A simple re-invest the dividend strategy back into the share, using good ole hindsight it would have been better to re-invest in another high yielding Trust but for better or worse etc.,

As always timing and then timein is important.

Results analysis from Kepler Trust Intelligence

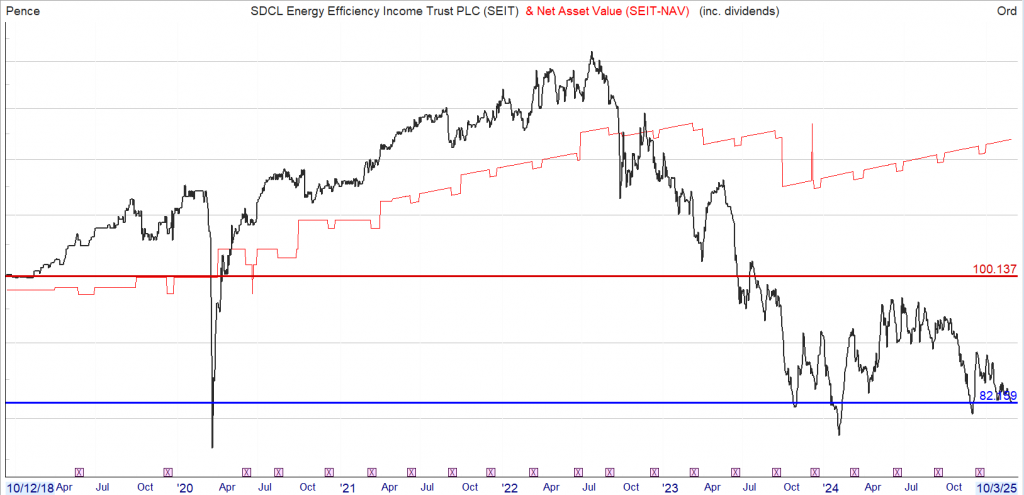

SDCL Energy Efficiency Income (SEIT) has reported its interim results to 30/09/2024, with the NAV stable at 90.6p (31/03/2024: 90.5p) and aggregate dividends of 3.16p compared to 3.12p for the same period last year. SEIT made a profit before tax of £35 million (2023 equivalent period: Loss of £89m). At the current share price, SEIT yields c. 11%. First half dividends were covered 1.1x by cash and the board reaffirmed its dividend guidance for the year ending 31/03/2025 of 6.32p (2024: 6.24p). SEIT’s portfolio valuation was £1,103m compared to £1,117m at 31/03/2023, with the main difference being the sale of UU Solar for £90m in May 2024.

SEIT’s gearing was 35% LTV, with 11% at a fund level through the trust’s revolving credit facility (RCF) and 24% at a project level. The same figures calculated as a percentage of NAV were 54%, split 17% at the trust level and 37% at a project level. The average interest rate was 5.6% and the average remaining life 4.1 years. Over 80% of debt at a project level is amortising, meaning it will naturally run off over time. SEIT’s discount at the half year end was c. 30% and is currently c. 36%. The Morningstar Renewable Energy Infrastructure peer group average was c. 20% and is currently c. 28%. The board and manager set out a plan to address the discount in the final results to 31/03/2024, the main points focusing on disposals, NAV return, capital allocation and reducing short term borrowings.

Kepler View

In the weeks before SDCL Energy Efficiency Income’s (SEIT) results announcement, the Morningstar Renewable Energy Infrastructure peer group in which it sits experienced significant discount widening, seemingly a result of the US election and investor worries about the different approach the new administration is expected to take to renewable energy. Share prices of other renewable energy companies were similarly hit. While it’s quite likely in our view that this is a sector-wide over-reaction, SEIT has some specific differences in its business model compared to the peer group.

First, the vast majority of SEIT’s revenues do not rely on any form of subsidy or incentive, and its projects are primarily rooted in their commercial attractions. Second, SEIT has very limited merchant exposure, with most of its long-term revenues contracted, and low direct exposure to power prices. SEIT is really an equity investor in platforms that provide corporate customers with efficiency solutions, so it participates not only in the contracted revenues that come from these solutions, but in the growth of the platforms themselves. Third, SEIT’s project-level debt is mostly amortising and so is repaid over a period of time, with many of its assets and investments extending well beyond the life of the debt, giving the trust different options in the future to enhance earnings. The team also point out one of the first moves made by the new US administration was the formation of a new Department of Government Efficiency, so ‘efficiency’ appears to be a positive theme in the US, which SDCL counts as its single largest country exposure at 67%.

Without getting into the flamboyant rhetoric, it is fair to say that the incoming US administration has an agenda much less focused on ‘energy transition’ and whatever the practical realities that unfold over the next few years, this is a negative for investor sentiment right now. We think SEIT’s business model, while aligned with energy transition, is relevant to customers with concerns about energy security, either more locally due to extreme weather events, or more widely due to geopolitical instability, as well as more straightforwardly simply helping customers to reduce costs. Thus, in our view, SEIT’s business model doesn’t really align with the main negatives of investor sentiment, and as the board’s plan to address the discount unfolds, the current discount could prove to be a significant opportunity.

09/12/2024

Current yield 12.5%

Current discount to NAV 46%

Definitely believe that which you said. Your favorite justification seemed to be on the

web the easiest thing to be aware of. I say to you, I definitely get annoyed while people consider worries that

they plainly do not know about. You managed to hit the

nail upon the top and defined out the whole thing without

having side effect , people could take a signal. Will likely be back to get more.

Thanks https://auhellspin.wordpress.com/