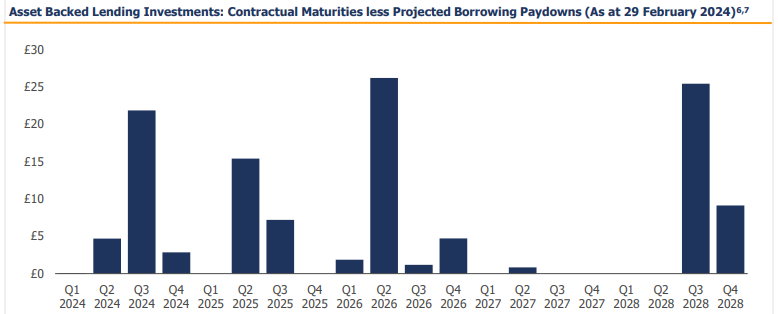

In the next 12 months over 40% of the loans will settle. The chart below is net of debt (£24m) plus about £45m of paydowns up to Q2 25. Obviously the 16.84% dividend will reduce but it’s likely to continue for another 4 periods at 2p a quarter – so an 8p a share return. After that (Q3 2025) it probably drops to 1p a quarter for another year and after Q3 2026 perhaps drops to 0.5p a quarter until the end of 2028.

If that’s the case then that’s 16p of dividends over 4 years. In 12 months time alone deducting 8p from today’s 48p buy price is equivalent to buying at a discount to NAV of 45.8%

Conclusion

Recency bias feels a good way to understand the discount here. It’s been bad for two years so 2024 must be bad too. Holdings in wind down must equate to a fire sale.

But there’s already been positive news in 2024 and there’s so much bad news already built in to the price – it would take a spectacular 1929 style crash to achieve what the market is assuming and ignoring that the US and UK are doing nicely thank you – on Bloomberg this morning “Maybe we are experiencing normal for longer” was an interesting comment. The nature of VSL’s assets are that they continue to generate strong returns over their contractual period of about four years, albeit returns fall as capital is returned.

Meanwhile because the liquidation of assets is reasonably near term that in the next 12 months it’s likely that there’ll be a 10p-15p capital return and 8p dividend. So potentially 50% of today’s share price.

A final thought is VSL is the sort of share which Simon Thompson of the Investor’s Chronicle likes to spot. VSL is like another Urban Exposure which was one of the ideas he advocated I believe in this article from 2021, or I believe he spoke of Amadeo earlier this week. VSL will reduce costs and probably delist at some point to save money, after which returns then get paid into your SIPP or ISA as cash – they did for me with Urban Exposure.

Regards

The Oak Bloke.

https://theoakbloke.substack.com/p/vsl-state

£££££££££££

At the higher end of the risk spectrum but a strong hold as we await news.

Leave a Reply