Thursday 9 April

Athelney Trust PLC ex-dividend date

BlackRock Smaller Cos Trust PLC ex-dividend date

CT Private Equity Trust PLC ex-dividend date

CT UK High Income Trust PLC ex-dividend date

F&C Investment Trust PLC ex-dividend date

JPMorgan China Growth & Income PLC ex-dividend date

JPMorgan Emerging Markets Investment Trust PLC ex-dividend date

Lowland Investment Co PLC ex-dividend date

Manchester & London Investment Trust PLC ex-dividend date

Mercantile Investment Trust PLC ex-dividend date

Murray International Trust PLC ex-dividend date

Schroder Asian Total Return Investment Co PLC ex-dividend date

Schroder European Real Estate Investment Trust PLC ex-dividend date

Author: admin (Page 3 of 384)

£20,000 in savings? Here’s how it could realistically be used to target £633 of passive income each month

Starting with the standard annual ISA allowance of £20k today, how much passive income could someone really aim for over the long term ?

Posted by Christopher Ruane

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Do you currently have a practical plan to try and earn hundreds of pounds in passive income each month? Some people do, but many do not. Passive income ideas can often seem quite esoteric, making the whole idea of earning money without working for it sound a bit pie in the sky.

But in reality, there are plenty of such ideas that are firmly grounded in reality. One is investing into companies that will hopefully pay their shareholders dividends.

Here I explain how, by doing that today with £20k, someone could target hundreds of pounds in passive income each month in the future.

Why time can be an investor’s friend

When I say future, in this example I am presuming a 25-year timeframe before the income starts flowing. It would be possible to get it sooner – indeed, as soon as this year – but at a lower level.

Why wait? The shares will hopefully pay dividends but rather than take them as passive income straight away, they can be reinvested. This is known as compounding and can be a powerful force multiplier when it comes to investing. Basically, dividends in turn start to earn dividends. That is because they can fund the purchase of more shares.

Over the course of time that can all add up substantially. Compounding £20k for the 25 years I mentioned at 7% annually, it would grow by over five times, to a size big enough that a 7% dividend would equal £633 of monthly dividends.

Focusing on quality, with an eye on costs

Is a 7% yield realistic? After all, that is over twice the current yield of the FTSE 100 index of blue-chip shares. I do think it is realistic, even while sticking to high-quality shares.

Of course, some shares can disappoint and no dividend is ever guaranteed to last, so it makes sense to spread the £20k over a diversified range of shares.

That could be in a Stocks and Shares ISA or other share-dealing account, but whatever investing platform is used, it is useful to keep an eye on costs as they can eat into the returns.

Well-known broadcaster with a 6.7% yield

One share I think investors should consider at the moment for its long-term passive income potential is FTSE 250 broadcaster ITV (LSE: ITV). It yields a juicy 6.7%. It also aims to maintain its annual payout per share at least at the current level.

Still, with its well-known brand, strong broadcasting footprint and extensive production business, why does the share have such a high yield? Why does it sell for pennies, after falling 38% in price over five years?

It is always worth asking such questions, not only because they could be a risk to the dividend, but also because even for an income-focused investor, capital loss can be painful.

ITV’s revenue last year fell slightly, while its pre-tax profit was down by over a third. Digital competition keeps growing and, while ITV is investing lots in digital provision itself, that is a costly process.

But it continues to generate sizeable advertising revenue – something this summer’s football World Cup could boost handily. The production and studios business provides some insulation against the ups and downs of advertising demand.

FT. Stocks and bonds slump in tandem as Iran shock leaves investors ‘nowhere to hide’ Traditional 60-40 portfolio of global equities and fixed income on course for worst month since 2022

Stocks and bonds slump in tandem as Iran shock leaves investors ‘nowhere to hide.

Global stocks and bonds have this month suffered their biggest combined sell-off since 2022 as the energy shock unleashed by the Iran war leaves investors “nowhere to hide”. The MSCI All Country World index, which tracks stocks across developed and emerging markets, has fallen around 9 per cent in March as the outbreak of war in the Middle East and de facto closure of the crucial Strait of Hormuz has caused a surge in energy prices. At the same time, a broad gauge of global government and corporate bonds has lost more than 3 per cent, as investors bet that central banks will need to raise borrowing costs to contain the inflationary fallout. The combined moves have put a traditional “60-40” portfolio of equities and bonds on track for the worst month since September 2022, when a previous cycle of global interest rate rises hammered markets. Even gold has tumbled as investors rush to liquidate previously winning trades, underscoring a lack of safe havens in financial markets. “What’s working for investors? Nothing,” said Raphaël Thuin, head of capital markets strategies at Tikehau Capital. “It’s really one of the worst set-ups you can think of. It’s been a very difficult few weeks to manage the market.” Wall Street stocks extended losses on Friday, following their worst day since the war began on Thursday, after US President Donald Trump failed to reassure investors by extending his deadline for attacks on Iranian energy infrastructure. The S&P 500 fell 1.7 per cent, taking its decline this month to more than 7 per cent. The sell-off in government bonds pushed the yield on the 10-year Treasury to as high as 4.48 per cent, its highest level since July. In Europe, which is more dependent than the US on energy imports, yields also touched their conflict highs. Trump’s deadline extension “does not fix the problem that builds day by day with the Strait of Hormuz being closed”, said Jordan Rochester, head of fixed income strategy for Emea at Mizuho. “Markets may start paying less attention to the White House jawboning and more to the energy scarcity situation on the ground.” Recommended The Big Read Stagflation is back The price of the international oil benchmark Brent crude has soared more than 50 per cent since the start of the conflict. That has prompted fears of global “stagflation” — a mix of faltering growth and rising prices — that has proved toxic for both equities and fixed income, as it was in the energy price surge that followed Russia’s full-scale invasion of Ukraine four years ago. “It’s been a brutal month for investors,” said Matt King, macro strategist and founder of Satori Insights. “Not only traditional 60-40, but almost every category of mainstream multi-asset portfolio is now showing year-to-date losses.”

Gold has tumbled 15 per cent this month as investors cashed in gains from a storming two-year rally that peaked in January and as a sharp shift higher in interest rate expectations dulled the attractions of the precious metal. Sophie Huynh, a multi-asset portfolio manager at BNP Paribas Asset Management, said that because there was “nowhere to hide”, investors were “liquidating some high-performing assets like gold”. Christian Mueller-Glissmann, head of asset allocation strategy at Goldman Sachs, said derivatives that allowed investors to bet on a rise in inflation or commodity prices were “the only things that can help you in the early stages of an inflation shock”. Bank of America’s recent fund manager survey showed that investors piled into cash at the fastest rate since the Covid-19 pandemic in March, highlighting the dearth of other safe-haven assets. “We shifted to overweight cash a week after the conflict started,” Mueller-Glissmann said. “We don’t like being overweight cash, it’s costly. As soon as we get a slowing of the conflict and the oil price trending down, we want to scale back into assets.”

Additional reporting by George Steer in New York.

Whilst it’s always a positive to have a dividend re-investment plan, some whiles are better than other whiles. Whatever the outcome to the Straits of Hormuz blockade, it’s going to take a while for constraints to normalize.

So most probably a U shaped recovery than a V shaped recovery, which could mean some great yields to lock away, hopefully for ever in your Snowball.

Why building a million-pound SIPP gets easier after £100k

Aiming to grow a seven-figure SIPP? Once you’ve got the first £100k, things get a lot easier thanks to the power of compounding. Here’s how.

Posted by Zaven Boyrazian

Published 5 April

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Building a million-pound Self-Invested Personal Pension (SIPP) is a goal shared by many UK investors. Reaching this coveted threshold is a multi-decade journey that requires immense patience and discipline, especially during periods of higher market volatility. But the good news is, once you’ve built the first £100k, things get a lot easier.

Here’s why.

Unleashing compounding

Let’s say someone’s putting aside £10,000 a year to invest in their SIPP. After receiving 20% tax relief from the government, that automatically gets topped up to £12,500 of investable capital. And investing this money at the stock market’s 8% average annualised return, a brand-new retirement portfolio would reach seven figures in just over 25 years.

The first six years of this journey are spent just trying to reach £100,000. But once a portfolio enters six-figure territory, compounding really starts working its magic.

After 10 years of consistently investing and staying disciplined, a SIPP would have grown to £190,557 – almost £200k. What’s exciting is that the second £100,000 only took around four years to achieve instead of six.

After 20 years, the SIPP is now worth £613,524. While only £190k was made in the first decade, during the second, close to £423,000 of wealth was unlocked. And with just another five years of staying focused and disciplined, the retirement portfolio will be on the verge of crossing over into millionaire-territory at £990,590.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

Aiming for 8%

Just last year, the FTSE 100 vastly outperformed its average. But when looking across the 2010s, the UK’s flagship index struggled to deliver close to 6% a year. And while a 2% difference may not seem like much, it actually adds close to five years to reaching millionaire status.

So rather than relying on index funds, investors can decide to invest directly into only the best and brightest of businesses. While this involves taking on more risk, it also opens the door to potentially market-beating returns, slicing years off the timeline.

Now lots of readers will not have 100k of capital to invest in a dividend re-investment scheme and even if they did they have to invest against all the mainstream advice they have been given over the years. That TR is more than important than dividends. The first six years of this journey are spent just trying to reach £100,000 so along as you add to your plan compounding really starts working its magic.

The first six years of this journey are spent just trying to reach £100,000. But once a portfolio enters six-figure territory, compounding really starts working its magic.

Benjamin Graham

My Top Dividend Bargains For April 2026

Rida Morwa Investing Group Leader

Summary

- Plant widely this spring; more income “seeds” mean a richer harvest.

- Don’t put all your eggs in one basket. Diversify for a steady income stream from your holdings.

- Our top picks to grow your income this spring; yields over 7%.

- Looking for more investing ideas like this one? Get them exclusively at High Dividend Opportunities.

Co-authored with Hidden Opportunities

Spring is here! This is the season when we spend more time in the beautiful outdoors. Gardening enthusiasts will head back to their backyards, ready to create wonders from the soil. The more seeds you sow, the merrier the garden becomes, and the more meaningful the harvest will be for you and your family. A single plant may produce enough to perhaps feed you once, but many plants together can fill the fridge with produce and feed your family throughout the season.

There is also reality. There could be infestations, imbalances in soil nutrient profile, the soil’s water retention capability, or unfavorable weather conditions, which could lead to losses in your garden and diminish overall returns. But even with these setbacks, a well-diversified garden with appropriate care can produce an abundant, dependable harvest.

Our Income Method follows the exact same logic.

At High Dividend Opportunities, we plant widely. We accumulate a large, diverse collection of income-producing holdings so that even if a few underperform or experience infestations through price volatility, economic shifts, or sector-specific headwinds, our portfolio continues to deliver a strong, steady harvest throughout the year.

As April begins, two holdings stand out as reliable income producers in our income garden, resilient, productive, and built to nourish your portfolio through all seasons.

Let’s dive in.

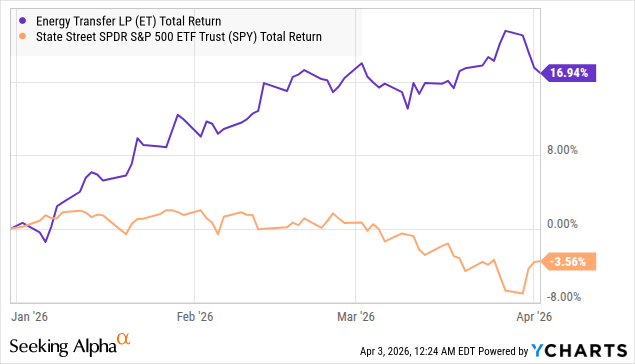

Pick #1: ET – Yield 7.1%

Not everything has been selling off amidst escalating tensions in the Middle East. To our subscribers, we outlined days before the beginning of the military operations against Iran that this involves a region quite critical for the global energy movement.

“The tension between the U.S. and Iran will influence oil prices more profoundly, as the Strait of Hormuz is the most critical oil chokepoint in the world, with 20 million barrels of oil per day passing through it.” – HDO Article, February 26th

The U.S. shale revolution gained momentum after 2005, significantly transforming the American energy landscape from a mindset of scarcity (as seen in the 1973 oil crisis) to one of abundance. The United States is currently the largest producer (and one of the largest exporters) of crude oil and natural gas.

Without a reliable supply of energy and the infrastructure to move it from extraction to processing, storage, and end users, a nation cannot achieve energy independence. This problem is clearly seen from the LPG (Liquefied Petroleum Gas) shortage in India and the closure of a substantial number of gas stations in Laos and Cambodia. Energy security is national security, and robust infrastructure is essential to supporting the industry and protecting the economy against geopolitical shocks.

Energy Transfer LP (ET) is a highly diversified midstream company with well-balanced business segments. ET is one of the largest midstream operators in North America.

Note: ET is a Master Limited Partnership that issues a Schedule K-1 to shareholders.

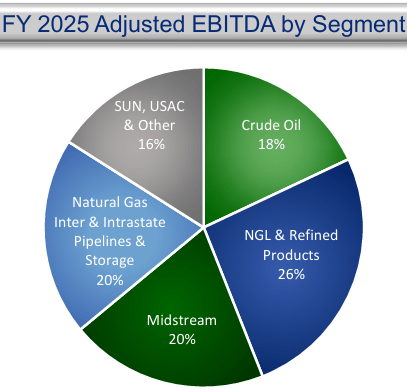

ET’s 2025 Adj. EBITDA represents a well-balanced business model, equally distributed between the following core segments.

- Crude Oil (18%) – Transports, stores, and markets crude oil through its pipelines and terminals.

- NGL & Refined Products (26%) – Transports, stores, and fractionates NGL (Natural Gas Liquids) and refined fuels.

- Midstream (20%) – Gathers, processes, and treats natural gas.

- Natural Gas Interstate & Intrastate Pipelines & Storage (20%) – Transports and stores natural gas across assets located nationwide.

- SUN, USAC & Other (16%) – Includes 100% ownership of Sunoco LP (SUN) fuel distribution and 39% ownership of USA Compression Partners (USAC) natural gas compression services.

ET holds higher debt levels compared to other midstream companies, expecting 2026 leverage between 4.0 and 4.5x Adj. EBITDA. This is due to significant CapEx (~$5.0-$5.5 billion earmarked for 2026), the majority around natural gas and NGL projects. ET has greater involvement in last-mile delivery to data centers, and the company has over 6 billion cubic feet/day of contracted pipeline capacity with a weighted-average life of 18 years, expected to generate over $25 billion in revenues from transportation fees. ET supplies natural gas to over 185 power plants across the country and has signed agreements with Oracle to provide natural gas to three data centers.

ET expects 2026 Adj. EBITDA between $17.45 and $17.85 billion, and targets a 3-5% annual distribution growth rate over the long term. About 90% of ET’s Adj. EBITDA is linked to fee-based contracts, implying that the company is not a direct beneficiary of higher commodity prices but is well-positioned to bring its newer assets to full capacity due to higher overall demand for midstream services.

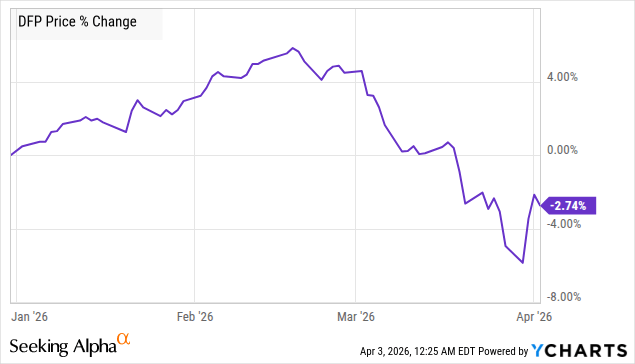

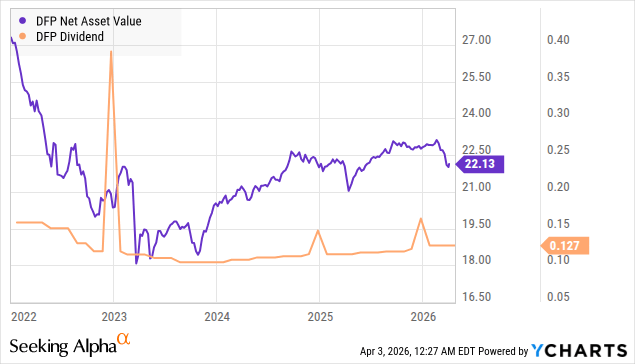

Pick #2: DFP – Yield 7.5%

Flaherty & Crumrine Dynamic Preferred and Income Fund (DFP) experienced a dramatic few weeks since the beginning of the armed conflict between the U.S. and Iran.

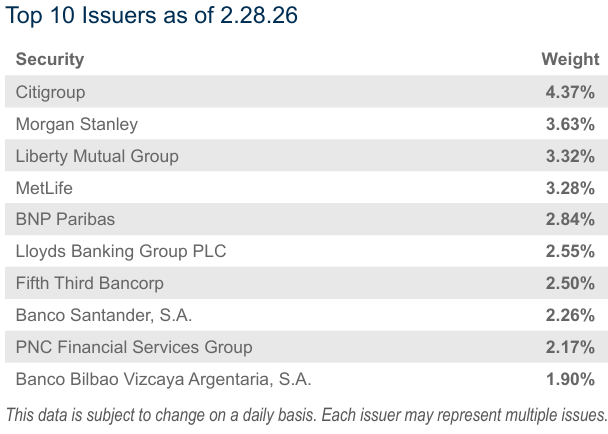

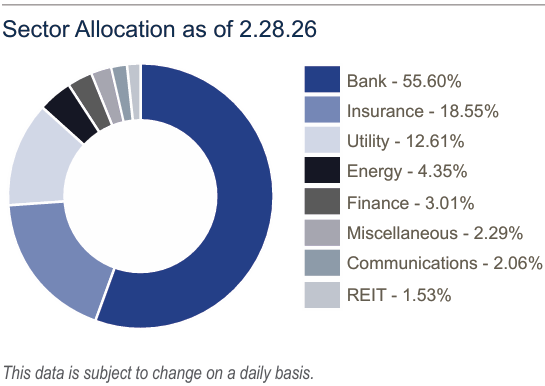

DFP holds publicly traded preferreds, mostly issued by banking, insurance, utility, and energy companies, with 70% of them based in the U.S., 10% in Canada, and the rest in the E.U. and the U.K. Source

What do they have to do with oil prices and the Middle East? Not much, but preferreds are sensitive to interest rates, and the market’s fear of the worst (rate hikes to combat higher inflation) is catching up on this relatively steady asset class. Notably, over 53% of DFP’s portfolio holdings are investment grade.

DFP operates with a 37% leverage at a borrowing cost of SOFR + 0.90%, and the CEF ended FY 2025 (November 30, 2025) with a weighted-average interest rate of 5.2%. This positions the fund for lower borrowing costs with every rate cut.

But what happens when rates rise?

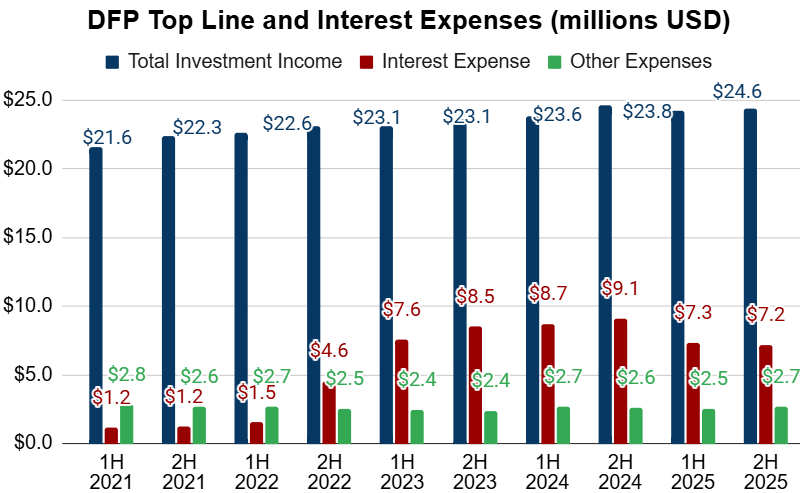

Borrowing costs rise, straining the 89% of DFP’s portfolio that is fixed-to-float securities, meaning that a substantial portion of this fund’s holdings will experience a reset in their coupon at staggered intervals. Looking at DFP since the rate hikes began in 2022, its NAV and distributions experienced a decline, followed by a steady rise as we continued to navigate through a declining rate cycle.

The higher allocation to rate-reset-type securities has resulted in a growing top line for the CEF as rate hikes intensified. Despite this, higher borrowing costs weighed down on funds available for distribution.

In recent years, DFP’s distributions have mostly been Qualified Dividends, making it highly efficient from a taxation standpoint. Wall Street’s fear about rate hikes to combat inflation will yet again be an opportunity for investors to buy fixed income on the cheap. To make things appealing, DFP trades at an 8% discount to NAV, letting you buy into the fixed-income space at a bargain.

Conclusion

A successful harvest isn’t built from a single plant; it’s built on many. At High Dividend Opportunities, we apply the same principle to our portfolio. We invest across several sectors and asset classes, including fixed-income positions. Our comprehensive bond ladder ensures that every year, a steady stream of capital matures and returns fresh cash to reinvest into the best opportunities the market offers, whether it’s a bull run or a downturn.

Our Rule of 42 enables our portfolio to benefit from an abundant, reliable flow of dividend and interest income. This is how we stay hungry and keep growing, even if market sentiment is weak. This is the power of income investing.

Why Smart Investors Are Thinking Long-Term Again

Elizabeth Carter

Years passed with folks hunting fast returns. Chasing meme shares, flipping trades daily, riding viral waves – all painted riches as simple. Yet now, things feel different. Swings grew wilder, excitement faded fast, bets on noise led straight to loss. Many watched savings vanish almost overnight. Slowly, more cautious minds are shifting back – to patience, to foresight, to playing the long game instead. Week by week, chasing gains takes a back seat while patience grows stronger. With everyone rushing ahead, calm focus on slow progress finds its moment once more. Discipline slips in where noise used to be, building step after step without fanfare. Steady climbs matter now, even when quick wins steal the spotlight. Time begins to show its weight, shifting things beneath the surface.

Less Emotional Stress

Now here’s something real: wild price jumps lately made many rethink quick trades. Instead of chasing every move, sticking around longer tends to even things out. Feelings often get loud when money dances up and down – planning ahead keeps those voices quieter.

Power of Compounding

Patience finds its match in compounding. Those who hold investments over long stretches see gains build on top of gains – something quick moves usually miss. Growth like this tends to grow quietly, over time.

Avoiding Hype

Falling fast after a flashy climb, once-hot investments have left plenty of buyers second-guessing their choices. Sticking with steady plans keeps people from tumbling into short-lived market surges.

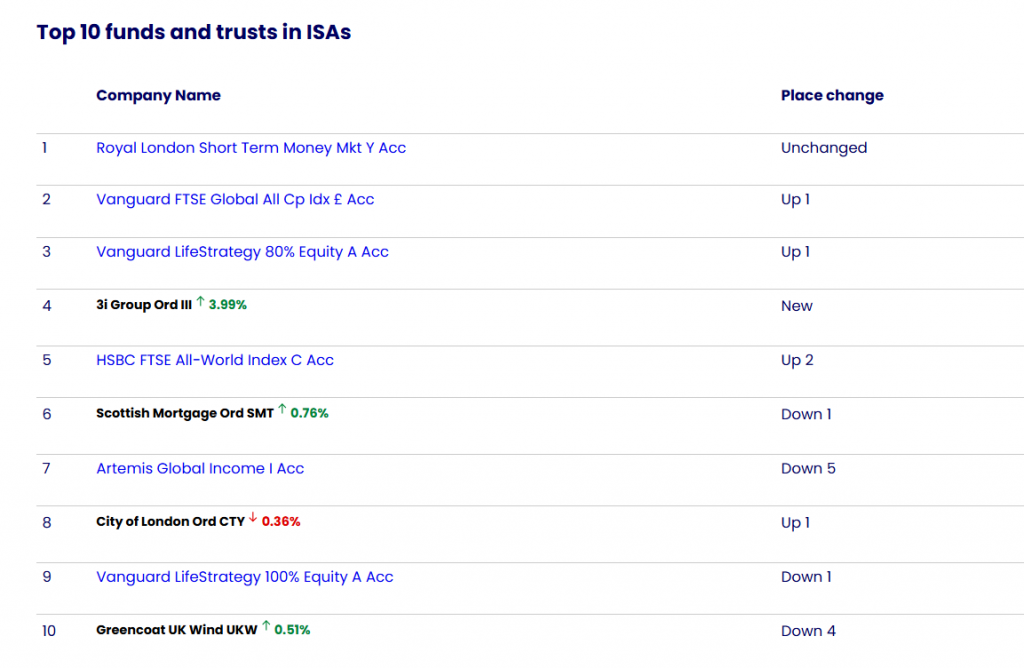

Investors are seeing widely discounted shares in 3i Group Ord

3.99% as a bargain, with the private equity behemoth soaring back into the bestsellers table.

The trust, associated both with its chunky stake in discount retailer Action and the substantial premium on which its shares have tended to trade, initially slipped late last year amid warnings of softening sales growth for its main holding.

The shares tumbled afresh late last week, after an update from Action that outlined plans to expand into the US market appeared to unsettle investors. 3i Group shares have moved to a discount in recent weeks and that has widened markedly in recent days.

Some separate trends otherwise hold firm. Royal London Short Term Money Mkt Y Acc retains its top position, perhaps unsurprising given the continued volatility of markets.

Interestingly, we also see plenty of investors taking advantage of such volatility via global tracker funds, with Vanguard FTSE Global All Cap Index £ Acc and Vanguard LifeStrategy 80% Equity A Acc each moving up a notch, to second and third place respectively. HSBC FTSE All-World Index C Acc also sits in the top five, having gained two places.

Artemis Global Income I Acc, which recently spent a few weeks in top spot and delivered massive gains in 2025, has now drifted down to seventh place.

The fund, which has substantial exposure to equity regions most shaken by recent conflict such as Europe and emerging markets, has lost around 9.5% since the onset of hostilities in late February.

A few other favourites retain their presence in the table, from future trends play Scottish Mortgage Ord

0.76% to high-yielding renewables trust Greencoat UK Wind UKW0.51%.

Forget Oil Stocks: This 7.7% Dividend Is a Smart Contrarian Buy Now

Michael Foster, Investment Strategist

Updated: April 2, 2026

Iran War volatility has tossed finance stocks “out with the bathwater.” It’s giving us a nice “second chance to buy” my favorite finance-focused dividend.

That would be the John Hancock Financial Opportunities Fund (BTO), which yields 7.7% today and, as we’ll see, trades at a discount that’s double what most investors think it is.

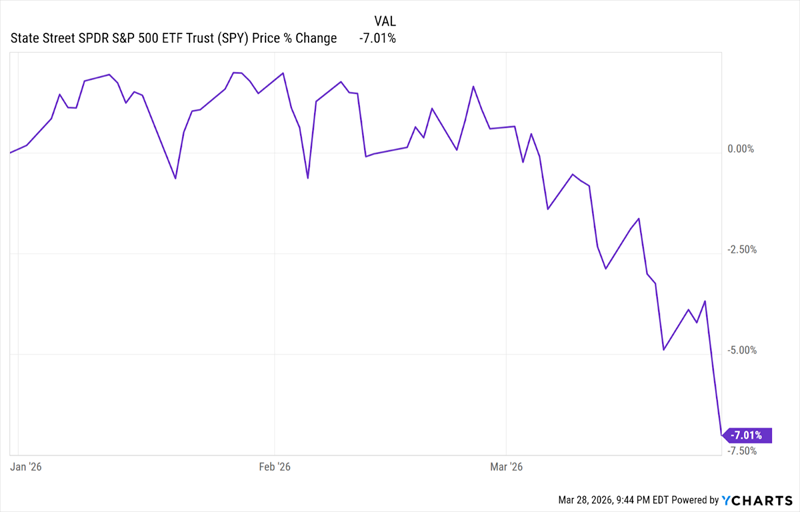

Why April 2026 Could Be April 2025 Redux (But With a Faster Rebound)

To see why I think the market is making a mistake when it comes to finance stocks, let’s rewind to last year, when stocks sold off on the so-called “Liberation Day” tariffs.

From the Spring 2025 Selloff …

That selloff has actually looked a lot like this one so far, with a similar depth:

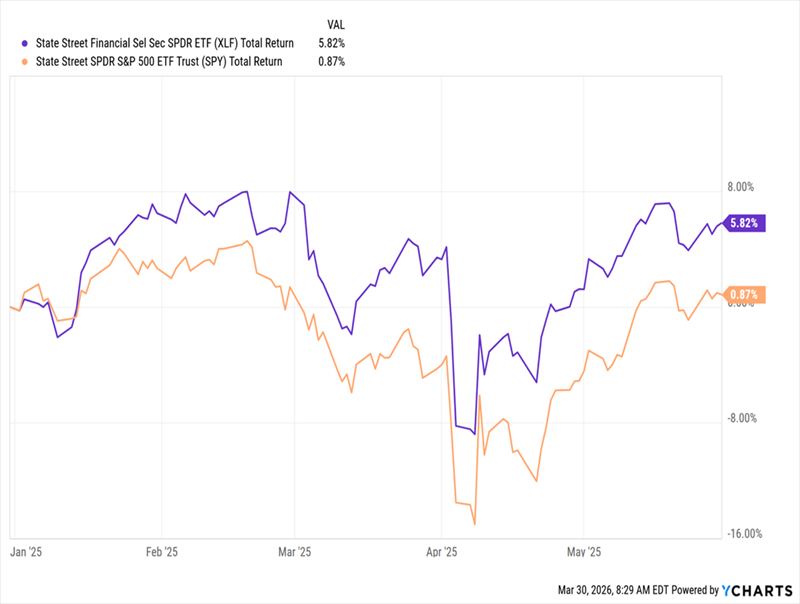

… to Its 2026 “Twin”

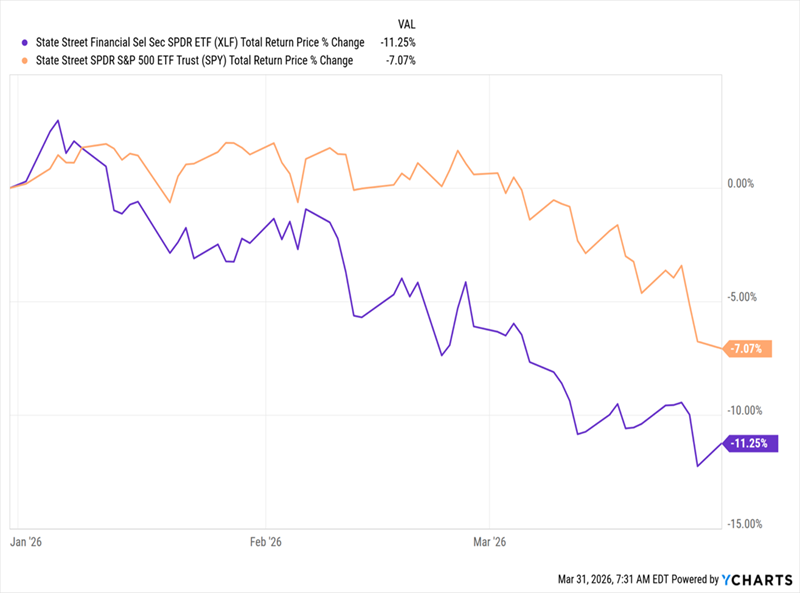

Here’s what I really want to draw your attention to: In 2025, the finance sector—shown by its benchmark ETF in purple below, didn’t fall as hard as the rest of the market, and soared on the other side:

Finance Beat the S&P 500 in the 2025 Plunge …

Fast-forward to this year, and finance stocks are being hit harder in the Iran War fallout, falling much further than the market since the start of the year.

… And Looks Like a Coiled Spring This Time Around

That’s excessive, in my view, and positions the sector for a stronger rebound this year. That’s because, at their core, both of these selloffs are about one thing: inflation. Last year, the driver was thought to be tariffs. This year, it’s oil prices.

And last year, it was hard to tell which sectors could win as the administration brought in tariffs on everything from lumber to car parts. This year, it’s easier to peg a winner: oil stocks, which have already surged.

That ship, of course, has already sailed for us, and we never chase trades at CEF Insider. But finance is setting up to be our still-discounted play here, as it’s poised to benefit from two trends stemming directly from the oil-price surge.

First, continued oil-price volatility—almost certain, no matter when the war ends—will drive higher commodities-trading revenue for banks. And if higher oil becomes a “new normal,” oil producers (most of whom are generally cautious about committing to higher production) will eventually expand output—and will of course look for financing to do so.

And then there’s a third angle few investors have even thought of.

Airline-Fuel Hedging Could Be Set for a Comeback

Years ago, airlines used derivative contracts on oil to hedge their exposure to energy prices. Intermediaries (banks, in other words) took a fee for this, alongside other players, like hedge funds. But these programs were expensive to run, so most airlines have wound down their hedging programs over the last decade or so.

But now it seems they’re thinking about doing it again:

“US airlines abandoned the practice of hedging against fuel costs long ago. With oil prices surging following US-Israel strikes ?on Iran, they could be looking at a big bite out of their bottom line in the event of a lengthy conflict that keeps prices elevated for months.”

This March 6 report from Reuters tells us that there may be more demand for options in the future, which is good news for the financial sector broadly.

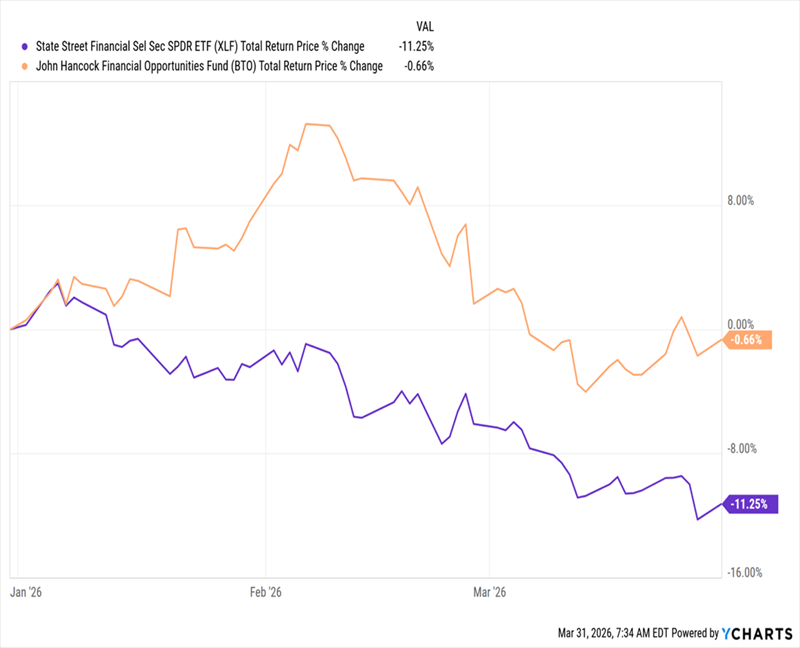

Which brings me back to BTO, which is roughly flat this year (shown in orange below), on a total-return basis as of this writing, compared to the more than 11% decline we’ve seen from the financial sector as a whole:

BTO Falls Less Than Finance …

That’s the kind of resilience we want to see from a CEF in this environment.

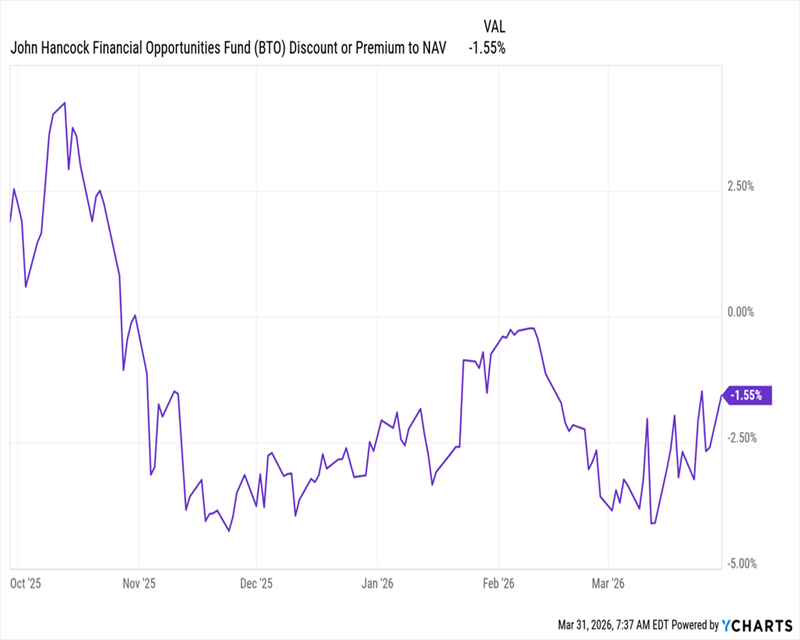

And here’s where things get interesting: Even though it’s held up better than the sector, BTO has remained a bargain by another key metric: the discount to net asset value (NAV, or the value of its underlying portfolio).

… While Keeping Its Discount

As you can see above, the fund now trades at a bit less than a 2% discount. And that discount is actually much larger in real terms, because BTO’s valuation is normally well above par, averaging a 3.9% premium over the last five years. Indeed, you can see in the chart above that it’s fallen from around that level just six months ago.

BTO is also notable in that it holds mainly regional banks, and while they may not be as exposed to things like airline fuel hedging, they stand to gain on improving prospects across the sector as a whole. Those in energy-producing areas are likely to do better, like Hancock Whitney (HWC), BTO’s No. 7 holding, based in Gulfport, Mississippi.

Moreover, regionals let us better diversify across the sector, while keeping our focus on the US, the world’s largest oil producer, which accounts for 95% of BTO’s portfolio.

The fact that regionals have been caught in the downdraft that’s affected the whole sector is an opportunity for us to get BTO at a 7.7% yield and that “larger-than-it-looks” discount. This way, we’re setting ourselves up for higher income and potential gains as that markdown moves back to a premium, where it belongs.

In times like these, a growing 7.7% dividend can bring us a lot of peace of mind. But the beauty of CEFs is we can get dividends that are even higher—and pay us every month, too.

That’s right in line with our monthly bills, of course. And if you want to reinvest, great ! Monthly payouts let you do so even faster.

Results analysis: Octopus Renewables Infrastructure (ORIT)

ORIT continues to execute on its 2030 strategy.

Alan Ray Updated 31 Mar 2026

Disclaimer

This is not substantive investment research or a research recommendation, as it does not constitute substantive research or analysis. This material should be considered as general market commentary.

- Octopus Renewables Infrastructure’s (ORIT) annual results to 31/12/2025 show a NAV total return of -2.8% (2024: +2.5%). At an operational level, ORIT’s power generation and revenues grew by 5% (2024: 7% and 12%), and EBITDA by 3% (2024: 16%). Total shareholder return was -1.5%.

- ORIT met its dividend target of 6.17p, 1.14x covered by operating portfolio cash flows (2024: 6.02p, 1.24x). The dividend was an increase of 2.5% over 2024, in line with UK CPI for a fourth consecutive year. The target dividend for the year ending 31/12/2026 is an increase of 1% to 6.23p and is expected to be fully covered. At the current share price (as at 30/03/2026) the yield is c. 10.9%.

- The NAV per share was 93.8p (2024: 102.6p), a c. 9% decline. The main components of the fall were adjustments for power prices and green certificates (-4.2p), RoC indexation adjustments (-0.9p), adjustments to developer valuations (-1.4p) and changes in discount rates (-0.7p).

- ORIT’s weighted average discount rate, in local currency terms, increased to 7.8% (2024: 7.4%). ORIT’s discount rate is calculated on operational assets, and factoring in the developer company assets as well as impacts of FX and the RCF, the expected portfolio return is 8.2%.

- Fixed revenues rose from 84% to 88% (forward fixed for two years), reducing ORIT’s exposure to short-term power price fluctuations. In addition, about half of revenues are inflation-linked over ten years.

- ORIT was geared 45% LTV or 82% as a percentage of NAV (2024: 45%), although the level of debt was reduced in absolute terms, with c. £56m paid down over the year. 75% of debt is fixed rate with an average cost of 3.3% and an average remaining term of ten years. The medium-term goal is to reduce gearing to 40% although the managers note this level could fluctuate on a short-term basis.

- ORIT defines itself as an impact fund with a core impact objective of accelerating the transition to net zero through its investments and is classified under Article 9 of SFDR. The impact highlight from the financial year is 1,304 GWh of renewable energy generated (2024: 1,240 GWh), with the portfolio having the potential to avoid 344k tCO2. A detailed breakdown including the cumulative impact over five years is in the annual report.

- Capital allocation policy update:

- Disposals totaling £74.3m brought the total under the policy implemented in 2023 to £235m, achieved at a weighted average uplift of 9%.

- £26m of the £30m share buyback now executed.

- ORIT 2030. In September 2025, the board announced its ‘ORIT 2030’ strategy, which sets out its four priorities for the next five years.

- Grow: Invest for NAV growth, deploying capital into higher growth investments, including an increased 20% target allocation to construction assets, maintaining the current 5% allocation to developers. There will also be a greater focus on asset improvement and disciplined capital recycling.

- Scale: Target £1 billion net asset value by 2030, to create a more liquid and investable company. Alongside investment growth, this could include corporate M&A.

- Return: Target medium-to-long-term total returns of 9-11% through a combination of capital growth and income, maintaining the progressive dividend policy, while preserving full cover and targeting medium-term gearing below 40%, although this level may fluctuate in short-term periods as mentioned above. Retain diversification across core technologies and geographies.

- Impact: Aim to build approximately 100 MW of new renewable capacity per annum (on average over the five-year plan).

As part of the ORIT 2030 strategy, the board is also recommending that the continuation vote moves to a cycle of every three years, from the current five. The change will be put to a vote at the 2026 AGM, with the next continuation vote then held at the 2028 AGM.

Chair Phil Austin said: “The ORIT 2030 strategic framework provides a clear structure for capital allocation and portfolio development over the medium term. The actions taken during FY 2025, particularly in relation to capital recycling, operational optimisation and capital structure discipline, are consistent with the early execution of this strategy.”

Kepler view

Once again, at an operational level, ORIT delivered good performance, with an increase in power generation and revenues. The ORIT management team also note that at a technical level, the portfolio performed well, with less downtime than expected. And diversification played an important role, with lower wind speeds offset by strong performance from solar assets, particularly in the UK.

Further, ORIT completed its fourth consecutive year of dividend growth, essentially increasing its dividend in every full operational year since its IPO. The target for the FYE 31/12/2026 is a further increase, albeit at a lower rate of 1%. Whereas the dividend policy has never explicitly targeted matching inflation, in the past ORIT’s dividend increases have been in line with UK CPI inflation. As ORIT shifts to its ORIT 2030 strategy, which targets higher returns through more investment in construction assets, and strategic recycling of operational assets, the goal remains to target a progressive dividend, but as the strategy evolves clearly a greater exposure to non-yielding construction assets will make it harder to increase dividends in line with inflation. Overall, though, the anticipated result of this shift is an increase in annual returns of 9-11%, up from the 7-8% envisaged at IPO.

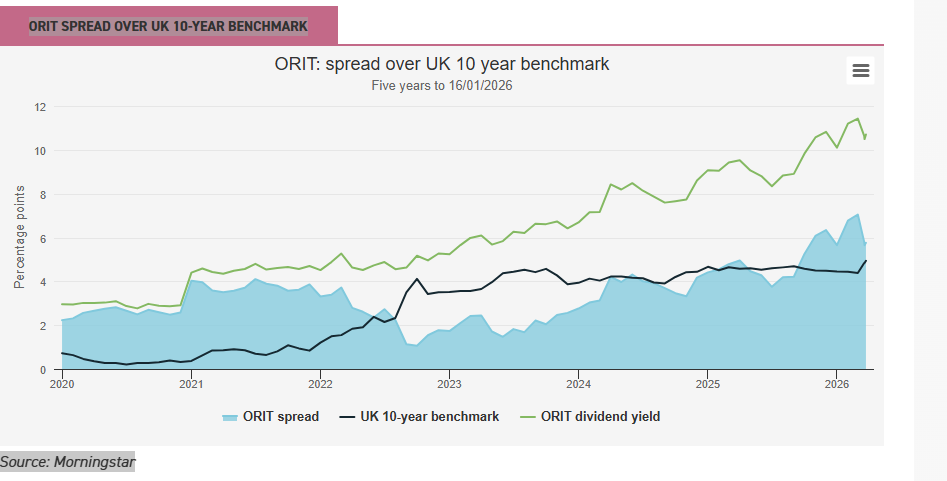

Clearly though, the macro backdrop remains challenging, with ORIT’s peer group of renewable energy infrastructure trusts all trading at wide discounts and, in many cases at dividend yields of 10% or more. This is an interest-rate sensitive asset class, and current events in the Persian Gulf are taking their toll on government bond yields, with the UK 10-year benchmark bond yield briefly touching 5% in recent days. ORIT’s near-term power prices are 88% fixed (for two years) so a short-term spike in energy prices will have little impact, although if longer-term futures rise, there may be opportunities to fix at higher rates further out. Rising interest rates will have an impact, but given these are likely to be a response to higher inflation, and half of ORIT’s portfolio is inflation-linked, revenues would rise, providing partial protection. So, there are push and pull factors that investors need to consider. But in considering the chart below, which shows ORIT’s dividend yield as a spread over the above mentioned 10-year benchmark, it’s worth reflecting that this lifetime-high gap comes at a time when, once again, the UK and other European countries are under pressure to evolve their energy security policy. Notwithstanding the uncertainty around bond yields and inflation, the valuation of assets that generate power without any reliance on global hydrocarbon supply chains seems like an anomaly investors should be paying more attention to.

Orit spread over uk 10-year benchmark

| lemon casino belépés lemonkaszino.com/hux marthabeverly520@gmail.com 107.152.32.177 | I’m extremely impressed with your writing talents and also with the layout for your weblog. Is this a paid topic or did you customize it your self ? Anyway keep up the nice quality writing, it is rare to look a nice blog like this one these days.. |

All my own customizing, with a big help from Copilot for the Graphics.