Not Soho but SOHO. Triple Point Social Housing REIT

2024 Dividend Guidance

While rent collection in the first three months of 2024 has increased relative to 2023, the Board has decided to keep the dividend target flat to preserve dividend cover whilst the Investment Manager concludes the transfer of 38 properties from Parasol to Westmoreland and proceeds with the proposed sale of a portfolio of properties (as per the Company’s Portfolio Sale and Lease Transfer announcement of 3 May 2024). As a result, the Company is targeting an aggregate dividend of 5.46 pence per Ordinary Share for the financial year ending 31 December 20241.

Dividend Declaration

The Board has declared an interim dividend in respect of the period from 1 January to 31 March 2024 of 1.365 pence per Ordinary Share, payable on or around 28 June 2024 to holders of Ordinary Shares on the register on 31 May 2024. The ex-dividend date will be 30 May 2024.

Slightly below fcast but still above market average.

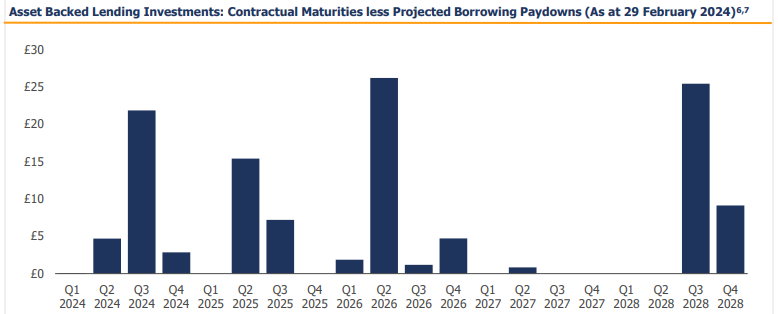

In the next 12 months over 40% of the loans will settle. The chart below is net of debt (£24m) plus about £45m of paydowns up to Q2 25. Obviously the 16.84% dividend will reduce but it’s likely to continue for another 4 periods at 2p a quarter – so an 8p a share return. After that (Q3 2025) it probably drops to 1p a quarter for another year and after Q3 2026 perhaps drops to 0.5p a quarter until the end of 2028.

If that’s the case then that’s 16p of dividends over 4 years. In 12 months time alone deducting 8p from today’s 48p buy price is equivalent to buying at a discount to NAV of 45.8%

Conclusion

Recency bias feels a good way to understand the discount here. It’s been bad for two years so 2024 must be bad too. Holdings in wind down must equate to a fire sale.

But there’s already been positive news in 2024 and there’s so much bad news already built in to the price – it would take a spectacular 1929 style crash to achieve what the market is assuming and ignoring that the US and UK are doing nicely thank you – on Bloomberg this morning “Maybe we are experiencing normal for longer” was an interesting comment. The nature of VSL’s assets are that they continue to generate strong returns over their contractual period of about four years, albeit returns fall as capital is returned.

Meanwhile because the liquidation of assets is reasonably near term that in the next 12 months it’s likely that there’ll be a 10p-15p capital return and 8p dividend. So potentially 50% of today’s share price.

A final thought is VSL is the sort of share which Simon Thompson of the Investor’s Chronicle likes to spot. VSL is like another Urban Exposure which was one of the ideas he advocated I believe in this article from 2021, or I believe he spoke of Amadeo earlier this week. VSL will reduce costs and probably delist at some point to save money, after which returns then get paid into your SIPP or ISA as cash – they did for me with Urban Exposure.

On 15 May 2024, Close Brothers Asset Management sold 540,155 shares in SUPERMARKET INCOME REIT PLC ORD 1P. This brought our shareholding to 4.99% of the shares in issue. This is based on the shares in issue figure of 1,246,236,185 as at 15 May 2024. This is the required notification that the holding has crossed below 5% of the shares in issue.

Best and worst performing London-listed funds in April – QuotedData

(Alliance News) – China- and commodity-focused investment funds were among the star performers in April, according to the monthly winners and losers list from QuotedData, published on Wednesday.

A surging gold price last month helped Golden Prospect Precious Metals Ltd shine brightest, while Chelverton UK Dividend Trust PLC also impressed, shaking off a hot UK inflation reading. The investor backs “mid to small-cap companies exclusively outside the FTSE 100”.

Data from the Office for National Statistics last month had shown that consumer price inflation ebbed to 3.2% in March, from 3.4% in February. This was more inflation than the 3.1% expected, however.

“It was somewhat surprising to see the rate sensitive UK Smaller Companies sector rally on the back of April’s inflation data, which came in slightly hotter than expected, although dovish commentary from the Bank of England helped boost sentiment. Importantly, inflation continues to trend downward toward the 2% target,” QuotedData said.

“Chinese shares lead the list of best performers in April, although they remain deeply depressed with the world’s second largest economy still struggling with a range of long-standing structural issues.”

Hipgnosis Songs Fund, which has had a tumultuous time of late, saw a share price surge on takeover interest. Last month, the music royalty investment company agreed to a USD1.40 billion cash takeover from Alchemy Copyrights, which trades as Concord. Later in April, it backed a rival bid from Blackstone Inc worth USD1.50 billion.

The saga did not end there. Concord then upped its bid to USD1.51 billion, before the bidding war reached a crescendo, with Blackstone offering USD1.57 billion. Concord decided against sweetening its bid and said earlier this month that its offer was final.

The following were the best and worst performing London-listed investment companies in April, excluding trusts with market capitalisations below GBP15 million:

Five best performing funds in NAV terms with % change:

Golden Prospect Precious Metals 15.4

Rockwood Strategic PLC 12.8

JPMorgan China Growth & Income PLC 10.5

abrdn New India Investment Trust PLC 8.7

Chelverton UK Dividend Trust 8.5

Five worst performing funds in NAV terms with % change:

Bellevue Healthcare Trust PLC (9.7)

Baillie Gifford Shin Nippon PLC (8.5)

International Biotechnology Trust PLC (7.9)

Vietnam Enterprise Investments Ltd (7.4)

Martin Currie Global Portfolio Trust PLC (6.8)

Five best performing funds in price terms with % change:

Hipgnosis Songs Fund 50.7

Gresham House Energy Storage Fund PLC 36.4

Macau Property Opportunities Fund Ltd 32.1

Seraphim Space Investment Trust PLC 23.2

EPE Special Opportunities Ltd 19.3

Five worst performing funds in price terms with % change:

Asian Energy Impact Trust PLC (15.9)

Schroder British Opportunities Trust PLC (10.7)

Bellevue Healthcare Trust (9.3)

Gulf Investment Fund PLC (8.9)

Custodian Property Income REIT PLC (8.8)

Source: QuotedData. Full details at http://www.quoteddata.com

Despite receiving zero passive income, I reckon these are the happiest shareholders on earth.

Story by James Beard

Receiving passive income makes me happy. Getting money for doing nothing lets me buy more shares, hopefully increasing the level of dividends I receive the next time a payout’s due.

The Oracle of Omaha

But there’s a group of people I believe are happier than both me and the Finns. They’re shareholders in Berkshire Hathaway, billionaire investor Warren Buffett’s investment company.

Between 1964 and 2023, the company’s share price grew by 4,384,748%. During the same period, the S&P 500 increased by ‘only’ 31,223%.

And as usual, during the first week of May, it held its annual meeting in Omaha. With shuttle buses organised from local hotels, a $6 BBQ Meal Deal and the opportunity to buy exclusive rings, watches and fine gifts, I reckon there was a holiday-like atmosphere about the place.

And it’s no wonder. With one ‘A’ share costing over $600,000, the ‘typical’ shareholder is probably wealthier than most Americans.

And yet the company’s never paid a dividend.

That’s why I reckon they are such a happy bunch, particularly those from Finland!

By contrast, my portfolio’s stuffed with high-yielding shares generating good levels of passive income. And most of them are members of the FTSE 100.

My current favourite is Legal & General (LSE:LGEN).

Personal experience

Based on its 2023 dividend, it’s currently yielding 8.1%. And as the chart below shows, it has a long track record of steadily increasing its return to shareholders.

Of course, dividends are never guaranteed. But I’m hoping for future increases as the company has ambitious growth plans.

Legal & General also has a strong balance sheet. At 31 December 2023, its Solvency II ratio was 224%. This needs to be above 100% to meet its regulatory requirements.

However, its 2023 results were disappointing. They were lower than analysts’ consensus forecasts. And its investment management division saw a £154m (11.7%) fall in the average value of assets under management during the year.

Also, the business as a whole is sensitive to the wider economy. Any sign that growth is stuttering, particularly in the UK and US, and investors are likely to become nervous.

But I’m encouraged by the company’s plans to acquire £8bn-£10bn of new pension schemes each year. And if Legal & General continues to grow its dividend — and I receive the levels of passive income I’m expecting — I’ll be a happy man.

The post Despite receiving zero passive income, I reckon these are the happiest shareholders on earth! appeared first on The Motley Fool UK.

Anyone who bought in 2020 and never had a stop loss or stop gain policy would be nursing a sizeable loss today.

But anyone who had a stop loss or stop gain policy and bought recently would be in profit by around 20% plus.

If u don’t have a very strong stop loss or stop gain policy it may be best to stick to dividend shares and compound the dividends. The choice my friend is yours.

But becoming one does not just happen overnight – it takes time and patience.

The level of contributions, as well as the investments you decide to place inside an Isa and how they perform, are the main drivers that will determine whether you can one day reach the £1m savings milestone.

Here, Telegraph Money explains how you can do it.

Work out the returns you must achieve

To get to a million pounds, investors will need to max out their Isa each year and for investments to provide a certain level of returns.

Someone who put the full allowance in their Isa each year since their launch in 1999 and who earned a steady 5pc return a year would have built up a pot of just over £484,000 – not even halfway to reaching the £1m mark.

To reach £1m an investor would have needed to have invested the full Isa allowance each year and to have earned 11pc each year since.

If you include going all the way back to Peps – the precursor to Isas – you would have needed annual returns of 6.5pc.

Investing over the long term has paid off for many who started when Peps were introduced in 1986. The age of customers who have grown their Isa pots to £1m plus is around 73, according to data from stock brokers.

At brokers AJ Bell, the youngest Isa millionaire is just 35.

The investments millionaires have used

Listed investment funds have powered Isa millionaire portfolios at Interactive Investor, and account for the largest share of Isa portfolios: 42.5pc compared to just 8.2pc for unlisted funds.

Alliance Trust and Scottish Mortgage are two of the most common investment trust stocks found in the average Isa millionaire top 10 holdings.

They can borrow money to invest extra than that provided by their investors to boost performance in an upturn. Many also have great track records for paying dividends. The downside is theycan be expensive to trade, with many brokers charging flat fees for the purchase of shares, while units in unlisted funds can be purchased for a negligible fee.

Many investors have had success from unlisted funds, however. Popular funds among Isa millionaires include Rathbone Global Opportunities, Lindsell Train Global Equity, Fundsmith Equity and Fidelity Special Situations. They have also cashed in on rising share prices and dividends from individual stocks.

FTSE blue chips are widely held in Isa millionaire accounts. They include Shell and BP; Lloyds Banking Group and Aviva; Diageo and Rio Tinto.

“Isa millionaires only have an average of 5pc cash in their portfolios compared to 10pc across all Isa accounts, so they are putting more of their money to work,” says Dzmitry Lipski, head of funds research at Interactive Investor. “Long term this can help avoid cash drag,” he adds.

The fastest way to get to £1m

To get to £1m as quickly as possible, the first step is to invest the maximum each year.

It is arguably easier to become an Isa millionaire today, with a £20,000 a year allowance for savers (assuming you can afford to put away the maximum), compared to older investors who started out when Isas launched in 1999 with a £7,000 limit.

If you started saving today and the Isa limit remained at £20,000, it would take you 25 years to become an Isa millionaire, assuming an average annual return of 5pc.

The next key part of your strategy could be to invest early in the tax year. It means you will have up to an additional year in the market, which will also help power portfolios in a rising market, as more of your assets are invested for longer.

When it comes to selecting investments you’ll need a diverse, balanced mix according to your risk appetite. However, you may wish to consider listed funds which have been a good bet for many over the years.

A total of 28 investment companies would have made investors more than £1m if they had invested the full annual Isa allowance in the same company each year, according to research from the Association of Investment Companies, a trade body.

Investing the full Isa allowance each year from 1999 to 2023 – a total of £286,560 – and reinvesting the dividends into one of the five investment companies below would have generated a tax-free pot of over £1.4 million at the end of February.

These top five performing funds are: HgCapital, Pacific Horizon, Scottish Mortgage, Allianz Technology and abrdn Asia Focus. Among the common investment themes in these listed funds are technology and smaller companies.

While these figures are compelling, it is not advised to have all your money in one investment or one investment type.

The average Isa millionaire portfolio includes 28 holdings, according to AJ Bell.

Laura Suter, head of personal finance at the firm, says: “Focus on steady climbers that will gradually increase your wealth over time, rather than putting all your money in higher risk investments that could drop significantly, or at least give you a much more hair-raising ride on the way.

“Make sure you’re sticking to a risk level you’re comfortable with and that your portfolio is well diversified. Betting on a few stocks rising in value could be a recipe for disaster if the sector nosedives or the company hits some trouble.

“Lots of those who make it to millionaire status will invest directly in stocks, rather than entirely in funds. But you should only take this route if you know that you have the time and inclination to research and monitor the stocks regularly.”

Experts insist that getting rich slowly is a smart strategy.

Sarah Coles, head of personal finance at Hargreaves Lansdown, says: “Isa investors don’t take enormous risks.

“Their focus is to consistently invest as much as possible of their annual allowance, as early as possible in the tax year, in a diverse and balanced portfolio. And they’ve done this every year for decades.”

Why long-term investing works

Investing over a long period is a tried and tested strategy.

The sooner you start saving the more you can put aside, and early contributions are the most valuable because they have the longest to grow.

Compounding will also boost returns. In simple terms, your money earns a return in the first year and both the original cash and the return benefit from any growth in the second year. In the third year your investment is further enhanced by any returns achieved. This snowball effect is known as compounding.

Even when starting with zero savings, investing a modest sum of cash each day can potentially unlock a substantial passive income in the long run. Putting aside as little as £7 a day can be transformative to an investor’s wealth given sufficient time. Here’s how.

Saving little and often

Investing this money into top-notch dividend shares could instantly start generating a passive income overnight. But how much can investors realistically expect? This ultimately depends on the yield they manage to secure.

For index investors focusing on the FTSE 100, the average dividend payout by the UK’s flagship index is around 4%. Therefore, every £200 investment is roughly equal to an extra £8 in annual passive income. Of course, for stock pickers, this figure can be bolstered by being more selective. Building a portfolio yielding closer to 6% pushes this income to £12 – a 50% increase.

After a year of investing £200 a month at this rate, the income from a brand-new portfolio would be £144. Obviously, that’s not life-changing. But given time to compound, this can start to add up. After a decade, the income stream would grow to just under £2,000 – and even that might be conservative since it doesn’t include the extra returns generated from capital gains or future dividend hikes.

Of course, share prices don’t always go up. And a poorly constructed portfolio can easily end up backfiring. So, how can investors find the best income stocks to buy?

Picking the right shares

Stock picking is a complex process with countless aspects that investors have to consider. However, there are a few known shortcuts, especially for dividend shares. When hunting for companies that can systematically increase their shareholder payouts, investors could spend time analysing free cash flow, or they could just jump straight to the list of dividend aristocrats .

Does that make it the perfect solution for building a passive income? Not necessarily.

As with any investment, proper due diligence is required. And while it’s true that National Grid has raised dividends for more than a quarter of a century, the average annual growth rate has only been a modest 3.4%. Even in a normalised inflationary environment, the level of wealth created in real terms is pretty minimal. In other words, while the dividends may be “safe”, they may be a poor fit for an individual looking to build wealth.

However, that’s not always the case. Several Dividend Aristocrats have been growing payouts at a far more meaningful pace, some even in double-digit territory. And these could be the key to turning a £7 daily investment into a five-figure passive income for life.

City of London Investment Trust currently pays a yield of 4.85%, so is not in the current blog portfolio. If anyone wants to receive a ‘secure’ dividend it could be paired with a higher yielder to provide a higher level of security and retain a blended yield of 7%. CTY should be in your watch list for when the next market crash occurs.

CTY has an unmatched record of delivering consecutive years of dividend growth, now having reached 57 years. This is the longest continuous period of any investment trust and means CTY is top of the AIC’s ‘Dividend Heroes’ list. This is not to say that underlying earnings have increased each and every year.

Investment trusts have the ability to retain up to 15% of each year’s income in reserve and use this reserve in future years to smooth dividends if revenues subsequently fall. One such year was 2020, with many portfolio holdings cutting or passing on dividend payments in the face of the economic shock brought on by the COVID-19 pandemic. CTY was able to continue to pay an ever-increased level of dividends through the crisis, allowing earnings to catch back up again with the dividend by 2022 when the dividend was once again covered. CTY’s dividend was marginally covered in 2023. Total revenues over the first half of the current financial year, which ends in June 2024 were up, but earnings per share only increased marginally thanks to the short-term dilutive effect of share issuance so far this year. We understand that income generation is in any event biased towards the second half of CTY’s financial year, when many of the big income stocks pay their final dividends. The board has stated that it is confident that it will be able to continue to increase the annual dividend this year.