Cash was king last week, with Royal London Short Term Money Market rising two places to take the top spot.

The money market fund, which can be viewed as a cash proxy due to its investments in overnight deposits and ultra-short term bonds, yields around 4.8%.

However, given that UK interest rates have now fallen to 4.5%, the yield on this strategy will also fall over the coming months. The Y units automatically reinvest any income generated, rather than paying it out.

UK interest rates cut to 4.5%.

Tech funds lost popularity last week, even as the Nasdaq 100 index in GBP rose about 1.5%. Scottish Mortgage Ord SMT fell one place to second, L&G Global Technology Index dropped to fourth place, and Polar Capital Technology Ord PCT fell four places to ninth.

Tech shares have moved higher this year, with SMT up 13.7% and PCT up 4.6%. They continue a strong run since 2023, driven by developments in artificial intelligence (AI) technology and lower interest rates.

The other risers last week were Greencoat UK Wind UKW , Vanguard LifeStrategy 80% Equity and JPMorgan Global Growth & Income Ord JGGI, Global multi-manager trusts Alliance Witan Ord ALW and F&C Investment Trust Ord FCIT were new entries, while Fidelity Index World held on to seventh position. HSBC FTSE All World and Vanguard US Equity Index dropped off the list.

The Results Round-Up: The week’s investment trust results

Diverse Income (DIVI) outperforms both the benchmark and peers; Henderson Opportunities (HOT) outperforms despite the distractions of a strategic review and the unwanted attention of a certain activist investor; Brunner’s (BUT) all-weather approach clocks up a double-digit NAV return; and Scottish American’s (SAIN) managers put their money where their mouths are after a tough year.

By Frank Buhagiar

Diverse Income Trust (DIVI) outperforms

DIVI beat all comers hands down over the latest half-year period. For all comers read the benchmark and the small-cap investor’s peer group: NAV total return came in at +4.9% compared to the Deutsche Numis All-Share Index’s +2.1% and the peer group’s +0.9% average return, while DIVI’s +5.3% share price total return topped the lot. Not bad going considering, as Chairman Andrew Bell points out, that “the share prices of smaller companies and AIM stocks remained under pressure.” Reasons cited include “persistent selling of UK equities by domestic investors, amid uncertainties over forthcoming tax rises by the new government, during the prolonged lead-up to the October Budget.”

The fund’s longer-term track record stacks up too. Over the 13 years and seven months since launch, the fund has generated NAV and share price total returns of +235.5% and +196.2% respectively, easily trumping the +190.0% and +176.1% NAV/share price returns of the peer group and +123.6% for the Deutsche Numis All-Share Index. No surprise then that the Board’s regular review of the Company’s strategy and approach concluded that these remained “relevant and appropriate”. Well, if ain’t broke. Shares closed unchanged on the day of the results at 94.6p.

Winterflood: “Top ten holdings represented 25% of NAV as at 30 November, with largest sector exposures being Financials (35%), Industrials (18%) and Basic Materials (10%). In July, shareholders will be able to elect to redeem shares at the next redemption point of 29 August 2025.”

Henderson Opportunities’ (HOT) heating up

HOT’s busy year included a strategic review, the drawing up of a scheme of reconstruction offering shareholders a full cash exit at NAV and/or the opportunity to roll into an open-ended fund and, if that wasn’t enough, the unwanted attention of activist investor Saba Capital culminating in a requisitioned general meeting that went in favour of the Board. Didn’t affect the full-year performance though: NAV total return came in at +17.1%, comfortably ahead of the FTSE All-share’s +16.3%. According to the investment managers, the outperformance mostly driven by the portfolio’s holdings in larger companies which offset a weak showing from the small-cap contingent.

As for HOT’s future, well that’s in the hands of shareholders who are due to vote on the scheme of reconstruction at two general meetings to be held on 21 February 2025 and on 14 March 2025. Question is, how will shareholder Saba vote? The results were good for a 1.5p rise in the share price to 229p.

Winterflood: “Small cap overweight (AIM stocks 33% of portfolio) has detracted over time (AIM underperformed FTSE All Share by 55% over last 3 years). Takeover activity aided performance over the reporting period.”

Brunner’s (BUT) all-weather approach

BUT not only clocked up NAV and share price total returns of +17.9% and +39.3% respectively, but the latest full year also saw the global fund win the ‘Investment Company of the Year – Global’ award from Investment Week and promotion to the FTSE 250 Index. Only blot on the report card was that NAV performance couldn’t match the +23.6% clocked up by the composite benchmark (70% FTSE World Ex. UK/30% FTSE All-Share). Although BUT had outperformed the benchmark in each of the previous five years, so was perhaps due a breather. Besides, as the portfolio managers point out, “Most of the underperformance is best explained at the stock level within the Financials and Technology sectors. Both of these important sectors roared ahead. Our holdings participated but did not keep up.” That’s largely down to the managers’ “balanced approach, but also our bias to prudency. This means that we always run the risk of underperforming in a cyclical rally, as happened this year, but we should be better protected on the downside in the event of a cyclical downturn.”

Chair Carolan Dobson adds “Ultimately, our ‘All-Weather’ approach does not mean chasing some kind of absolute return or constant outperformance of the benchmark – rather it means the pursuit of consistent performance”. And Dobson goes on to finish on “a high note” that, although many macroeconomic and geopolitical risks remain, “opportunities to invest in great companies continue to abound.” Market liked what it heard – shares added 5p to close at 1415p.

Winterflood: “Share price TR +39.3%, as discount moved to premium, despite no shares repurchased (aided by index inclusion). First-ever issuance £3.9m. Underperformance mainly attributable to stock selection within the Financial and Technology sectors. Portfolio composition 49% US, 27% UK, 20% Europe.”

Scottish American’s (SAIN) staying true

SAIN’s investment managers described the global equity income fund’s full-year performance as “mixed”. First the good bits, “growth in earnings across the Company’s portfolio was strong. The backbone is our investment in equities, where dividend growth was robust. Income from the property, infrastructure and bond portfolios was also solid. Together, these investments drove growth in the Company’s earnings per share, lifting it 7.6% above the prior year. This strong result underpinned another inflation-beating increase in SAINTS’ dividend to shareholders.” Followed by the not-so-good bits, “NAV growth of the Company lagged global equity markets, as measured by the FTSE All-World, by some way”: +6.1% NAV total return compared to the market’s +19.8%.

The relative shortfall “was due primarily to the more balanced approach that SAINTS takes to investing, and in particular our focus on companies with resilient earnings and income growth.” Problem is, “These were not the type of companies that saw the strongest rises in share prices in 2024.” The investment managers have no intention of deviating from their strategy though “We will stay true to SAINTS’ objective of delivering a resilient income that grows ahead of inflation, while also aiming to grow capital value. Our analysis of the investment portfolio suggests it is well-placed for this task.” And the managers are putting their money where their mouths are “We remain resolutely aligned with shareholders, investing alongside them as owners of SAINTS’ shares.” Investors adopting the wait-and-see-approach – share price was unchanged at 519p.

Winterflood: “Board remains confident in approach and believes discount is cyclical rather than structural. Board expects future market environments to lead to a reduction in ‘manufactured’ dividends or a need to sell assets, hence current income generation method is preferred. US underweight (43% vs. 70%) and Tech underweight detracted, as did quality and income factors. Property and bonds allocation detracted as well relative to equities. Infrastructure (3% of NAV) detracted as well (-3% TR).”

The Board of Assura plc (“Assura” or the “Company”) notes the recent media speculation and confirms that it has received a preliminary, unsolicited approach from Kohlberg Kravis Roberts & Co. Partners L.L.P. (“KKR”) and USS Investment Management Limited (as agent for and on behalf of Universities Superannuation Scheme Limited (acting in its capacity as sole corporate trustee of the Universities Superannuation Scheme)) (“USSIM”) which may or may not lead to an offer being made for the Company.

The Board is currently reviewing the proposal with its advisers. A further announcement will be made as appropriate. There can be no certainty that any offer will be made, nor as to the terms of any such offer.

Shareholders are advised to take no action.

The Board remains confident in the long-term prospects of the Company and believes that Assura is strongly positioned to create value for shareholders.

££££££££££££££

The Snowball may sell on Monday to book a profit as it will not presently be able to build a full position.

The current plan for the Snowball is to re-invest all earned dividends back into the portfolio with an income target of £14,500.

If you have longer to retirement, compound interest growth starts to accelerate the longer you stay invested.

If we use CTY as the working example, your capital should increase if you have an unexpected call on your cash. No guarantees though.

Also the earned dividends would be re-invested, either back into the share or another Trust, earning more dividends to re-invest in the portfolio.

The options for you cash, the totals are the unknown.

An annuity yielding 7% but you have to surrender all your cash.

Interest rates may be lower a lot lower, that’s the gamble.

Canada Life figures show the 65-year-old with a £100,000 pension pot could buy an annuity linked to the retail price index (RPI) that would generate a starting annual income of £3,896. That’s up from £2,195 in the New Year following a 77% spike in rates this year. Oct 22

So not an option for me.

The 4% rule.

To use the 4% rule your 100k would need to have grown to £360 k.

Good luck with that.

Also if you want to pass on any of your wealth, your fund could be depleted depending on how long you live.

OR

You could have a foot in each camp, if you are not retiring soon.

Dividends can be more reliable than share prices as they’re driven by the companies performance itself and not by the whim of investors. As part of a total return / reinvestment strategy, this income could be reinvested into income assets or back into the equity market depending on the relative valuations.

Are you wondering when the best time is to retire, and how much you should take from your pension pot? We explain how the 4% rule could help you retire comfortably

Accessing your hard-earned pension pot when you are ready to retire is a major milestone in life.

After years of setting money aside, you will have the freedom to withdraw money as you please, and spend it on the lifestyle you desire.

But deciding when to start taking money from your pension savings, and how much to withdraw, can be tricky.

Get 6 free issues + water bottle gift

Try MoneyWeek magazine today for unparalleled financial insight, analysis and expert opinion.

As well as hopefully enjoying the returns from your pension savings, money still needs to be available for bills and possibly your own long-term care.

That is especially important as the cost of retirement is rising. Inflation rose to 2.5% in December, and could increase to 3.7% later this year, according to the Bank of England. Inflation will eat into the real value of your pension pot over the long term.

“It’s well known that most people are starting to plan for their retirement too late in life and do not have enough saved for a comfortable retirement,” Brian Byrnes, head of personal finance at Moneybox, tells MoneyWeek.

The latest research from the Pensions and Lifetime Savings Association, a trade body, suggests retirees need an income of £43,100 per year a “comfortable retirement”. For a couple, the joint figure needed is £59,000 a year.

However, a little-known rule called the 4% pension rule may be able to help you plan your retirement, and ensure your money lasts as long as you do. We explain what it is and how it works.

What is the 4% pension rule?

The rule states that retirees should take 4% of their fund in the first year of withdrawals, and the same monetary amount (adjusted for the rate of inflation) each year.

For example, if your pension pot is worth £500,000, you could withdraw £20,000 in the first year of your retirement. If inflation is 2% during that year, then in the second year you would withdraw £20,400.

This should ensure that your pension pot will support you through a 30-year retirement, in almost any economic environment. For that reason it is often referred to as the “safe withdrawal rate”.

Academics at the American Association of Individual Investors devised the 4% rule in 1998 after researching a sustainable withdrawal rate for a retirement pot that wouldn’t deplete the savings.

It looked at data from 1926 to 1995 and found that a rate of 3-4% is “extremely unlikely to exhaust any portfolio of stocks and bonds”.

“As a rule of thumb, the 4% rule is a good place to start when thinking about how much you need to save for retirement,” Olly Cheng, director of financial planning at Rathbones Group, tells MoneyWeek. “It is a nice benchmark rate to use, and therefore lets people set a simple target to see if they are on track with their savings.”

Can I rely solely on the 4% rule?

It is worth thinking about when to start accessing your pension pot, as market returns will have an influence on the success of the 4% rule.

A study from Morningstar in 2022 argued that 3.3% is the “safe” level of drawdown in order to protect a portfolio’s value over the long term.

However, this was based on the fairly downbeat market conditions at the time. Morningstar’s latest insight on the matter suggests that, with today’s more favourable market conditions, a 4% starting drawdown is once again safe.

Market conditions impact the 4% rule because it is based on the assumption that, over a 30-year period, a balanced portfolio (usually modelled as a 50/50 or 60/40 portfolio) will generate sufficient returns to cover the impact of 4% withdrawals annually.

This is true on average, over a 30-year period. Some years, though, a balanced portfolio will grow at less than 4%, and it may even fall in value.

According to Morningstar, in 2022 the average 50/50 portfolio lost 16% of its value. This is why Morningstar recommended a lower safe withdrawal rate for people retiring that year; withdrawing the full 4% would have further compounded their pension pot’s losses during the bad year, before it had a chance to gain value in any good years.

For that reason, it pays to check the economic outlook carefully, and research the safe withdrawal rate for your first year in retirement before jumping straight in with a 4% withdrawal rate. The good news is that it is only during particularly bad years that 4% isn’t a safe initial drawdown rate, which is why this rule of thumb has, on the whole, stood the rest of time.

When should you retire?

Timing your retirement is a key decision. Ideally, you’ll retire in a good year for your portfolio. In any given 30-year period there are bound to be some bad years, but you want your pension pot to have registered some gains during the good years before these come around.

While hard to predict in advance, it is worth checking the economic outlook when you first start thinking about retiring. If the outlook is bad, and you feel you can still manage a year or two more of work, then it could be worth delaying your retirement and giving your pension pot a better chance of getting off to a good start.

This has the added benefit of fattening it up through your working income beforehand, and reducing the amount of time it will need to last you. All these factors swing the maths in your favour, and increase your chances of enjoying a comfortable retirement.

Of course, it is impossible to know in advance whether next year will be a better or worse year to retire than this one. Plus, there are many reasons why you may not want, or be able, to postpone your retirement for an extra year.

For this reason, John Corbyn, pensions specialist at the wealth manager Quilter, suggests making more conservative withdrawals early in your retirement, especially if you do happen to retire during a period of economic downturn.

What else do I need to know about the 4% rule?

Like all rules of thumb, says Corbyn, the 4% concept is based on certain assumptions.

“It needs to be overlaid with someone’s state of health and propensity to spend, which is likely to be higher for younger clients and lower for older clients,” he says.

“Care needs to be taken to ensure the attitude to risk and propensity for loss is also built into these assumptions.

“Depending on your risk tolerance, investment strategy, and the actual returns you get, you might consider a slightly more conservative withdrawal rate.”

Corbyn says it is crucial to continuously review and adjust your strategy based on your actual investment returns, spending needs, and the broader economic landscape.

“Ultimately, pensions are a long-term savings vehicle and potentially may need to pay for someone’s income for up to 30-40 years, and care needs to be taken if the fund is accessed early, as short-term gain may lead to long-term pain so getting advice is key,” he adds.

According to Cheng, retirement expenditure isn’t usually a flat annual amount, with the early years sometimes showing a higher expenditure when people want to travel, before expenditure starts to reduce slightly. He comments: “In the final years of their lives, many people will then see a further spike in expenditure as care is required.”

It’s important to note that this strategy may not work for everyone and is just one of many factors to consider when planning to retire.

Make a retirement plan

What you plan to do with your retirement will also have a huge impact on when you should start accessing your pension pot, so it’s a good idea to know what you want to do and the costs of doing it.

“If you have dreams of travelling the world then you might need much more retirement income than if you are content with a quiet life at home,” says Corbyn.

“It’s essential to have a realistic projection of your monthly and yearly expenses, including contingencies for unexpected costs.”

Cheng echoes this, saying “there is often a real benefit to undertaking some more detailed cash flow planning and speaking to an adviser”.

According to Moneybox data, just 11% of people are confident they will have a comfortable retirement. It is therefore vital that retirees have access to the right drawdown advice, and understand when to retire, and how much to withdraw, says Byrnes.

Pensions tax

Whatever rule you use, experts say it is always important to consider the tax implications when withdrawing money from a pension.

This is because beyond the 25% tax-free lump sum, you will need to pay income tax on withdrawals if you are earning above the tax-free personal allowance.

It may not take much to go above the £12,570 personal allowance, given the full new state pension is currently more than £11,500 a year.

“Tax planning is a crucial aspect of accessing a pension, and those who are thinking for instance of buying an annuity accessing a pension flexibly by withdrawing taxable amounts should take note if they are earning or taking taxable income from elsewhere, including the state pension,” says Alice Haine, personal finance analyst at the investment platform Bestinvest.

“For someone drawing the full flat-rate state pension at the moment, additional income – whether from work or a private pension – of [just over £1,000] will take them over the personal allowance and into basic-rate tax.

“For those with larger pensions or higher incomes, there will be the potential risk of being taken into the higher or even additional-rate tax brackets, and some savers in drawdown should moderate their pension income to avoid this.”

I first wrote about VSL back in October 2023. It wasn’t an “idea of the year” or anything like that. It was something I already held, and the reporting had always been pretty dire so when they announced a wind down, I decided to try to write about it trying to make head or tail of it, if I could. Over 5 articles which were roughly looking at the semi-annual updates I continued to be hopeful it could turn around. The company reports showed a pathway to realisations.

The Oak Bloke’s Substack

Part of this optimism was the fact that some holdings notably WeFox was also held by Chrysalis. Good company and all that.

In October 2023 VSL was £200m Asset-backed loans delivering a 14% yield, £150m of near term maturities, -£75m of liabilities, over £100m of equity (plus options) and a £150m market cap. So the thesis was based on VSL info the fund would be debt free and 50% of the market cap returned before we reached 2026. That was the theory; the reality was very different.

These were asset-backed loans with great geographic diversity, a spread of counter parties, the prospect of 12% yield for several years. We’ve had no great recession, no great crisis, and the stock market has been at record levels. Rising interest rates and inflation took their toll on holdings. A lack of exit opportunities and a depressed Venture Capital and M&A environment really didn’t help either. As I write in February 2025 sentiment has improved a little but VC is hardly back to anything approaching real bullishness and positivity.

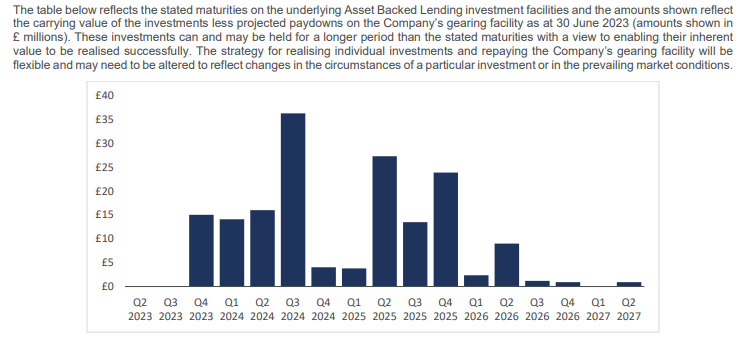

This was the near term expected cash realisations back in October 2023:

Maturities as at 30/06/23

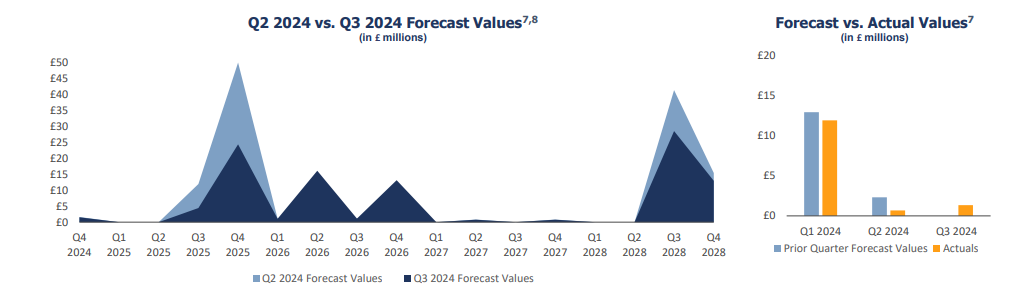

The reality however was, the timelines being reported by the fund proved hopelessly optimistic. Actual maturities have been pushed back and pushed back, quarter after quarter. Even recently this continues to happen. See 2Q24 and 3Q24 below. Have you ever known such a forgiving lender? Payment holiday no problem Mr Customer. We’ll just bump our investor cash forecast back another few years. VSL shrugs.

There have been substantial write offs of equity since October 2023 (-29.2%) but also write offs of asset-backed loans too. (-8.35%)

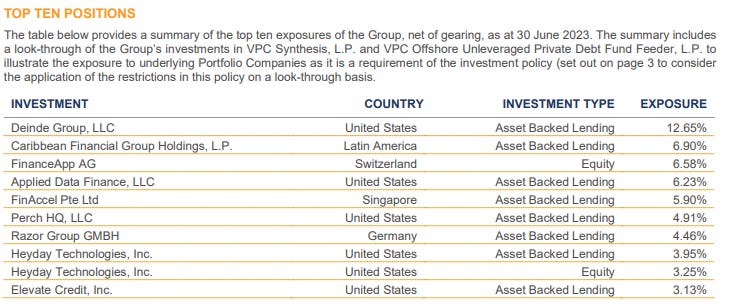

The fund trades on a 57% discount and once again is and “should be” very tempting. But this RNS at Christmas time was the clincher. Razor is £17m loan and £12m equity so £29m of the £167m NAV. ~20% of the NAV and ~40% of the share price.

VSL had a buy of 70.8p when I first wrote about it. I sold at just 27.2p. So a 43.6p loss. Factor in a capital return of 3.2p and dividends of 11.12p then the loss is a net 29.28p = a 41.3% loss.

Lessons to learn?

As some kind readers have pointed out you can’t win ‘em all and you win some and lose some. Inevitably the hope is to learn lessons.

Of course one lesson is to be sceptical over statements like “overcollateralised protection”. The reality was this protection proved to not be much protection whatsoever.

Should investors not take information at face value? The annual report is subject to audit and PWC were the auditors here and reported no material misstatements.

Should macro considerations have been considered more seriously? A share which lends money at high enough levels of return to sustain a 12%+ yield of course is susceptible to the danger of its customers, already burdened with expensive debt (from VSL) to implode when higher interest rates and rapid inflation tipped them over the edge. That’s entirely plausible and likely, and that is the lesson to learn here.

Anyways, this is the Oak Bloke calling time on VSL. Good luck to remaining holders.

“Diversification is an established tenet of conservative investment” – Benjamin Graham

One of the most prevalent mistakes made by investors is a lack of diversification within their portfolio.

Before diversifying, each investor should first assess and attempt to understand underlying risks across their asset allocation, their tolerance to those risks, their time horizon, and their goals.

We are investing in a VUCA world i.e. one which is Volatile, Uncertain, Complex and Ambiguous. There is so much out of our control and the fate of a particular company; its stock can change overnight. For example, Patisserie Valerie, Carillion, Theranos*(privately held), 4D Pharma, Credit Suisse, and the Woodford Equity Income Fund all had experienced unexpected changes to their predicted returns.

Failing to diversify investments across different asset classes, sectors, and geographical regions can result in heightened risk. By spreading investments across a variety of asset classes, investors can reduce the impact of any single investment’s poor performance and potentially enhance their long-term returns. Case in point, many ISA investors are mainly UK-centric investors and this has led to their investment portfolios lacking exposure to US listed stocks which in the main have significantly outperformed UK listed stocks, especially the US best-performing tech behemoths during the past ten years.

The Company also announces a quarterly interim dividend of 1.95 pence per share for the quarter ended 31 December 2024, in line with the dividend target of 7.80p per share for the year to 31 March 2025, as set out in the 2024 Annual Report – which represents a yield of 11.1% on the closing share price on 13 February 2025.