SNOWBALL SHARE NESF. Not buy advice DYOR

Have we seen

Investment Trust Dividends

SNOWBALL SHARE NESF. Not buy advice DYOR

Have we seen

Picking high-income stocks in an ISA can be a route to securing long-term passive income.

Posted by Alan Oscroft

Published 5 February

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

The ability to invest up to £20,000 per year in an ISA and not pay a penny tax on the passive income it can generate can be life-changing.

In the 2023/24 financial year, the latest for which we have the numbers, UK adults held 15m ISA accounts. And the total cash invested in those ISA accounts came to £103bn ! So we’re a nation of canny savers and investors, right ? Well, we need to dig a bit deeper.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

Of those 15m ISA accounts, 9.9m were Cash ISAs — and only 4.1m were Stocks and Shares ISAs. Cash ISAs held £69.5bn, but only £31.1bn — less than half that amount — went into Stocks and Shares ISAs.

Cash ISAs can be a great way to protect some emergency cash or short-term savings. And for folks who really don’t want any stock market risk at all, the guaranteed returns offer a safer option. But over the long term, Stocks and Shares ISAs have wiped the floor with the Cash ISA alternative.

The top Cash ISA interest rates are currently a bit above 4%. And that’s actually not bad at all. But over the past 10 years, the average annual Stocks and Shares ISA return has come in at a whopping 9.6%.

The total sum we’d need to build up depends on the rate of return we can achieve.

From that 9.6% Stocks and Shares ISA return, around £132,000 should generate enough passive income to cover our target £1,000 per month. And investing £500 per month with all dividends reinvested, we could get there in 12 years.

To get the same from a 4% Cash ISA return, we’d need more than £320,000. And at that interest rate, it should take 29 years to build that up.

To be fair, that 9.6% from shares has been above average for shares in general. But the 4% from cash can’t be maintained when Bank of England (BoE) rates come down. I can easily see Cash ISA interest getting down below the BoE’s 2% inflation target. To take home £1,000 per month from a 2% return, we’d need more than £600,000 — and 56 years to get there.

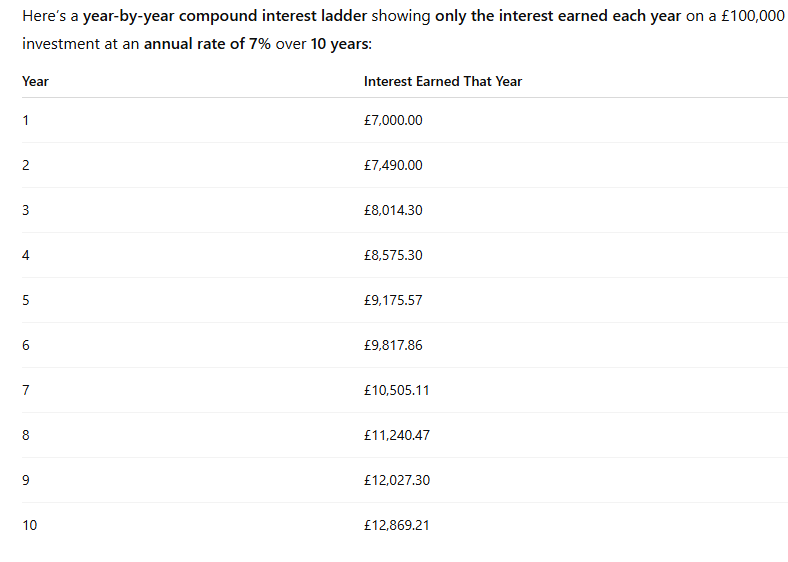

The target for the SNOBWALL is a return of 10% on seed capital of 100k. Hopefully in 2 years time it will earn income of 1k per month.

Your Snowball should be different to mine, to reflect you risk profile and how many years before you want to spend your dividends instead of re-investing them. Depending on how many years you have to re-invest your dividends there may be surplus income that you could continue to re-invest with.

Monthly Dividend Superstars:

11% Average Annual Yields

Most investors with $600,000 in their portfolios think they don’t have enough money to retire on.

They do – they just need to do two things with their “buy and hope” portfolios to turn them into $5,000+ monthly income streams:

The result? More than $5,000 in monthly income (from an average annual yield just over 11%, paid about every 30 days). With potential upside on your initial $600,000 to boot!

And this strategy isn’t capped at $600,000. If you’ve saved a million (or even two), you can just buy more of these elite monthly payers and boost your passive income to $9,166 or even $18,333 per month.

Now we’re talking!

But if you’re a billionaire, sorry, you are out of luck. These Goldilocks payers won’t be able to absorb all of your cash. With total market caps around $1 billion or $2 billion, these vehicles are too small for institutional money.

Which is perfect for humble contrarians like you and me. This ceiling has created inefficiencies that we can take advantage of. After all, in a completely efficient market, we’d have to make a choice between dividends and upside. Here, though, we get both.

Inefficient Markets Help Us

Bank $100,000 Annually (per Million)

Fortunately for you and me, the financial markets aren’t 100% efficient. And some corners are even less mature and less combed through than others.

These corners provide us contrarians with stable income opportunities that are both safe and lucrative.

There are anomalies in high yield. In an efficient market, you wouldn’t expect funds that pay big dividends today to also put up solid price gains, too.

We’re taught that it’s an either/or relationship between yield and upside – we can either collect dividends today or enjoy upside tomorrow, but not both.

But that’s simply not true in real life. Otherwise, why would these monthly payers put up serious annualized returns in the last 10 years while boasting outsized dividend yields?

For example, take a look at these 5 incredible funds that pay monthly and soar:

This is the key to a true “Monthly Payer Portfolio” – banking enough yields to live on while steadily growing your capital. It’s literally the difference between dying broke and never running out of money!

But I’m NOT suggesting you run out and buy these funds.

Some have been on my watchlist and in our premium portfolios over the years, but I mention them only as examples of the potential ahead.

And get paid every month, too.

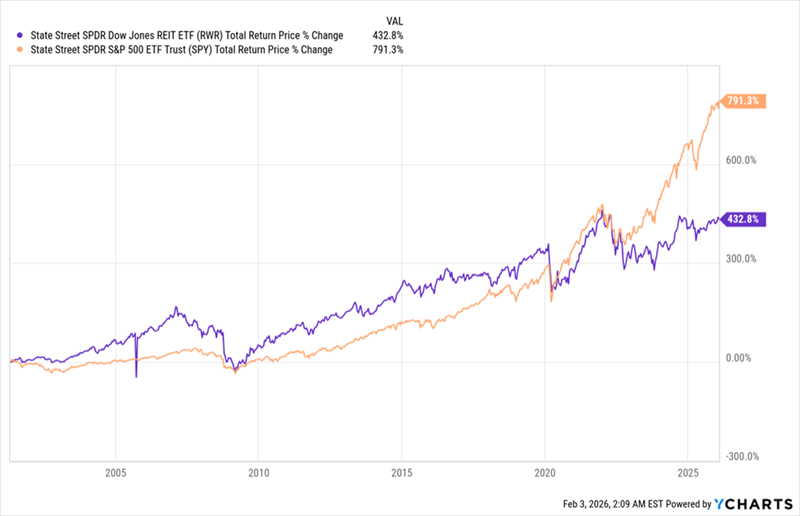

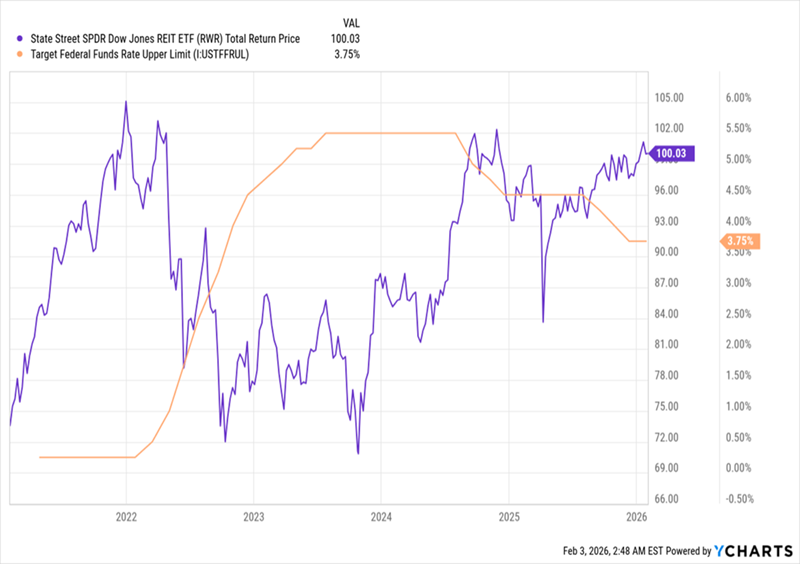

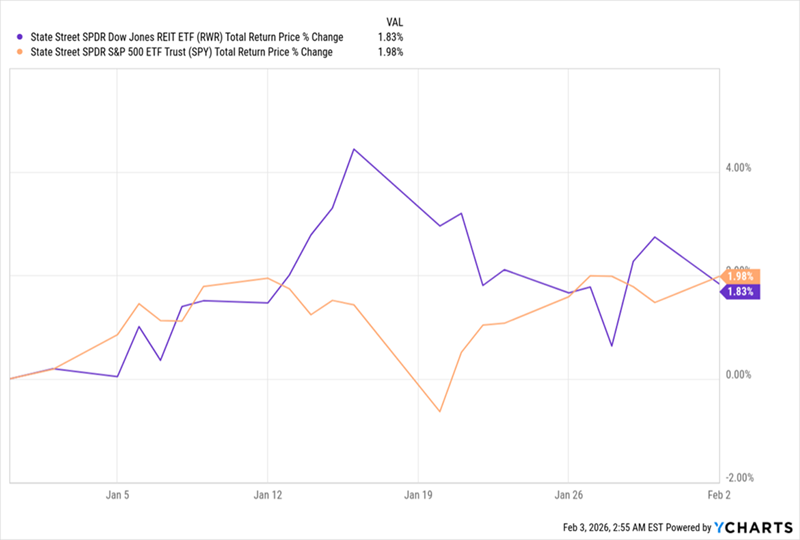

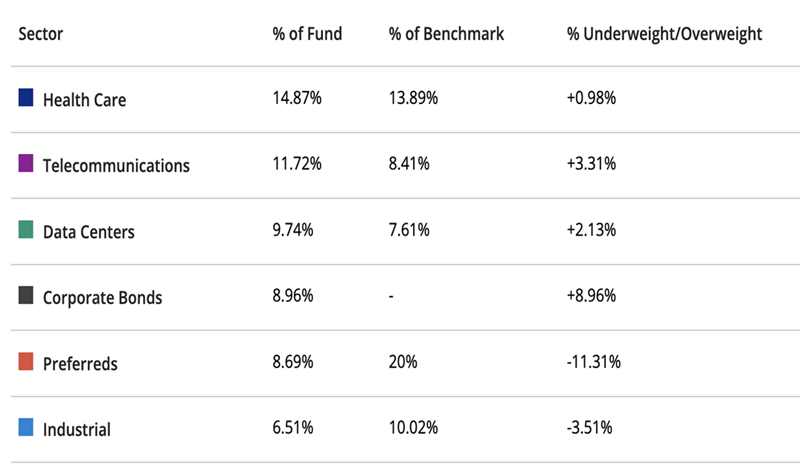

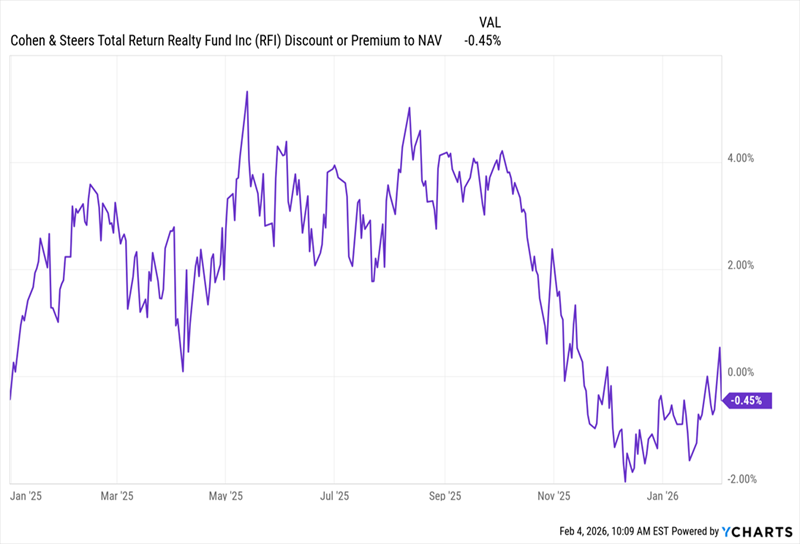

Our 8.6% Dividend Play on a “REIT Revival” by Michael Foster, Investment Strategist A multi-year disconnect in high-yielding REITs is about to turn on its head. When it does, these solid income plays are poised to shoot ahead of stocks. I’m talking about a quick reversal of pretty well everything investors thought had REITs left for dead, interest rate trends and the work-from-home shift among them. Now is the time to buy. And we contrarian income investors know the play: At times like these, we look to 8%+ paying closed-end funds (CEFs) to reap the strongest dividends and potential upside. I say this as REITs, long-time market outperformers, have been stuck in an unusually long slump. Remember when stocks ricocheted hard after the early days of the pandemic? REITs (with their benchmark ETF shown in purple below, compared to the main S&P 500 ETF, in orange) rebounded, too. But not nearly as much. REITs’ Slow Recovery  Why REIT Headwinds Are Diminishingand Setting Up to Reverse There are lots of reasons why REITs have lagged in the last six years, and none of them are really secrets: Work-from-home hit office demand. Interest rates jumped, hitting REITs’ bottom lines, as these companies borrow heavily to invest in their properties. Lower immigration into the US also had an effect on both housing and workspace demand. That last point – immigration into America – still applies. But both of those other barriers, which are far more meaningful, have either flipped or are in the process of doing so. Work-from-home? It’s largely been replaced by either a full-time return to the office or hybrid work. Interest rates? This is where things get intriguing. Rates Fall, REITs Start to Respond  REITs, as mentioned, borrow to invest in real estate, so rate cuts go straight to their bottom lines. The cuts the Federal Reserve has delivered since mid-2024 (in orange above) have come more slowly than markets expected. So it follows that the boost to REIT profits, and therefore their share prices, is real (purple line), but smaller than investors hoped. That leaves REITs in a strong position – still underpriced, but starting to show momentum. And with the first month of 2026 now behind us, we can see the current state of play here: REITs Nearly Reeled In Stocks in January  As you can see, in January, REITs (again with their benchmark in purple above) almost met the stock market’s returns. Now, one month does not make a trend, but that’s a switch from what we saw in 2025, when the S&P 500 gained over 17% and RWR returned a mere 3.2%. The takeaway: The lead stocks have held over REITs is finally starting to fade. And if interest rates fall faster than the market expects – quite possible if President Trump’s nominee for Fed chair, Kevin Warsh, is confirmed – REITs could not just match the S&P 500 but beat it this year. That would finally end REITs’ six-year lag. Let’s buy in before that happens. How? My favorite avenue is through those aforementioned CEFs. Consider, for example, the Cohen & Steers Total Return Realty Fund (RFI), a holding in my CEF Insider service that yields 8.6% as I write this. The fund is a solid play here, thanks to that 8.6% dividend, which has been rock-steady for years. The fund pays that dividend monthly, to boot. Source: Income Calendar RFI is also nicely diversified, boasting a portfolio that gives us exposure to AI’s infrastructure needs, with significant weightings in data center and communications (think cell-tower) REITs.  Source: Cohen & Steers Source: Cohen & SteersIt also holds industrial REITs, giving us broad exposure to both the reshoring and automation of factories. That top allocation to healthcare is also a plus, letting us tap into the aging of the US populations – a trend that still has decades to run. Finally, its allocations to bonds and preferred shares add stability. The fund is cheap, too. As I write this, we can buy RFI at a 0.5% discount to net asset value (NAV, or the value of the fund’s portfolio). I know that doesn’t sound like much of a deal, but it’s far below the premiums at which RFI traded for most of last year:  The kicker? That “small” discount is also well below RFI’s average premium of 3.7% over the last five years. That makes now a good time to buy this overlooked bargain, before other investors pick up on the many tailwinds shifting in RFI’s favor. 5 More “Built-for-2026” Income Plays You’re Not Too Late On (Yields Up to 10.7%) CEFs are, hands-down, the top plays on disconnects like the one we’re seeing shape up with REITs today, for three reasons:CEFs pay us (mostly) in cash, thanks to their rich dividends (around 8% on average).CEFs give us a double discount – on both washed-out stocks (or in this case REITs) themselves and on the fund itself through its discount to NAV.CEFs put our investments in the hands of a professional who knows their asset class inside and out. |

Whether you’re an ISA investor seeking reliable returns, looking to add a bit more risk to your portfolio or are new to investing, MoneyWeek asked the experts for funds and investment trusts you could consider in 2026

By Laura Miller

ISA fund and trust picks for every type of investor – which could work for you?

(Image credit: Getty Images)Share

With the end of the 2025/26 tax year approaching on 5 April, now is the time to make full use of your current £20,000 ISA allowance and start thinking about what to do with the next allowance when it resets on 6 April.

Stocks and shares ISAs provide investors with a home to grow money free of any tax on the gains, which can be significant. Those who invested the full ISA allowance every year into the FTSE All-Share Index from when ISAs launched in April 1999, for example, would have a portfolio worth £665,696 over the 26 years to April 2025, according to calculations by Interactive Investor (having contributed £326,560).

Picking the right investments for your stocks and shares ISA portfolio is key – ideally you should balance your attitude to risk, the types of investments you already hold and where you are in your investment learning curve.

Stay ahead of the curve with MoneyWeek magazine and enjoy the latest financial news and expert analysis, plus 58% off after your trial.

MoneyWeek asked investment experts at fund platforms Fidelity International and Interactive Investor for their top ISA fund and ISA investment trust picks, to suit different types of investors.

Stocks and shares ISA investors seeking a reliable return might look at global equity income funds. Investing in dividend-paying companies across the globe, they have the potential for a growing income stream alongside long-term capital growth.

Global equity income funds often lean towards financially robust, well-managed businesses, a great match for anyone who loves the idea of steady earnings but still wants exposure to global markets.

Dzmitry Lipski, head of funds research at Interactive Investor, suggested the Fidelity Global Dividend fund, which has been managed by Dan Roberts since its 2012 launch, drawing on more than two decades of dividend-investing experience.

“It invests in companies globally that offer a healthy dividend yield and the potential for capital growth and aims to generate roughly 25% more income than its benchmark,” said Lipski.

The portfolio holds around 46 large, resilient companies, with Europe representing roughly 48%, North America 26% and the UK 15%, and no Chinese exposure. Lipski said: “Sector allocations are deliberately defensive, led by financials, industrials and consumer staples.”

Alternatively, Jemma Slingo, pensions and investment specialist at Fidelity International, said she likes Pyrford Global Total Return – about two thirds of the portfolio is in high quality bonds, and a third is in equities.

“It tries to keep volatility low, while providing a stable stream of inflation-beating returns,” she said. Slingo said that, while at first glance at the fund’s performance chart reveals few serious falls, “on the flip side, growth has been fairly muted particularly when inflation is accounted for”.

Pyrford has turned an initial investment of £1,000 into £1,440 over the course of the decade. If you want a ‘sleep at night’ option, however, this might be a trade off you’re willing to make.

With global stock markets becoming increasingly concentrated and growing fears of the AI theme potentially being overheated, those wanting to spice up their stocks and shares ISA portfolio with some interesting diversification could take a look at investment trust Murray International.

Kyle Caldwell, funds and investment education editor at interactive investor, said he likes the trust because he is “looking more towards those investment trusts that use their full global remit in having a good chunk of exposure to Asia Pacific and Latin America – Murray International ticks this box”.

The portfolio is very different from the wider market, it has a value investment style, and it offers an above average dividend yield of around 4%, Caldwell pointed out.

Fidelity’s Slingo is also concerned about the stock market being dominated by a handful of US technology stocks – and also likes Latin America and Asia, but this time in the form of the Lazard Emerging Markets fund.

“The fund seeks out companies that are cheaper than the market but that have better fundamental prospects,” she said, adding emerging markets were among the best performing equity assets last year and the outlook remains positive.

“Strong earnings growth, a weak US dollar and a rotation out of the US could all boost performance this year,” Slingo said.

For newer investors who would like something a little more interesting than a global tracker fund and who are nervous about jumpy markets, the Fidelity Global Dividend fund could be a good option.

“It invests in companies from around the world; offers a combination of growth and income; and aims to keep volatility lower than the wider market. The fund has delivered steady gains over the past 10 years,” Slingo said.

The fund contains some well-known names like Unilever and National Grid, Slingo added, so “new investors will know that buying the fund means buying real businesses that impact them”.

Alternatively Lipski at Interactive Investor highlights a managed solution, like Interactive Investor’s Managed ISA, might be a good place to start, where the investments are chosen for you.

Investors fill out a questionnaire and are matched with one of 10 portfolios – in two styles (index investment style and sustainable investment style) and five different levels of risk. Once invested, the portfolio is periodically rebalanced – in line with the risk level you signed up for.

The fund fees are low, and there is no separate management fee as it sits within Interactive Investor’s existing flat-fee subscription-based charging model.

A less experienced investor may also want to look at absolute return or capital preservation funds. They use a mix of strategies to limit volatility and help protect against big downturns.

Lipski suggested looking at the Trojan Fund: “Managed by Sebastian Lyon, Trojan Fund takes a conservative, disciplined approach focused on preserving capital and delivering long-term real returns,” he said.

Lyon invests across a broad range of asset classes. The equity portion is focused on large, financially robust companies in developed markets, particularly the UK and US. The fund also holds high-quality sovereign and inflation-linked bonds as defensive assets, alongside a strategic allocation to gold. Cash is also used meaningfully to protect capital and allow swift investment when opportunities arise.

“The fund offers a steady, defensive option for investors seeking long-term real returns with controlled risk,” said Lipski.

More experienced investors may want to consider smaller companies for their stocks and shares ISA. “These can be significantly riskier than large ones,” Fidelity’s Slingo pointed out, “however, experienced investors with long time horizons might want some exposure to this part of the market”.

Slingo suggested the Brown Advisory US Smaller Companies fund. “It deploys a big team of researchers to find the most promising smaller companies listed in the US. Their strategy is based on the belief that good fundamental research coupled with a long-term approach can generate attractive outperformance,” she said.

The fund is a higher risk option, and its performance has lagged the benchmark in recent years. “However, it may appeal to experienced investors who are concerned about the dominance of huge US tech stocks in their portfolios,” said Slingo.

Finally, according to Dave Baxter, senior fund content specialist at Interactive Investor, another good option for the more seasoned investor is the Marlborough Special Situations fund.

It invests in the dynamic growth potential of the UK’s innovative and agile smaller companies. Its sector bets are markedly different with big weightings to industrials, consumer discretionary shares and technology. Top holdings include Zegona Communications, Boku and SCA Investments.

Baxter said: “Marlborough Special Situations has been poor in 2025, and in recent years. The fund has more than 150 holdings and small position sizes, with its top holding making up only 2.6% of the portfolio.

“However, the fund has a good long-term record, and good exposure to micro caps, small caps and mid caps. It should in theory do better when interest rates fall in earnest.”

Now the NESF dividend has been announced the income earned for the first quarter of 2026 should be £3,641.00

The total for the year should be around £10,769.00.

There should be income from the dividends, as they are re-invested and also a contribution from VPC, which is a known unknown and should act as a buffer for the 2026 target of 10k.

IF the snowball earns £10,505.11, it will put the SNOWBALL several years ahead of the plan.

Next energy have announced their dividend target for year ending 31 Mar 2026

IF they pay the same dividend next year and you add 2.11p the total dividends could be 10.54p.

The current share price is 51p, if you buy before the xd date next week and IF they hold the dividend and don’t cut it, the yield would be 20% for holding just over a year.

The Board reconfirms the Company’s full-year dividend target guidance for the year ending 31 March 2026 remains unchanged at 8.43p per Ordinary Share (31 March 2025: 8.43p). | |

| · | Dividend cover for the full-year is forecast to be covered in a range of 1.1x – 1.3x by earnings post-debt amortisation. |

NextEnergy Solar Fund Limited

Third Interim Dividend Declaration

NextEnergy Solar Fund, a leading specialist investor in solar energy and energy storage, is pleased to announce its third interim dividend of 2.11p per Ordinary Share for the quarter ended 31 December 2025, in line with its previously stated target of paying dividends of 8.43p for the year ending 31 March 2026.

The third interim dividend of 2.11p per Ordinary Share will be paid on 31 March 2026 to Ordinary Shareholders on the register as at the close of business on 13 February 2026. The ex-dividend date is 12 February 2026.

Kyle Caldwell explains how you can build your own portfolio to provide regular income.

27th January 2026

by Kyle Caldwell from interactive investor

Since the pension freedoms were introduced in April 2015, it’s become increasingly common for individuals to use their pension to pay themselves an income in retirement.

For most people, the aim will be to secure a reliable and regular income from their investments, with the intention of not inflicting too much harm on the capital.

The good news is that for those who arrange their investments carefully, a monthly income can be achieved. There are several ways to go about this, as we explain below.

First some groundwork needs to be done. The starting point is to calculate what your existing provision will provide, and then compare this against what you need.

To calculate how much income you need to generate, factor in the state pension (if you are at an age where you can claim it), as well as any other assets that can be drawn on in retirement, such as ISAs and, for those who have them, defined benefit pensions.

Once you’ve done all the sums, you can work out the size of your income gap, which will determine the return you need to generate.

How much income you need/would like is a personal decision, depending heavily on lifestyle. However, ‘The Retirement Living Standards’ from Pensions UK are often cited. The calculations show someone living alone would need a pension pot of around £540,000 to £800,000 for a ‘comfortable’ retirement. For couples, the amount would be £300,000 to £460,000 per person.

Bear in mind that this is only an illustration, makes a host of assumptions, and is based on a single person buying an annuity. The figures shown are after tax, so the true amounts would be higher to meet the standards.

It could be that your pot is too small to achieve the target you have in mind, or that it requires stomaching a higher amount of risk than you are comfortable with.

For example, to generate income of £20,000 a year, a pot size of £400,000 would require an investment return of 5%. For larger sums, the dividend yield target would be lower, at 4.5% for £450,000 and 4% for £500,000.

Another thing to bear in mind is that the sooner you retire, the longer you will need your pension pot to stretch to last the course (assuming you choose income drawdown). There’s always the risk of draining your pension too soon if the investments underperform and if withdrawals are overly aggressive.

Another thing to consider is whether to use some of your pot to buy an annuity, which will provide guaranteed income for life. However, bear in mind the amount of income annuities offer tends to become more attractive the older you get. Moreover, buying an annuity is an irreversible decision.

Keeping your money invested at retirement provides more flexibility in terms of how much to withdraw and for estate planning. However, from next April, unspent pension funds will come under the inheritance tax net for the first time following a rule change by the government.

It is also worth remembering that choosing to remain invested at retirement or opting to buy an annuity is not a binary decision – you can do both. You could look to secure a guaranteed income through an annuity to cover a certain amount of expenditure, and then keep the rest invested to take flexibly.

There are various ways to arrange investments to pay yourself an income at retirement, with the most obvious being to focus primarily on income-generating assets.

To reduce risk, which is particularly important in retirement, one approach is to draw only the income produced by the underlying investments held in professionally managed funds and investment trusts (the “natural yield”), rather than eating into capital growth.

This is because in a scenario where stock markets fall sharply and income withdrawals are maintained or increased, it is difficult for a retirement fund’s capital value to recover after.

That’s particularly the case if you’re drawing on capital to maintain the required level of income when the market falls (as opposed to taking only the “natural” yield), since reducing the number of fund units you own makes it much harder for the fund to regain value.

For those who continue to draw income from a pension pot at that stage, a vicious cycle is created, resulting in the number of units and value of investments reducing further. The phenomenon is known as pound-cost ravaging, and in the worst-case scenario, this potentially means the pension pot running out before you die.

As a rule of thumb, withdrawing 4% a year is potentially considered a safe withdrawal rate. The theory is that by taking this percentage as an income, adjusted annually to account for inflation, retirement pots will potentially last 30 years or more.

However, this rule by no means offers cast-iron certainty. There are many unknown future variables that can impact whether 4% withdrawals will avoid draining your portfolio too soon.

Chief among the problems of this strategy is that investment performance is impossible to accurately predict. If your portfolio gets off to a bad start, continuing to draw 4% could mean your pot drains quicker than planned.

That said, 4% a year isn’t an overly aggressive withdrawal rate. It can certainly be a good starting point, so long as you annually review where you are to make sure any withdrawals are sustainable.

The 4% rule was devised by US financial planner Bill Bengen in 1994. Bengen backtested a portfolio of 50% in US equities and 50% in US bonds over 30-year rolling periods from 1926. He found that withdrawing 4% a year, increasing it in line with inflation, would see the pot size last at least 30 years.

Bengen recently published new research that examined whether investors with a more diversified portfolio, containing seven asset classes rather than just shares and bonds, could be more adventurous with how much they withdraw.

This new research (30 years on from the original analysis) suggested that 4.7% is the new safe withdrawal rate. We took a deep dive into this new research in an On The Money podcast episode, which you can watch/listen to here.

However, bear in mind that this isn’t financial advice and is only intended to be food for thought. Ultimately, how much money to withdraw is a personal decision and everyone in retirement has their own set of unique circumstances.

It’s important to regularly review the amount you’re withdrawing to check that it fits with the things you want to do in retirement, and to examine how the investments are performing.

Having a cash buffer is one way to give a pension portfolio ample time and opportunity to recover.

The idea is to keep roughly two or three years’ worth of expenditure in cash. If a notable stock market slump occurs, withdrawals from your investments can be paused and the cash bucket utilised. This gives the pension portfolio a better chance of recovering because money hasn’t been taken out of it.

If possible, top up the cash, so that you are protected again if further sizeable market falls happen in future.

This cash could be held in a money market fund, which invests in high-quality bonds that are due to mature soon, meaning that investors can get a modest income without taking much investment risk.

In interactive investor’s latest ii Top 50 Fund Index, six money market funds appear in the ranking of the 50 most-bought funds, investment trusts and ETFs in the fourth quarter of 2025.

They are Royal London Short Term Money Market (accumulating)

Royal London Short Term Money Market (distributing)

Amundi Smart Overnight Ret GBP H ETF Acc CSH2

Fidelity Cash Fund, Legal & General Cash Trust and Vanguard Sterling Short-Term Money Market.

Let’s now move on to the different types of fund options to consider, as part of your wider research, on a post-retirement portfolio.

The hassle-free route is to focus solely on funds paying a monthly income. Around a decade ago there were only around a couple of dozen funds paying out monthly, but now there’s more than 150.

The downside is that there’s only a small number that solely invest in equities. Most monthly income funds invest in bonds or adopt a multi-asset approach, which means investing in both shares and bonds. For those in retirement, a balanced approach such as this helps to both protect and grow capital.

Bear in mind that some monthly income funds invest solely in, or have big weightings to, high-yield bonds, which is the risker end of the bond market.

With monthly income funds, the amount of income generated is based on the dividends or coupons that the underlying holdings have paid each month. Therefore, the income can vary, but to counteract this, most funds smooth the dividend payments into 12 equal amounts, holding back some income in good months, which is then used to top up leaner periods. Any excess cash left over at the end of the year is handed back to investors.

Two funds endorsed by our fund analyst team that provide monthly income are Man Income and Artemis Monthly Distribution.

Man Income, which has a current yield (as at 23 January 2026) of 4.3%, invests in UK stocks with above-average dividend yields.

Artemis Monthly Distribution, a multi-asset fund, invests around 60% in bonds and 40% in shares, and has a yield of 3.6%.

However, it’s prudent to avoid betting the house on income strategies. Given that average life expectancies are in the mid 80s, a pension portfolio also needs exposure to growth-producing assets to strike an appropriate balance.

Having exposure to growth strategies will help give your portfolio greater diversification, and it also reduces exposure to bonds, assuming you can tolerate the higher volatility associated with shares.

Most income funds tend to aim to generate capital growth, as well as income. However, some put more focus on income generation. As ever, it’s a case of looking under the bonnet to find out which approach is being taken.

an investment trust that has raised its dividend every year since 1966, aims to deliver a mixture of growth and income. Since 1991, it’s been managed by Job Curtis, who focuses on dependable dividend payers in the FTSE 100 index. It is regarded as a ‘Steady Eddie’ due to its conservative approach and its yield is currently 3.9%.

Another fund endorsed by our fund analyst team is Artemis Income, which also focuses on UK companies producing excess cash to sustainably pay dividends.

However, there’s a potential downside if you opt for the convenience of taking a regular income from income-producing investments, as those who buy funds focusing more on capital growth could benefit from higher overall total returns.

Yet adopting this approach means the income would need to be achieved by selling fund units rather than relying on income generated from the underlying investments in the fund.

Selecting funds or investment trusts just because they pay income out in a particular month shouldn’t be the main reason you buy those investments.

Given that most funds and trusts pay quarterly or twice a year, you could manually spread the income produced into regular payments throughout the year. Not focusing solely on when dividends are paid or monthly income funds gives you a much bigger pool to fish in.

One way to achieve a mix of growth and income is to consider investment trusts. As seasoned investors can testify, the investment trust structure can work very well for investors looking for a regular income stream.

This is because one of the advantages of investment trusts is their ability to squirrel away income for a rainy day. Up to 15% of income generated each year from underlying investments can be saved, in what is called revenue reserves. In contrast, funds have to distribute all the income generated by the underlying investments each year.

When there’s a period when income from underlying investments dries up, which happened during the Covid-19 pandemic and the financial crisis, investment trust boards can utilise those reserves and top up shortfalls.

This is why there are an impressive number of “dividend hero” investment trusts, which have raised their dividends year in, year out, for long periods.

Ten dividend heroes – City of London Ord CTY

Caledonia Investments Ord CLDN0

The Global Smaller Companies Trust Ord GSCT0

F&C Investment Trust Ord FCIT0.

have consistently increased payouts for more than 50 years.

Bear in mind that for some dividend heroes, the dividend yield is fairly low, which reflects the trusts’ broad emphasis on growing the capital and raising the payout, rather than offering a high level of income. Also, in the case of Murray Income, it’s worth noting that the trust’s management firm is set to change from Aberdeen to Artemis.

For those who are happy to prioritise income and are seeking a high income of over 6%, there are fewer options, and they are more adventurous.

For equities, you could consider the small number of funds that artificially boost their dividend yields through a special technique that involves selling derivatives to other investors.

Under this strategy, the fund manager agrees to share any future capital gains with a third party. A fee is paid for the agreement, which creates immediate, up-front income. This can be distributed to fund investors as a stream of income.

The downside is if the fund’s holdings rise in value, as some of that gain goes to whoever bought the derivative. Therefore, such funds lag the pack in rising markets.

However, seeing as the buyer’s paid up front, the risk of not being able to deliver a chunk of extra income is limited.

Three UK equity income funds offering an income boost are Schroder Income Maximiser, Premier Miton Optimum Income and Fidelity Enhanced Income. The trio typically yield between 6% to 7%.

However, as these funds are specialists, they would work better as smaller weightings in a portfolio, and in combination with more conventional funds and investment trusts to deliver a mixture of growth and income.

For bonds, it is the riskier end of the market, high-yield corporate bonds and emerging market debt, that offers the best chance of the highest income.

Elsewhere, some infrastructure funds and investment trusts offer yields above 6%. However, this is a more specialist area and higher risk, resulting in sizeable losses for many names in recent years as interest rate rises hit this investment area.

The idea is to keep roughly two or three years’ worth of expenditure in cash. If a notable stock market slump occurs, withdrawals from your investments can be paused and the cash bucket utilised. This gives the pension portfolio a better chance of recovering because money hasn’t been taken out of it.

If possible, top up the cash, so that you are protected again if further sizeable market falls happen in future.

The elephant in the room is that if the market falls for three years and you use all your cash reserves, you will have to sell shares to withdraw your 4% and also sell shares to top up your cash reserve, all at lower prices.

How low is the gamble.

© 2026 Passive Income Live

Theme by Anders Noren — Up ↑