We asked our freelance writers to reveal the top US stocks they’d buy in November.

Posted by

The Motley Fool Staff

Image source: Getty Images

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Every month, we ask our freelance writers to share their top US stocks with investors — here’s what they rate highly for November!

CrowdStrike Holdings

What it does: CrowdStrike operates a cloud-based cybersecurity platform that leverages AI to continuously evolve and defend businesses.

By Zaven Boyrazian.

CrowdStrike Holdings (NASDAQ:CRWD)recently found itself in the media spotlight, and not for a good reason. A botched software update triggered a global outage of IT systems that impacted airlines, medical institutions, and even banks.

Unsurprisingly, this disaster resulted in a significant drop in the CrowdStrike share price. Yet even though the bug that triggered the outage has been fixed with new protocols in place to prevent a repeat, the stock still trades almost 20% lower.

To be fair, there is some justification behind investor concern. Delta Airlines is already in the process of filing a lawsuit, and more legal action could be coming down the pipe. However, when looking at the long-term potential, this may ultimately be a short-term hiccup.

After all, this wasn’t a failure of cybersecurity. In fact, the group’s Falcon platform continues to be one of the best in the world based on the results of the latest SC Awards Europe. Considering the group’s explosive growth and trajectory, this looks like a buying opportunity in my eyes, although volatility is expected.

Zaven Boyrazian does not own shares in any of the companies mentioned.

Netflix

What it does: Netflix is an entertainment streaming service that provides on-demand tv shows, movies and documentaries.

By Harshil Patel : Netflix (NASDAQ:NFLX)is a streaming giant that has over 280m paid subscribers in over 190 countries.

It recently experienced a jump in the number of subscribers in Q3 of 2024, adding 5.1m new users. This along with profit for the quarter beat market expectations.

Netflix has an excellent business model that benefits from a network effect. It has reached a scale that keeps subscribers locked in. More investment in new shows creates content, and more content keeps users hooked.

This was evidenced recently when it changed its pricing model to crack down on password sharing. Its ability to raise prices demonstrates pricing power too. This is a key attribute of a high-quality business.

With Amazon, Disney and Apple all offering streaming services, there is ample competition for Netflix to worry about. Also, raising prices is great for its profits, but there will be a limit to what users are prepared to pay. Getting the balance right will be key to maximising its profitability.

Harshil Patel does not own shares in Netflix.

Nu Holdings

What it does: Nu Holdings is the parent company of Nubank, the leading digital bank in Latin America.

By Ben McPoland. A stock I plan to buy in November is Nu Holdings (NYSE: NU).

While still largely unknown in the West, Nu is Latin America’s largest branchless bank, offering customers loans, insurance, bill payments, stock investing, and more.

Incredibly, it now has 105m users, despite only operating in three countries (Brazil, Colombia, and Mexico). Over half the adult population of Brazil use the app, and it has added more customers in the past 12 months than the five largest Brazilian incumbents combined.

Of course, as the firm expands its credit portfolio, it opens itself up to an increase in non-preforming loans. This is worth monitoring.

Despite this risk, Nu Holdings looks like a high-quality growth stock. Revenue has soared from $1.7bn in 2021 to a forecast $10.3bn this year. Profits are expected to grow above 50% over the next five years. Its return on equity (ROE) is 28%, one of the highest in the industry.

It’s led by founder-CEO David Vélez, a former partner at venture capital firm Sequoia. With tens of millions still underbanked across Latin America, the growth opportunity appears massive.

Finally, the stock isn’t grossly overvalued. At $14, it’s trading at 23 times forward earnings.

Ben McPoland does not have a position in any stocks mentioned

Bluefield Solar (LON: BSIF), the London listed UK income fund focused primarily on acquiring and managing solar energy assets, announces its net asset value (‘NAV’) as at 30 September 2024. Unless otherwise noted herein, the information provided in this announcement is unaudited.

Unaudited Net Asset Value as of 30 September 2024

(pps)

Audited NAV as at 30 June 2024

129.75

Power prices

0.00

Operational updates

0.28

FY24 third interim dividend announced and paid

-2.20

FY24 fourth interim dividend announced

-2.20

Share buyback accretion

0.18

Other movements

0.33

Unaudited NAV as at 30 September 2024

126.14

The unaudited NAV as at 30 September 2024 was £753 million, or 126.14 pence per Ordinary Share (‘pps’), compared to the audited NAV of 129.75 pps as at 30 June 2024. This equates to a movement in the quarter of -2.8% and a NAV total return for the quarter of +0.6% when adjusting for the two interim dividends declared in the period. Dividends are accrued in the period in which they are declared and this Q3 is unusual in that two dividends were declared in the period, which have the effect of detracting a total of -4.40 pps from Bluefield Solar’s NAV. The Company intends to declare its next interim dividend in January 2025.

The latest valuation reflects the completion of Phase Two of the Strategic Partnership with GLIL Infrastructure, being the sale of a 50% stake in 112MW of operational solar assets. A substantial part of the sale proceeds were used to repay £50.5 million of the Company’s Revolving Credit Facility.

The Company has also continued to recycle capital and realise value from its project development activities by disposing of one co-located solar and battery storage project in the period. The Fund received proceeds c.20% above holding value, now reflected in the working capital and captured in ‘Other movements’.

Power price forecasts have remained similar to those used for the June 2024 NAV. Short term forward electricity prices have risen, driven by higher commodity prices, while longer term prices are largely unchanged. The Company remains well hedged against shorter term volatility due to its high proportion of fixed revenues.

The increase in valuation from operational updates (+0.28 pps) reflects the latest tax forecasts available to the Company and updated debt balances as at the end of the period.

‘Other movements’ reflect the change of the calculation date of cash flows from 30 June 2024 to 30 September 2024, along with tax, degradation, debt, and working capital adjustments.

The Company repurchased 5.9 million shares during the quarter to 30 September 2024, providing +0.18 pps of NAV accretion to shareholders.

Gearing

The Company’s UK holding companies and subsidiaries have total outstanding debt of £583 million as at 30 September 2024, with a leverage level of circa 43% of Gross Asset Value.

Dividend Guidance Reaffirmed

The Board is pleased to reaffirm its guidance of a full year dividend of not less than 8.90 pence per Ordinary Share for the financial year ended 30 June 2025 (2024: 8.80 pence). This is expected to be covered by earnings and to be post-debt amortisation.

Investing £100k in this share could add £1.2m to my SIPP valuation!

Christopher Ruane identifies a FTSE 100 share that he thinks could potentially transform the long-term performance of a SIPP.

Image source: Getty Images

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Imagine putting £100k into one share in a SIPP and then sitting back to see the holding grow in value to £1.3m.

I know, £100k is a lot to invest – especially as I believe in keeping a SIPP diversified, so I would not invest £100k in one share unless I had a much larger pool of money in my SIPP to invest.

Still, turning £100k into £1.3m sounds excellent to me!

In this example, I am not even presuming any share price increase. A growing share price could speed things up, though the reverse is also true.

Taking the long-term approach

When I talk about speeding things up, I ought to mention that my approach here is a long-term one.

I think that makes sense. In this example, I am considering a timeframe of 25 years.

In the context of a SIPP, I see that as a practical timeframe. Many investors plan to hold their SIPP for multiple decades.

The power of compounding

So, how could I hope to turn my £100k into £1.3m even across 25 years, if the price of the share I buy does not move even an inch?

Simple: compounding the dividends.

Compounding at 10.8% annually, my £100k investment would end up worth £1.3m after a quarter of a century.

FTSE 100 share with a 10.8% yield

That brings me, though, to the question of whether a blue-chip FTSE 100 share would offer anything close to a 10.8% yield. After all, that is triple the average FTSE 100 yield at the moment.

One almost does: Vodafone. But its 10.6% yield is set to collapse as the company has announced plans to halve the dividend. That is a useful reminder that no dividend is ever guaranteed to last – and a high yield can be a sign that the City has doubts about whether it will.

Another FTSE 100 share has a 10.8% yield and has not announced plans to reduce its dividend. Quite the contrary, in fact: this year it affirmed its plan of continuing to raise the payout per share annually.

That company is Phoenix (LSE: PHNX), a financial services firm that bills itself as the country’s largest long-term savings and retirement business.

It has around 12m customers and operates using brands including Standard Life and Sun Life.

Looking to the future

One of the challenges when analysing financial services companies is that earnings are not always helpful. For example, fluctuating asset valuations can lead to higher or lower earnings numbers that do not necessarily help assess the underlying financial health of a business.

On the plus side, Phoenix is in a large, well-established business area and has a very sizeable customer base and deep experience in a specialist field. Those attributes could help the business, which turned over £4.9bn last year, to generate sufficient free cash flows to maintain its generous dividend.

That may not happen; one risk I see is a property market downturn hurting the valuation of Phoenix’s mortgage book, forcing it to write down the valuations.

But on balance, I think Phoenix is a share investors with an eye on long-term passive income streams should consider.

£££££££££££££££

Note: It’s doubtful u will be able to re-invest the dividends at 10.8% for 25 years.

Asia Dragon (DGN) and Invesco Asia (IAT) plan to merge, with DGN winding up and transferring assets to IAT. If approved, the combined fund, rebranded as Invesco Asia Dragon, will be the second-largest Asia Pacific equity trust. Gulf Investment Fund (GIF) will liquidate, with trading suspended after 99.6% shareholder approval. Meanwhile, Baillie Gifford Japan (BGFD) cuts fees.

By Frank Buhagiar

Asia Dragon and Invesco Asia to tie the knot

Asia Dragon (DGN) and Invesco Asia (IAT) become the latest investment companies to announce they are combining. This follows the completion of a strategic review by DGN which considered a wide range of options including entering into a combination with another investment trust. In the end, “The Board was impressed by the distinctive and disciplined value-oriented investment approach employed by Invesco Fund Managers Limited which has delivered attractive returns for Invesco Asia shareholders over the long term.”

If approved by both sets of shareholders, DGN will be wound up with its assets transferred to IAT in exchange for new shares in the enlarged Invesco fund – the transaction will include a partial cash exit opportunity for up to 25% of DGN’s issued share capital. There will be a name change too. Invesco Asia will become Invesco Asia Dragon.

Winterflood: “We note that it is relatively uncommon for a fund to merge into a vehicle that is a third of its size (hence, full cash exit take up may result in limited scale benefits) but the enlarged IAT will nevertheless be well beyond what most would consider ‘sub-scale’. Given the shareholder overlap and commitments received, we see no reason for this merger to fail to obtain approval.”

Numis: “The board of IAT is seeking to make IAT the ‘go-to’ Asian trust, with a premium rating to grow organically and through further combinations. The combined assets of c.£815m will make it the second largest IC in the Asia Pacific – Equity sector, behind Schroder AsiaPacific (£909m net assets). To achieve its aims, we believe Invesco Asia will need to raise its profile.”

Gulf Investment Fund to wind up

Gulf Investment Fund (GIF) shareholders voted to wind up and liquidate the company at the Extraordinary General Meeting held on 29 October 2024 – 99.6% of shareholders voted in favour. No hanging about. As per the press release, the shares were suspended from trading at 7:30 a.m. on 29 October 2024 and just a day later the admission to trading of the ordinary shares on the Specialist Fund Segment was cancelled. PricewaterhouseCoopers LLC has also been appointed as the liquidator of the company to action the wind-up.

Baillie Gifford Japan lowers fees

Baillie Gifford Japan (BGFD) is the latest fund to announce changes to its fee structure. As per the latest full-year results, as from 1 September 2024, the first tier of the investment management fee structure, the 0.75% fee rate on the first £50m of net assets, is to be removed. As a result, the fee payable to the managers is now 0.65% on the first £250m of net assets and 0.55% on the remaining net assets. This translates into an annual saving of £50,000 for the company. Every little bit helps.

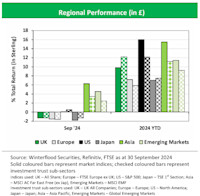

A three-quarter year review of London’s Investment Company Sector

As Q3 2024 wraps up, we analyse London’s investment company sector to identify this year’s winners and losers. The FTSE Closed End Investment Index (FTSE CEI) rose +0.5% for the quarter, maintaining positive returns but trailing the FTSE All-Share’s +9.9% year-to-date. Top-performing sectors include Growth Capital and Leasing, while Renewable Energy Infrastructure and Regional REITs struggled.

By Frank Buhagiar

With the numbers in for Q3 2024, it’s time to check in on London’s investment company space. Which investment companies are having a year to remember and which are having a year to forget?

Three for three

Another positive quarter for the FTSE Closed End Investment Index (FTSE CEI). The sector closed up +0.5% for the three months ended 30 September 2024. That’s a little off the +2.3% sterling total return delivered by the FTSE All-Share over the same period, but at least the record of posting positive returns for each quarter of the year has been maintained: Q1 / Q2 2024, the FTSE CEI was up +2.3% / +3.4% respectively. With just Q4 to go, the clean sweep is on.

Year-to-date, the FTSE CEI is now showing a +6.3% positive return. Once again, a little behind the FTSE All Share’s total return of +9.9% for the first nine months of the year. Barring a barn-stopping Q4, looks like a fourth successive year of the FTSE CEI falling short of the All-Share. As the table below from FTSE Russell shows, 2020, the last year London’s closed-end space outperformed the wider market:

The shoe is on the other foot

Worth pointing out though that London’s investment companies haven’t always struggled to keep pace with the wider market. Indeed, the opposite could be argued – the wider market has struggled to match London’s closed-end sector. For, as the table above shows, over the ten-year period 2014-2023, the FTSE CEI outperformed the wider market in six of the ten years. And it turns out between 2017-2020, the closed-end fund index had its own four-year winning streak. The FTSE All-Share then merely catching up with London’s investment companies.

And according to the above table, the FTSE CEI chalked up a handsome +113% gainbetween 2014-2023. The FTSE All-Share by contrast could only manage a cumulative gain of +68% over the same ten-year period. The FTSE 100 too is only up +68%. Over the ten years to 2023, London’s investment companies have trounced the wider market.

In terms of the average share price discount to net assets, this stood at 13.7% as at end of September, no change on the end of August level. This compares to the average 12.8% discount as at the end of 2023 and 10.8% as at the end of 2022.

The standouts – regional and sector levels

Given the UK market’s well-documented troubles – companies leaving London for the US and elsewhere; pension funds internationalising their portfolios at the expense of UK allocations; and persistently low valuations – perhaps surprising to see the UK All Companies subsector joint top year-to-date in terms of best-performing investment trust region. Alongside North America, UK All Companies up +12.2% over the first nine months of the year. As the below graphic from Winterflood shows, all regions are in positive territory year-to-date with the worst-performing investment trust region Europe still managing a +5.8% gain:

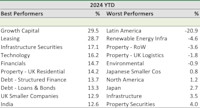

At the wider sector level, Growth Capital tops the list with a +29.5% share price total return to show for the first nine months of the year – the eight-fund sector includes the likes. At the half-year stage, the sector was up +21.53% and was second in the table behind then leader Technology and Technology Innovation which boasted a gain of +28.03%. Three of Chrysalis (CHRY) which recently commenced a share buyback programme as part of its capital allocation programme; Petershill Partners (PHLL) which returned US$222m during the first half of 2024 via a mixture of dividends, a tender offer and buybacks; and the Baillie Gifford-run Schiehallion (MNTN)months on and the Technology sector has slipped to fourth after its year-to-date gain shrank to +16.2%. An underwhelming reporting season for the Magnificent Seven mega-techs weighing on sentiment there.

Not far behind Growth Capital is Leasing with a share price total return of +28.7%. Both aircraft and shipping leasing companies have been performing strongly this year. The two Doric Nimrod Air Funds reacted well to news t DNA2 is selling its five remaining aircraft to United Arab Emirates for an aggregate combined total of US$200m or £153.53m. The valuation had positive read across for sister fund DNA3 –share prices of both funds reacted well to the news.

The table below from Winterflood lists the ten best and worst performing sectors year-to-date:

Below Growth Capital and Leasing, interest-rate sensitive subsectors, such as Property, Debt and UK Smaller Companies, well represented in the best performers column. As for the worst performers, sectors comprised of just one or two funds feature highly, including Latin America (BlackRock Latin American) and Property RoW (Ceiba Investments and Macau Property Opportunities). Renewable Energy Infrastructure completes the bottom three – a mix of higher-for-longer interest rates, weaker power prices and bad weather all at work here.

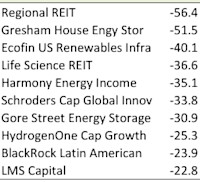

The standouts – investment company level

First, the laggards. Regional REIT the worst performer to date – a deeply discounted rights issue to blame. Elsewhere, five Renewable Energy Infrastructure funds in the bottom ten. As highlighted above, a range of top-down reasons for this, but also company-specific ones too. For example, a failure to find a buyer for its portfolio did for Ecofin US Renewables Infrastructure, while the suspension of its dividend didn’t help sentiment at Gresham House Energy Storage.

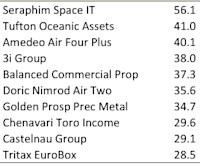

As for the winners, no surprise to learn that investment companies belonging to this year’s top-performing sectors feature highly in the best performers list. In first place, Seraphim Space from Growth Capital keeps hold of top spot, a position it held at the half-year stage. That’s despite seeing its gain on the year fall slightly to +56.1% from +58.72% as at 30 June.

As the table below shows, a small gap between Seraphim and the rest of the pack. The next two top performers both herald from the Leasing sector – Tufton Oceanic Assets and Amedeo Air Four Plus up +41% and +40.1% respectively. DNA2 also makes it into the top ten courtesy of a +35.6% rise.

Elsewhere, strong gold prices lie behind Golden Prospects Precious Metals’ seventh place. Meanwhile 2023’s top performer 3i Group still in the hunt to retain its crown – shares are up +38% over the nine months to end September. A little ground to make up true, but certainly doable. At the half-way stage, 3i shares were up +28% which was only good enough to squeak into the table in tenth place. Three months later and 3i is up to fourth spot. What’s more, the gap between the private equity giant and Seraphim has narrowed from +30.7% to +18.1%. The race to be London’s best-performing investment company in 2024 is well and truly on.

Should investment trust buyers be looking at active ETFs as well?

There have been no new investment trust IPOs in two years, but many active ETFs are emerging. This week, Janus Henderson launched a new Japanese equities active ETF, which could have been an investment trust. Active ETFs are booming in the US and launching regularly in Europe. We explore the key differences and similarities.

By David Stevenson

The whole investment trust sector has to fight for new money inflows, but barely a week goes by without news of some new active exchange-traded fund launch. Just this week, for instance, came news that Janus Henderson – a major player in the investment trust space – announced the launch of its first active ETF in Europe: the Janus Henderson Tabula Japan High Conviction Equity UCITS ETF (JCPN). According to the manager “the fund will adopt a high conviction approach and invest in an actively managed all-cap concentrated portfolio of 20 to 30 holdings, providing exposure to companies that are set to benefit from structural themes and trends in the Japanese Equity market, and showcasing the best of Janus Henderson’s stock selection skills. The launch of this active ETF represents an important milestone for Janus Henderson, allowing the firm to cater to client demand globally for its investment strategies to include a UCITS ETF wrapper; and builds upon the firm’s extremely successful active ETF proposition in the US where it is fourth largest provider of actively managed fixed income ETFs.”

That last sentence should be of particular concern to investment trust fans – active ETFs have been growing exponentially in the US, with many big fund managers getting behind the space with huge marketing pushes. Remember that the US also has a vibrant closed-end fund space that echoes the UK investment trust sector. What should be especially concerning is that the Janus Henderson Japanese fund could have been an investment trust, but the manager has chosen to use an active ETT format.

This news prompts an important question: Are active ETFs and investment trusts very different structures, or are there many similarities? Put another way, are active ETFs and investment trusts fighting for the same investor attention?

Many fund managers publish useful guides to ETFs to help explain the similarities and differences. I’d highlight this one from AXA and this one from JPMorgan as helpful. In this article, I want to simplify the explanation so that investors can make up their own minds.

The first point is that an active ETF differs from a traditional passive ETF in one very important way. In the latter, a fund manager identifies an index, such as the FTSE 100 or the S&P 500 and then replicates or tracks that index passively. If Nvidia suddenly doubles as a holding in the S&P 500 because of rocketing valuations, then the passive fund will track that change.

An active ETF might still have an index or benchmark, but its explicit focus is on actively beating the index through its portfolio of active stock or bond picks. In a sense, this is exactly what an actively managed investment trust also seeks to do – if we look at Alliance Witan Trust, it too chooses to reference an index, a global equities index, and then aims to beat that index. So, there is an obvious similarity in investment strategy between an active ETF and an investment trust. Another similarity is that both investment trusts and ETFs are listed funds, i.e. they have a ticker with a real-time quote for buying and selling shares all day, every day (when the markets are open). That makes them very different from unit trusts, which only issue an end-of-the-day price for underlying holdings which then triggers any buy or sell orders.

However, the similarities between an ETF and an investment trust stop there. Both a passive ETF and an active ETF are open-end fund vehicles (like unit trusts), which means the manager can issue shares regularly – in fact, daily or even in real-time if they so choose. By contrast, Investment trusts are closed-end vehicles, which means they start with a fixed issuance of shares. That doesn’t mean that the fund can’t issue new shares via a placing programme for instance, or buy back shares regularly, as many investment trusts are doing – but they don’t have quite the same flexibility to change the amount of shares in issue.

The next big difference is the passive and active creation and redemption process in ETFs. This mechanism allows the ETF to trade at close to, or exactly at, the shares’ net asset value. In this complex process, the fund manager issues shares based on the portfolio holdings, which are fully transparent in real-time (in the US there are semi-transparent ETFs but let us ignore that for now). This list of holdings is available to a market-making authorised participant firm, usually a financial intermediary, which can then look at the index and compare it to the fund holdings. If the fund’s assets are worth, say, £100m, but the value of the fund is only £95m, for argument’s sake, the AP can buy the shares and then exchange these shares for a basket of securities ‘in kind’ , or vice versa.

The AP can create and redeem shares based on an agreement with the fund issuer. If there is a shortage of ETF shares in the market, the AP can create more ETF shares, and again, this works in reverse as well – they can redeem shares. It all sounds complicated, but the key impact is that there should be a close match between the fund’s net asset value and the ETF share price. This doesn’t mean that an ETF can never trade at a discount to its NAV (or premium), which does happen in some instances with some exotic investments, but for the vast majority of the time, there should be no discount or premium for an ETF. Crucially, this mechanism works for active ETFs as well – instead of an index, we have a model portfolio or basket of shares equivalent to the fund holdings.

Investment trusts operate in a very different way. Discounts are common in the closed-end fund space, and although managers and boards can use all sorts of mechanisms to close the gap (buybacks and tenders, for instance), many of these don’t move the discount appreciably.

Another key difference between trusts and active ETFs worth noting is cost and structure. It’s very easy to create an ETF because there is no board of non-executive directors or NEDs, and the fund structure is simplified and streamlined based on a common set of European-wide rules set mainly by Ireland and its central bank under the regional UCITs framework. No sponsoring broker officially launches or IPOs the fund as an adviser, which also helps cut costs. Crucially, suppose you are an active fund manager. In that case, you can probably issue an ETF with just a few million pounds in assets under management and then slowly build it up in scale – most analysts reckon break even for an ETF is probably somewhere between £10m and £50m. And that’s true even though most ETFs charge less than 0.50% per annum in total expenses which is much lower than the equivalent investment trust. The Janus Henderson Japan equities fund, for instance, charges 0.49%. In contrast, most Japanese investment trusts charge between 0.50% and 1% – according to Numis, the average large-cap Japanese equities fund charges 0.81%, while the average small-cap Japanese equities fund charges 1.1%.

Now, its important to step back at this point and say that the extra structures in place with an investment trust may cost more – you need to pay those directors and broker advisers – but they also provide real protection for investors. If the fund manager underperforms, the board can fire them and find a new manager. That isn’t the case with an active ETF. A closed-end fund structure also provides permanence – this is a long-term commitment of capital unless the fund decides to wind up. With active ETFs, you can start with a few million pounds in assets under management and then remain under the radar for years, not attracting much capital or research interest. Many active ETFs close in the US because they fail to attract much interest and the manager can just decide to close down whenever it suits them – although you will receive your net asset value per share back when the fund closes.

I’d also argue that the obvious advantage of active ETFs over investment trusts – the discount or lack of with an ETF – can be seen in two ways. Sure, we should expect most active ETFs to trade at their NAV but there is an advantage to buying an investment trust at a discount – you’re buying a collection of hopefully valuable assets at a discount to their ‘real’ (we hope) value i.e. a catalyst emerges that closes the discount. That value opportunity is not good news to the seller of the deeply discounted investment trust, but discounts are an essential feature of the investment trust proposition.

As for active ETFs, they can serve a slightly different need. They’re great for fund managers looking to sell a fund across Europe quickly and easily. The fund managers can also easily set up different classes of shares for different currencies and even introduce hedged classes of shares – the same goes for accumulating and distributing classes of shares. For investors, active ETFs can work very well for niche ideas or strategies that might never attract huge sums of capital, i.e. as investment trusts get bigger and more liquid, not all investment ideas will attract hundreds of millions in capital, whereas an active ETF might work well.

One last point: The nature of the assets. Many active ETFs focus on underlying assets such as equities or bonds that are easily traded, i.e. there is real liquidity in the underlying assets. That underlying liquidity allows the authorised participants to ensure the share price equates to the NAV. Investing in illiquid assets such as private assets (real estate, renewables, or infrastructure) becomes much more challenging. It’s one thing to trade in Japanese equities in real-time (by the way, not always as easy as you think), quite another to sell a wind farm or a stake in a private business. Active ETFs are unlikely, for now, to be very common in these private asset markets, although some managers are pioneering ways of accessing private markets with an index-like structure of more liquid assets. Alternative assets will almost certainly remain a key selling point for the closed-end investment trust sector, giving investors access to less than liquid asset classes usually reserved only for large institutional investors.

The Results Round-Up: The week’s investment trust results

JPMorgan Global Emerging Market Inc (JEMI) matches the index; Intl Biotechnology (IBT) posts a 15.9% return; BlackRock Greater Europe (BRGE) +16.4%; Henderson Far East Income (HFEL) can’t match that but manages 11.9%; Fidelity Special Values (FSV), the standout up +24.1%; while Scottish Mortgage’s (SMT) half-year numbers can’t add to its long-term record of outperformance.

By Frank Buhagiar

JPMorgan Global Emerging Markets Income’s (JEMI) second half turnaround

JEMI’s net asset value (NAV) total return of +6.3% for the full year almost exactly in line with the MSCI Emerging Markets Index’s +6.4%. That means the second half of the year saw quite a turnaround in performance as the fund was nursing a 5% loss at the half-year stage. Over the five years to end of July 2024, the fund however has the upper hand and by some margin: the +25.3% NAV total return almost double the benchmark’s +12.7%. Meanwhile, the cumulative return on net assets over 10 years was +87.5% compared to +70.3% for the benchmark.

The strong track record serves as a thumbs up for the fund’s stock selection process. As the investment managers explain “Our principal focus is the same as it has been since the inception of the Company: we seek out companies able to produce attractive returns on equity, generate healthy free cash flow and pay shareholders reliable dividends. By identifying stocks with these characteristics, and buying them at attractive valuation levels, we can construct a portfolio with both value and quality attributes.” Well, if it aint broke. Market seems to agree – shares tacked on 2.5p to close at 136p.

Winterflood: “Bottom-up stock-picking methodology resulted in overweight positions in South Korea, Indonesia and Mexico, as well as underweight allocation to India. JEMI is overweight Information Technology, Consumer Staples and Financials, while underweight Materials, Industrials and Healthcare.”

International Biotechnology (IBT) sees green shoots

IBT had a strong year: NAV rose +15.9% compared to the NASDAQ Biotechnology Reference Index’s +15.3%. Good start then for new managers Schroders and a welcome return to form for the sector as a whole after a tough few years. As Chair, Kate Cornish-Bowden, notes “It is rewarding to report on the green shoots of a recovery in the biotechnology sector following an unprecedented period of share price declines in the sector.”

Cornish-Bowden lists several reasons for having a positive outlook including strong fundamentals, ageing populations and innovation in disease areas such as oncology, obesity and neurological conditions. Throw in increasing M&A activity “as large, cash-rich pharmaceutical companies seek solutions to impending drug patent expiries”, compelling valuations “and the potential rewards for investors in innovative companies developing future treatments look more attractive than ever.” Market took a little while to appreciate the results – shares only added 1p on the day to close at 685p. But by 7 November the shares were exchanging hands at 710p each.

Numis “The track record remains strong, with the fund outperforming the index over one, five and ten years, due to its flexible, valuation-driven strategy, adapting to evolving market conditions via selective risk-taking, with a focus on limiting volatility via its approach to binary event risk and a basket approach to key themes. We believe that this approach means that the fund is well-placed to continue this outperformance over the long term.”

BlackRock Greater Europe (BRGE) thinks optimists will be rewarded

BRGE outperformed over the full year – NAV per share returned +16.4% compared to the FTSE World Europe ex UK Index’s +15.8% (sterling terms and dividends reinvested). The investment managers see structural and cyclical tailwinds at work in Europe. Structural, “the European market is home to an ecosystem of companies which possess the enabling technologies required not just AI adoption, but also the energy transition and global efforts to reorganise supply chains.” Cyclical, “we detect a cyclical upturn in a variety of industries like construction, life-sciences and chemicals which have suffered from pronounced volume declines for the best part of two years.” Put the two together and “We see 2025 as a recovery year for earnings and beyond that we envisage a multi-year period of healthy profit growth, alongside the potential for this historic valuation gap to the US to narrow. Those prepared to take the optimistic view should be rewarded over time.” Just not yet – shares shed 4p to 551p on the day of the results.

Winterflood: “Board used discretion to not implement semi-annual tender offer in November, due to market conditions. Key contributors included Novo Nordisk, ASML, RELX and Ferrari.”

Henderson Far East Income’s (HFEL) repositioning pays off

HFEL posted an +11.9% NAV total return for the year. While a tad lower than the FTSE All-World Asia Pacific ex Japan Index’s +13.0% and the MSCI AC Asia Pacific ex Japan High Dividend Yield Index’s +17.4%, the share price total return of +16.6% fared better. According to the fund manager “In many respects the period under review shared several similarities with the year preceding it; India and Taiwan were the strongest markets and technology was a standout sector performer whilst China remained weak and sentiment arguably worsened over the period.” Excellent timing as “Our repositioning of the portfolio at the beginning of the period was positive for performance given that we had predominantly increased exposure to two of the strongest performing markets – India and Taiwan.” Market liked what it heard – shares added 2.5p to end the day at 228.5p.

Winterflood: “Asian dividend growth ahead of the managers’ expectations, aided by South Korea corporate governance reforms and some promising developments in China (several stocks +50% DPS growth). Underperformance vs. Dividend Yield index due to the latter’s concentration and the portfolio underweight to Chinese state-owned enterprises, particularly banks.”

Fidelity Special Values (FSV) looking for the volume to go up

FSV’s NAV total return came in at +24.1% for the year, easily beating the FTSE All-Share Index’s +17.0%. Chairman, Dean Buckley, puts the strong returns down to “a quiet renaissance in the still-unloved UK equity market” as well as the fund’s focus on identifying “quality companies with valuations lower than peers within the UK market.”

It’s an approach that has worked well over the long term too: £1,000 invested in the fund 12 years ago when Alex Wright became lead Portfolio Manager would now be worth £3,055 with dividends reinvested. And there could be more to come thanks to “an improving corporate earnings environment, the prospect of some political stability and a gradual economic recovery” all of which “may help to bring greater attention to the many good companies listed on the London Stock Exchange, which would undoubtedly give further impetus to the market” and, potentially, “be the catalyst to turn a quiet renaissance into something with greater volume.” Market got the message loud and clear – shares added 2p to close at 311.5p.

Numis: “We rate the managers highly and admire the investment approach which has a strong contrarian flavour, looking for unloved stocks where the downside is limited and there is a catalyst for change. We believe that the c.10% discount is an attractive entry point.”

Investec: “since IPO in 1994, the NAV total return is a non-too-shabby 2,817% or 11.8% annualised, 5.2% greater than the FTSE All Share total return CAGR. We regard Fidelity Special Values as a core strategic holding for UK exposure, and the fundamental attractions are enhanced by the current discount.”

Scottish Mortgage (SMT): Man versus machine

SMT reported a +1.9% NAV per share total return for the six months to 30 September. That’s a little short of the FTSE All-World Index’s +3.6%. Different story over longer time frames though. Over five years, NAV is up +88.9%, easily beating the index’s +66.9%, while over 10 years NAV boasts a +347.8% gain compared to the index’s +211.3%.

The growth investor’s interim management statement opens with an admission “Writing the interim report this year was notably different. I didn’t start by sitting down with a blank page. Instead, AI systems competed to provide me with summaries of the most significant events over the past six months. They tried to explain stock price movements and even suggested topics that might resonate with readers.” The statement then goes on to provide a rather matter-of fact run-through of the fund’s various positions in AI, tech, space, China and private companies. None of the usual anecdotes, observations and dare I say colour of previous statements from the company – have a read of the Half-year Report 12 months ago to compare. Same author at the bottom true, but different style. Perhaps the machine did write the whole report after all. Shares were off 7p at 903p at the time of (non-AI) writing.

Jefferies: “The results highlight a meaningful reduction in the proportion of the overall portfolio held in private companies.”

Numis: “The shares are currently trading at c.10% discount, and ultimately a period of strong performance is likely needed to narrow the discount. Scottish Mortgage has a market cap of c.£11bn and therefore flexibility to return capital whilst remaining a large, liquid Investment Company.”

It’s very much the case all around Britain. Our population is up to over 68m these days and of those, only 22m are funneling extra cash into the ISA tax vehicles. But even of the ISA holders, only 4m of these accounts are Stocks and Shares ISA where the most powerful of passive income investments lie. Folks seem to have pretty big reasons not to invest in this way.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

Rough beginnings

One of the issues of building an income through stocks is how meagre the initial returns are. A figure like 10% isn’t wowing anyone, for example. Sure, if you do the maths, then the money invested begins to snowball given enough time, but the first year or two seems fairly pointless. Anyone who can sock away £200 might not be too thrilled seeing £1.67 average return in their first few months. Is that really worth sacrificing a day at the races or a new toy from Amazon?

But the way this kind of growth works often flummoxes the human brain, even those who have experience with it. I still remember a science teacher asking the class how tall an A4 paper folded over 100 times would be. Most of us guessed in millimetres or centimetres. One crazy classmate guessed over a metre. The answer was it would reach to the moon!

Stratospheric growth from modest beginnings in investing can work too. Drip-feeding a monthly £200 at 10% might not make much after a year, but after 40 years it balloons into over £1m. While this little example is over a longer time span than many would have to work with, it shows how this growth does some bizarre-sounding things.

Jon Smith goes over the theory and the practical elements of what he’d need to do in order to solely live off dividend income from stocks.

Motley Fool

The content of this article was relevant at the time of publishing. Circumstances change continuously and caution should therefore be exercised when relying upon any content contained within this article.

Image source: Getty Images

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

In a world of high interest rates and generous dividend yields, the possibility of generating sizeable passive income from my cash holdings is real. By being smart with the choices of where to invest and what time frames are involved, I feel there’s a potential for me (and other investors) to live solely off dividend income.

Understanding how it works

Before getting to exact figures, let’s run through how it’s possible to live off dividend income. The core idea revolves around the strategy of having a portfolio of stocks that cumulatively pay out enough cash to support my household bills and other expenses.

This portfolio isn’t something that can be achieved in a matter of weeks, unless I have a very large amount of free cash sitting in a bank account. Rather, this is something that needs to be built up over time.

Do you like the idea of dividend income ?

The prospect of investing in a company just once, then sitting back and watching as it potentially pays a dividend out over and over?

If you’re excited by the thought of regular passive income payments, as well as the potential for significant growth on your initial investment.

Aside from the process of building the portfolio, to live off the income I need to sort other logistics. For example, I want to own enough stocks to receive some form of payment each month. Given that an average dividend stock might pay out a couple of times a year, this requires careful planning.

Another key point is that in the early days, it helps if I reinvest the dividends received. This will help to compound my gains and grow my pot at a faster pace. So I need to ensure that when I reach a point of taking money out of the portfolio, I’m aware that future growth will be slower.

A big pot needed, but not impossible

The figure that everyone needs to live off is different from person to person. I live in London, so mine will be higher than those living in rural areas. A fair estimate for me would be £35,000 a year.

I feel I can achieve an average dividend yield of 6.5% on a robust dividend portfolio. So my investment pot needs to be £538k to hit my financial target. On the face of it, this seems a very large figure.

Yet I never thought this was going to take a year or two. After all, living solely off dividend income is an incredible feat. But it doesn’t mean it’s impossible. For example, if I invested £500 a month, it would take me just under 30 years. That’s assuming my portfolio doesn’t encounter setbacks, which is always a risk, of course.

Granted, this might be too long for some investors, especially depending on their starting age. Things can be sped up if I already have a large investment pot, or a chunk of cash to put to work straight away. If I already had a £100k portfolio or cash deposit, it would only take me 19 years to reach my goal.

There are many different ways of looking at this strategy, but the reality is that there are people out there living solely off dividend income !