Ian Cowie: this investment trust sector has plenty of bargains

Our columnist explains why he’s confident about the outlook for trusts tapping into a long-term trend. While the sector has seen short-term pain over the past year, he says valuations are cheap and investors can plug into above-average income yields.

by Ian Cowie from interactive investor

Wind power became Britain’s biggest source of electricity last year, according to National Grid data published by Imperial College London this week. But many investors remain frozen in the fossil fuels era. Is it time for investment trusts to help blow the warm winds of change through your portfolio?

Winter gales helped wind farms generate 32% of Britain’s electricity, compared to 31% from gas, said Iain Staffell of Imperial, who added: “Britain has become only the sixth country in the world where wind farms are the top source of electricity.”

Demand for electricity is likely to double in the next few years, according to the International Energy Agency (IEA), which should support share prices of businesses that generate this form of power. Demand is being driven by the rise of heavy new consumers including artificial intelligence (AI), data centres and electric vehicles.

The IEA predicts that a total of 1,000 terawatt hours of power (with a terawatt equalling a trillion watts) will be needed globally by 2026, compared to 430 terawatts in 2022. The spokesperson added: “This is roughly equivalent to the electricity consumption of Japan, which has a population of 125 million people.”

Closer to home, for one hour last month, Britain’s National Grid hummed happily along almost free from fossil fuels. Between 12.30pm and 1.30pm on 15 April, coal and gas power plants provided just 2.4% of the country’s electricity supply, a record low.

Across Britain, homes and businesses were running almost entirely on electricity generated by wind turbines, solar panels, nuclear reactors, biomass, plus cables from France and Norway. The UK government has pledged to create a zero-carbon electricity grid by 2035. Labour aims to reach that target by 2030.

Here and now, investment trusts that provide professionally managed exposure to renewable energy can enable individual investors to fund and benefit from these trends, generating capital growth and above average dividend income. These trusts had a hard time when energy prices were falling and interest rates were rising, making their high yields relatively less attractive, but they are now recovering.

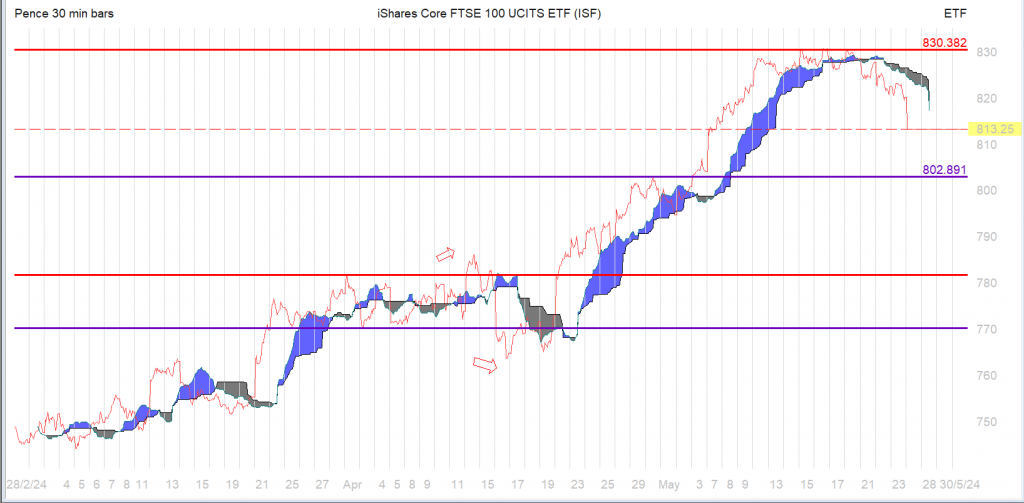

For example, Greencoat UK Wind UKW

is the top-performing fund among more than 20 rivals in the Association of Investment Companies (AIC) “Renewable Energy Infrastructure” sector. Over the last decade, five years and one-year periods, UKW’s total assets of more than £4.7 billion delivered total returns of 138%, 37% and -0.4%. It currently yields just over 7% dividend income that has risen by an annual average of 8.15% over the last five years.

It is important to beware that the past is not necessarily a guide to the future and that dividends can be cut or cancelled without notice. However, if UKW succeeds in sustaining its current rate of raising shareholders’ income in future, this would double in less than nine years.

Bluefield Solar Income Fund BSIF

a £1.4 billion fund, came second over the last decade with a total return of 94%, followed by 10% over the last five years and -17% over the last year. Disappointing recent capital returns were offset to some extent by BSIF’s high yield of 8.4% dividend income, rising by nearly 3% per annum over the last five years.

Renewables Infrastructure Grp TRIG

a £3.3 billion fund, came third over the decade with total returns of 72% followed by 8% and -11% over the medium and short term. Once again, a high yield of 7.4% rising by just over 2% per annum delivered dividend comfort to offset capital disappointment.

However, potential investors should beware so-called value traps, where the price of a high income today can be low or no capital growth in future. Alternatively, too high a yield can sometimes signify capital destruction in the past.

For example, the industrial-scale batteries specialist Gore Street Energy Storage Fund Ord GSF

yields nearly 11.5% dividend income but destroyed 31% of shareholders’ capital last year after a positive return of 9% over the last five years. As it launched in 2018, GSF lacks a 10-year track record.

Investors willing to accept lower initial income can gain more diversified exposure to rising demand for electricity. For example, Ecofin Global Utilities & Infra Ord EGL

is a £271 million fund where America is the single biggest country weighting, followed by Italy, Britain and France.

0.35% and National Grid NG.11.50%. Founded in 2016, it delivered total returns of 70% over the last five years and minus -5% over the last year. EGL’s current dividend yield of 4.3% increased by an annual average of just over 4%.

All these funds remain out of fashion and their shares are priced below their net asset values (NAVs) to reflect that fact. For example, UKW trades -10% below its NAV; BSIF has a -22% discount; TRIG is -20% and EGL is -12%.

While there is no guarantee that discounts will narrow – and they could widen – all those valuations might look like bargains if demand for electricity continues to rise, as the IEA predicts. Buyers today could enjoy capital growth and plug into above-average income yields. Or am I just whistling in the wind?

Ian Cowie is a freelance contributor and not a direct employee of interactive investor.

Ian Cowie is a shareholder in Ecofin Global Utilities and Infrastructure (EGL) and Greencoat UK Wind (UKW) as part of a globally diversified portfolio of investment trusts and other shares.