ETF’s with dividends re-invested

Investment Trust Dividends

ETF’s with dividends re-invested

We have some exciting news to share! The Motley Fool UK has now become The Twelfth Magpie — an independent, UK-owned company, led by our long-serving UK management team — Mark Rogers, Chris Nials and Heather Adlington. In practical terms, it’s the same team you know, now fully focused on serving our UK readers and members.

Just as importantly, our approach remains unchanged: long-term, jargon-free, and on your side. This site is our new home, and there will be extra tweaks made across the coming few days as we settle in. So if anything looks a little off, please bear with us!

How can these 3 iShares ETFs keep delivering huge dividends? Here’s your answer!

Exchange-traded funds (ETFs) can provide a reliable and large passive income over time. Royston Wild explains how — and picks three top ones to consider.

Posted by Royston Wild

Published 7 June

You’re reading a free article with opinions that may differ from The Twelfth Magpie’s Premium Investing Services.

Exchange-traded funds (ETFs) can be powerful weapons if you’re seeking a dependable passive income. Creating a diversified portfolio that can protect dividends from temporary shocks is essential. An ETF can help investors achieve this simply and effectively.

Dividends are never guaranteed, even from these types of funds. But their diversified approach — with holdings that can be spread across different sectors, regions, share types, and even asset classes — can greatly reduce this risk.

But which ETFs should you buy to target a long-term passive income? Here are three top ones to consider from iShares.

Real estate investment trusts (REITs) can be among the most reliable dividend sources out there. One reason is their focus on property shares, which generate a steady stream of rental income that can be distributed.

But these particular stocks have a trick up their sleeves. Unlike other real estate businesses, these firms are obligated to pay at least 90% of annual rental earnings in dividends. That’s in exchange for tax breaks.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

Shareholder payouts can be still volatile during economic downturns, however, when tenants might miss rent payments. The iShares MSCI Target UK Real Estate ETF (LSE:UKRE) spreads this risk out. How? It invests in 25 different REITs.

That’s not all. The trusts it holds are spread across a variety of cyclical and non-cyclical industries. The result? It offers a blend of stability and the potential for strong income growth. Its dividend yield today is 6.3%.

The iShares World Equity High Income UCITS ETF (LSE:WINC) doesn’t focus on ultra-reliable property stocks. But it offers stability in other ways, namely by enjoying exposure to dozens of global dividend-paying shares.

This can sometimes deliver even greater resilience. In its own words, the fund’s objective is

To generate income and capital growth with lower volatility than developed market equities.

In total, this ETF has holdings in more than 500 dividend-paying shares. On the downside, it’s not immune to stock market downturns that can see it fall in value. However, its exposure to cash and US government bonds cuts this risk and improves dividend visibility.

The dividend yield here is 9.7%.

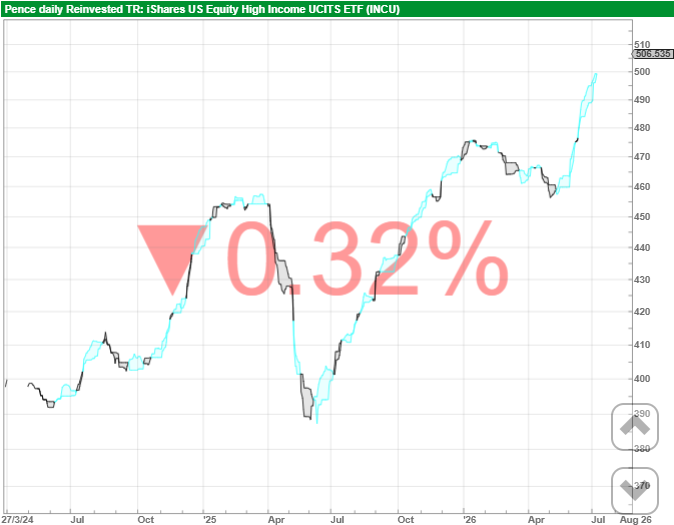

The iShares US Equity High Income Active (LSE:INCU) has more regional concentration than global funds. That’s the bad news.

The good news? Its portfolio is still brilliantly diversified to generate a large and reliable passive income. The more than 300 companies it holds span sectors as diverse as information technology, healthcare, banks, and consumer goods. Some of the fund’s capital is also tied up in cash for extra resilience.

Furthermore, though it focuses on US stock market shares, almost all the companies are multinational businesses. The fund may fall if broader appetite for Wall Street shares dips. But this is less likely to hit dividends.

The forward dividend yield with this ETF is 8.5%.

Thursday 11 June

3i Infrastructure PLC ex-dividend date

Capital Gearing Trust PLC ex-dividend date

CT UK Capital & Income Investment Trust PLC ex-dividend date

Henderson High Income Trust PLC ex-dividend date

JPMorgan US Smaller Cos Investment Trust PLC ex-dividend date

Mercantile Investment Trust PLC ex-dividend date

Pacific Assets Trust PLC ex-dividend date

Schroder Real Estate Investment Trust Ltd ex-dividend date

Scottish Mortgage Investment Trust PLC ex-dividend date

Worldwide Healthcare Trust PLC ex-dividend date

There is £1,056 for re-investment, 1k to buy more shares in AIRE for it’s yield as it’s currently unloved by Mr. Market.

Investor Edition

Fund Profile

Disclosure – Non-Independent Marketing Communication

This is a non-independent marketing communication commissioned by Invesco Bond Income Plus (BIPS). The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

BIPS continues to issue new shares for its high-yielding portfolio.

Overview

Invesco Bond Income Plus (BIPS) is managed by Rhys Davies who aims to deliver a significant yield pick up over gilts and cash without taking imprudent risks. Rhys invests in the high yield bond space, and will delve into subordinated bank debt and other corners of the market, but always with a keen eye on valuation to ensure he isn’t taking excessive credit risk to deliver the income. BIPS yields 7.1% at the time of writing, and has raised its dividend for five consecutive years despite the manager being cautiously positioned for most of this period .

Rhys continues to view the market overall as quite expensive, leading to the continued defensive positioning. He has a relatively high proportion of the fund in investment-grade debt rather than high yield, and has let Gearing fall to slightly below the usual 10-15% range. Nonetheless, the dividend target for 2026 has been held at the same level as last year. The trust has healthy revenue reserves, and Rhys is confident of hitting this target from current year income anyway, despite his defensive positioning.

BIPS has continued to see strong demand for its shares, even during the volatility surrounding the outbreak of war in the Gulf. It has traded on a premium for most of the past three years, and issued large amounts of new shares, including a placing and retail offer in February. At the time of writing, the premium was 1.8%. BIPS is the largest trust in the AIC Debt – Loans & Bonds sector, and this helps it offer the lowest charges by some distance.

Analyst’s View

We think BIPS should have strong appeal for the typical investor looking for an income. The yield is significantly higher than that on offer from gilts or cash, but the prudent approach to risk should limit the volatility in the value of the portfolio and help preserve the real value of the capital. The trust has held or raised its dividend each year for over a decade, and with healthy revenue reserves is in a strong position to continue this record. When we do eventually see a sell-off in credit markets, which tends to occur when equity markets sell off too, Rhys will be in a strong position to recycle some lower-risk positions into higher-yielding credits and boost the income once more. BIPS’ size brings low charges and liquidity in the shares, which helps make it an easy option for investors seeking a higher yield.

In the short term, the war in the Gulf has led to the market expecting modest rate hikes in the UK over the coming months. This would hit bonds’ capital value, but on the other hand would mean higher yields should be available in the market. BIPS is positioned to take advantage if this happens, with a defensively positioned portfolio which should limit the hit to the NAV and allow Rhys to add to higher yielding investments. We would add that one of its strengths is the geographical diversification into Europe and the US which means it is not overly sensitive to UK policy or indeed the health of the UK economy. With the UK looking exposed to energy prices and enjoying some Italian-style politics, although sadly not the weather or the ice cream, this is another defensive feature we find attractive at this point in time.

Brett Owens, chief strategist of the Contrarian Income Report high-yield investing service.

Imagine what an 11% dividend could do for you in this volatile market…

That’s $917 every month on a $100k investment …

$22,000 in yearly dividends on $200k …

Invest half a million and you’re looking at $55,000 per year.

That’s a decent middle-class income in many parts of the US!

Got more? Great!

A $1-million buy-in would land you $110,000+ in dividends every single year!

You can see where this is going …

No more grinding down your principal by withdrawing some “magic” percentage year after year …

No more worrying about running out of money in retirement …

No more sleepless nights wondering which way the market winds will blow next.

Heck, a lot of my readers could start living off dividends alone, without any of these concerns!

This 11% Yielder Is Poised for Stock-Like Gains

I’m also imploring readers to grab this fund now because it’s set up for big capital gains as the Fed continues to cut interest rates.

Why am I so confident that will happen? Because the new Trump-appointed Fed chair, Kevin Warsh, is certain to work with the administration to bring rates down. And likely faster than most market-watchers expect.

That’s great news for this 11%-paying fund’s holdings: high-yield credit, a.k.a. corporate bonds.

Because when interest rates move lower, new bonds will be issued at lower rates, driving up the value of our 11%-payer’s already issued bonds.

As that happens, our high-yielding pick will jump from relative obscurity to the top of many “first-level” investors’ buy lists.

The bottom line:

We’ve got an 11% dividend here, and a shot at price upside, too!

Even better, there’s something else you should know …

In addition to its monster 11% yield, this fund has a history of actually growing its payout: Since its inception around four years ago, it has already increased its regular dividend by 8% and has paid two special dividends, too!

A Dividend Hike Plus 2 Big “Specials”

Sure, these special dividends and raises are great news for current investors in the fund. But there’s something else few people realize about them …

They don’t typically show up in the yield calculations on the free stock screeners, like Yahoo! Finance and Google Finance.

This means that the fund’s 11% stated yield could turn out to be an undercount.

Now I’m not going to claim this is the norm for the fund. Fact is, no one can say for sure what management will do when it comes to future dividend hikes and special payouts.

But this track record shows that management isn’t afraid to drop a nice bundle of extra cash on shareholders when the time is right. So we can assume our buy now locks in an 11% “starter yield,” with plenty of potential to move higher.

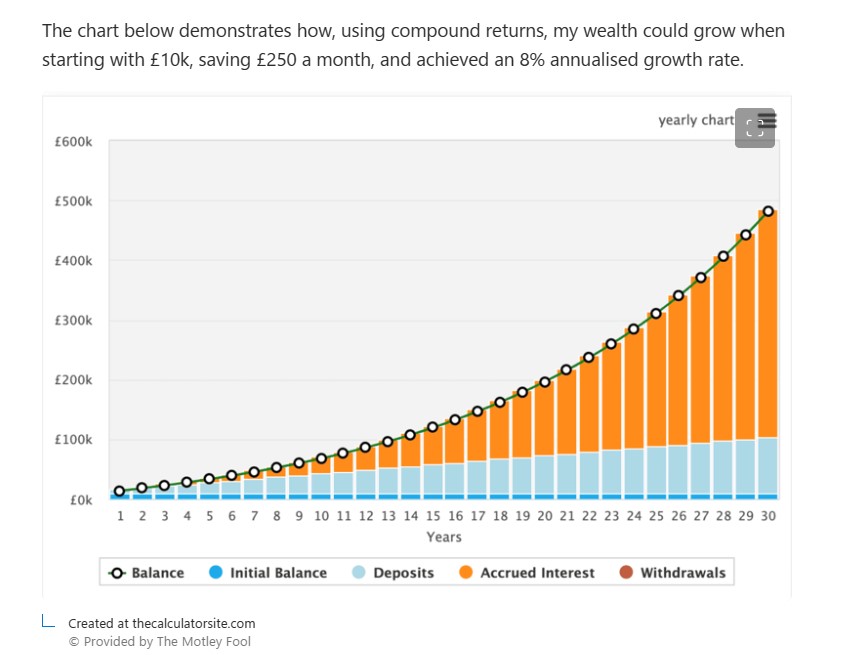

If you can re-invest your dividends at 7% or above, you can double the capital in your Snowball every ten years, so in twenty years your yield should be 14%+.

Better if you have longer before you want to drawdown and better if you can cash add to your Snowball.

We take arms against a field of sacred cows.

Thomas McMahon

Updated 03 Jun 2026

This is not substantive investment research or a research recommendation, as it does not constitute substantive research or analysis. This material should be considered as general market commentary.

Fund managers have lots of advantages over retail investors: no day job to take their time away from investing, great access to information and research, other investors around them to feed them ideas and challenge them, and brightly coloured Lambos to make them feel better after a tough day. This is all well known. However, the professionals don’t have it all their own way. Retail investors have a lot of advantages too, which receive less attention. In fact, we think the humble retail punter may even be better placed to make active management pay off.

There’s a fair amount of academic research kicking about which claims to show that active management doesn’t outperform, because less than 50% of active funds outperform an index over a given time period. A fundamental problem with all such studies is that they aren’t really looking at what they purport to be. Fund managers are not perfectly free actors making whatever decisions they like to try to outperform the index over a given time period — they don’t represent ideal ‘active management’. In fact, they are severely constrained by a number of institutional, psychological, and regulatory factors, all of which the self-directed investor can avoid.

The framework that has been built up within and around the asset management industry has some perverse consequences. Professional fund pickers want managers who have a consistent style and approach. In this world, style drift is the worst sin. However, the most obvious example of style drift is the career of the world’s most famous investor, Warren Buffett. Buffett’s initial approach to investing was very focussed on finding cheap companies, businesses with real assets which could be bought at a substantial discount to their fair value. Over the years, his portfolio became more focussed on finding cash-generative businesses with strong competitive positions — it’s certainly hard to classify Berkshire Hathaway’s top holding, Apple, as a value company.

There are a number of reasons this might have happened. Buffett may have decided there was a better method of investing. It may be that as Berkshire grew, he was more constrained in the businesses he could invest in. It is certainly true that the economy has changed over the 60 years since Buffett began running Berkshire. Whatever the combination of reasons for the change, it has clearly worked well for Buffett’s investors, who enjoyed 19.7% annualised returns under Buffett’s tenure (last year he handed the keys over to Gregory Abel), compared to just 10.5% for the S&P 500 over this time frame.

There are huge dangers to sticking to the same investment approach, particularly over the ultra-long term. The past decade has seen some quality growth managers run into real trouble as artificial intelligence has upended many assumptions and business models. We saw a similar phenomenon around 15 years ago when quality growth managers in Asia struggled after the rapid emergence of the Chinese tech and ecommerce industry, with Tencent and Alibaba coming out of nowhere to top the indices. In general, a quality growth approach is likely to do better when industry dynamics are stable, as recurring revenues are more likely to recur in such circumstances. Other approaches might work best in different circumstances.

However, there are strong incentives for fund managers to stick to the same investment style, even if it stops working. Managers will usually have been employed on the understanding from their employer that they will invest in a certain way, and the infrastructure around them will be set up to facilitate this, be it the analysts who are hired, the teams that are formed, or the research that is bought from outside analysts. Then, perhaps more importantly, there is the marketing angle. Fund managers have to be able to sell what they are doing to the end investor. This involves a lot of work to explain how and why they take a certain approach and how that is expected to deliver outperformance. Over time, investors will come to live through the ups and downs with the fund manager, if they are successful, watching periods of underperformance or stock picks that aren’t working transform into prolonged periods of outperformance or those companies turning good. The longer this goes on, the harder it is to do something different without sounding like you are contradicting what you have been telling everyone for years about the best way to invest and without looking foolish. The best managers will find a way to finesse an evolution of their strategy, but that is a tough thing to achieve successfully from a messaging point of view, and requires ace marketing skills, not investing skills, and support from your employer.

As a retail investor — or ‘punter’, in the slightly dismissive industry jargon — you are completely unconstrained by these considerations. Unless you are a particularly boring pub companion, you have no reputation or image as a particular type of investor to maintain. If you want to pivot, you go, girl. Funds are expected by professional investors to behave predictably and follow the same strategy over time, but you can be sure that no matter how much their sales talk focusses on diversification, part of the reason is so that professional investors in funds can switch horses when they think the time is right. Fund managers have the least freedom of all in this chain!

This isn’t only about a change of investment style. Turning back to the recently retired great, Warren Buffett, he made some oil and gas investments for Berkshire Hathaway shortly after the Russian invasion of Ukraine in 2022. If you were to classify this trade, perhaps it would be opportunistic rather than value or quality growth? In any case, he clearly wasn’t afraid to make a big move based on newsflow and a changing environment, something that might be impossible for most fund managers without his reputation and working with a much more constrained framework. In that light, it is interesting to note how few global equity managers overweighted NVIDIA after the launch of ChatGPT. As a retail investor, you have the licence to make a call when something new comes up, without having to worry about what you have told other people about how you invest.

In a recent strategy article, we analysed how the market indices most often used by professional fund managers as benchmarks are deeply flawed, and represent the outcome of a series of choices made by index providers to aid their usability and to boost sales, rather than reflecting the actual economic value of the businesses that are listed on them.

Benchmarks can create perverse incentives. For a fund manager with a restricted mandate, outperforming in a falling market might represent success. But taking a step back, if a manager was convinced their market is going to fall, if they were managing their own money, they might sell out rather than looking for the stocks which will fall the least. Within the framework of the modern wealth management industry, a UK small-cap manager who went 50% to cash would be deeply unpopular, as the professional investor wants to make the asset allocation decision themselves. Moreover, the professional investor is highly unlikely to make such a bold asset allocation, as the model portfolio services, which increasingly dominate the professionally managed industry, take long-term structural asset allocations, and adjust tactically around them, which is precisely why an equity manager going to cash is unwelcome.

Additionally, managing to a benchmark means excluding vast swathes of opportunity, with the ultimate justification being to make portfolio behaviour more able to be modelled, something that a truly active investor wouldn’t be considering. Does it make much sense for an investment in UK companies to be limited to listed businesses only, especially with fewer companies going public than in the past? Does it make sense for a mid-cap manager to exclude larger small caps, or sell a stock when it enters the large-cap segment, even if they think its potential returns are just as attractive? Only within an institutional or marketing framework that adds other objectives alongside maximising returns.

‘Time in the market beats timing the market’ is the old industry adage. What it really means is something like ‘timing the market poorly results in a worse outcome than remaining invested’, which is trivially true, and something else like ‘it is impossible to time the market’, which is simply false. Godwin’s Law says any argument on the internet will result in a reference to Hitler, and perhaps we need the equivalent for investing to note that any argument about investing will result in a reference to Saint Warren, before noting that one of the secrets to Buffett’s success later in his career has been using his estimate of market valuations to manage his cash position aggressively. Timing the market is hard, but so is stock-picking. Frequent trades will have a cost, so they should be minimised. But neither fact means market timing shouldn’t be a tool in the average investor’s kit.

This isn’t a suggestion to trade in and out like a White House-connected oil trader – none of us has that sort of access to information. Getting market timing consistently right is going to be extremely difficult, and so it is probably best used in moderation. But anyone who stared the pandemic in the face in February 2020 and didn’t take down their exposure to equities, missed a generational opportunity to boost their relative returns. If you had sold all or some of your equities when the pandemic was looming, and then bought back in to a passive tracker any time before July 2020 and remained invested, making no other active decisions, you would still be ahead of the index today. Market timing is an incredibly powerful tool, and lots of fund managers in the investment trust sector use it when it comes to gearing, while many others manage their cash position actively too, but they are relatively constrained in their use by a number of factors that private investors can look through. Fund managers have a mandate with an objective; they frequently have to bear in mind sector rules too, and then on top of this, expectations they have built with investors and employers that mean selling down and going heavily into cash is unlikely to go down well.

Source: Morningstar

Past performance is not a reliable indicator of future results.

We think private investors have three major advantages over professionals: the ability to be truly flexible when it comes to investment style and strategy, the ability to be benchmark-unconstrained and invest on- and off-market, and the ability to sell and sit it out for a bit. None of these is risk-free, and all are tools which need to be used judiciously. Ultimately, we think they are just features of truly active management and reflect being free from the institutional and marketing restrictions that fund managers have to deal with.

All can be the source of failure as well as success, just like a more restricted approach to active management, and not everyone wants to take this responsibility on themselves. Luckily, the investment trust sector includes a number of trusts which use these features to the full, reflecting in most cases what could be considered a family office approach to investing, or almost a halfway house between outsourced investment management and a personally managed portfolio. We think these trusts capture how a truly active investor might manage their own money.

One we would highlight is Majedie Investments (MAJE), which was established to manage the wealth of the Barlow family, who still own about half the shares. MAJE has long had a distinctive approach, and in 2023 took a different direction, being managed to a liquid endowment strategy by Marylebone Partners (now part of Brown Advisory). MAJE is benchmark-free with external allocations to specialist managers covering mainstream equity markets, and even in these allocations, can be highly specialised. This is accompanied by special investments in carefully selected co-investments, special purpose vehicles, or thematic situations, all expected to deliver a higher return profile of at least 20% IRR, but which must be monetised within a maximum of three years. It really is a unique portfolio, and a truly active approach to generating its objective of 4% above CPI. We will discuss the portfolio in greater detail in our upcoming note, click here to be notified when it’s published.

It’s not quite a family office, but Global Opportunities Trust (GOT) surely owes some of its independent character to the fact that manager Sandy Nairn owns c. 16% of the shares, with his wife owning an additional 2.5% (as of 31/12/2025). This has to help explain how Sandy and his co-managers are bold enough to hold 40% of their portfolio in cash or equivalents. The managers view markets as unattractively expensive, and aim to reinvest when these valuations eventually deflate. This approach means the trust will inevitably lag if markets continue to grind higher, but if we do see a major sell-off, there is the potential for investors to add to it now to remain ahead of global benchmarks for some time to come. GOT also has a highly distinctive and truly active approach to its stock portfolio, with only 23 positions currently, and each held at equal weight, with absolutely no attention paid to their weights in global stock market indices. We have recently published a new note on GOT, click here to read it.

The Salomon family still own c. 50% of the voting shares in Hansa Investment Company (HAN), and 33% of the total shares. HAN is another highly distinctive portfolio managed on a truly active basis. Country-specific and thematic funds are invested in via active managers where the team think they can add value, and via passive funds when they think alpha is challenging to generate. The team also invest in direct-listed equities and in private assets, along with a highly eclectic pool of diversifying assets in which hedge funds sit alongside trend-following strategies and other investments, all designed to offer diversification and offset market exposure elsewhere.

Source: Hansa Capital Partners

Past performance is not a reliable indicator of future results

The family ownership means the trust is managed with the aim of generating long-term growth on an intergenerational scale without reference to market benchmarks, career risk, or short-term marketing goals, with full freedom. The sale of Wilson Sons by Ocean Wilsons and the combination of Hansa with the latter last year have led to a significant build-up of cash in HAN, which means we think the wide discount of 40% looks particularly attractive.

Brett Owens, Chief Investment Strategist

Updated: June 2, 2026

Inflation forever?

The fear has taken root seemingly everywhere: the media, the bond market, the futures market. They’ve all bought into the idea that scorching price hikes (and high interest rates) are here to stay.

If you’re like me, my fellow contrarian, you’re paying attention—but you also know something else about times like these: When everyone expects something to happen, something else usually does.

That’s what I want to talk to you about today. Because all the data I’m watching tells me the crowd is wrong: It’s deflation, not inflation they should be focused on.

Falling rates, not rising rates.

This disconnect has put some top-quality “preferred” (hint!) 7%+ dividends on the outs, giving contrarians a chance to buy cheap and “lock in” their high yields. Let’s get into it.

Inflation “Groupthink” Runs Deep

Let’s start where everyone looks when talking inflation and rates: the bond market.

The 10-year Treasury yield sits just under 4.5%. The 30-year yield is right around 5%, where it’s been for weeks. That’s a headache for anybody looking to borrow money (including Uncle Sam, with his already bloated credit card!).

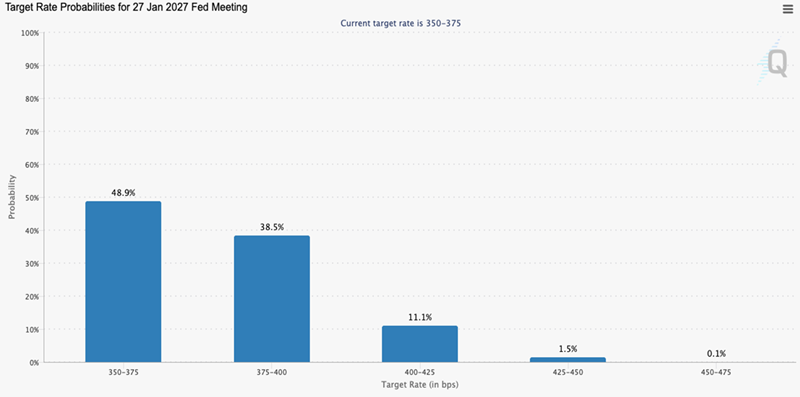

Futures traders, too, have bought in. They see the Fed keeping rates where they are for the next six months or so. Then, by a slim majority, a rate hike in January:

Source: CME Group

That looks like a pretty airtight argument for higher rates, right?

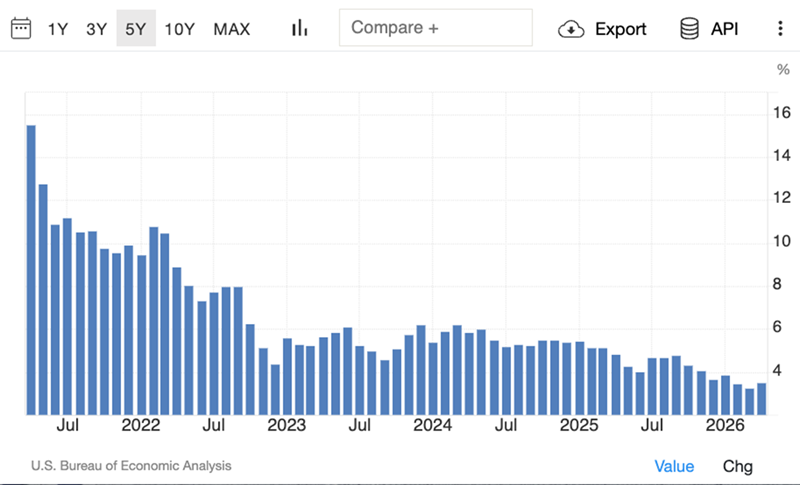

Except, well, here’s the other side of things, starting with wage growth, which has been trending one way since the pandemic: down.

That’s clearly deflationary—and April’s rate of 3.6% fell behind the CPI. When that happens, people do one thing: cut back. The cure for high prices really is high prices!

Then there’s AI, which is an anchor on hiring. According to an April 2026 Goldman Sachs study, AI slowed monthly payroll growth by 16,000 jobs in the US over the preceding year. But the numbers don’t really matter here. Just talking about replacing workers with robots will cause some folks to sit on their wallets.

Iran? Neither it nor the US can afford to let this situation fester. Sooner or later, the strait will reopen. The oil will flow—and inflation will ease when it does.

And let’s not forget, we’ve got Kevin Warsh settling in at the Fed. The administration wants him to cut rates, and he’ll likely do so as soon as he can justify it.

But even with all this, investors still think inflation is here for the long haul. Let’s call that out with two 7%+ paying funds—including one with a payout that’s growing.

Inflation Fears Put These “Preferred” 7%+ Dividends on Sale

A couple weeks ago, we highlighted corporate-bond closed-end funds (CEFs) as timely plays on this situation, and they still are. Now let’s peer into another discounted corner of CEF-land: preferred shares.

The best way to think about preferreds is as stock/bond hybrids. They trade like a stock, and they pay dividends. But like a bond, they tend to trade around a par value, and the payout is usually fixed.

One more thing about those payouts: They’re typically a lot higher than those on a company’s common shares—regularly two or three times higher.

And like bonds, preferreds—or CEFs that hold them—are oversold today. That’s because while bond yields have risen with inflation fears, their prices have fallen (because prices move inversely to yields).

But as is the case with bond CEFs, these discounts have gone too far with preferred funds. That’s our cue.

A “Hybrid” Fund Trading for 12% Off (and Yielding 7.7%)

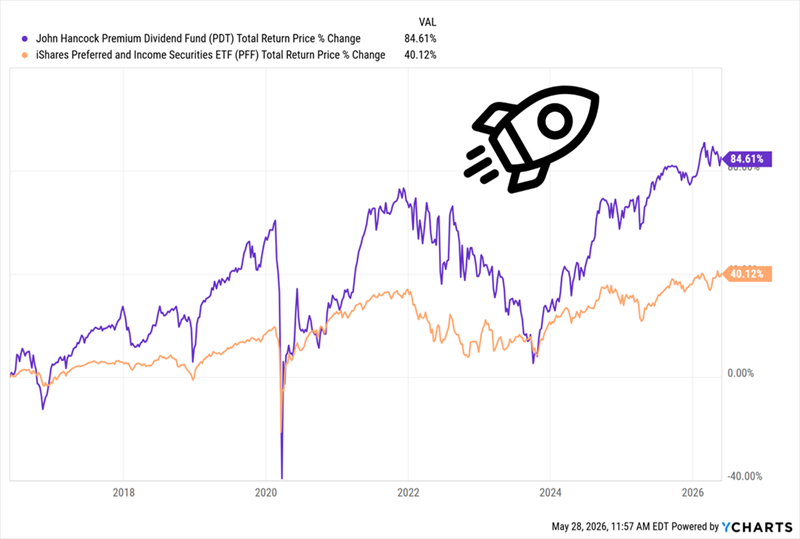

The 7.7%-yielding John Hancock Premium Dividend Fund (PDT) is a good place to start with preferreds because it’s a “hybrid,” investing 43% of its assets in common stocks, 30% in preferreds and 26% in bonds and other income securities.

That strategy has paid off, with the PDT’s common shares helping power the fund’s total return (in purple below) past the preferred-stock benchmark iShares Preferred and Income Securities ETF (PFF) in the last decade:

PDT’s “Hybrid” Portfolio Gives It a Boost

PDT also boosts its returns (and by extension an investor’s dividends and preferred-stock exposure) with leverage, to the tune of around 34% of its portfolio.

That would send many vanilla investors to the exits, with today’s interest rates. But we know this is a feature, not a bug: As rates fall, PDT’s borrowing costs will, too—as that rate decline boosts the value of its fixed-income portfolio.

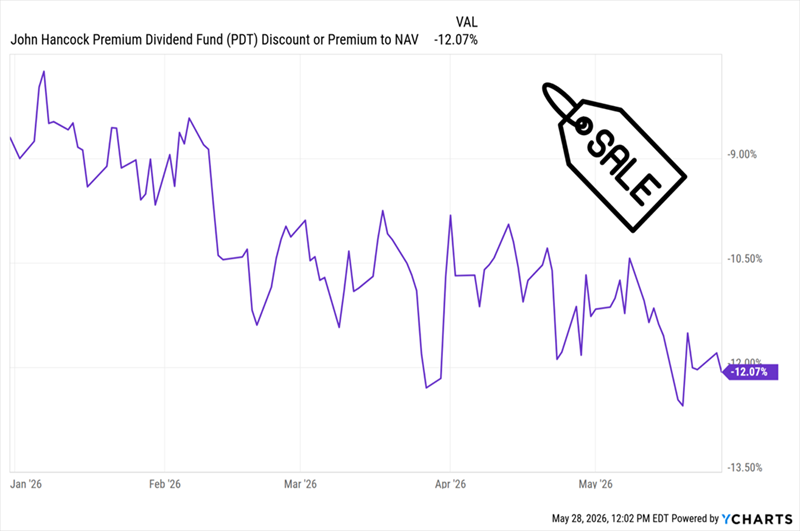

Meantime, this smartly built fund is available at a 12.1% discount to net asset value (NAV, or the value of its underlying portfolio) as I write this. You can see that discount widening as the “inflation forever” mindset took hold this year:

PDT Gives Off a Clear Contrarian Buy Signal

That’s a particularly sweet deal when you consider that PDT has, on average, traded around par over the last five years. A discount this deep is rare, and I don’t expect it to last in light of the steady 7.6%-yielding (and monthly paid) dividend PDT offers.

This 8.6% Dividend Is On a Growth Tear

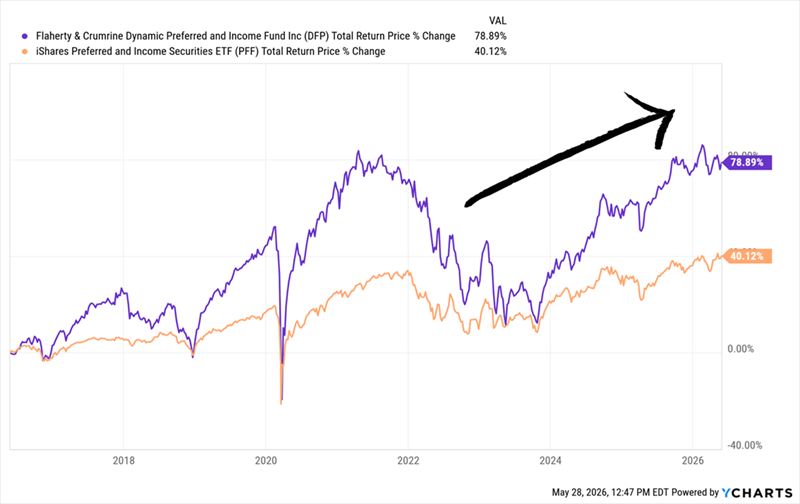

The Flaherty & Crumrine Dynamic Preferred & Income Fund (DFP) is a “purer” play on preferreds than PDT, with 51% of its portfolio in these shares as of February 28. The rest is 45% bonds and around 4% convertible bonds and cash.

But even without PDT’s common-stock “afterburner,” DFP (in purple below) has still cleanly beaten its benchmark ETF, PFF, over the last decade, by nearly the same margin.

DFP Easily Beats Its Benchmark

This performance shows why “human” preferred-fund managers won’t be replaced by AI. The preferred market is small, and personal connections are key to getting in on the hottest new issues. And F&C, which has been in fixed income for more than 40 years, has one of the deepest contact lists out there.

The fund’s strong return also supports its 8.6% dividend (again paid monthly), which has grown since DFP emerged from 2022’s inflation spike.

Management clearly sees through the current rate scare: It delivered a special dividend at the end of last year and hiked the regular payout again with the latest payment:

DFP’s Dividend Grows—and Shrugs Off the Fearmongers

Source: Income Calendar

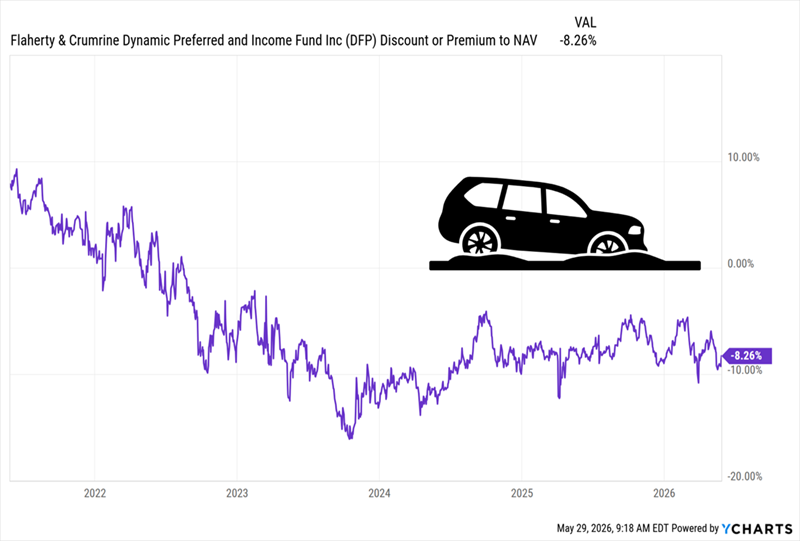

That’s great for DFP shareholders, but what management is likely really trying to do here is narrow the fund’s discount, which has slumped to 8.3% in the last few years and has been stuck there since. Special payouts and dividend hikes are great ways for them to signal confidence and draw more buyers in.

DFP’s Discount Is Spinning Its Wheels (for Now)

My prediction? They’ll be successful—and the fund’s high, and growing, monthly payout will put a floor under DFP’s discount and let investors pocket the fund’s growing income stream in peace.

Then, when today’s inflation scare ebbs, yields on existing fixed-income assets will slide, increasing the value of DFP’s portfolio and pushing its discount back toward par, where it was before the 2022 mess.

An 8.6% Payout Is Fine … But It Pales Next to a 11% Monster

What now for central banks as higher oil prices driven by the Middle East conflict create a stagflationary shock for the global economy ?

Jumana SaleheenVanguard European Chief Economist

Shaan RaithathaVanguard Senior Economist

“The Middle East conflict has thrust global central banks into uncomfortable territory. With oil prices elevated, central banks are forced to navigate the classic stagflationary shock – where inflation accelerates as growth slows.”

Jumana Saleheen

Vanguard European Chief Economist

The Middle East conflict has thrust global central banks into uncomfortable territory. With oil prices having risen above $100 per barrel since the start of the conflict and expected to remain elevated in the weeks ahead, central banks face a challenge: how to respond when inflation accelerates and growth slows simultaneously.

This is a classic stagflationary shock. Oil price increases hit consumers and businesses almost immediately. Drivers feel it at the pump, the cost of transporting goods rises and price pressures start to ripple through the economy. Households and companies forced to pay more for energy have less to spend and invest, dragging down demand and pressuring economic growth.

Central banks find themselves pulled in opposite directions. Higher inflation implies tightening, but slowing growth implies easing. This high inflation/low growth combination could weigh on both equity and bond prices.

The US Federal Reserve (Fed), European Central Bank (ECB), Bank of England (BoE) and Bank of Japan (BoJ) explicitly addressed the energy shock in their April policy statements.

The ECB, given its reliance on energy imports, is particularly sensitive to the shock. Although it isn’t our baseline case, this sensitivity could lead the ECB to reverse a rate-cut cycle that took the deposit facility rate from 4% to 2% between June 2024 and June 2025. We have already revised our policy outlook for the UK and now expect the BoE to maintain the bank rate at 3.75%, not make two quarter-point cuts in 2026 as we had anticipated before the conflict.

How our central bank forecasts have shifted

Notes: Forecasts are for monetary policy rates at year-end 2026. The Fed’s forecast reflects the rounded midpoint of the Fed’s target policy-rate range.

Source: Vanguard.

We assess US monetary policy to be near neutral, where the policy rate would neither stimulate nor restrict economic activity. Although we continue to expect one quarter-point rate cut in 2026 from the current 3.5%–3.75% range, risks have shifted towards a longer period of policy inertia while the conflict plays out.

The fundamental challenge is timing. While energy prices can surge overnight, monetary policy works with a lag. By the time higher interest rates soften demand – and, by extension, price increases – inflationary pressures may have already taken hold. The conventional wisdom has been to “look through” such supply shocks. But central banks can’t ignore potential knock-on effects. If higher inflation leads workers to demand higher wages, which feeds into broader price pressures, a temporary shock could become persistent. This is why we expect central banks to err on the side of caution in containing inflation.

The path depends on each central bank’s starting point. With inflation having tracked close to its 2% target in recent months and the labour market stable, the ECB finds itself in a stronger position to deal with an inflationary shock than in February 2022, when inflation was already at 6% and the labour market was tight. That recent history could keep the course of policy finely balanced between hiking and holding, with memories of surging inflation still fresh.

Assuming oil prices in a $90–$100 per barrel range and natural gas averaging €60/megawatt-hour for one to two quarters, we upgraded our 2026 ECB headline inflation forecast to 2.5% while lifting our forecast for core inflation – which excludes volatile food and energy prices – more modestly to 2.1%.

The BoE finds itself in more precarious territory. UK inflation has been above its 2% target for roughly five years. Core inflation remained above 3% in March 2026. Policymakers are still fighting the last battle even as a new one arrives. We recently downgraded our 2026 UK GDP forecast by 0.4 percentage points to 0.6%.

The US central bank has greater flexibility. As a net oil exporter, the US is experiencing a smaller shock overall. Higher oil prices hurt consumers but benefit domestic producers. While sticky services inflation and tariff pass-through create complications, the Fed can be patient. The dominant risk is that rates stay higher for longer, not that the Fed tightens policy.

The BoJ, meanwhile, is navigating upward price and policy normalisation rather than disinflation. Higher oil prices and yen weakness support that journey by lifting near-term inflation while strong wage growth underpins the broader normalisation narrative.

Stagflation is likely to be negative for both stocks and bonds. But assuming a limited duration for the Middle East conflict, we expect medium-term market dynamics to reassert themselves. We also continue to emphasise the potential for AI to be transformative and to spread its benefits throughout economies, as outlined in our 2026 annual outlook.

| Investor’s Daily brought to you by Nickolai Hubble | June 5, 2026 |

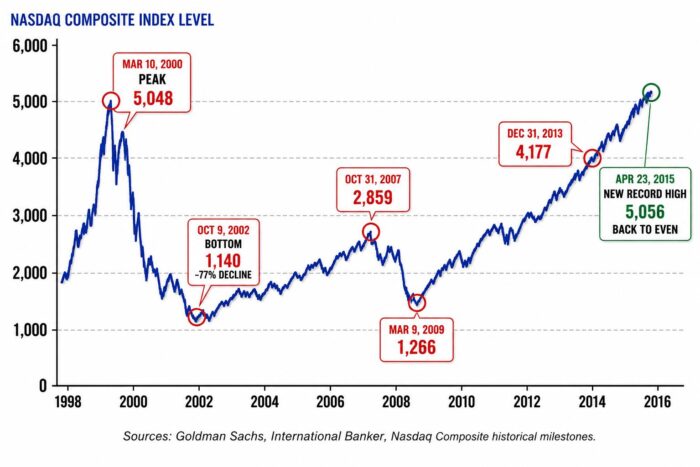

In March 2000, the dot-com bubble popped.

The companies were real… the technology was real and the internet turned out to be every bit as transformative as the believers said it would be…

But the revenues were not real… and that was enough.

It took 15 years for the market to fully recover.

A generation of investors who planned to retire in the early 2000s didn’t. They watched their portfolios collapse and went back to work.

Here’s the question worth sitting with today.

The technology is impressive. The potential is genuine. But when you follow the money — when you ask where the actual commercial revenue is coming from — the answer looks uncomfortably similar to the dot com era.

Microsoft has invested billions into OpenAI. OpenAI uses that money to buy computing power from Microsoft’s Azure platform. Microsoft books that as AI revenue.

The money circles back. The same capital, moving between two companies, being reported as proof that the AI boom is real.

In 2000, investors learned that “users” and “eyeballs” were not the same thing as revenue. The market had built trillion-dollar valuations on top of that confusion.

Right up until March 2000, the people buying believed the story. Build it and they will come. The valuations would be justified.

It never happened.

My colleague Jim Rickards believes we are in the AI version of that moment right now… and that by 26 August the AI Bubble will pop.

© 2026 Passive Income Live

Theme by Anders Noren — Up ↑