Unsurprisingly TENT has moved from the trending up portfolio

to the trending down portfolio.

As always best to DYOR before making any trading decisions.

Investment Trust Dividends

Unsurprisingly TENT has moved from the trending up portfolio

to the trending down portfolio.

As always best to DYOR before making any trading decisions.

Posted on | By Bruce Packard

Bruce remembers a metaphor from the founder of the Georgian Stock Exchange and wonders how it might apply to Chinese financial markets.

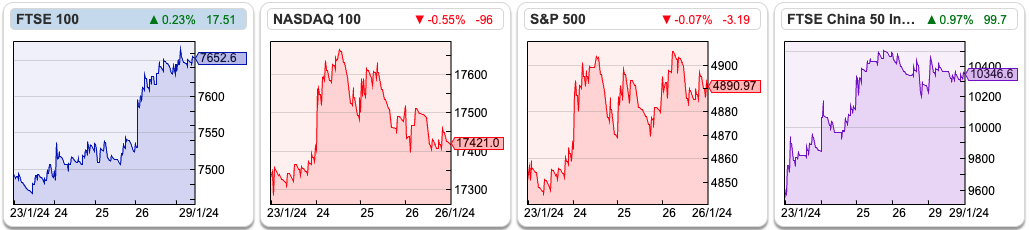

The FTSE 100 was up +2.2% to 7653 last week. The Nasdaq100 and S&P500 rose +2.4% and 1.1%. Brent Crude was up +4% in the last 5 days, most of which was on Monday morning. Chinese stockmarkets have bounced with the FTSE China 50 up +8.3% and the Hang Seng +7.5%.

The FT has reported that the Chinese authorities have tried to halt the sell-off in domestic equities. For instance, institutional investors have been told not to sell equities and short selling has been curbed. That might explain the short-term bounce but the FTSE China 50 is still down -31% in the last 12 months. ETFs tracking US and Japanese markets are becoming increasingly popular among Chinese retail investors, such that mutual funds were hitting limits that were designed to protect capital controls. The Chinese Yuan (CNY on Sharepad) is linked to the US dollar – but allowed to fluctuate around a narrow band. If the CNY continues to weaken, that could also be bad news for commodities and mining shares.

Many years ago I met the founder of the Georgian Stock Exchange, a chap called Gogi Loladze. He cut a dashing figure and was something of a capitalist philosopher, in the style of George Soros. Autocratic leaders, he said, craft their own narratives, and prevent any data that contradict their stories from circulating. However, these autocrats feared financial markets, because liquidity requires buyers and sellers to trade on good (that is, not unfair) information. The financial markets are like a barometer, it tells you what the air pressure is, and if a storm is blowing in, the meteorological instrument will warn you. That’s in contrast to government statistics like GDP which can be manipulated by less scrupulous leaders.

Gogi was keen to develop the Georgian Stock Exchange because

i) it would provide an alternative source of capital in competition to the banking system

ii) it would strengthen Georgia institutionally, which at the time wanted to be the “Singapore of the Caucasus”

iii) it would make him rich.

Building any two-sided platform is hard and he couldn’t get to critical mass and benefit from network effects. The Georgian Stock Exchange still exists but is owned by the large banks, which are not keen to develop it for some of the same reasons above. As a generalisation bankers prefer “discretion” (also known as secrecy) to the circulation of financial information.

Since then it has struck me that Gogi’s insight from a former Soviet Union country could apply equally well to China, which is communist, and increasingly autocratic but has a huge stock market. The Chinese GDP figures were announced a couple of weeks ago and were in line with expectations at c. +5%. No one seems to have a convincing narrative on why Chinese equities are selling off, but I would be wary. Below is a chart showing the FTSE China 50 (XINO) has fallen for 3 consecutive years in a row.

Impact Healthcare REIT plc

(“Impact” or the “Company” or, together with its subsidiaries, the “Group”)

2023 UPDATE, DIVIDEND DECLARATION AND 2024 DIVIDEND TARGET

HIGHLIGHTS

Our tenants continue to improve their performance with higher care home occupancy and increased fees to residents as inflation peaked in the year. Our rent increases are largely capped at 4%, so this helps tenants’ rent cover, and makes our income more secure. Boosted by an acquisition, our total rent roll grew strongly and this has flowed through to both earnings and dividend growth.

· 13.2% increase in contracted rent to £48.8 million for the 2023 year (+£5.7 million). Rental growth was driven by inflation-linked rent reviews (capped at 4%) plus a significant acquisition.

· 2.2x tenant rent cover(1) in Q3, up from 1.9x in the same quarter the previous year. This is the strongest quarterly tenant performance since the Company’s inception in 2017.

· 20.8 years weighted average unexpired lease, up from 19.7 years the previous year.

· Delivered a 3.5% increase in dividends per share in 2023 with a Q4 dividend of 1.6925 pence in line with our target of 6.77 pence per share for the year to 31 December 2023.

· 2.7% increase in dividend target to 6.95p for the 2024 year.

PORTFOLIO TRADING UPDATE

· Stronger tenant rent cover is driven by several factors: improving room occupancy; growth in average weekly fees charged by tenants; and rent increases largely being capped at 4%.

· The Group has received 100% of rent payments due (excluding the ex-Silverline homes) for the quarter to 31 December 2023 .

· Tenants maintained their profit recovery in Q4 and, based on the 88% of the Company’s portfolio that has reported so far, we estimate that the full year 2023 rent cover rose to 2.0x, up 0.2x compared to the full year 2022 of 1.8x.

· Occupancy at 31 December 2023 was 88.2%, up from 87.4% at 31 December 2022.

· The average weekly fees the Group’s tenants charge for the care they provide grew by c.12% in the 12 months to 31 December 2023.

· The £5.7 million growth in contracted rent was due to;

o £3.9 million from the acquisition of a portfolio of six homes near Shrewsbury leased to Welford, in January 2023.

o £1.6 million from 119 rent reviews in the year at an average increase of 4.1%.

o £0.3 million from rentalised capital expenditure with the largest projects being at Mavern and Yew Tree.

o Less £0.2 million from the disposal of one home.

· The former Silverline portfolio of seven homes continues to show improved performance under the management of Melrose, an affiliate of the Minster Group

o Melrose has undertaken a significant amount of work in a relatively short space of time including: measures to stabilise staff teams and to reduce use of agency staff; settling outstanding invoices with suppliers; renegotiating utility contracts; and focusing on improving processes and the care environment for both staff and residents.

o The portfolio of four homes in Scotland has an average occupancy of 88% and is now cashflow positive. Negotiations are well advanced to transfer these homes back to rent generating operational leases.

o The portfolio of three homes in Bradford is expected to be cashflow positive by the end of first quarter of 2024 with discussions underway on a new management proposal.

· At 31 December 2023, our portfolio comprised 140 healthcare properties, of which:

o 138 are care homes managed by 13 tenants on fixed-term leases with an average WAULT of 20.8 years (no break clauses), subject to annual upward-only Retail Price Index-linked rent reviews (with a floor and cap at 2% p.a. and 4% p.a., respectively on 117 leases, and 1% p.a. and 5% p.a. on 21 leases).

o In addition, the Group owns two healthcare facilities leased to the NHS with an annual CPI uplift (uncapped).

o In total, the Group had 14 tenants across its Portfolio.

FINANCING

· As at 31 December 2023 the Group’s drawn debt was £184.8 million:

o 95% hedged through a combination of fixed debt (£75 million at 3.0%) and SONIA interest rate caps (£50 million at 3% and £50 million at 4%).

o EPRA LTV of 27.7% based on 30 September 2023 balance sheet information.

o The current average cost of drawn debt, including hedging and fixed rate borrowings, is 4.56%.

DIVIDEND DECLARATION AND 2024 DIVIDEND TARGET

· The Board has today declared the Company’s fourth interim dividend for the year ended 31 December 2023 of 1.6925 pence per ordinary share, payable on 23rd February 2024 to shareholders on the register on 9th February 2024. The ex-dividend date will be 8th February 2024. This dividend will be paid as a Property Income Distribution (“PID”).

o This is consistent with the prior three quarters dividends and delivers on the Company’s annual dividend target of 6.77 pence per share for the year ended 31 December 2023. This is in line with the Company’s dividend policy, which seeks to maintain a progressive dividend that is covered by its adjusted earnings.

· The target dividend for the year to 31 December 2024 is 6.95 pence per share, a 0.18 pence increase from the prior period.

· The Company expects to report its full accounts for the year to 31 December 2023, which will include an updated valuation of the portfolio, in late March 2024.

Thursday 1 February

AEW UK REIT PLC ex-dividend payment date

Albion Enterprise VCT PLC ex-dividend payment date

Blackstone Loan Financing Ltd ex-dividend payment date

Capital Gearing Trust PLC ex-dividend payment date

CC Japan Income & Growth Trust PLC ex-dividend payment date

Dunedin Income Growth Investment Trust PLC ex-dividend payment date

Ecofin Global Utilities & Infrastructure Trust PLC ex-dividend payment date

Edinburgh Investment Trust PLC ex-dividend payment date

Henderson International Income Trust PLC ex-dividend payment date

JPMorgan Emerging Europe Middle East & Africa Securities PLC ex-dividend payment date

JPMorgan Global Core Real Assets Ltd ex-dividend payment date

JPMorgan Mid Capital Investment Trust PLC ex-dividend payment date

JPMorgan UK Smaller Cos Investment Trust PLC ex-dividend payment date

M&G Credit Income Investment Trust PLC ex-dividend payment date

Marwyn Value Investors PLC ex-dividend payment date

Polar Capital Global Financials Trust PLC ex-dividend payment date

Polar Capital Global Healthcare Trust PLC ex-dividend payment date

Schroder Oriental Income Fund Ltd ex-dividend payment date

Starwood European Real Estate Finance Ltd ex-dividend payment date

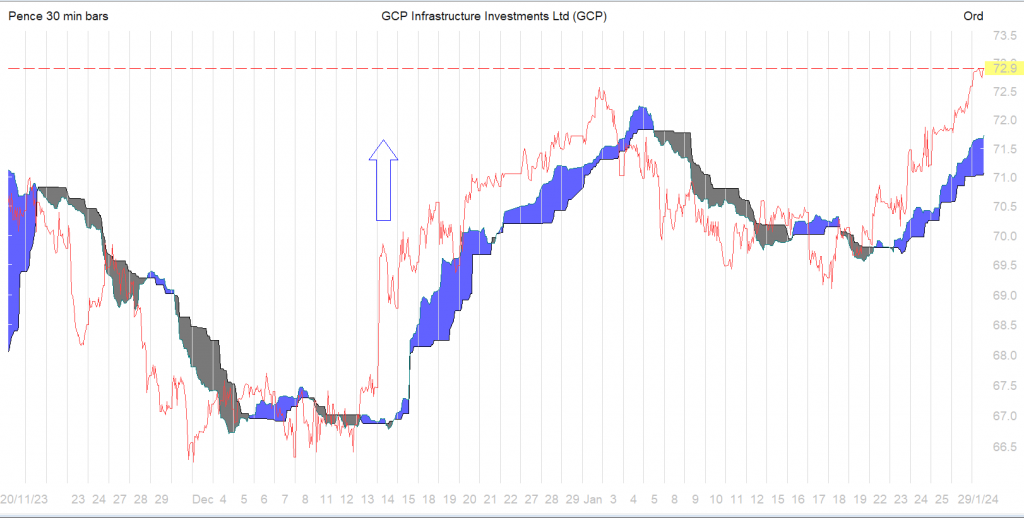

Could u have made a profit trading the GCP news.

Yes, but patience needed and better to have traded.

CT global have two Portfolios CMPG and CMPGI

The trust of interest is CMPGI as it pays a dividend.

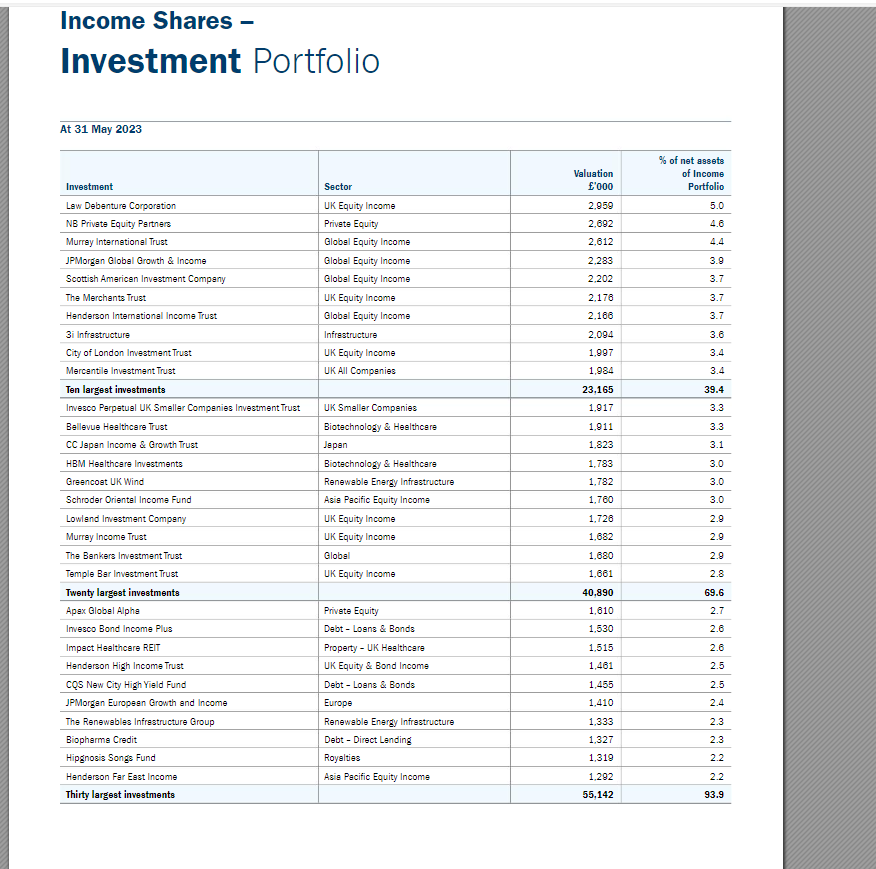

ACTIVITY BREAKDOWN

Top 10 Holdings

Name Holdings

Law Debenture Corp (The) PLC 4.7%

NB Private Equity Partners Class A Ord 4.6%

JPMorgan Global Growth & Income PLC 3.9%

Murray International Ord 3.9%

3i Infrastructure Ord 3.5%

Greencoat UK Wind 3.4%

Mercantile Ord 3.4%

Scottish American Ord 3.4%

Merchants Trust Ord 3.4%

Henderson International Income Ord 3.2%

U would have a holding in each of the above.

Dividend

Income Shares – Financial Highlights and Performance Summary for the Six Months

· Dividend yield of 6.5% at 30 November 2023, compared to the yield on the FTSE All-Share Index of 4.0%. Dividends are paid quarterly.

· Net asset value total return per Income share of -2.9% for the six months, underperforming the total return of the FTSE All-Share Index of +1.6% by -4.5% points.

Revenue and Dividends

The Company’s net revenue return for the six months was £2.12 million which is equivalent to 4.19p per Income share (compared to 4.01p per Income share for the corresponding period in 2022). Income shareholders are entitled to all the dividends paid by the Company. The second half of the financial year will see the impact of the removal of dividends by Digital 9 Infrastructure and Hipgnosis Songs Fund referred to above. However, these will not impact the Board’s dividend intentions for the financial year as the Company enjoys significant distributable reserves that can be used to overcome any temporary or extraordinary revenue shortfalls.

As I referenced in the 31 May 2023 Annual Report and Financial Statements, in the absence of unforeseen circumstances, it was (and it remains) the Board’s intention to pay four quarterly interim dividends, each of at least 1.80p per Income share so that the aggregate dividends for the financial year to 31 May 2024 will be at least 7.20p per Income share (2023: 7.20p per Income share).

To date, a first and second interim dividend in respect of the year to 31 May 2024 have been announced and paid, each at a rate of 1.80p per Income share (1.67p per Income share in the corresponding periods in the year to 31 May 2023).

The minimum intended total dividend for the financial year of 7.20p per Income share represents a yield on the Income share price at 30 November 2023 of 6.5% which was materially higher than the yield of 4.0% on the FTSE All-Share Index at the same date.

The Income Portfolio was particularly affected by the adverse environment for investment companies in the alternatives sub-sector and this was a key factor in the portfolio lagging the benchmark. The best performers included CC Japan Income & Growth Trust which had a 9% rise in its share price. Although the Tokyo market performed well, much of the rise was diluted for UK investors due to a weakening of the yen relative to sterling; however, the value orientated style of the manager helped the trust to outperform. Private equity trust NB Private Equity Partners has been a long-term outperformer for the Income Portfolio, and this continued with a 10% rise in its share price. Another consistent outperformer has been JPMorgan Global Growth & Income which continued to do well with a 8% rise in its share price. The main detractors were Digital 9 Infrastructure with a 48% fall in the share price. This was a disappointment as the trust has some valuable assets, but too much debt led to a removal of the dividend and was behind the share price decline. Another high profile detractor was Hipgnosis Songs Fund whose share price fell by 16%, at least in part due to it also removing its dividend, though in addition there have been governance, accounting and debt level concerns too. Impact Healthcare REIT, a specialist healthcare property REIT, experienced a 16% fall in its share price. This was a case of higher interest rates being reflected in a modest decline in the net asset value which caused the shares to move to a wider discount. Encouragingly the dividend was raised by 3.5%.

Positive

If the Trust buys a clunker such as SONG it’s less detrimental in a bigger

portfolio.

GCP Infrastructure Investments Limited

Company update, net asset value(s) and Dividend Declaration

Net Asset Value

GCP Infra announces that at close of business on 31 December 2023, the unaudited net asset value per ordinary share of the Company was 109.84 pence (30 September 2023: 109.79 pence), an increase of 0.05 pence per ordinary share. The net asset value takes into account cash, other assets, accrued liabilities and expenses and leverage of the Company attributable to the ordinary share class.

The primary driver of the Company’s NAV movement in the quarter was the updated OBR inflation forecast, following the Autumn Statement in November 2023, that contributed c. 1.0 pence per ordinary share. This was offset by further reductions in forecast electricity prices, primarily decreases in short-term power prices, decreasing forecast cash distributions to the Company from certain renewable energy investments. This power price volatility is partially offset by the positive performance of the Company’s hedging arrangements. The overall net power price movements negatively contributed c. 0.7 pence per ordinary share.

Increases to discount rates led to a reduction of c. 0.5 pence per ordinary share, resulting in the weighted average discount rate used by the Company to value its investment portfolio of 7.76% at 31 December 2023. This was offset by increased actual cash distributions to the Company from its renewable energy investments that contributed c. 0.1 pence per ordinary share. A summary of the constituent movements in the quarterly net asset value per ordinary share is shown below.

| Net asset value analysis (pence per share) | NAV | Change |

| 30 September 2023 NAV | 109.79 | |

| November 2023 OBR inflation forecast | 0.98 | |

| Q4 2023 power price forecast (inclusive of hedging value changes) | (0.72) | |

| Discount rate increases | (0.48) | |

| Actual generation across the renewable energy portfolio | 0.08 | |

| Share buyback accretion | 0.18 | |

| Other valuation changes | 0.01 | |

| 31 December 2023 NAV | 109.84 |

Portfolio

Notwithstanding the lower electricity price forecasts, the portfolio continues to perform materially in line with the Company’s expectations. The Company’s mature, diverse and operational portfolio provides defensive access to income against a backdrop of market volatility and uncertainty. It is the view of the Company that the long-term and structural demand for infrastructure, and particularly infrastructure debt, offers investors an attractive exposure to an asset class whose performance is non-correlated to wider markets and benefits from long-term and partially inflation protected income. Further portfolio information is available at: http://www.graviscapital.com/funds/gcp-infra/literature, including a line-by-line breakdown of the investment portfolio and underlying assets that will be updated by the Company periodically.

Buybacks

On 14 March 2023 the Company announced a proactive programme of share buybacks in response to the persistent discount at which the Company’s share price is trading relative to the published net asset value. The Company remains committed to pursue buyback opportunities in line with the capital allocation strategy that has been set out in the annual report, and to benefit from the investment opportunity that the Company’s shares offer at the current price. At 31 December 2023, the Company had bought back 16,985,019 shares.

Dividend

GCP Infra is pleased to announce a dividend of 1.75 pence per ordinary share, for the period from 1 October 2023 to 31 December 2023. The dividend will be paid on 8 March 2024 to holders of ordinary shares recorded on the register as at the close of business on 9 February 2024

EJF Investments Ltd

(“EJFI” or the “Company”)

Dividend Declaration

The Directors of EJFI are pleased to announce that they have declared a dividend of 2.675 pence per share in respect of the quarter ended 31 December 2023.

The dividend will be payable to shareholders on the register as at close of business on 2 February 2024, and the corresponding ex-dividend date will be 1 February 2024. Payment will be made on or about 29 February 2024. As previously notified, shareholders are able to receive their EJFI dividends in USD rather than GBP if they elect to do so. Any shareholder who would like to receive their dividend payments in USD and/or would prefer to receive a wire in lieu of a check and has not already submitted the election form should contact Computershare, the Company’s Registrar, by 5 February 2024.

Real Estate Investors Plc

TRADING & STRATEGIC UPDATE

Real Estate Investors Plc (AIM: RLE), the UK’s only Midlands-focused Real Estate Investment Trust (REIT) with a portfolio of commercial property across all sectors, is pleased to provide the following update as at 31 December 2023:

DISPOSALS – ACCELERATED SALES PROGRAMME

· Sales in 2023 of £17.97 million at an aggregate uplift of 2.93% (pre-costs) to 31 December 2022 book value

· Further pipeline sales in legals, with focus on reducing portfolio debt further

DEBT REDUCTION & REFINANCING

· Receipts from sales during 2023 have been used to repay £17.1 million of debt

· Total drawn debt reduced to £54.3 million (FY 2022: £71.4 million / FY 2021: £89.4 million)

· Aviva facility fully paid – lenders are now National Westminster Bank Plc, Barclays plc and Lloyds Bank plc

· Average cost of debt maintained at 3.7% (H1 2023: 3.7%)

· Discussions well advanced with lenders to renew facilities due to expire in May, June, and December 2024

PORTFOLIO SUMMARY

· Occupancy levels at 83.03% (FY 2022: 84.54%)

· Contracted rental income of £10.9 million p.a. (FY 2022: £12.6 million p.a.)

· Major letting contracted to complete in April 2024. This will improve existing occupancy to 85.91% and boost contracted rental income to £11.2 million p.a. (subject to sales and other lease activity)

· Portfolio WAULT improved to 5.24 years to break and 6.01 years to expiry (FY 2022: 4.98 years & 6.29 years)

· Continued robust rent collection levels with overall rent collection for 2023 of 99.82%

STRATEGIC UPDATE

The Board has previously stated an intention to accelerate its sales programme, through the sale of assets either on an individual or collective basis, on terms that represent value for shareholders. Given the ongoing substantial discount between the share price and NAV, combined with a lack of liquidity in its shares, the Board has concluded that it will conduct an orderly strategic sale of the Company’s portfolio over the next 3 years with the objective of maximising the return of capital to shareholders (the “Disposal Strategy”). To achieve this outcome, assets will be sold individually, as smaller portfolios or as a whole portfolio sale, with the initial priority to repay the Company’s debt.

Over the last 3 years, the Company has sold £56.4 million of assets, on an aggregate basis, at or above book value, and significantly reduced drawn debt from £101 million to £54.3 million (as at 31 December 2023).

The ongoing pace of the disposals will depend on market conditions however, it is the Company’s intention to secure disposals at book value or higher, maximising returns to shareholders.

To support the Disposal Strategy and the return of capital to shareholders, the Company is implementing a new Shorter Term Incentive Plan (“STIP”). The STIP will replace the existing Long Term Incentive Plan (“LTIP”), help to retain Paul Bassi, Chief Executive Officer and Marcus Daly, Finance Director (the “Executives”), and the wider management team and incentivise them to achieve an orderly and timely disposal of the Company’s assets to maximise the capital return to shareholders.

In addition, the Company’s Remuneration Committee has approved changes to the Executives’ remuneration to align the policy with the wider Company strategy.

REVISED REMUNERATION POLICY (EFFECTIVE 1 JANUARY 2024)

1. Basic salary: Executive salaries to be reduced by one third. New salaries – Paul Bassi, CEO reduced to £367k (previously £550k) and Marcus Daly, CFO reduced to £229k (previously £344k) amounting to a cost saving of approximately £330k (including National Insurance contributions). In addition, Non-Executive Directors’ fees also to be reduced by one third

2. Annual discretionary bonus: The Executives’ bonus is reduced from up to a maximum of 100% of basic salary to a maximum of 50% of the new reduced basic salary

3. Executives’ service contracts: If contracts are to be paid up following a corporate transaction or equivalent, then compensation under the Executives’ service contracts reverts to old salary levels

4. LTIP Awards: The Executives’ entitlement to awards under the Company’s existing LTIP scheme have been amended as follows:

· Unvested awards granted re: FY2020 – to be reduced by one third

· Unvested awards granted re: FY2021 – to be reduced by two thirds

· Unvested awards granted re: FY2022 – to be cancelled

· No further awards under the LTIP going forward

· The approximate value in the reduction in the awards equates to approximately 4 million Ordinary Shares, which at a share price of 30p equates to £1.2 million

5. Shorter Term Incentive Plan (“STIP”): To compensate the Executives (albeit not to the same extent) for the retrospective reduction in LTIPs in relation to FY2020 and FY2021, the cancelling of awards relating to FY2022 and no further issuing of awards under the LTIP in relation to FY2023 or going forward, the Executives will be entitled to participate in the STIP.

SHORTER TERM INCENTIVE PLAN

The STIP is being implemented to compensate the Executives for the retrospective reduction in awards and cancellation of future awards under the LTIP.

1. Under the STIP, the participants will receive a proportion of a notional cash pool (the “Pool”) which will be created from the excess (“Gain”) of Total Shareholder Return (“TSR”) over the market value of the Company as at 31 December 2023.

2. TSR is cash per Ordinary Share returned to shareholders, excluding ordinary dividends.

3. To ensure the timely disposal of assets, the Gain attributable to the Pool will be reduced over time.

4. If the Company’s sell down strategy is completed in 2024 then the Pool is calculated as 10% of the Gain. If the strategy is completed in 2025 the Pool reduces to 7.5% and if by 2026, the Pool reduces to 5%.

5. Of the Pool, a minimum figure of £410k is ringfenced for the management team (excluding the Executives) equivalent to a bonus of 100% salary.

6. The STIP will pay out as soon as reasonably practicable after the earliest of (1) the sale of all the assets, (2) a takeover of the Company or (3) when the Remuneration Committee determine that a sufficient proportion of the assets have been sold and that the STIP has achieved its original purpose.

In determining the revised remuneration policy and STIP, the Company’s Remuneration Committee has consulted with REI’s largest institutional shareholders.

NOTICE OF FINAL RESULTS

The Company will release its results for the year ended 31 December 2023 on 26 March 2024.

PAUL BASSI, CHIEF EXECUTIVE, COMMENTED:

“Against a backdrop of high interest rates and stubborn inflation, political instability and unrest in Ukraine and the Middle East, the REI portfolio remains stable, with robust rent collection levels. The portfolio is well managed and remains sheltered from wider economic pressures due to its diverse nature and lack of exposure to large office schemes and other challenging sectors.

Having finalised our strategic plan, our priority is to continue disposing of assets at or above book value, maximising returns to shareholders. During 2023, despite an inactive property market, we made sales of £17.97 million (predominantly to private investors) and receipts from these disposals were utilised to reduce debt by £17.1 million. We currently have a further healthy pipeline of sales in legals, which we anticipate to complete in H1 2024.

With the benefit of our unique market insight, we will continue to capitalise on ongoing buyer demand for our smaller lot sizes from private investors and special purchasers. We have identified other larger assets that are ready for disposal, some of which we will hold for income until corporate and institutional buyer demand returns. In the meantime, the business is operationally robust and we will continue intensively managing assets to maximise income and reduce vacancy levels, supporting our fully covered dividend.

Despite a strong year of sales to private investors and special purchasers, market sentiment remains weak and we anticipate valuation decline across the industry. This is due to the lowest level of transactions since the financial crisis of 2008, high interest rates and the political uncertainty in an election year. However, we are confident that our diversification will outperform market benchmarks.

The Board is committed to maximising shareholder returns, whilst remaining open to a corporate transaction that is in the best interest of the shareholders. In the meantime, it is the Board’s intention to continue paying a fully covered quarterly dividend payment, subject to the pace of disposals.”

© 2026 Passive Income Live

Theme by Anders Noren — Up ↑