Whilst you may never be a millionaire, if you concentrate on the tail not the dog, you should have plenty of repeatable income when you retire. The more years you have to retirement the more repeatable income you should have in your Snowball.

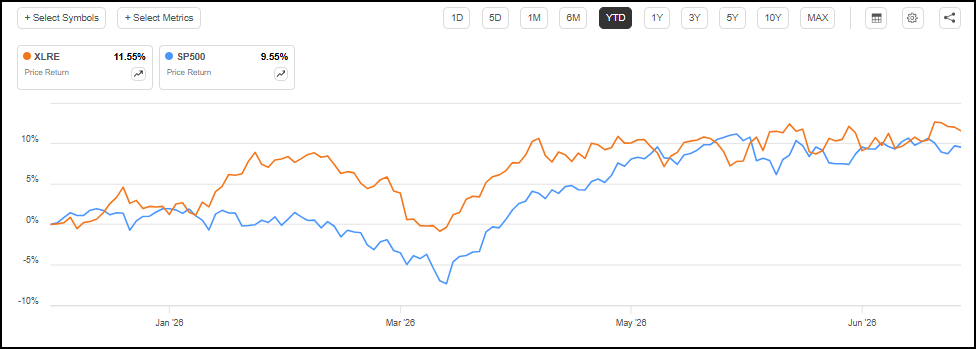

REITs are staging a comeback in 2026, with the real estate sector (XLRE) outperforming broad equities, potentially signaling stronger full‑year returns.

Given recent market volatility, REITs can be a smart addition to portfolios, offering steady income today alongside meaningful long‑term capital appreciation potential.

SA Quant’s proprietary REIT factor model has identified three REIT Strong Buys delivering an average forward yield of nearly 9.8%, pairing high income potential with solid dividend safety grades.

I am Steven Cress, Head of Quantitative Strategies at Seeking Alpha. I manage the quant ratings and factor grades on stocks and ETFs in Seeking Alpha Premium. I also lead Quant Growth and Income, which is a model portfolio for dividend investors interested in capital appreciation and income.

8vFanI/iStock via Getty Images

Why 2026 Could Be the Year REITs Rebound

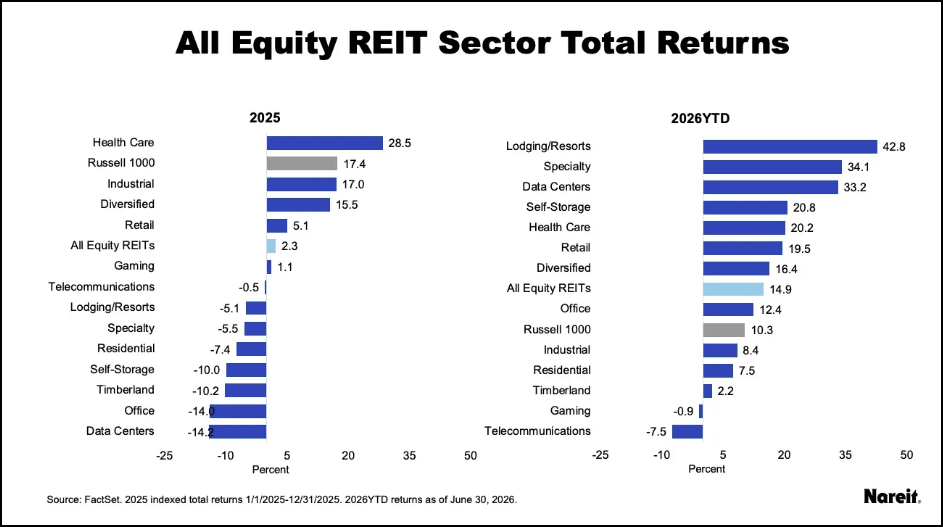

2026 is shaping up to be a brighter year for REITs than 2025. The real estate sector (XLRE) has outperformed broad equities so far this year, and that early strength has historically been a good indicator for full-year performance.

State Street Real Estate Select Sector SPDR ETF (XLRE) vs. The S&P 500 YTD

SA Premium

Last year, REITs lagged as higher-for-longer rates and valuation pressure weighed on returns, even though fundamentals remained solid. In 2025, the broad equity market outperformed REITs, but by mid 2026, REITs had reversed that gap and were ahead of the Russell 1000, with gains broadening across most property sectors. That strength reflects both supportive operating trends and the shifting landscape of the REIT sector tied to long-term shifts in the economy.

Macro tailwinds could also portend continued strength for the sector. Recent inflation data has cooled, which could lower expectations for additional Fed tightening and help stabilize rate expectations that are paramount for real estate valuations. June CPI declined 0.4% month over month, core CPI was flat and running at 2.6% year over year, and June PPI also came in softer than expected, reinforcing the idea that inflation pressures may be easing rather than reaccelerating.

With that macro pressure easing, the sector is getting more support from fundamentals too. Industrial REITs continue to benefit from reshoring-related demand, while retail, senior housing, hotels, and data centers have been cited as areas where demand is outpacing new supply, giving landlords more pricing power.

Outside of appreciation potential, REITs can be a useful portfolio tool in the current volatile market because their income stream can help steady overall cash flows. Their dividends may offer a more reliable return profile than many equities, especially as investors rotate between inflation concerns, rate-cut expectations, and growth-stock swings. In that role, REITs can provide both income and a measure of stability while markets digest a still-uncertain macro backdrop

How I Chose My Top 3 REITs Averaging 9.8% FWD Yield

When I write dividend-focused articles, I tend to focus on companies with excellent dividend safety and growth grades. However, for this exercise, I targeted REITs using Seeking Alpha’s Top Real Estate Stock Screener, filtering for Strong Buys with yields above 5% and dividend safety that’s better or broadly in line with the sector. I placed less emphasis on dividend growth because the goal here was to identify names that could offer a sizable income stream today, even if near-term payout growth is not especially compelling. Let’s take a closer look at the names below.

Quant Sector Ranking (as of 7/23/2026): 15 out of 168

Quant Industry Ranking (as of 7/23/2026): 3 out of 13

Quant Rating: Strong Buy

FWD Yield: 12.20%

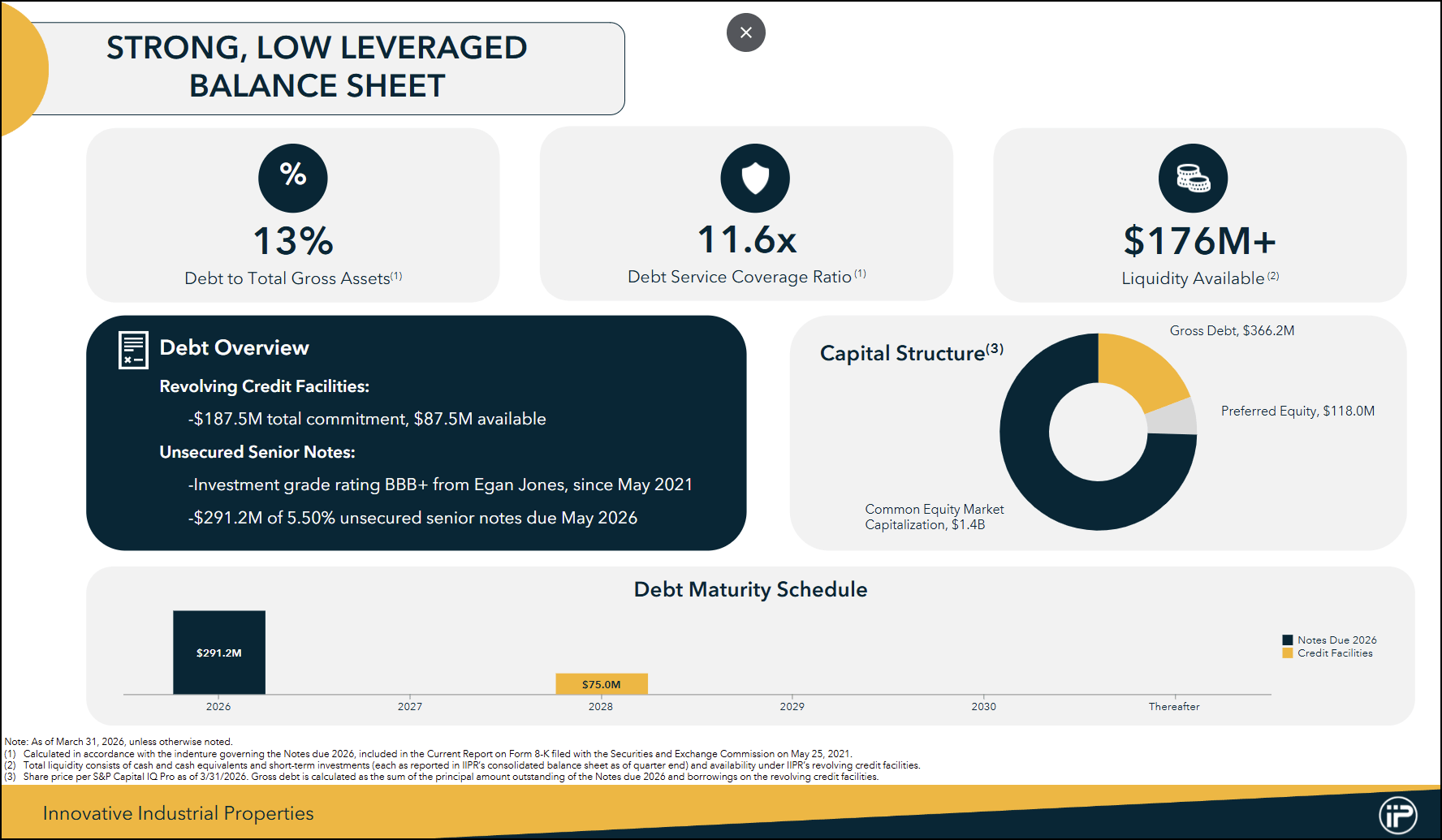

Innovative Industrial Properties (IIPR) is the No. 3 Quant-ranked Industrial REIT that owns and leases specialized facilities to state‑licensed cannabis operators, with a growing foothold in life‑science real estate. Its recent earnings call showed revenue and cash flow holding steady while growth is driven by signing new tenants on formerly defaulted properties, progressing dozens of lease agreements, and investing in the IQHQ life‑science project, all supported by solid liquidity and modest debt.

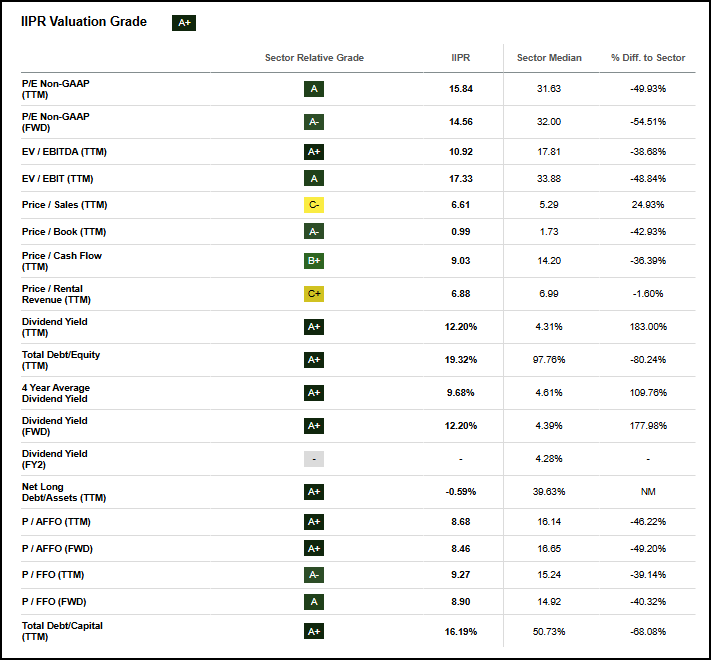

IIPR AFFO growth 5Y CAGR is 77% above the sector median, accompanied by stellar profitability. The company offers an AFFO margin that’s 94% above the REIT sector median, alongside a net income margin of nearly 46%. The company especially stands out in terms of its valuation where it offers both trailing and forward price/AFFO ratios that are 46% and 49% below the sector median, respectively.

IIPR Valuation Grade

SA Premium

The company is particularly attractive for its dividend profile. Currently yielding 12.20%, well above the sector average, IIPR also has solid dividend safety, supported by an FFO interest coverage ratio of 9x compared to the sector’s 3x. IIPR’s offers a potent combination of excellent fundamentals alongside stable income, making it hard to overlook for REIT investors.

Quant Sector Ranking (as of 7/23/2026): 17 out of 167

Quant Industry Ranking (as of 7/23/2026): 1 out of 11

Quant Rating: Strong Buy

FWD Yield: 6.00%

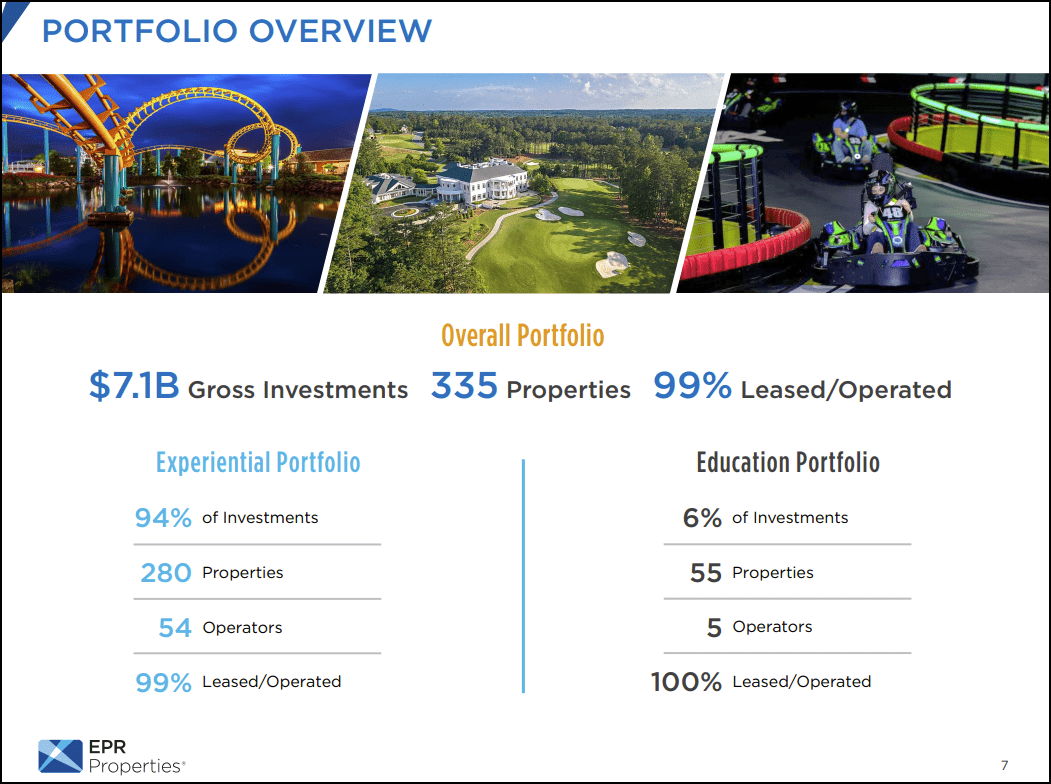

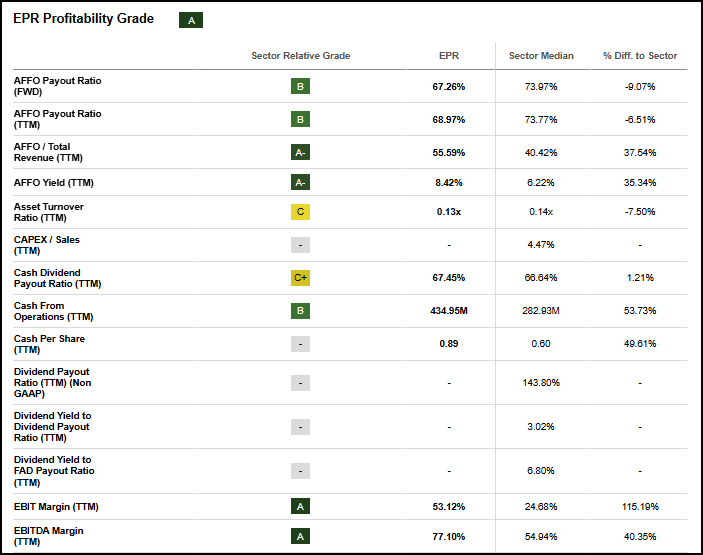

EPR Properties is a specialty REIT that owns experiential real estate, including movie theaters, education assets, and recreation venues such as ski resorts and water parks, largely under long-term net leases. The company was one of the inaugural holdings in the Quant Growth & Income portfolio and has stood out in this volatile market, returning about 10.3% since the portfolio’s launch on June 3. The company has invested $7.1 billion across 335 properties and maintains a 99% leased or operated rate.

EPR’s growth profile has rapidly improved to an ‘B+’ after sitting at a ‘C’ just six months ago. Highlights include Its forward AFFO growth of 5.40% that exceeds the sector median by nearly 85%. The company also showcases a TTM dividend growth rate of 4% vs. just 2% for the broader REIT sector. ERP’s triple‑net lease structure has helped fortify its profitability by shifting property‑level costs (taxes, insurance, and utilities) to tenants. This protects margins even in a higher‑rate, higher‑inflation environment.

EPR Profitability Grade

SA Premium

EPR offers a forward dividend yield in the 6% range, which is comfortably above the broader REIT sector. This sizable dividend is supported by its forward AFFO yield is close to 9%, creating a cushion that supports the current payout while still leaving room for the company to reinvest in future growth.

Quant Sector Ranking (as of 7/23/2026): 6 out of 167

Quant Industry Ranking (as of 7/23/2026): 1 out of 13

Quant Rating: Strong Buy

FWD Yield: 11.10%

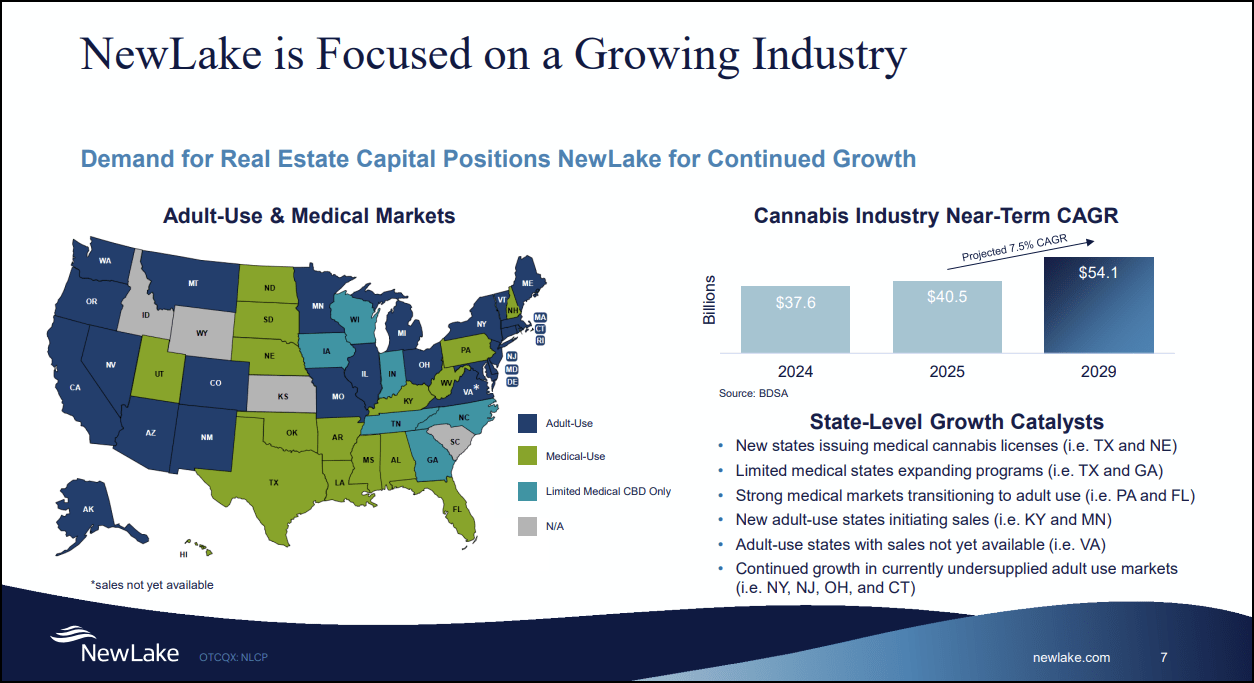

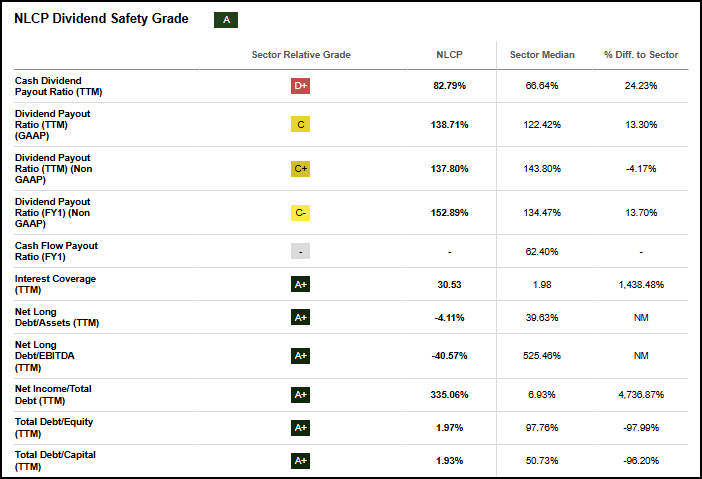

NewLake Capital Partners is another cannabis-adjacent REIT provides real estate capital to state‑licensed cannabis operators. The company operates a triple-net lease model that involves sale‑leaseback deals on cultivation facilities and dispensaries. The REIT buys properties and leases them back to operators, giving tenants growth capital while retaining long‑term ownership of the underlying real estate. NLCP is benefiting from a rapidly expanding U.S. cannabis footprint. Rising rising state adoption and a projected mid single‑digit industry CAGR create a long runway for NewLake.

NLCP’s forward dividend yield sits around 11% and exceeds the sector median by more than 150%. Its dividend profile is further supported by strong coverage metrics, including an interest coverage ratio of roughly 30x, which underscores both payout safety and balance‑sheet strength.

NLCP Dividend Safety Grade

SA Premium

NewLake’s growth story is increasingly tied to a more accommodative regulatory environment, dovetailed by its conservative balance sheet. A potential federal rescheduling of medical cannabis, potential 280E tax relief, and a coming ban on intoxicating hemp products could strengthen tenant finances, creating more opportunities for NewLake to deploy capital into cultivation and dispensary properties. The stock trades at a hefty discount across key REIT valuation metrics like its FWD Price/AFFO, which sits 51% below the sector median. With the cannabis industry on the cusp of multiple growth catalysts, now could be an opportune time to consider adding this high‑yielding value name to a diversified income portfolio.

Concluding Summary

REITs are finally getting some tailwind in 2026, with the sector outperforming broad equities as inflation has been leveling and interest‑rate expectations stabilize. In this environment, income seekers can find attractive opportunities in select high‑yield names that combine strong payouts with solid fundamentals and balance‑sheet strength. SA Quant has identified Innovative Industrial Properties (IIPR), EPR Properties (EPR), and NewLake Capital Partners (NLCP) as three REITs offering a near average 9.8% forward yield alongside strong factor grades and robust dividend safety.

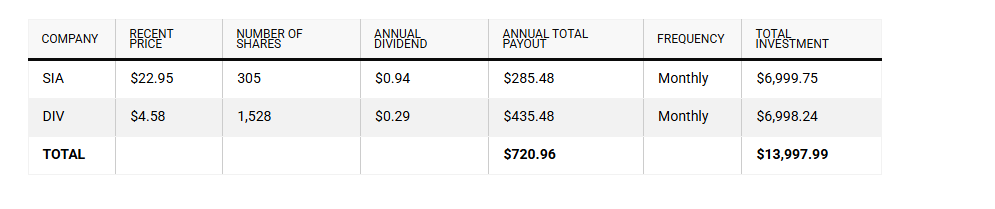

Split $14,000 between Sienna Senior Living and Diversified Royalty to target about $721 yearly income, paid monthly.

Sienna’s dividend looks better covered, with improving occupancy and an AFFO payout ratio around 68.5%.

Diversified Royalty pays a higher yield but had a payout ratio above 100% last quarter, so monitor coverage and diversify.

One $14,000 Tax-Free Savings Account (TFSA) balance could trigger more than 120 tax-free deposits over the next decade, without selling a single share. How? At current prices, two monthly dividend stocks could produce about $60 every month, creating a small retirement paycheque that keeps showing up while the portfolio remains invested.

That income won’t replace a salary, but it can buy new shares, cover a bill, or grow into something far more useful over time. The key is building the payments around businesses supported by different sources of cash flow rather than chasing one enormous yield.

Once invested inside a TFSA, dividends and capital gains can grow without Canadian tax. That gives monthly payments more money to compound, which leads me to Sienna Senior Living (TSX:SIA) and Diversified Royalty (TSX:DIV).Z

SIA

SIA stock owns and operates retirement residences and long-term-care homes across Canada. Demand should continue growing as the population ages, while government funding and resident fees create recurring revenue from services people can’t simply postpone.

* Returns as of July 6th, 2026

The company’s retirement same-property occupancy reached 94.7% during the first quarter, while its adjusted funds-from-operations (AFFO) payout ratio improved to 68.5%. That coverage supports SIA stock’s monthly dividend of $0.078 per share, equal to $0.936 annually.

SIA stock therefore provides a relatively defensive starting point, but healthcare exposure alone won’t create a balanced income plan. The second holding adds royalties collected from a much broader group of consumer businesses.

DIV

Diversified Royalty earns cash by owning trademarks and other rights used by brands including Mr. Lube, BarBurrito, and AIR MILES. Those partners pay royalties based on sales or fixed agreements, allowing Diversified Royalty to collect cash without operating every restaurant, tutoring centre, or automotive shop itself.

First-quarter revenue rose 11.8% to $17.5 million, while distributable cash increased to $12 million. The first-quarter payout ratio reached 101.1%, partly due to seasonal weakness among certain partners. Investors should watch that figure closely, although management aims to pay a stable monthly dividend and grow it as cash flow allows.

The $14,000 income plan

With that $14,000, I’d divide the money equally, giving SIA stock’s healthcare operations and Diversified Royalty’s consumer brands the same starting weight. Using recent prices, the portfolio could generate approximately $720.96 annually, or $60.08 per month.

Of course, SIA stock faces staffing expenses, government regulation, development costs, and substantial debt. Diversified Royalty depends on its partners remaining healthy enough to make their payments, while its first-quarter payout exceeded distributable cash.

Those risks make both holdings better suited to one portion of a broader collection of monthly dividend stocks. Reinvesting the income can also reduce the temptation to treat each deposit as guaranteed spending money.

Bottom line

SIA stock brings senior-housing demand and strong distribution coverage, while Diversified Royalty supplies a higher yield backed by several consumer brands. Holding both could keep monthly cash moving into a TFSA today, then let reinvestment turn that modest paycheque into a much larger source of retirement income.

A big concern I hear from those who want to gift money is the fear of leaving themselves short in later life. But that is exactly what annuities are there for, and now is actually a great time to buy one.

Annuities were unpopular for many years because low interest rates meant they offered relatively poor returns, but higher interest rates over the past few years have meant they offer vastly better value.

The average annuity rate was 7.62 per cent as of March 2026, according to insurer Standard Life. That means a healthy 65-year-old with a £100,000 pension pot can lock in a guaranteed annual income of up to £7,620.

With £300,000, you could generate £22,860 income annually – with the full new state pension, that’s an annual income of almost £35,000 a year.

If you’re waiting for the perfect moment to do anything in life, there’s a risk you’ll never get around to it. And when it comes to saving and investing, you’ll pay a real price for the delay. So, it can help to know when other people have taken the plunge, and just how they’re doing, to see whether we’re on track, or if we need to get cracking. Here are the ages that are financial landmarks among AJ Bell customers.

First year of life: Junior ISA accounts are most commonly opened

The most popular time to open an AJ Bell Junior ISA (JISA) is in the first year of a child’s life. It’s a great idea for when you have a newborn, so anyone who wants to celebrate the birth can do so with a gift into the JISA that they’ll appreciate far more than a new rattle or babygrow.

However, people aren’t just using them for one-off payments. The first year of a child’s life is also the most popular time to set up a regular direct debit into the account. If this is a bit of a stretch in the expensive early years, talk to grandparents and the wider family. They may be able to make manageable monthly payments that will keep building a valuable nest egg for when they’re 18.

Age 25 to 26: The most Stocks and shares ISAs are opened

The fact that the most common age to open a Stocks and shares ISA overall is 18 is a testament to the success of the Junior ISA, and how many people have already become investors before they leave childhood.

Excluding maturing JISAs, the most popular age to open an AJ Bell Stocks and shares ISA is either 25 or 26. By this age, people will have started work and have a few years under their belt. They’ll have got to grips with their expenses and are likely to have been in a workplace pension for a few years. They don’t necessarily have vast sums of cash to put away if they’re at the start of their career, but making a start investing this early can make an enormous difference to the rest of their life. If you reach this age and investments aren’t on your radar at all, it’s worth at least investigating what it has to offer.

Age 27: When Lifetime ISAs are most frequently used for property purchases

This is the most common age to use an AJ Bell Lifetime ISA to buy a property (measured as people making penalty-free withdrawals). Given that, overall, the average age to buy a first property is 34 in the UK, there’s a decent chance the government bonus has played a vital role in helping people build the deposits they need to get onto the property ladder.

You can pay up to £4,000 a year into a LISA and the government will top it up by 25%. The LISA will eventually be replaced by a new scheme for first-time buyers, but the date of the replacement, and the size of the government top up on the new scheme haven’t been confirmed. Meanwhile, the government has emphasised anyone opening a LISA before it’s replaced will be able to pay into it and get the bonus as usual for as long as they want, so there’s still enormous benefit in taking advantage of the LISA. For anyone under the age of 27, it may be worth getting started at a younger age, while you still can.

Age 33: Most likely age to make contributions

ISA customers who are age 33 have the highest percentage making an ISA contribution than any other age group on the platform. Some people will be on higher incomes or have made investment a key priority early in life, so will have been making the most of their ISAs for years. However, others will have waited until they were on a firmer financial footing before they made a start.

If you haven’t started investing, it’s a decent time to take stock. You may have other pressing priorities, or a gap in income which means now isn’t the time for you. Otherwise, this may well be an opportunity to start your investment journey.

Age 39: Most likely to open a Lifetime ISA

This is the oldest you can be when you open a Lifetime ISA, although once it’s open, you can keep paying into it until the age of 50. It’s also the age when people are most likely to open an AJ Bell LISA. The rush at 39 might be from some people keeping their options open, just in case they want to use a LISA later.

However, there’s more to it than that, because this is the age when people are most likely to start regular payments into an AJ Bell LISA too. It’s a flexible option for retirement savings, especially for basic rate taxpayers who work for themselves or who have already taken advantage of any employer contributions to their pension. It can also be helpful for anyone who has maxed out their pension contributions. If you want to take advantage of the LISA, it’s worth doing so sooner rather than later, while you still can.

Age 56: Most likely to max out their Stocks and shares ISA

Age 56 is the most common age to max out an AJ Bell Stocks and shares ISA.** One key driver is likely to be from people who have taken the tax-free cash from a pension, who want to keep it invested tax-efficiently.

If you want investments to grow within a tax-efficient environment, then there’s no need to take the cash at 55, because a pension is a great home for your money. By leaving your cash where it is, you also give the pot chance to grow, so you can eventually withdraw a bigger sum.

However, some people have taken tax-free cash because of a lack of reassurance from the government that they’re not going to tinker with the rules. While this is a decision which should be carefully thought through, if you’re going to do this, then a Stocks and shares ISA is a sensible home for your money.

The fact this is a key time for maxing out is also partly down to the fact many people will be empty nesters. Their offspring may have moved out or started working and contributing to the household, so they may have more money to work with and more opportunities to save. It means they can concentrate on building as much for retirement as they can, as soon as they can, in a mixture of pensions and ISAs.

If you’ve reached the empty nest period, it’s worth using a pensions calculator and factoring in additional savings and investments. If you have a shortfall, you can consider whether you can afford to put more aside for the future, to make up for lost time.

Age 63: Average age of a SIPP millionaire

This is the average age of AJ Bell SIPP millionaires, but if you haven’t quite got there, there’s no need to panic. It was always bound to be the age when people have built as much as possible in their pension and start spending it down. However, it’s a handy reminder that a commitment to pension investing from an early age, sticking with it whenever possible, and investing strategically, can help build a really substantial pot for the kind of retirement you always wanted.

Age 70: Average age of an ISA millionaire

This is the most common age of AJ Bell ISA millionaires. This isn’t going to be a target for everyone, but it’s a great demonstration of the power of compounding over time. By investing consistently over the decades, ISA millionaires haven’t had to take enormous risks or trade on a daily basis. They’re evidence of how successful a ‘get rich slow’ plan can be.

*Based on existing customers on the AJ Bell platform, as of 29 June 2026 **Refers to tax years since 2017/18, when the ISA allowance has been set at £20,000

The SNOWBALL currently earns income of 11k per year.

If you re-invest the dividends at a blended yield of 7% it will double every ten years.

So in twenty years, from now, your snowball should be yielding 44% per year. Better if Mr. Market allows you to re-invest at a higher yield as you can shorten the journey. You may not be a millionaire but you should be able to spend like one. GL

How can I learn the secrets of the passive income millionaires?

Story by Alan Oscroft

• 8mo

I’ve been doing a bit of research on the habits of successful passive income investors, and I came across a bit of a surprise.

They all seem to name dividend stocks as a major part of their investment portfolios — though that’s not the surprising part. No, what I hadn’t expected was to find a large number of them recommending real estate.

Yes, real estate has been profitable for a number of people. But I had a very shaky venture into it. And it has a fair few drawbacks for individual investors.

Not really passive

One is that many of us won’t have the capital to go for, say, rental properties. It’s not the kind of thing we can get started with just a few hundred pounds, like we can with a Stocks and Shares ISA.

It’s not entirely passive either. Finding tenants, collecting rent consistently, and maintenance all take time and effort. And the latter can sometimes prove very costly if you’re unlucky.

But there’s a way we can get into real estate without facing those major hurdles. And that’s to consider buying real estate investment trusts (REITs). They’re investment companies that put their money into various kinds of properties, and they do all the management. All we have to do is buy shares in them, just as we do with shares in general.

Healthy property

I like Primary Health Properties (LSE: PHP), which invests in GP surgeries, pharmacies, dental clinics. Importantly, they’re mostly rented to the NHS on long-term leases.

Having the UK government as its main customer provides some stability and predictability. But it hasn’t made the trust immune to weak property values in recent times. Over the past five years, the PHP share price has fallen 35%.

Higher interest rates are a burden, especially with debt on the books. At the end of the first half this year, net debt reached £1,367m, up from £1,323m in December 2024. There doesn’t seem to be any liquidity problem, but it could keep the shares down for longer.

Big dividends

On the bright side, a lower share price means a bigger dividend yield. Right now, we’re looking at a forecast 7.3%. And analysts are forecasting rises between now and 2027. We could have long-term capital appreciation too — especially when interest rates fall.

Is Primary Health one to consider for long-term passive income? Even in the current tough real estate market, I think it has to be, especially while the share price is low.

There are plenty of other REITs to choose from, addressing different sectors of the property market.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

Millionaire style

Quite a few millionaire investors also invest for deferred income. That is, they aim for total returns — capital and dividends — and plan to convert it to income later.

So how do we emulate the millionaire approach to passive income? If we focus mainly on dividend shares, include a REIT or two in our portfolio, and look for long-term growth opportunities too — we could get pretty close. And we don’t have to be millionaires to start.