TR over 1 year 25%, as the price rises the yield falls.

Yields 7.2%, so still a hold for the portfolio, maybe with a floor of 6% where reluctantly it might be sold.

Investment Trust Dividends

TR over 1 year 25%, as the price rises the yield falls.

Yields 7.2%, so still a hold for the portfolio, maybe with a floor of 6% where reluctantly it might be sold.

Zacks Equity Research

Wed, June 25

Strange but true: seniors fear death less than running out of money in retirement.

And unfortunately, even retirees who have built a nest egg have good reason to be concerned – with the traditional approaches to retirement planning, income may no longer cover expenses. That means retirees are dipping into principal to make ends meet, setting up a race against time between dwindling investment balances and longer lifespans.

In the past, investors going into retirement could invest in bonds and count on attractive yields to produce steady, reliable income streams to fund a predictable retirement. 10-year Treasury bond rates in the late 1990s hovered around 6.50%, whereas the current rate is much lower.

While this yield reduction may not seem drastic, it adds up: for a $1 million investment in 10-year Treasuries, the rate drop means a difference in yield of more than $1 million.

And lower bond yields aren’t the only potential problem seniors are facing. Today’s retirees aren’t feeling as secure as they once did about Social Security, either. Benefit checks will still be coming for the foreseeable future, but based on current estimates, Social Security funds will run out of money in 2035.

So what’s a retiree to do? You could cut your expenses to the bone, and take the risk that your Social Security checks don’t shrink. Or you could find an alternative investment that provides a steady, higher-rate income stream to replace dwindling bond yields.

As we see it, dividend-paying stocks from generally low-risk, top notch companies are a brilliant way to create steady and solid income streams to supplant low risk, low yielding Treasury and fixed-income alternatives.

Look for stocks that have paid steady, increasing dividends for years (or decades), and have not cut their dividends even during recessions.

Dear reader,

I looked at FGEN last November and a few readers asked me to look again given its annual results release for the year to 31/3/25.

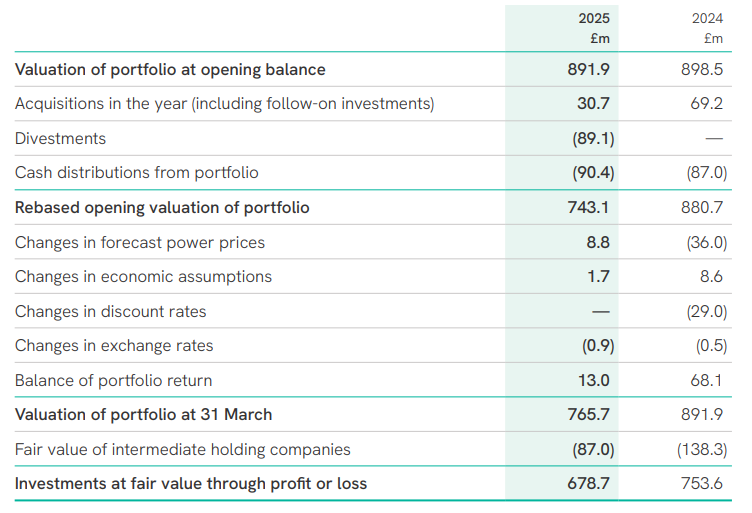

FGEN’s portfolio now comprises 40 assets across the UK and Europe, diversified across renewable energy generation (73% by value), sustainable resource management (17%), and other energy infrastructure (10%). Key holdings include the Cramlington biomass plant, the Rjukan aquaculture facility in Norway, and wind, solar, and anaerobic digestion projects in the UK.

FGEN’s net asset value (NAV) per share declined by 6.3% over the reporting period, from 113.6p to 106.5p. This was partly the write off off its investment in hydrogen platform HH2E – and otherwise good old discount rates.

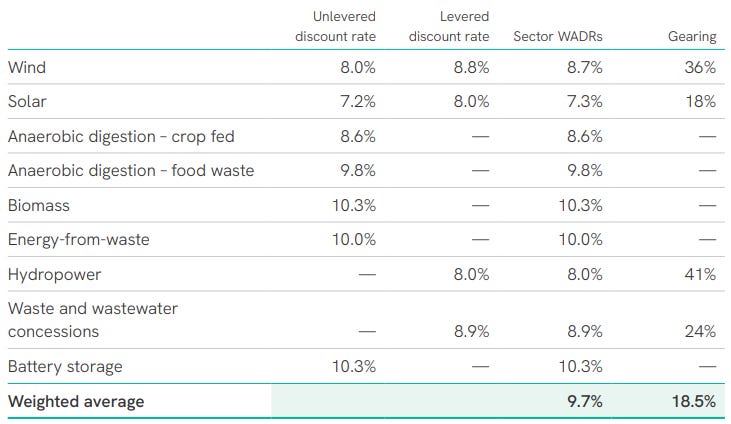

I wrote yesterday about how fellow IT SEIT is at a 9.6% discount rate. FGEN is at a slightly higher 9.7% rate. The rate appears very high even for comparable assets (e.g. Gore Street BESS are 7%-9% vs 10.3% here.

The discount rate is made up of the following rates:

An increase in the discount rate of 0.5% would result in a downward movement in the portfolio valuation of £17.2 million (2.7 pence per share) compared to an uplift in value of £18.0 million (2.8 pence per share) if discount rates were reduced by the same amount.

So compared to NESF’s 8% rate FGEN would gain £61.2m to be at 8% too.

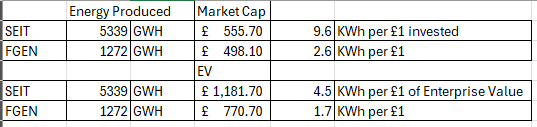

1.27 TWh is 50% more than NESF but still sits below SEIT.

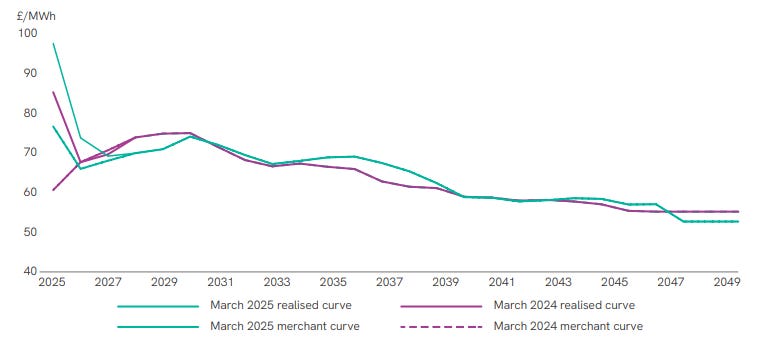

Power curves once again are, based on the forecasts of 3 experts due to be dropping away in the years ahead even though the 2024 power curve forecast for 2025 was well below the current 2025 rate (incorrect by about £15/MWh). If these experts can’t even forecast 1 year ahead accurately how much credence should you give to 5 years or 10 years?

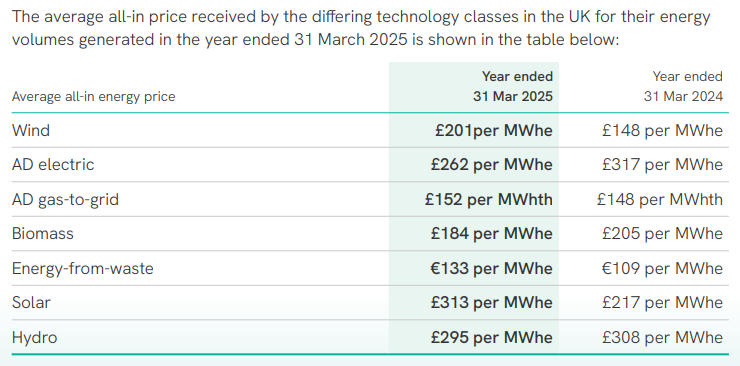

Of course the power curve also bears little resemblance to the energy prices FGEN quote in their investment manager’s report:

Now this is interesting since an FY25 EBITDA of £131.6m for FGEN compares very favourably to a SEIT’s EBITDA of just £86m. Favourably to the £678.7m NAV closing value.

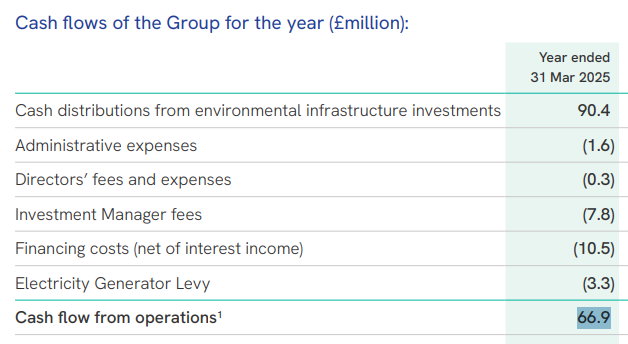

So how are cash distributions so different to EBITDA? £90.4m of what might be approximated to be free cash flow (and is much lower than SEIT’s) nets to £66.9m as what appears to be a better proxy to the “real” returns for FGEN.

It mirrors the £63.4m of interest and dividends that FGEN earned as below.

I suspect the answer to this riddle is the EBITDA was £131.6m and FGEN own half those portfolio companies. It’s pretty frustrating to not just be given facts in a consistent manner.

Of course the statutory result was a loss due to a £57.4m fair value loss. We are told this is due to a power price forecast contraction and future cash flows. Well you know what I think of that.

Judging by the 92% operational and 8% in construction there isn’t much still to complete, but a review of the actual assets under construction reveals a vast array of big ticket items (e.g. a 0.75GW interconnector). Again a riddle, but the answer must be FGEN is taking a minority ownership. Perhaps even just 2%-5%.

Of course a 2.1% dividend increase for FY26 to 7.96p per share and covered 1.32x by operating cashflow. FGEN has delivered consistent annual dividend growth over numerous years.

On top of dividends there were also NAV-accretive share buybacks and a £1.3m gain from asset disposals. The NAV total return was +0.6%. During the year, the company completed £88.6m of asset disposals (equivalent to approximately 10% of its portfolio), all at or above carrying value. The proceeds were used to repay floating rate debt and fund a £30m share buyback programme, of which £24.3m had been deployed by the end of March. Gearing was reduced to 28.7% from 31.2%, maintaining FGEN’s position among the least leveraged funds in the sector.

FGEN’s strategic review concluded a refocused strategy centred on proactive asset management and disciplined capital allocation would best serve shareholders. Quelle surprise.

FGEN say they will prioritise new investments in core environmental infrastructure sectors – including renewables, energy storage, and sustainable resource management – that offer long-term, stable, inflation-linked revenues. Investments in higher-risk growth assets will be limited. It intends to monetise existing positions in platforms such as the Glasshouse, Rjukan, and CNG Fuels when they reach maturity and can command premium valuations. The portfolio will instead focus on income-generative assets and value enhancement at operational sites.

Investment manager’s fees change from 1 October 2025, where the base management fee will be calculated on a blended metric of 50% NAV and 50% market capitalisation (capped at NAV), replacing the previous NAV-only basis.

I am trying not to say meh. Oops just said it.

FGEN has a 10% yield, and the share price is up from a 66p low to 80p a share but there’s still a 31% discount to NAV. The discount rate and the power price assumptions make that 106.5p very likely to be understated. There are various assets coming on line in FY26 too. FGEN have said they are going to stick to their knitting with inflation-linked returns.

I’m just not convinced that there’s any great upside here. The investment manager manages to say a lot and presents well but leaves me not feeling excited. I previously said that FGEN is “a decent way to earn solid dividends and where the margin of safety appears higher than the market perceives.” I still believe that that’s true. Even more so today.

So FGEN appears a trusty plodder but not an Arabian thoroughbred. What horse do you want in your portfolio?

Regards

The Oak Bloke

Disclaimers:

This is not advice – make your own investment decisions.

Micro cap and Nano cap holdings, even FTSE250 companies like SEIT, might have a higher risk and higher volatility than companies that are traditionally defined as “blue chip”

Stephen Wright thinks two FTSE 250 REITs looking to merge could be an interesting opportunity for investors looking for passive income to consider.

Posted by Stephen Wright

Published 25 June

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

After falling almost 5% in a day, Primary Health Properties (LSE:PHP) has slipped back to 99p. But the FTSE 250 real estate investment trust (REIT) has had some potentially big news.

It looks as though the firm has managed to hijack KKR’s takeover of fellow healthcare REIT Assura (LSE:AGR). And the result could be a very interesting stock for passive income investors.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

There has been a lot of interest in UK REITs over the last few months. As well as Assura, Care REIT, Warehouse REIT, and Urban Logistics REIT have all been attracting attention.

After a short bidding war, Assura announced it intended to accept a best-and-last offer of £1.7bn from a consortium led by US investment firm KKR. But it’s now switched courses.

Officially, the preferred offer from Primary Health Properties values the company at £1.8bn. There are, however, a couple of things to keep an eye on.

The deal involves merging the two companies to create a much bigger healthcare REIT. And Assura shareholders are set to receive the following (for each share they currently own):

The firm currently has a market value of £1.62bn – around 10% below the proposed takeover price. But the final value of the deal depends on what happens to the Primary Health Properties share price.

With that in mind, I’m not looking for a quick win based on the deal going through. But I am interested in the combined company as a potential long-term passive income opportunity.

In their current forms, Assura and Primary Health Properties are very similar businesses. Both make money by owning and leasing portfolios of healthcare properties – notably GP surgeries.

There’s a slight difference in terms of the balance of state (mostly NHS) and private tenants. But combining the two clearly offers some benefits of scale for shareholders.

The similarities between the two businesses mean they also have similar risk profiles. Both use their reliable income stream to operate with unusually high debt levels. Assura and Primary Health Properties both have net debt levels roughly equal to their entire market value. That’s something investors need to factor into their calculations.

Both stocks currently have dividend yields of around 7%. So even if the combined company has to issue shares to pay off some of its debt, investors might still hope for a good return.

An aging population and the UK government’s desire to use private healthcare to try and reduce NHS waiting times should both be benefits. As a result, I think this is an interesting opportunity.

I’ve owned shares in both Primary Health Properties and Assura in the past, but I’ve since sold both. Looking back, I think that was probably a mistake. The merger of the two companies could well be my chance to get back in. But I have a clear preference for which stock I prefer at this stage.

There’s still a risk the deal doesn’t go through. And in that situation, I expect both share prices to go back to where they were before the latest news. That means up (slightly) for Primary Health Properties and down (slightly) for Assura. So to cover that possibility, I think I prefer the former.

The Snowball has profits in

Assura of £2,925.00 and PHP £2,281.00, which now re-invested back into the Snowball will accelerate the planned timescale.

One to watch ?

Dr James Fox explores whether it would could be possible to generate enough dividend income to live comfortably and stop working.

Posted by Dr. James Fox

Published 30 May, 2023

The content of this article was relevant at the time of publishing. Circumstances change continuously and caution should therefore be exercised when relying upon any content contained within this article.

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.Read More

Like many investors, I receive dividend income from the stocks I own. In my case, dividend-paying stocks represent the core part of my portfolio. But just how much would I need to earn from dividends to live off this income alone? And would it be possible?

Let’s take a close look.

Well, I’d want to build a portfolio of dividend stocks that collectively pay me enough money to live from. Let’s say this is £30,000, but I appreciate this might not be possible in London.

Do you like the idea of dividend income?

The prospect of investing in a company just once, then sitting back and watching as it potentially pays a dividend out over and over?

And I’d want to be doing this within an ISA wrapper. That’s because any capital gains, dividends, or interest earned within the ISA portfolio is tax-free.

So, if I was earning £30,000 from dividends, I’d actually be taking home more money than someone on a £45,000 salary — including student loan repayments.

Of course, unless I picked specific stocks, I wouldn’t expect this income to be spread evenly across the year. At this moment, the majority of my portfolio’s income comes around April and May, shortly after the end of the financial year. So that’s something to bear in mind.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

Well, to earn £30,000, I’d need to have at least £375,000 invested in stocks. That’s because I believe the best dividend I can achieve is around 8%. This would involve investing in companies, like Legal & General, that don’t offer much in the way of share price gains.

But what if we don’t have £375,000? And let’s face it, the majority of us don’t.

Well, I’d need to build a portfolio over time. And I could do that using a compound returns strategy. This involves reinvesting my dividends and earning interest on my interest. It’s very much like a snowball effect.

Naturally, there are several key variables here. The starting figure, the yield I can achieve, and the amount of money I contribute from my salary every month.

If I started with £10,000 and stocks yielding 8%, in theory I could reach £375,000 in 19 years. But this would require me to contribute £400 a month and increased this contribution by 5% annually throughout those 19 years.

And by contributing £400 a month, I’d fall way under the maximum annual ISA contribution of £20,000.

Compound returns isn’t a perfect science, and as with any investment, I could lose money. But it’s certainly safer than investing in growth stocks.

Of course, the above is great in theory, but I’d need to pick the right stocks. I’m looking for stocks with strong dividend yields, but I also need to be wary. Big dividend yields can be a warning sign, and the dividend coverage ratio is a good place to start.

The prospect of investing in a company just once, then sitting back and watching as it potentially pays a dividend out over and over?

If you’re excited by the thought of regular passive income payments, as well as the potential for significant growth on your initial investment…

REGIONAL REIT Ltd.

(“Regional REIT”, the “Group” or the “Company”)

Lettings Update

Regional REIT (LSE: RGL), the regional property specialist, is pleased to announce that it has secured seven new lettings and eight lease renewals across its portfolio since the trading update on 15 May 2025. The fifteen transactions deliver a total annual rental income of over £1.6m and represent a 6.32% increase above estimated rental values, demonstrating the impact of the Group’s active asset management strategy.

Stephen Inglis, Head of ESR Europe LSPIM Ltd., Asset Manager commented:

“This letting activity underscores the effectiveness of our capital expenditure strategy, securing rents above ERV. The lease renewals also announced today reflect the quality of our existing properties and strong relationships with our occupiers.

As demand continues to grow for sustainable, well-located and high-quality regional office space, and given the diminishing supply, Regional REIT is well-positioned to harness this momentum and deliver lasting value for shareholders, including the distribution of our attractive and fully covered dividend.”

The Snowball expects to earn income of 10k this financial year, which will be three years ahead of the written plan.

The fcast for next year will be £10,500.00 and the target yet to be decided.

I bought shares in this FTSE 100 financial giant in 2020 based on high passive income potential and major share price undervaluation. I’m very happy I did.

Posted by Simon Watkins

Published 24 June

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

I bought £10,000 of Legal & General (LSE: LGEN) shares in June 2020, principally for their passive income potential.

This is money made with little effort, most appositely in my view with dividends paid by shares. The only real work on my part is selecting the stocks in the first place and then monitoring their progress.

I had already built up a stake in the financial services giant over previous years, in increments of £5,000. However, given how well it had performed – and its forecast earnings at that point – I decided to double my holding.

After all, earnings are the key driver for any firm’s share price and dividends over time.

Looking back I am very happy with my decision.

In Legal General’s case, my £10,000 bought me 4,545 shares at the 24 June 2020 opening price of £2.20.

Since then the firm has paid a total of 97.09p in dividends. This has given me £4,413 in dividends – a return of 44% over the five years.

In addition, I have made a profit on a rise in the share price too. This was not altogether unexpected, as I only buy stocks that look significantly undervalued to me.

The primary aim of this in my passive stocks is to minimise the risk that I lose dividend gains through share price losses. However, it also conversely increases the chance that I may make a profit on the share price as well.

This has been the case with Legal & General, which now trades at £2.52. It gives me an additional profit of £1,454 on the share price.

This, added to the dividends made, means a total profit of £5,867 over the five-year period – a near-60% return.

A risk for Legal & General is the intense competition in its sector, which may squeeze its margins.

That said, consensus analysts’ estimates are that its earnings will grow a spectacular 27.9% a year to end-2027.

The forecasts are that the firm’s dividends will rise to 21.8p this year, 22.3p next year, and 22.6p in 2027. This would generate respective yields on the current share price of 8.7%, 8.9%, and 9%. The dividend for 2024 was 21.36p, giving the current yield of 8.5%.

If the shares averaged this 8.5% yield over the next 10 years, then my £10,000 would make £13,326 in dividends. And if it averaged the same over 20 years I would make £44,412.

This is based on me reinvesting the dividends into the stock – known as ‘compounding’. But I have to take into account that none of this is guaranteed.

Legal & General shares continue to look extremely undervalued to me.

More specifically, a discounted cash flow analysis shows they are 56%undervalued at their current £2.52.

Therefore, their fair value is technically £5.73.

Consequently, given its strong earnings prospects – and what this should mean for its share price and dividends — I will buy more of the shares very soon.

Dividend

Our dividend of 6.875p per Ordinary Share remains cash covered at 1.00x (2024: 1.06x). The level of cash cover is lower than the previous year, due in part to “cash drag”, referring to cash held over the year reducing the Fund’s level of investment income and less capitalised interest received.

The repayment of capitalised interest is an essential component of the Company’s cash cover. However, given that its timing is tied to the eventual repayment or sale of the Company’s assets, it is unevenly distributed over the life of the Company, which can result in fluctuations in the dividend cash cover. This also affected this year’s cash cover.

In addition, the share buybacks, while being accretive to NAV, free up less cash than cash generated by extending new loans.

The Board has also considered the ratio of dividends per share to earnings per share, which is 137% (2024: 105%). While a ratio of more than 100% is undesirable, it does not imply that the dividend is unsustainable, as the ratio is driven in part by unrealised mark-to-market adjustments in the carrying value of performing loans – this type of price adjustment does not affect the long-term income-generating ability of those loans. Moreover, the ratio does not reflect the NAV benefits of the share buyback, which creates capital value in an economic sense, but this is not captured in earnings per share.

Paying a stable, attractive and covered dividend is an important part of the Company’s value proposition to investors The Board believes that the current level can and will be maintained. However, the Board is mindful of the increased risk environment and the fact that interest rates are forecast to fall, and so will keep the level of dividend under review to ensure that it remains affordable and sustainable.

© 2026 Passive Income Live

Theme by Anders Noren — Up ↑