I’ll collect checks this month and next month and again the following month and so on.

I mean think about it: your bills come every month, right? The mortgage. The electricity bill. The gas bill. The cable bill. The phone bill. So why shouldn’t your dividend income be monthly, too?

Look, everyone’s household budget operates monthly. You get each bill throughout the month and like most of us, pick one day a month to pay all the bills, whether online or via check.

And that’s how your dividend income should be, steady throughout the month.

For example, if you start by February 3rd you’ll be in a position to collect your first check on February 5th and 10 more checks all totaling $4,395 by February 27th and you can continue collecting multiple paychecks every month indefinitely.

Now is a great month to get started with the Monthly Dividend Paycheck Calendar.

If you join by February 3rd you could collect your first payment in under a week. Then you’ll be on course for an average of $3,184 a month… but in some months the payouts can be much, much more.

The true value to starting with the calendar right now is earning $3,184 on average each month in 2025, 2026, and into 2027 and so on… then watching that number increase year after year. That is, of course, only if you start today with the Monthly Dividend Paycheck Calendar.

Add that up for 12 months and you are looking at over $38,218 in extra income for the year… money you didn’t have before… money you didn’t have to lift a finger for other than picking up a few shares.

Imagine that for a second, that’s enough to pay for a new car… in cash, or plan multiple vacations, finally pay off some bills, and more… and still know there are more checks to come.

All of this extra income can be yours only if you start using the Monthly Dividend Paycheck Calendar by February 3rd.

Like I said, as long as you own these stocks you’ll have a steady and reliable income stream. The way I’ve constructed the payout dates you’ll receive at least 11 checks each month. And in some months, when you follow along with the Monthly Dividend Paycheck Calendar you’ll get 29 payments or more!

Now is a great time to get started as you could be set to collect an extra $4,395 by February 27th just for following the Monthly Dividend Paycheck Calendar strategy. And, the best part is that this income does not stop after that.

Imagine that just when you’re starting to see holiday bills show up on your credit card… you’ve collected $4,395 in extra income… to put toward holiday bills, an extra vacation, or any expense you might have been putting off.

Think about it: that’s a quick $4,395 in extra cash that you didn’t have before deposited into your account in a matter of weeks.

Each and every month, if you join the Monthly Dividend Paycheck Calendar today, you will have the opportunity to collect a growing stream of dividend paychecks just like the ones I detailed above. This level of financial freedom is an opportunity that you should not pass up.

Well, we just talked about how much you can expect over the next several weeks when you get started today and start collecting checks as early as next week. You may bring in more or less depending on how much you choose to start with. It’s entirely up to you.

My calendar tells you what to buy and when, and when to expect your paycheck.

How much those paychecks are is entirely up to you.

That flexibility and the ability to tailor the calendar to your own particular needs is one of the advantages my Monthly Dividend Paycheck Calendar gives you.

You saw from the example above, just 500 shares in each of those stocks — nets you an extra $4,395 over the next few weeks that you didn’t have before. It’s kind of like finding free money. Of course you can start with as many or as few shares as you, even if just testing out the Monthly Dividend Paycheck Calendar

Then the cycle starts all over again so you’re getting paychecks every month with this system.

Remember, you’ll be set up to easily make an average of $3,184 for each month of 2026, 2027, and into 2028 and beyond. You can use this money to pay your bills, build up your retirement savings, or begin to live a life stress-free from worries about your income.

That’s how powerful this simple yet highly effective monthly dividend paycheck calendar can be. That’s how wealth creation begins. And it’s so easy for you to get started. Regular investors are using these stocks all the time to create their own income streams specific to their own needs.

Income for January £1,669.00. Do not scale to reach a figure for the year.

Cash to re-invest £1,234.00 of which 1k to be added to UKW

© 2026 Passive Income Live

Theme by Anders Noren — Up ↑