If you owned the SNOWBALL’s comparator share VWRP, the price is the same as last October, so you have added zero, zilch, nothing to your retirement fund.

The SNOWBALL has earned £3,678 in dividends, which have all been re-invested at a blended yield of 8% plus, earning extra income of £300 for the SNOWBALL.

With dividends of up to 12.6%, these could be the FTSE 250’s best passive income stocks

The FTSE 250’s stuffed full of high-yielding dividend shares, many of which are offering returns close to 10%. James Beard takes a look at three of them.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Although the FTSE 250‘s full of passive income opportunities, it’s sometimes overlooked by investors. In fact, the index is presently offering a yield higher than the FTSE 100, its more famous cousin.

Here are three members of the UK’s second tier index of listed companies that currently have an amazing combined average yield of 9.6%. I think all are worth considering for those on the lookout for dividend shares.

As safe as houses?

Despite suffering a torrid time following the pandemic, UK housebuilder Taylor Wimpey (LSE:TW.) is currently paying a dividend of 8.8%. And with the housing market appearing to be recovering slowly — driven primarily by an improvement in mortgage affordability — I think the worst could be over.

In 2025, completions were 636 (6%) higher than a year earlier. And the group was able to raise its average selling price by £16,000 (5%). Despite this, as a reminder of how post-Covid inflation has affected the cost of building materials, operating profit was broadly flat. Its margin fell from 12.2% to 11%.

But with interest rates expected to fall over the coming months, this could help reinforce the early-stage recovery. And despite its recent woes, the group has a healthy balance sheet. Further ahead, the government’s proposed planning reforms should benefit Taylor Wimpey.

Becoming more efficient

The SDCL Energy Efficiency Income Trust (LSE:SEIT) has a current yield of 12.6%. Although it’s been steadily increasing its dividend, the dramatic fall in its share price has been the biggest factor behind this incredible return.

Financial year

Dividend per share (pence)

Share price (pence)

Yield (%)

31.3.21

5.50

111

5.0

31.3.22

5.62

118

4.8

31.3.23

6.00

84

7.1

31.3.24

6.24

59

10.6

31.3.25

6.32

48

13.2

Source: London Stock Exchange Group/company reports

The trust now trades at a huge 42% discount to its net asset value (NAV). Part of this is explained by difficulties in valuing unquoted companies. But its relatively high debt has also been a concern. The trust has borrowed more than the 65% of its NAV that’s allowed under its rules. Asset disposals are underway to reduce this.

However, I think companies providing energy efficiency solutions are going to be among the long-term winners. We will get to net zero one day, but it might take longer than some, including shareholders in SDCL, would like. In my opinion, the trust’s been marked down more due to sector-wide concerns than anything specific to its own operations.

Going shopping

Primarily because of its 7.5% yield, Supermarket Income REIT (LSE:SUPR) is my favourite real estate investment trust (REIT). During its last financial year (30 June 2025), it reported 100% occupancy and no bad debts. This is testimony to the quality of the well-known grocery names that occupy its buildings in the UK and France.

Potential challenges include higher interest rates and a cyclical commercial property sector. Investors should also be aware that massive share price growth is unlikely.

But by whatever method we buy our groceries, whether it be online or in-store, there’s always going to be a need for physical shops. And with an average unexpired lease term of 12 years — and the majority of its leases containing provisions for inflation-linked rent increases — the REIT has plenty of visibility over future income levels.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

Some quick maths

Although I know there can never be any guarantees with dividends, a £10,000 investment spread equally across all three could yield £963 in year one. In my book, that’s worth considering.

From Bank Bloodbath to Pipeline Boom: An 8.1% Yield Escape Plan

Brett Owens, Chief Investment Strategist Updated: January 28, 2026

“And what can we do to get better shots?”

Your fulltime income strategist and part-time basketball coach asked his team of fifth and sixth graders for their ideas. Or, at least, tried to.

Then a ball bounced. After coach specifically said hold balls for a second time. This third infraction ended the conversation.

“That’s it—on the line. Start running.”

When coach says run, the players don’t really have a choice. Get moving in practice or lose playing time in the games they all love.

Likewise, when the government tells an industry that there is a cap on their profits, well, they’d better get moving too.

“Fat cat” financial lender stocks have tanked since the Oval Office asked for a 10% national cap on credit card interest rate. This went from a campaign slogan to a formal request to Congress. Ugly reaction from some stocks.

Capital One (COF), for one, shed 9.1% last week. The 10% cap created a hard ceiling on the company’s net interest margin (NIM), installing a much lower ceiling on its business model. What’s in your wallet?Less NIM for you!

The industry CEOs know it’s ugly. Everyone’s favorite financial villain, big boss at JPMorgan (JPM) Jamie Dimon, called the proposal an “economic disaster.” (Jamie always talks his book.) Bank of America (BAC) meanwhile is scrambling to design a “capped” card. Which will voluntarily put a lid on its profits.

Google searches for “credit card limit” are spiking amid the cap chatter. It’s ugly out there in the financial sector. But this has presented a “baby with the bathwater” buying opportunity. Indiscriminate selling gives us opportunity.

Visa (V), for example, is not a bank. It’s a financial plumbing tollbooth. Yet, it’s off 8% over the last month! Silly investors. They miss the distinction:

The Banks (like Capital One) risk their own capital to lend money. They need high interest rates to maintain their fat profit margins.

A Network (Visa) takes a small fee on every swipe.

Visa doesn’t care if the interest rate is 10% or 30%. To be blunt, they don’t care if the user pays the bill or defaults! They only care that the card is swiped. Visa processed $15 trillion last year—the caps won’t touch that. It’s a misunderstood growth model that features

The real pivot, though, is from “capped” banks to “uncapped” energy. The regulatory hammer is flexing on financials. But Washington is doing just the opposite with energy pipelines. In fact, the administration is peeling back red tape and rolling out the red carpet.

Pipelines are becoming the “boring” cash machines that banks used to be. They charge fixed fees to move natural gas and oil. And the sector is gushing so much free cash flow that they are raising payouts…and unlike the banks, the pipelines earn without having to fight Washington. Energy production is a priority for this administration, and these companies directly benefit with less regulation.

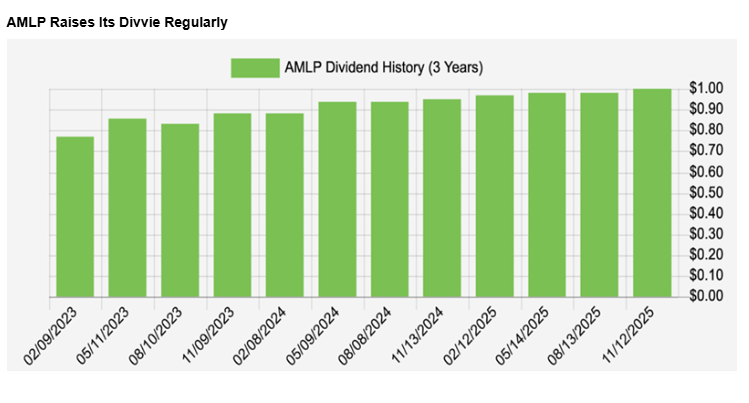

My preferred way to play this trend, which will run through at least 2028, is the Alerian MLP ETF (AMLP). AMLP owns a basket of midstream MLPs (master limited partnerships), the pipeline and infrastructure companies that mint fee-based cash flow. These businesses don’t need $100 or even $80 oil. They merely require traffic.

And traffic is what the US energy system does in 2026. We produce. We refine. We export. Oil is cheap but the pipes are still filling up. Whether prices are high or low, the tolls are getting paid.

And so are we, collecting an 8.1% yield from AMLP!

The fund provides us with a paperwork advantage, too. It is structured as a C-corporation fund, so shareholders receive a 1099. No K-1s, the tax headache many income investors endure when they buy individual MLPs.

AMLP also hikes its payout prodigiously:

AMLP Raises Its Divvie Regularly

What a contrast with banks like Capital One! They are fighting for their fat-cat lives against a 10% cap. Meanwhile, energy pipelines quietly toll the cash flow, free of regulatory scrutiny, paying us 8.1% to hold them.

This is how we live off $500,000…practically forever. By buying elite 8.1% dividends that are favored by the current administration.

Of course, there’s no need to dump a full $500K portfolio into AMLP alone. Diversify!

Q4 2025 Dividend Declaration and Increased FY 2026 Dividend Guidance

Q4 2025 Dividend Declaration

The Board of Octopus Renewables Infrastructure Trust plc is pleased to declare an interim dividend in respect of the period from 1 October 2025 to 31 December 2025 of 1.55 pence per Ordinary Share, payable on 27 February 2026 to shareholders on the register as at 13 February 2026 (the “Q4 2025 Dividend”). The ex-dividend date will be 12 February 2026.

The Q4 2025 Dividend is the final of four dividends totalling 6.17 pence per Ordinary share (FY 2024: 6.02 pence per Ordinary Share) for the financial year to 31 December 2025 (“FY 2025”), meeting the Company’s FY 2025 dividend target in full. The dividend was fully covered by cash flows arising from the Company’s operational assets.

A portion of the Company’s dividend is designated as an interest distribution for UK tax purposes. The interest streaming percentage for the Q4 2025 Dividend is 57.1%.

Increased Dividend Guidance for FY 2026

In line with the Company’s progressive dividend policy, the Board of Octopus Renewables Infrastructure Trust plc is pleased to announce a further increase in the target dividend to 6.23p* per Ordinary Share for the financial year from 1 January 2026 to 31 December 2026 (“FY 2026”), an increase of 1.0% over FY 2025’s dividend target. The FY 2026 dividend target is expected to be fully covered by cash flows arising from the Company’s operational assets.

Phil Austin, Chair of Octopus Renewables Infrastructure Trust plc, commented: “The Board is pleased to declare its final interim dividend for the financial year which, combined with the three prior quarters, meets our FY 2025 target of 6.17 pence per Ordinary Share and delivers a yield to shareholders of 11.2% as at Friday’s closing share price.

“We are also pleased to announce, for the fifth consecutive year in a row, an increase in dividend guidance in line with our progressive dividend policy. Importantly, this is expected to be fully covered by operating cash flows.”

To live off dividend income, consider the following strategies:

Calculate Your Needs: Determine how much income you need to live comfortably, which can vary based on lifestyle and location.

Invest in Dividend Stocks: Build a portfolio of dividend-paying stocks. The average UK stock market offers around a 4% dividend yield, so a portfolio worth between £750,000 and £1,250,000 could be necessary for a comfortable lifestyle.

Reinvest Dividends: Reinvesting dividends can help compound your income over time, allowing you to grow your portfolio faster.

Diversify Your Portfolio: Spread your investments across various sectors to mitigate risks associated with market fluctuations.

Consider Long-Term Investment: Focus on long-term growth and compounding, as it can take several years to build a substantial portfolio.

By following these strategies, you can work towards living off dividend income sustainably.

There aren’t many investors who will have a retirement pot of a million £/u$, so concentrate on re-investing your dividends to earn more dividends.

Is now a smart time to build wealth by buying UK passive income shares ? Judging by recent data, it seems targeting high-yield dividend shares from the London stock market can be a great way to boost one’s portfolio.

Yet now isn’t a ‘once-in-a-decade’ chance to capitalise on unusual market conditions. The truth is, UK dividend shares have been outperforming the wider market for years.

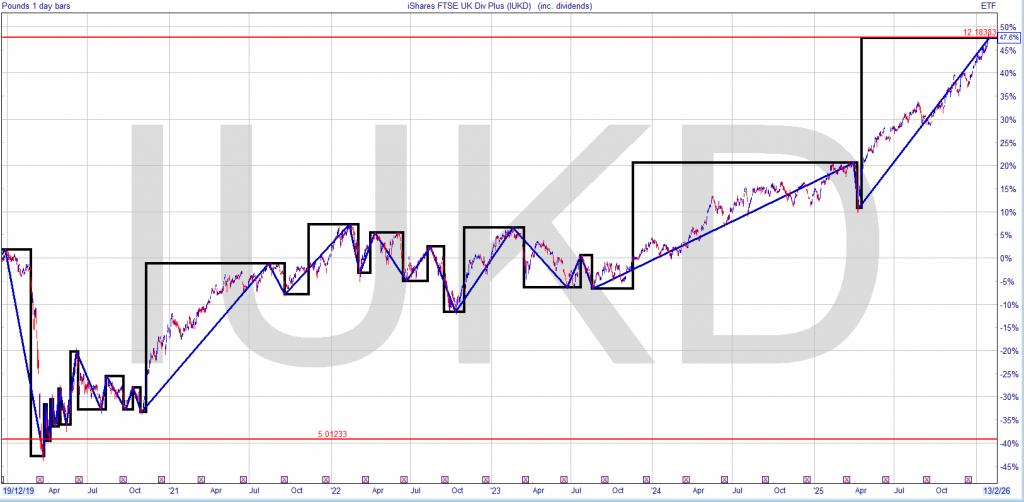

Over five years, the FTSE UK Dividend+ has delivered a 96.3% total return, meaning someone who invested at the start of 2021 would have almost doubled their money. By comparison, the broader FTSE 350’s provided a 74.8% total return.

Source: FTSE Russell

The question is: can investors continue to beat the market by targeting dividend stocks?

Sunny outlook

I think they could. The London stock market is packed with financially robust, market-leading companies with diverse revenue streams. So investors can realistically expect strong and sustained dividends in most economic scenarios.

Having said that, individuals may need to get a bit more selective if they’re looking to maximise their dividend opportunities. Surging share prices in 2025 have pulled the average yield on UK shares down to a forward-looking 3.3%. So how can investors best tackle this challenge

Next steps

The first step is to find a good stock screener to find higher-yield shares. They’re out there — it just takes a little bit of research to find them. My own analysis shows there are still around 100 passive income stocks today with yields of 6% and above.

The good news is modern investors have more tools at their disposal to find these dividend gems than ever before. They can use company reports, analyst notes, financial websites, and investing experts like the Fool to sort the wheat from the chaff. I myself have added more Aviva (LSE:AV.) shares to my portfolio after doing some careful researc

A FTSE 100 income share

For 2026, Aviva’s dividend yield is an enormous 6.1%. And for next year it rises to 6.5%. Dividends have risen consistently since 2020, and analysts expect the company’s strong balance sheet to underpin further growth. As of November, its Solvency II capital ratio was 177%, even after the purchase of rival Direct Line.

Can the FTSE 100 firm keep delivering, though? I think it can, though profits could come under pressure if core regions like the UK continue to struggle. I expect Aviva’s share price and dividends to rise strongly over time as the broader financial services sector rapidly expands.

The post UK passive income shares: a once-in-a-decade chance to get rich? appeared first on The Motley Fool UK.

How a stock market crash could boost passive income potential by 33%

Jon Smith points out why the ability for investors to enhance passive income from dividend shares can increase when the market falls.

Posted by Jon Smith

Published 1 February

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Chatter about a market wobble is growing louder amid a spike in geopolitical tensions. Of course, no one can predict what might cause a crash (if they could, it would take away the surprise). Therefore, the next best thing is to have a clear game plan for when (or if) a crash does happen. When it comes to passive income, here’s an approach investors can consider.

Enhanced yield potential

For all of the carnage that a stock market crash causes, there are actually some positives to take from it. One relates to the rise in dividend yields. If we break it down, the dividend yield is made up of the share price and the dividend per share. Logically, if the share price falls but the dividend stays the same, the yield will increase.

Let’s say a stock is trading at 100p with a 5p dividend. The yield is 5%. If a crash causes the stock to fall to 75p, but the dividend stays the same, the yield is now 6.66%. In terms of the change, it’s a 33% boost!

This means that shrewd income investors can pick up dividend stocks that fall during a crash and benefit from this added yield. Of course, if the dividend gets cut in the future due to the company being negatively impacted by whatever caused the crash, that’s a problem. But during a market rout, some stocks fall simply because investors panic. Some firms are unaffected by the cause of the fall but still experience a short-term drop. Those are the stocks to target.

Over the medium term, we could see share prices recover, with dividends remaining unchanged. Of course, there’s no guarantee this will happen, and it ‘ a risk that needs to be acknowledged.

You could buy the enhanced yield with earned dividends but you could boost your Snowball if have a list of coveted shares you would like to buy if the yield was better.

The SNOWBALL recommends a blended yield of 7%, because if you can add your dividends at a rate of 7% you income doubles every ten years.

If you want a safe fund, money market or a short dated gilt to maturity, you could use that to buy a share you coveted.

Everywhere in life, you pay for flexibility; In the financial markets, you get paid to seek flexibility.

Regular income from your portfolio creates cash flow flexibility and gives you options to navigate volatile markets.

We discuss our top picks that enable consumers and businesses to grow, innovate, and expand.

Looking for more investing ideas like this one? Get them exclusively at High Dividend Opportunities.

Co-authored with Hidden Opportunities

Flexibility always comes at a price. If you cancel your appointment with a doctor or dentist without providing 24–48 hours’ notice, you will be charged a fee. Life happens, but the policies are firm. Yet, when the doctor or dentist cancels on you with little notice, you are not compensated for your time.

The same dynamic exists in travel. In the post-pandemic era, airlines have monetized flexibility by turning it into a product. If you want to cancel or rebook your flight, you must pay extra for that privilege. If you want to choose your seat, or board early, that costs extra too. The aircraft or travel durations haven’t changed, but pricing has. As a traveler, you pay a premium for flexibility and convenience.

From subscriptions, services, and travel, and everywhere in life, you pay for the privilege of keeping your options open. The financial markets are one of the rare exceptions. Here, the market pays you for providing flexibility to others – through capital, timing, and liquidity.

Every time a consumer makes a purchase that they couldn’t upfront in cash, or delays a payment, and every time a business borrows to expand or manage working capital, they are using flexibility. The two investments discussed in this article let you collect generous dividends from companies that enable that flexibility.

Let’s dive in!

Pick #1: BIZD – Yield 11.5%

That local restaurant you love visiting is opening a new location at the other end of town. How do you think they secure the capital to pursue this business expansion? Unlike large public companies, they can’t issue more shares or debt, nor are they flashy enough for a VC (Venture Capital) to step in. Yet, they provide a service that hundreds, if not thousands, relish.

Born from the Small Business Investment Incentive Act of 1980, BDCs (Business Development Companies) are designed to support small and developing U.S. companies. According to The National Center For The Middle Market, there are over 200,000 middle-market businesses in the U.S., employing over 48 million people, representing one-third of the private sector GDP. This category represents the pulse of the American Dream.

BDCs themselves have different focus areas, with larger ones primarily pursuing first-line senior secured loans, while smaller players concentrating on niches like asset-based lending, equipment financing, life sciences loans, or venture growth financing. They provide capital in different forms to their borrowers, and collect interest payments at rates often in the +10% ranges, regardless of the interest rate landscape.

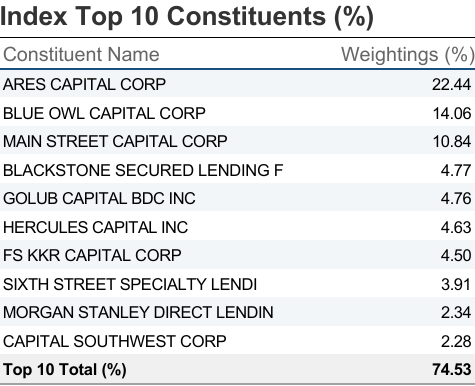

You can invest in time-tested BDCs like Ares Capital Corporation (ARCC) or Main Street Capital Corp (MAIN), focus on custom-lending solutions pursued by Capital Southwest Corporation (CSWC), or lean towards growth sectors through Runway Growth Finance Corp (RWAY) and Trinity Capital (TRIN). Or you could buy the entire basket of BDCs, in a market-cap weighted approach.

VanEck BDC Income ETF (BIZD) invests in 30 public BDCs with market-cap weighted allocation levels. This means ARCC, the largest public BDC, is its top holding, representing 22.4% of invested assets, followed by Blue Owl Capital Corporation (OBDC) at 14%. Source

Fact Sheet

Public BDCs provide exposure to over 4,800 middle-market companies. This makes BIZD a large, diversified fund that benefits from the power of the American Economy, almost as the equivalent of the S&P 500 (S&P 5000, anyone?) for middle-market companies.

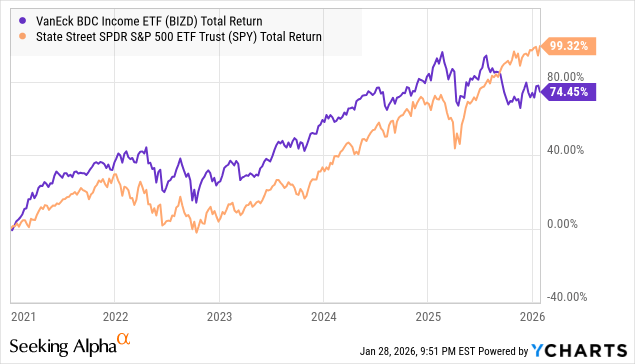

Now, just because of the focus on middle-market companies, BIZD’s 5-year performance against the popular index is not to be underestimated. The ETF has beaten the S&P 500 in the post-COVID recovery, as well as the AI-infused market recovery since 2021, with one notable divergence in mid-2025.

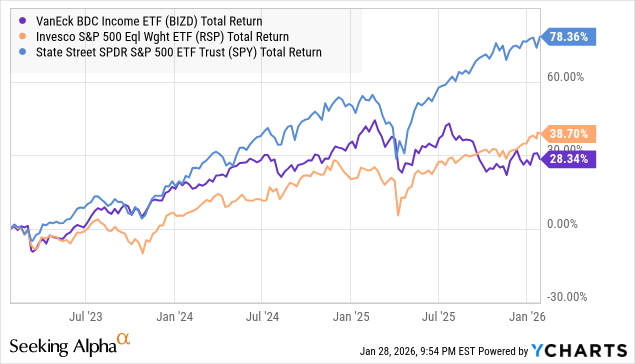

Looking at the 3-year period, the S&P 500 has largely been propelled by the mag-7, and this disconnect from the rest of the index is seen from the equal-weighted S&P 500 significantly underperforming the popular benchmark index. BIZD’s struggles are clearly seen in mid 2025, following the anxiety related to private credit.

Market jitters around private debt quality, caused by the bankruptcy of First Brands and Tricolor, resulted in a steep sell-off in BDCs. None of the larger BDCs invested in either, and despite what the market fears or believes, debt will continue to be a driver for corporate and middle-market America for the foreseeable future.

With over $500 billion in aggregate assets, BDCs represent a major pillar in middle-market debt. A belief in widespread defaults across this segment is not just a bearish view on BDCs; it is a bearish view on the broader economy and capital markets.

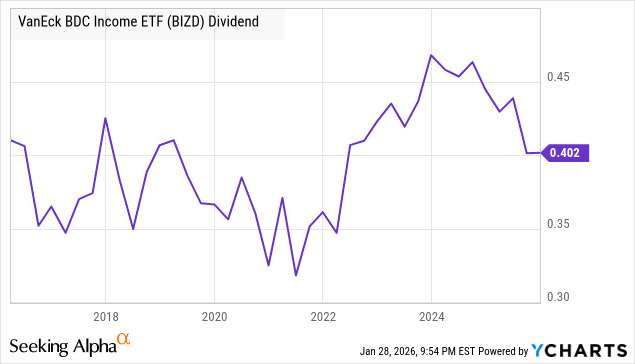

BIZD maintains a variable distribution policy, and its current yield can be estimated at 11.5%. The ETF has delivered reliable distributions over the past ten years, with levels only modestly lower amidst the post-COVID-19 near-zero interest rate conditions.

BDCs benefit from higher rates, but they also benefit from more loan origination at slightly lower rates. We will note that BDCs continue to operate below the midpoint of their target leverage levels, indicating room for expansion. With declining interest rates and massive investment in data centers, and industrial & manufacturing operations, we expect tailwinds for BDC loan origination activity, and BIZD lets you regularly put a portion of all that action in your pocket.

Pick #2: COF Preferreds – Up To 6.4% Yield

Following the acquisition of Discover,Capital One Financial (COF) became the largest credit card issuer and the sixth-largest bank in the U.S., with total assets of around $660 billion.

The acquisition is expected to result in significant cost savings while positioning the bank for expanded market share and profit synergies.

The Trump Administration seems to want to impose a 1-year, 10% cap on credit card interest rates and also slash interchange fees. This would be problematic for card issuers, but we want to emphasize that such a significant change requires legislation, and it will still face legal challenges by the biggest banks in America. The Federal Government does not dictate rates that lenders can charge, because there are complex underwriting functions to determine that based on borrower profile and financial stature.

Looking at it from a business angle, attempts to dictate credit pricing tend to produce the opposite of the intended outcome of improving affordability. Banks will tighten underwriting, reduce approvals, and shift activity toward higher fees, and other products like line of credit, personal loans, and BNPL. Cuts to interchange fees will lead to sharp reductions in perks and rewards. Overall, lower access to credit is bad for consumers and bad for the economy in general.

Every industry, from time to time, receives the threat of regulation. This doesn’t push the industry out of business, but pushes them to evolve, and those who innovate through the challenges thrive. Capital One has specialized in technology-driven lending for over three decades, successfully navigating numerous regulatory changes and economic cycles. We seek to take advantage of the market panic, but invest with a higher degree of safety with COF preferreds.

COF’s card business continues to deliver growing purchase volume, boosted by the synergies from Discover, up 39% YoY. The provision for credit losses rose by $280 million YoY, and the Net charge-off rate was 4.61% at the end of Q3, comparable to pre-pandemic levels. The acquisition reflected strong consumer banking as well, with Q3 ending deposits of $107.2 billion (up 35% YoY), and auto loan originations up 17% YoY to $1.6 billion. COF finished Q3 with excellent regulatory capital ratios, with the Discover merger positioning the bank as a leader in consumer banking, lending, and credit, providing financial flexibility to millions of consumers in America (and U.K. and Canada)

During the first nine months of 2025, COF spent $1 billion on common stock and $195 million on preferred stock dividends, compared to $3.2 billion in net income during Q3. The preferreds enjoy excellent coverage and safety, and pay qualified dividends to eligible shareholders.

5.00% Non-Cumulative Perpetual Preferred Series I (COF.PR.I) – Yield 6.3%

4.80% Non-Cumulative Perpetual Preferred Series J (COF.PR.J) – Yield 6.4%

4.625% Non-Cumulative Perpetual Preferred Series K (COF.PR.K) – Yield 6.4%

4.375% Non-Cumulative Perpetual Preferred Series L (COF.PR.L) – Yield 6.4%

4.25% Non-Cumulative Perpetual Preferred Series N (COF.PR.N) – Yield 6.3%

Currently, COF-L and COF-N offer ~6.4% yields, with ~45% upside to par, which makes it a safer choice for strong total returns in the rate cut cycle.

Conclusion

Flexibility is rarely free. In most areas of modern lifestyle, you pay extra to keep your options open, and those who provide flexibility are the ones who get paid.

BDCs supply capital to the businesses that drive employment, growth, and innovation, filling a giant void left behind by traditional financing options. Banking institutions extend credit and liquidity to millions of consumers to help them enhance their affordability and better manage their cash flows. In both cases, investors are compensated not for speculation but for enabling the system to function. With picks like this in your portfolio, the income you generate isn’t just return; it is the fee you get paid for flexibility. This is the beauty of our Income Method.