Fear Just Hit “Extreme.” Here’s the Dividend Grower to Buy.

Brett Owens, Chief Investment Strategist

Updated: April 1, 2026

Half of individual investors think the stock market will be lower six months from now. That’s a level of bearishness that intrigues contrarians like us!

The weekly AAII Sentiment Survey reports 49.8% bears. The historical average is just 31%:

Most investors, at any given time, think the stock market is heading higher. And at any given time, they are likely to be right! We all know that over long time periods the path for the market is up.

However, it does so in fits and starts. Bull markets stroll the stairs on the way up but bear moves take the elevator lower. This is scary and tricks vanilla investors into “moving to cash” with the notion they can time the bottom and “buy back in” at the lows—or when “it’s safe again.” Ha!

This is generally a losing strategy because markets rebound so quickly off lows that the cash hoarders miss the best gains! Too bad for them but helpful for thoughtful investors like us who are not afraid to buy bargains when the near-term looks bleak. Because, well, that’s when the best deals are had!

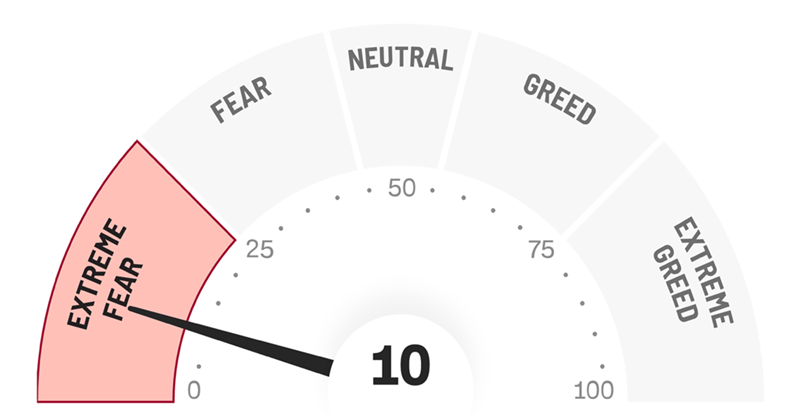

And oh boy, do things look bleak. The so-called pros are running too. CNN’s Fear and Greed Index—which mashes together seven market indicators into a single “mood ring” for Wall Street—just hit “Extreme Fear”:

Fund managers are hoarding cash at the fastest clip since March 2020. That was the COVID crash—and it turned out to be one of the best buying opportunities in a generation!

I’ve seen this movie before. We saw it again in late 2022, when everyone was convinced the Fed had broken the economy. And in April 2025, when the Fear and Greed Index hit single digits—and the S&P 500 ripped higher for the rest of the year!

Every single time, the investors who sold into fear looked back six months later and wished they hadn’t. So what should we dividend investors do instead? The opposite, of course. We should be buying dividend growers on sale.

The Dividend Magnet: Our Fear-Proof Strategy

I’ve spent over a decade developing what I call the “Dividend Magnet” strategy. The idea is simple but powerful: when a company raises its dividend year after year, its stock price follows the payout higher, like a magnet pulling iron filings.

It works in bull markets. It works in bear markets. And it works especially well when we buy during moments like now—when fear pushes stock prices down while the dividends keep marching higher.

Think about it. When a stock’s price drops but its dividend keeps growing, what happens to the yield? It goes up! We lock in a bigger income stream at a lower price. And then, when the fear passes (it always does), the dividend magnet pulls the stock price back up to where it belongs.

We contrarians love fear. Let me give you a real example. Aflac (AFL)—the supplemental insurance company with the duck commercials—is a textbook dividend magnet.

AFL has hiked its dividend for 43 consecutive years. Over the past decade, the payout has grown by an average of 11% per year. And AFL just hiked it 16% last year! The total increase over the past 10 years? A near-triple, 197% to be exact.

AFL’s Decade-Long Dividend Triple

And management doesn’t stop there. Over that same decade, Aflac’s buybacks have shrunk its share count by nearly 40%. So each remaining share commands a bigger slice of a growing profit pie. It doesn’t get more shareholder-friendly than this!

Here’s what I love about AFL in this fearful market: the stock trades around $108, down about 10% from its 52-week high. Vanilla investors see a falling stock and run. I see a dividend magnet on sale.

AFL yields about 2.2% today—not jaw-dropping at first glance. But remember, this isn’t a stagnant 2.2%. It’s a 2.2% that grows by double digits per year. Buy AFL today and that yield-on-cost balloons over time. (Investors who bought Aflac a decade ago now earn substantially more on their original investment. That’s the magic of accelerating dividends.)

Plus, AFL’s payout ratio is just 33%. That means the company pays out only a third of its earnings as dividends—leaving enormous room for future hikes. The dividend is about as safe as they come, backed by an A.M. Best A+ financial strength rating.

And here’s the kicker: Aflac is actually benefiting from AI. The company uses AI-powered systems to process insurance claims in minutes rather than weeks. Industry benchmarks show AI-driven fraud detection reduces suspicious payouts by 20% to 30%—and Aflac is deploying these tools aggressively. Faster claims, lower costs, happier customers—all flowing straight to the bottom line and fueling future dividend raises!

This is the kind of “boring” stock we contrarians love. Broader fear gives us a buying opportunity to get rich safely. And AFL is just one of several dividend growers on sale today. I’ve built an entire portfolio of dividend magnets in my Hidden Yields service—companies with accelerating payouts that pull their stock prices higher year after year.