Investment Trust Dividends

The number of investment companies trading at a 52-week high has fallen for the fifth week in a row. With just eight funds making it into the latest Discount Watch.

ByFrank Buhagiar•07 May

We estimate there to be eight investment companies which saw their discounts hit 52-week highs over the course of the week ended Friday 03 May 2024 – two less than the previous week’s 10.

The number of 52-week high discounters has now fallen for five weeks in a row. Just eight funds make it on to the list this time round compared to 10 previously.

What’s behind the ever-diminishing list of names, particularly as a high degree of uncertainty remains over the timing and depth of any interest rate cuts this year? Could it be that investment company discounts are seasonal?

For the last two years, the weekly number of 52-week high discounters has followed a very similar pattern. Only two years of data, true, but could there be something that causes a significant drop off in year-high discounters around end of March/beginning of April? Well, there just might be.

The top-five discounters

FundDiscountSectorGround Rents Inc GRIO-70.08%Property

Gore Street Energy Storage GSF-45.70%Renewables

VPC Specialty Lending Inv VSL-39.62%Debt

New Star Investment NSI-39.20%Flexible

Downing Renewables & Infrastructure DORE-38.09%Renewables

The full list

FundDiscountSectorVPC Specialty Lending Inv VSL-39.62%Debt

Impax Environmental IEM-12.32%Environmental

Jupiter Green JGC-32.83%Environmental

New Star Investment NSI-39.20%Flexible

Schroder British Opps SBO-35.78%Growth Capital

Ground Rents Inc GRIO-70.08%Property

Gore Street Energy Storage GSF-45.70%Renewables

Downing Renewables & Infrastructure DORE-38.09%Renewables

Hipgnoisis Songs continues to play a merry tune and Gresham House Energy Storage keep the party going. Both find themselves occupying the top spots on Winterflood’s list of monthly movers in the investment company space. Which other funds are performing well and what’s the update on Scottish Mortgage?

ByFrank Buhagiar•07 May

The Top Five

Hipgnosis Songs (SONG) still holding onto top spot on Winterflood’s list of monthly movers in the investment company space. The shares’ +54.3% gain on the month, a little below the previous week’s +67.1%_ but still comfortably ahead of the rest of the pack. Week ended Friday 26 April 2024, Concord Chorus’ announcement that it had upped its cash offer to US$1.25 a share stole the headlines. Just days later on 29 April and Blackstone Europe trumped Chorus with a US$1.3 (104p) bid of its own. What will Concord do next?

Gresham House Energy Storage (GRID) held onto second place as the shares extended their monthly gain to +34.7% compared to +22.5% previously. Shares still benefiting from a flurry of positive updates, including one on 24 April which highlighted a meaningful improvement in revenues. GRID clearly on a run in terms of press releases – the full-year results were subsequently put out on 29 April. Be interesting to see if the company has another update up its sleeve for the week ahead.

Seraphim Space (SSIT) jumps one place to third and at the same time increases its monthly gain to +24.2% from +16.3%. The space investor followed up its well-received sale of early-stage portfolio companies announcement on 22 April 2024 with its regular monthly newsletter. Enough in there to keep the momentum going it seems.

Regional REIT (RGL) still in the top five but drops from third to fourth and that’s despite increasing its gain on the month to +24.2% from +20.5%. Last week, Weekly Gainers highlighted how RGL was in need of a positive trading update of its own to stay in Winterflood’s top five. Lo and behold, the office landlord announced a positive letting update on 1 May.

Schiehallion (MNTN) completes the top five with a +19.1% monthly gain. The growth capital investor has been something of a regular on the Winterflood list this year. That’s largely down to its ongoing share buyback programme. Right on cue, the fund announced another share repurchase on 30 April.

Scottish Mortgage

Scottish Mortgage’s (SMT) share price made up lost ground over the course of the week ended Friday 03 May 2024 – shares finished the week up +0.5% on the month, having been down -5.7% previously. NAV followed suit – up +0.3% compared to -3.8%. As did the wider global investment trust sector which ended the week up +1.1%, seven days earlier it had been off -1.4%. The combination of the Nasdaq rising during the week and SMT’s ongoing share buyback programme, enough to push the shares into positive territory for the month.

The Results Round-Up – The Week’s Investment Trust Results

Which fund would have turned a £1,000 investment made on 31 January 2019 into £1,698 today? And which fund has either met or beaten its annual target return of 8-10% for 10 years in a row?

By

Frank Buhagiar

Doceo

3i Infrastructure (3IN) hits the target again

3IN clocked up an +11.4% NAV total return for the year which, according to Chair Richard Laing, means the infrastructure investor has now either met or beaten its annual target return of 8-10% for 10 years in a row. Laing describes the year as “another year of outperformance from our unique portfolio.” What’s unique is the fund’s underlying businesses being aligned with long-term megatrends. The full-year report lists a number of these including renewable energy, electrification, automation/digital operations, demand for healthcare, smart cities and urbanisation. And because of the exposure to these megatrends, the portfolio managers believe the fund can continue to deliver across the economic cycle. A fund for all seasons.

Investec: “The portfolio continues to perform strongly and we think the company remains well-placed to provide investors with a respectable yield and attractive total returns. We reiterate our Buy recommendation.”

Liberum: “We continue to view 3IN as one of the best-placed funds to deliver attractive NAV returns in a capital-constrained environment due to its active management of Core-plus companies”.

JPMorgan: “A headline discount of around 8%, which although narrow relative to peers is justified in our view by higher net returns given active management, relatively low financing costs, a materially higher discount rate than most peers and a proven ability to capture uplifts on exit. We thus see no reason to change our Overweight recommendation.”

Jefferies: “The portfolio’s underlying earnings growth and the potential for realisations continue to position it well going forward.”

Numis: “We would add to holdings for exposure to a well themed portfolio and strong management team.”

ICG Enterprise Trust (ICGT) refreshes the parts other funds can’t reach

ICGT reported a +2.1% NAV per share total return for the year. According to Chair Jane Tufnell, that brings the annualised NAV per share total return generated over the last five years to +14.6% and an annualised Share Price Total Return of +11.2%. In hard cash terms, £1,000 invested in the private equity investor on 31 January 2019 would now be worth around £1,698 (assuming reinvestment of dividends). Portfolio manager Oliver Gardey, puts the positive performance down to the fund’s focus on investing in companies with defensive growth qualities.

Looking ahead, the Tufnell believes ICGT is more relevant than ever. That’s because private ownership of companies is expected to keep on growing in the years ahead, which is handy as ICGT’s purpose is “to make the private available to the public”. As Tufnell writes, “we enable you to invest in parts of the economy that you cannot directly access through public markets.” Anyone else reminded of that famous 20th century advertising campaign for a Dutch beer beginning with the letter H?

Numis :“We believe ICG Enterprise’s NAV is a good result in a difficult market backdrop”.

Jefferies: “The introduction of a supplemental share buyback programme highlights the current wide discount in absolute terms and versus peers.”

JPMorgan: “A key part of private equity investment company disclosure is measures of average EBITDA growth, valuations and debt levels. ICGT has listened to market feedback and increased the size of the sample of companies it covers such that it now represents circa two-thirds of the total up from circa one-third previously. In our view this makes the numbers more representative and is a very welcome change. We are Overweight.”

International Biotechnology’s (IBT) ‘quoteds’ steal the show

IBT comfortably outperformed over the latest half year courtesy of an +11.2% NAV total return per share – the Reference Index could ‘only’ manage an +8.2% gain. The star of the show was the fund’s quoted portfolio which generated a +13.1% NAV per share total return – the unquoteds put in a more in line +7.9%. A thumbs up then for the investment strategy which looks to identify companies with innovative technologies, robust intellectual property and strong growth potential.

And the portfolio managers think the combination of reasonable valuations, the increasing pace of innovation, the improved competitiveness of companies and the relatively high number of new drugs being approved all bode well for biotech in 2024. A case of more of the same then?

Numis: “The long-term track record remains strong, with the fund outperforming the index over five and ten years and we believe that the fund, through its risk-aware approach, is well placed to continue this outperformance over the long term. IBT’s shares currently trade on a c.10% discount to NAV, which we believe offers an attractive entry point.”

3i Group’s (III) positive Action

III’s total return for the year ended 31 March 2024 came in at +23%. Chief performance driver once again was European discount retailer Action, which posted a +33% gross investment return. In his comment, CEO Simon Burrows, puts the strong performance down to investment decisions taken over a decade ago. One of these was Action in which 3i first invested back in 2011. Today, it owns 54.8% of the fastest growing non-food discount retailer in Europe and our largest portfolio company according to 3i.

Just how fast is Action growing? Net sales were up 28% to €11,324 million while operating EBITDA grew 34% to €1,615 million in 2023. And 3i has no plans to get rid of its stake any time soon. As Burrows writes in his full-year review “We have been clear for some time that we are going to hold Action for the long term, enabling us to benefit from its compounding growth and returns.” Can’t put it any clearer than that.

JPMorgan: “Overall, this is a strong set of numbers, though the premium to NAV has run up strongly ahead of the results to ~38% (LT average 15%), and we would not be surprised to see this contract at some point. But we have high conviction that the RoE (Return on Equity) over next two years will comfortably exceed 20% and, thus, prospective total returns still remain attractive. We remain Overweight.”

Liberum: “Overall, this is a mixed set of results, in our view, with Action’s performance holding up very well given the circumstances, but the company generally experiencing a sharper slowdown in growth and profits than expected. We wouldn’t be surprised to see some profit taking in the shares, any weakness in the share price should be short-lived and considered an opportunity to add stocks to a portfolio”.

North Atlantic Smaller Companies (NAS) keeps its powder dry

NAS posted a +3% NAV per share return for the full year, some way off the S&P’s +15.2% (in sterling terms), but comfortably ahead of the Russell 2000’s -2.3% (in sterling terms). One reason for the relatively stable performance is what Chairman Sir Charles Wake describes as NAS’ “conservative investment strategy” – as at end of January the fund held £70 million, or more than 10% of the market cap, in cash and US treasury bills. That means the investment managers have plenty of funds to hand to take advantage of any attractive opportunities they come across.

Winterflood: “Share price -5.4%, as discount widened to 28.0% from 23.5%. Repurchased 140k shares. Portfolio comprised 8.3% US exposure, 81.8% UK exposure and 9.9% US Treasuries.”

For any new readers the rules are. There only 2.

Buy Investment Trusts that pay a dividend to buy more Investment Trusts that pay a dividend.

If any Trust that drastically alters its dividend policy, it must be sold, even at a loss.

The current buying yield is 7% minimum, as dividends compounded over ten years doubles your income thru thick and thin and there will be plenty of thin.

Yield versus Price

If u buy a Trust at 100p yielding 10% a dividend of 10p.

If the the trust doubles in price doubles and the dividend is still 10p, the yield is now 5%.

In the future when one of your Trusts doubles in price, u can either.

Sell half and re-invest in another higher yielder, an option if the dividend has increased over the holding period, or sell all the position and try to do it all over again, all depending on the yields in the market at the time

As stock markets surge ahead, shares become more expensive and dividend yields decrease. But columnist Robert Stephens argues that the index is still undervalued and income investors can still obtain a very generous dividend yield.

by Robert Stephens from interactive investor

The FTSE 100’s surge to an all-time high may naturally prompt some income investors to question the appeal of large-cap shares. After all, the index’s rise means dividend yields will inevitably have been squeezed and market valuations will have expanded. This could equate to lower returns in future.

However, the index’s new record needs to be put into context, with its performance having been hugely disappointing from a share price perspective (excluding dividends) for the past 25 years. While the S&P 500 index has gained 256% since the turn of the century, the FTSE 100 index has risen by a paltry 20%. This equates to an annualised capital gain of just 0.8%. Although this figure does not include the impact of reinvested dividends, and therefore does not paint a full picture of the index’s true investment performance over recent years, it nevertheless highlights that many of its holdings are unlikely to be overvalued.

Indeed, the FTSE 100 index currently yields around 3.6%, even after surging by 13% over the past six months. By comparison, the S&P 500 index yields just 1.4%. This suggests that rather than now being ‘overvalued’, the FTSE 100 index’s constituents are more likely to have moved from being “grossly undervalued” to just plain “undervalued”. As such, income investors can still obtain a very generous dividend yield, both on a stand alone basis as well as relative to other stock market indices and asset classes, alongside income growth and further capital gains.

Source: Refinitiv as at 9 May 2024. Bond yields are distribution yields of selected Royal London active bond funds (end March 2024), except global infrastructure bond which is 12-month trailing yield for iShares Global Infras ETF USD Dist as at 7 May. SONIA reflects the average of interest rates that banks pay to borrow sterling overnight from each other (3 May). *Data prior to May is based on 3-month GBP LIBOR. Best accounts by moneyfactscompare.co.uk refer to Annual Equivalent Rate (AER) as at 8 May.

An improving economic outlook is a key reason for the FTSE 100 index’s recent rally. Investors are looking ahead to a continued fall in inflation that will ultimately allow central banks to cut interest rates from their current multi-decade highs. While this process is arguably not progressing as quickly as many investors had hoped for, with inflation having been stickier than expected, it is nevertheless widely forecast to continue falling in the coming months.

Lower inflation that brings an end to the cost-of-living crisis and falling interest rates that encourage spending instead of saving among consumers, are likely to prompt improved operating conditions for FTSE 100 companies. This should equate to higher profits that allow them to increase dividends. Indeed, shareholder payouts are likely to rise at a significantly faster rate than inflation as the pace of price rises becomes far more in keeping with its historical average than has been the case over recent years

Monetary policy which becomes more accommodative in response to falling inflation is also likely to persuade investors to become less risk averse. It should prompt a much improved rate of economic growth that raises demand among investors for riskier assets such as equities. This could provide further capital gains for investors in FTSE 100 stocks, with the index having the potential to reach new highs alongside the provision of a generous and rising income in the years ahead.

With the FTSE 100 being a globally focused index due to over 75% of its members’ sales being generated from outside the UK, it offers a significant amount of geographic diversification that equates to reduced risk for investors. The index’s constituents should also benefit from central banks in the US and the eurozone being in a very similar position to their UK counterpart, in terms of inflation falling and interest rate cuts being on the near-term horizon.

Furthermore, the index contains a wide range of high-quality companies that have well-covered dividends, solid competitive positions and sound balance sheets. Their size and scale means they are less risky than smaller peers, while their low valuations mean they offer wide margins of safety.

Having been overlooked for over two decades, FTSE 100 stocks offer excellent value for money in many cases and still represent a significant long-term buying opportunity for income-seeking investors.

Robert Stephens is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only.

NatWest retail share offer latest

There is speculation in the press that Jeremy Hunt is putting together the final pieces of a plan to offer the public a chance to buy shares in the high street lender.

by Graeme Evans from interactive investor

Sky News also said the proposed public offer is likely to have a £10,000 cap on applications and a £250 minimum investment to encourage wider participation.

NatWest shares, which were 204p in the hours after Hunt’s surprise announcement, traded as high as 317.9p this afternoon, a six-year best, as sentiment continues to improve across the banking sector.

TradingView. Past performance is not a guide to future performance.

A record high for the FTSE 100 index has also created a favourable backdrop for the sale as the government looks to fulfil its commitment for a full exit of its NatWest stake by 2025-26.

The 84% position taken after the 2008 rescue of Royal Bank of Scotland was down to 37% by the start of this year, falling to 27% or a total of £7.2 billion by the end of April.

UBS notes that the current level of open market share sales combined with NatWest buybacks could reduce the Treasury position to 21-22% by the month end.

The City bank said: “If the Treasury continues selling in the open market at current rates the shareholding would be roughly 17% by mid July, worth £4.6 billion at today’s price.”

To get to a 10% residual stake would require a 7% sale of stock worth £1.9 billion, less than the two institutional placings worth £2 billion and £2.5 billion in 2015 and 2018 respectively.

Sky News said an announcement on the launch of the public offer could come late May or in early June, subject to market and political conditions.

It revealed that ministers have been exploring plans that could award one bonus share for every 10 bought by retail investors and held for at least a year.

The proposed ceiling of £10,000 would mirror a previous Treasury plan – subsequently abandoned in 2015 – for a retail offering of Lloyds Banking Group

NatWest recently posted robust first-quarter results, including the return to positive trends in its net interest margin alongside profits 5% ahead of City forecasts at £1.3 billion.

Broker Peel Hunt, which has a 330p target price, views NatWest independence as important for the rating of the shares.

The broker said recently: “The end of directed buybacks would mean that share repurchase programmes would have a greater market impact.”

In addition, the desire to remove the government as a shareholder has meant a bias towards buybacks. “Although we expect significant share repurchases to remain a core part of the investment case for NatWest, capital deployment decisions could evolve more in favour of growth capital initiatives in the future.”

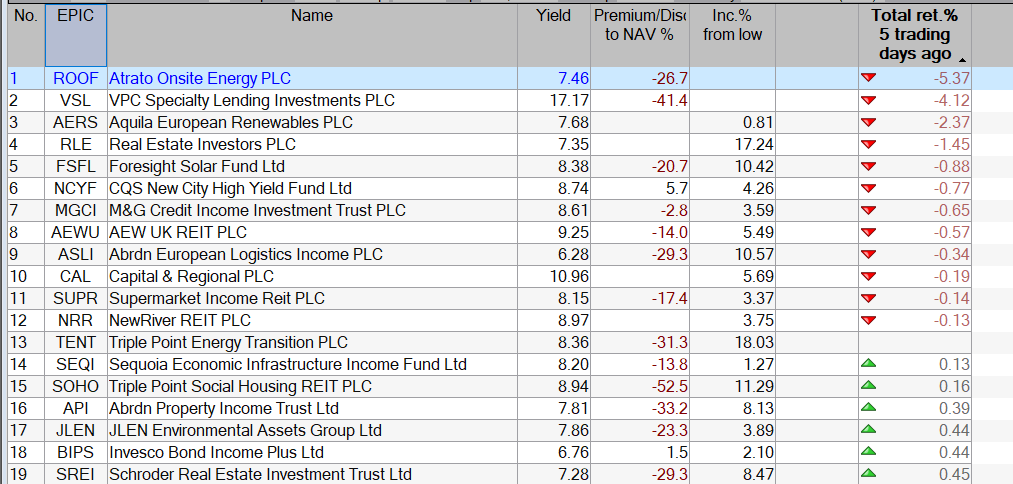

Investing has become more perilous as Trusts move away from their lows.

© 2026 Passive Income Live

Theme by Anders Noren — Up ↑