For the fourth year running, Kyle Caldwell has assembled a portfolio of funds aiming to generate £10,000 of income.

4th February 2026

by Kyle Caldwell from interactive investor

Related Investments

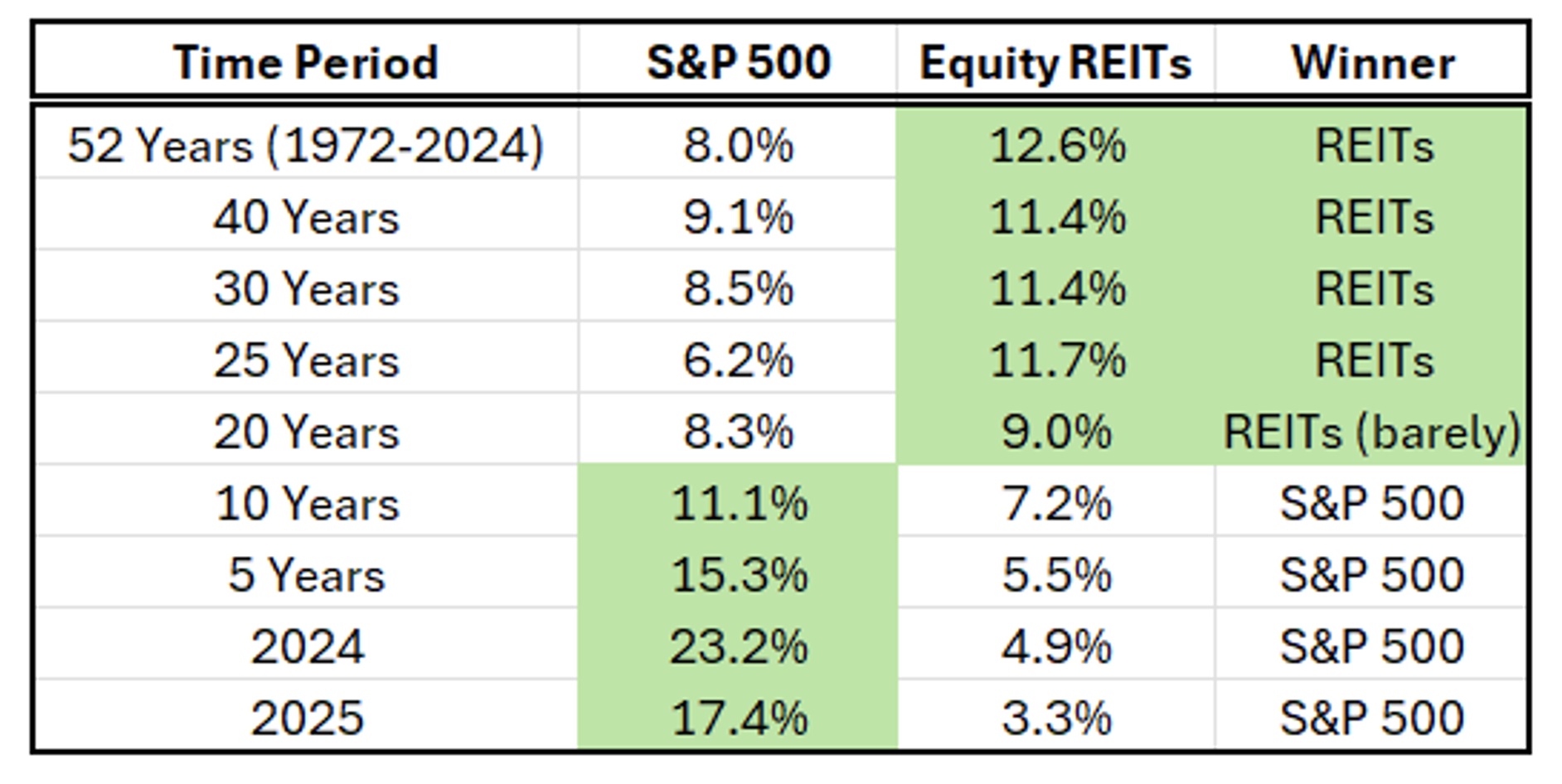

The UK stock market was one of the world’s top performers in 2025, with the FTSE 100’s return of 25.8% comfortably outstripping returns across the pond, with the S&P 500 delivering 9.3% in sterling terms.

As a result, UK funds had a strong year, particularly those with a focus on generating income, with the average gain of 18.7% for the Investment Association (IA) UK Equity Income fund sector ahead of returns of 15.4% for the UK All Companies sector and 4.8% for UK Smaller Companies.

Various FTSE 100 sectors performed well both in terms of capital growth and income generation, including financials and defence stocks. In turn, this played a big role in dividend-focused strategies outperforming.

However, while rising share prices are welcome for existing investors, they have the effect of pushing down yields. As a result, I’ve made changes to the 2026 line-up to raise the portfolio’s yield to a higher level than would otherwise have been achieved.

As ever, bear in mind that this portfolio is hypothetical and educational. The portfolio is designed to provide food for thought and demonstrate the challenges DIY investors face when building an income-producing portfolio. For more information, please see the section on ‘purpose of the portfolio’ in the final section of this feature.

How the 2025 portfolio performed

The 2025 portfolio (the article can be found here) required £235,000 for the £10,000 income challenge (a portfolio yield of 4.26%).

The hypothetical portfolio size grew to £275,389 at the end of 2025, which represented a percentage return of 17.2%. The income generated fell slightly short, at £9,593, but this shortfall was more than mitigated by a capital gain of just over £30,000 (with the overall total return being just over £40,000). Therefore, income investors could have dipped into their capital for extra cash if necessary.

As the 12-month yield figure is used to reflect the income that’s been generated by the fund, rising share prices had the effect of reducing fund yields, which led to slightly less income being produced than expected.

Below, I share how the portfolios have fared each year since I started constructing them in 2023. While there’s no benchmark to ‘mark my homework’, I’ve listed the return of the IA’s 40-85% Mixed Investment Sector, which in common with this hypothetical portfolio contains funds holding both shares and bonds.

| Year | Income generated | Total return (%) | Mixed Investments 40-85% Shares sector average (%) |

| 2025 | £9,593 (based on portfolio size of £235,000) | 17.2 | 11.6 |

| 2024 | £10,152 (based on portfolio size of £230,000) | 10.0 | 9.0 |

| 2023 | £10,139 (based on portfolio size of £225,000) | 6.9 | 8.1 |

Source: FE Analytics. Past performance is not a guide to future performance.

How the equity funds performed

Funds should be regarded as a medium- to long-term investment rather than being judged over shorter time frames – for good or bad. However, it’s advisable to review your investments annually and consider switches if circumstances have changed.

When investing in funds, the key things to watch out for include whether the same manager is running the fund, whether they are sticking to their knitting in terms of the investment objective and style, and whether performance has soured on the back of too many poor stock selection decisions.

None of those factors applied to the 10 funds I picked for last year’s income challenge.

In terms of the best performers, the UK trio all outperformed the average UK equity income fund. Vanguard FTSE UK Equity Income Index led the way, with a gain of 31.2%.

The value-focused and actively managed Man Income delivered handsome returns, up 27%, while larger company-focused Artemis Income also outperformed peers in gaining 21.7%.

Artemis Monthly Distribution, the portfolio’s largest holding, returned a very solid 23.1%. This fund typically holds 60% in shares and 40% in bonds.

Both global equity income funds from the portfolio also outperformed the sector average return of 12.8% in 2025.

Vanguard FTSE AllWld HiDivYld ETF $Dis VHYD 0.56%

returned 17.7%

while Fidelity Global Dividend was up 15.1%.

Guinness Asian Equity Income lagged its sector average return, up 12.6% versus 19%. But this is perhaps no surprise owing to the strong rising market over a short time period and given the fund’s income focus and equal-weighted approach. Over three years, it has matched the sector average return of 28.3%, but is ahead over five years, up 41.5% versus 25.6%.

Bonds carried out their defensive duties

Bond fund returns are expected to be less exciting as their role in a portfolio is to generate income and provide defensive ballast against any unwelcome sell-offs in equity markets.

In 2025, I dialled up the portfolio’s exposure to bonds from 30% to 40%. This was due to yields being at attractive levels at the time of around 4.5% on the lowest-risk areas of the bond market such as gilts and money market funds. Moreover, the move to beef up bonds was also down to the prospect of more interest rate cuts occurring in 2025, which would have the effect of boosting bond prices.

Those interest rate cuts did materialise and while yields on the lowest-risk areas of the bond market have been declining (as a result of bond prices rising), there are plenty of opportunities further up the risk scale for bond fund managers to take advantage of.

In 2025, Jupiter Strategic Bond gained 9.8%, followed by returns of

8.4% for Royal London Global Bond Opportunities and

4.4% for Royal London Short Term Money Market fund, which aims to deliver a cash-like return.

| Group/Investment | Starting Value (£) | Total Return (1 January 2025 to 31 December 2025) (%) | Value at end (£) | 12-month yield (as at 31 December 2025) | Estimated Income (£) |

| Global Equity Income | |||||

| Fidelity Global Dividend W Inc | £23,500.00 | 15.09 | 27,046.25 | 2.57 | £604.13 |

| Vanguard FTSE All World High Dividend Yield ETF $Dis | £17,625.00 | 17.69 | 20,743.66 | 2.81 | £494.61 |

| UK Equity Income | |||||

| Artemis Income I Inc | £23,500.00 | 21.68 | 28,594.13 | 3.36 | £788.93 |

| Man Income Professional Inc D | £17,625.00 | 27.00 | 22,384.26 | 4.56 | £804.12 |

| Vanguard FTSE UK Equity Income Index £ Inc | £17,625.00 | 31.18 | 23,121.35 | 4.20 | £740.98 |

| £ Strategic Bond | |||||

| Jupiter Strategic Bond I Inc | £23,500.00 | 9.80 | 25,802.85 | 5.34 | £1,254.72 |

| Mixed Investment 20-60% Shares | |||||

| Artemis Monthly Distribution I Inc | £47,000.00 | 23.07 | 57,841.61 | 3.78 | £1,777.12 |

| Short Term Money Market | |||||

| Royal London Short Term Money Mkt Y Inc | £23,500.00 | 4.43 | 24,540.45 | 4.36 | £1,024.76 |

| Asia Pacific Excluding Japan | |||||

| Guinness Asian Equity Income Y GBP Dist | £17,625.00 | 12.56 | 19,839.47 | 4.13 | £728.75 |

| Global Mixed Bond | |||||

| Royal London Global Bond Opportunities Z GBP | £23,500.00 | 8.41 | 25,475.25 | 5.85 | £1,375.05 |

| Total | £235,000.00 | £275,389 (rounded) | £9,593 (rounded) |

Source: Morningstar. Past performance is not a guide to future performance.