Investment Trust Dividends

Markets are ending May with a strange but powerful mix: huge enthusiasm for AI-linked companies, relief over lower oil prices, and a broader rally that has spread well beyond tech. The result is a market that looks confident.

Romain Fournier

Published on 05/29/2026 at 08:57 am EDT – Modified on 05/29/2026 at 09:09 am EDT

+3.84%

+3.95%

HEWLETT PACKARD ENTERPRISE COMPANY

+2.72%

+0.58%

+3.47%

May is coming to an end on markets, and it is time to take stock of what the month has delivered. Dell jumped 39% after hours after reporting results and raising its guidance. The company is worth about $206 billion, which means it could be closer to $280 billion when trading opens on Wall Street. Anthropic, the private AI group behind Claude, has raised funds at a valuation of $965 billion, just above OpenAI’s latest valuation. SpaceX has reportedly trimmed its valuation target for next month’s planned IPO: the new goal is said to be closer to $1.8 trillion than the hoped-for $2 trillion. Given that people were still talking about $1 trillion only a few months ago, this is the kind of downgrade most companies would frame and hang in reception.

The common thread linking Dell, Anthropic, and SpaceX is their close connection to AI. Yet exuberance is not limited to that part of the market. Yesterday, discount retailer Dollar Tree and electronics chain Best Buy each surged more than 15% after their results. In short, there is action almost everywhere.

The S&P 500 gained 4.9% in May and is up 10.5% in 2026. That still leaves it well behind Japan, which rose 9.4% in May and 28.4% this year. But both have been flattened by South Korea, up 24% in May and 94% in 2026. Oil is down 17% in May, helped by hopes of easing tensions in the Middle East. That is good news for the economy, although crude remains up 50% this year. Gold is down 2.5% for the month and is now up only 4.4% in 2026. Bitcoin fell 4% in May and is down 16% for the year.

Today, investors are buying the idea that the Middle East may be stepping back from the edge. The S&P 500, Nasdaq, and Dow all moved higher as reports of a tentative U.S.-Iran agreement gave markets something they badly wanted: a reason to worry a little less. The reported deal would extend the U.S.-Iran ceasefire by 60 days and ease restrictions on shipping through the Strait of Hormuz, one of the world’s most important oil routes. Brent crude fell to about $91 a barrel, while West Texas Intermediate dropped to around $88.

Still, the ceasefire story comes with several asterisks. Donald Trump has not yet approved the memorandum. Iran has not formally responded to the latest version. Vice President JD Vance said talks are progressing but remain ongoing, while Treasury Secretary Scott Bessent described the negotiations as a continuing back-and-forth. There are also hard reminders that this is not a done deal. Iran reportedly fired missiles at unidentified targets on Thursday. The Pentagon said Iran launched a ballistic missile toward Kuwait and used attack drones in the Strait of Hormuz.

Today’s company news shows the AI narrative is still strong. As I mentioned above, Dell surged after raising its full-year revenue and profit forecasts, a sign that the AI infrastructure boom still has plenty of market power behind it. Hewlett Packard Enterprise and Super Micro Computer rallied too.

But not every corner of the economy looks so confident. The Gap shares fell sharply after the retailer cut its annual sales forecast, pointing to pressure on budget-conscious consumers. Costco, meanwhile, reported higher fiscal third-quarter earnings and revenue, offering a more stable read on consumer spending. The company is often treated as a rough thermometer for the American household. Its results suggest consumers are still spending, especially where they see value.

Today’s economic calendar gives investors more to chew on. The April trade-in-goods report is expected to show the deficit narrowing slightly to about $87 billion from $87.4 billion. The Chicago purchasing managers index is expected to rise to 50.3 from 49.2, which would put it just above the line separating contraction from expansion. Several Fed officials are also speaking today, including Michelle Bowman, Anna Paulson, Neel Kashkari, and Mary Daly.

I’ve bought for the SNOWBALL, using spare cash, 13 shares in XSTR for £2,367.00

Only yields 4% but builds up the cash pot to buy some bargains when the market turn downs, until then keep banking the dividends when they are paid.

May 20, 2026 DMLP, LYB, O, PFFA

Follow Seeking Alpha on Google for the latest stock news

Transcript

Rena Sherbill: Will Barton from High Dividend Opportunities. Great to have you back on Investing Experts. Thanks for coming back on.

Will Barton: Thanks for having me, Rena.

Rena Sherbill: It’s great to have you. So first things first, you have some sale news happening at High Dividend Opportunities. I think that’s a great place to start because a lot of people are looking at the market, wondering how to play it.

You’re going to be talking about, obviously, some high dividend opportunities and how you’re thinking about things. But let investors know, let listeners know what you have going on at your service, please.

Will Barton: Yes, right now we have a Memorial Day sale. It is 28 % off of an annual membership. So that’s five hundred thirty six dollars for the year and we’re going to be running that sale through May 26 and it’s an opportunity for people to get the first year at a discount and really give our service a full year to try it out and check out our ideas.

We find that most people who join for a year, tend to stick around for a long time. We’re a very long-term focused service, focusing on investments over three to five-year investment horizons, rather than a daily trading service.

So to get the most out of our service, find that giving people an opportunity to try us out at a reduced price for a full year gives them that opportunity to really check out all of the tools and everything that we have to offer.

Rena Sherbill: I think that notion of long-term investing is, or relatively, let’s say, relatively long-term investing, I think is a good place to start because, you know, there’s volatility in the market, a lot of questions about price and value and how to properly value companies.

How are you thinking about the long-term nature? And what do you, when you look at the, do you even look at the VIX? Are you paying attention to market volatility? Maybe let’s start there in terms of how you think about the long-term nature of investing.

Will Barton: Well, our strategy is an income focused strategy, right? So our goal is to have an eight to 10 % average yield on our portfolio at any given time and to have that solid, steady income stream coming in so that you have enough money to withdraw some if you need some, if you’re in that retirement age and you’re actually taking money out of your portfolio to live off of and you have enough leftover to reinvest.

We recommend that even if you’re retired, you plan on reinvesting at least 25% of the income that’s coming into your portfolio so that you always have money available to be buying stocks.

And in that respect, we really are permabulls. We are always buying something.

As things change, we change what we’re buying. We buy things that we believe are relatively good values right now based on current conditions. But we’re always buying stocks, right?

We’re never going to say, hey, sell your whole portfolio and let’s just hunker down into a turtle and hope that the market doesn’t keep going up.

Because I think the market today is kind of an example of how if you go back to like early March when the whole Iranian war started, if you would have told people that the Strait of Hormuz is still going to be closed in May anybody would have told you, well, you should sell all of your stocks.

And yet we’re sitting here today with the market pushing all time highs. The market doesn’t always do what you’re expecting, even if you happen to have a crystal ball and know what the future is.

I can’t tell you what the news is going to be tomorrow. And so we really focus on what’s the opportunity that we can buy today. What is the market giving us?

What holdings do we have that are getting too expensive and the market’s giving us a good price to exit and deploy somewhere else? Because even in a expensive market like today, there are still a lot of great opportunities out there to take advantage of.

Rena Sherbill: So what opportunities would you highlight right now?

Will Barton: Right now, the area that I really like right now is commodities. And in particular, we have some oil royalty companies, for example, Dorchester Minerals, (DMLP) is a royalty company. They make money from American oil that’s being pumped and sold.

Even if everything works out great and the Strait of Hormuz opens up tomorrow, the price of oil has fundamentally changed for certainly the next year or two.

And so they’re a direct beneficiary of that. They don’t have a lot of hedges. So as oil prices go up, that’s going right to their bottom line. And so we expect to see a lot more dividends coming out of them.

They pay a variable dividend. So it’s completely dependent upon quarter to quarter, how much the oil price is. And we expect to see a lot more flowing out of them.

So that’s probably one of the most immediate examples of, hey, the market is giving us an opportunity here to buy income. It’s still at a very reasonably price, reasonable price, and we can expect it’s going to be higher for the next year or two.

Rena Sherbill: And what makes you get out of that?

Will Barton: Well, the last time we actually ended up exiting when oil prices were still high because the price just got high especially with these variable dividend companies what you often see is when they declare the higher dividends people start buying it like crazy they look at well the yields high now.

So now I’m gonna buy well, okay, but it’s variable. So when oil comes back down in price the dividends will come back down and so we exited that when it was trading in the mid thirties and we just decided that, okay, well our forward outlook is that the distributions are going to be smaller and it no longer fits our investment profile.

We started buying it back last December when oil was low and we’ve had kind of a little fortunate bounce in oil prices, but the price was lower and even at the lower prices, we determined that, okay, the distribution still makes sense, still achieving our goals, still helping us hit our targets.

And now even right now, I think today’s trading around 28-ish, it’s still a very good price to be buying to take advantage of what you can expect the distributions to be over the next year or two.

Rena Sherbill: How much does the interest rate conversation affect how you’re looking at things? And does that correlate at all to dividend cuts? Do you see that being a correlation at all? There were, you know, we have a new Fed chair. There’s a lot of talk of expectations being changed, that rate hikes are coming. How much does that play into your thinking?

Will Barton: We generally don’t try to predict what interest rates are going to do in terms of choosing our investments. It’s one of those things that, it has a direct and immediate impact, but predicting them is hard. We have our market outlook every week where we try to predict what’s going to happen.

And just like everybody else, we can be as wrong about rates as anybody else can, right? So what we do again, is we kind of go back to that taking the opportunities that the market gives us.

The 30 year is up a lot today, we’re buying municipal bonds. We have a couple of municipal bond funds in our portfolio.

Is the current height going to be as high as it goes? Who knows, right? It could keep going to 6 % for all I know. But what I do know is that when you’re getting 5.1 % on municipal bonds, compared to the last 20 years, that’s a really good interest rate to be receiving.

If it keeps going up, the price will keep coming down. But again, we’re investing for the dividend.

So when we get the dividends, we’re reinvesting 25 % of it. If the price is lower in the future, we’re happy to just average down and get higher yields. In the grand scheme, when you’re at 20 year highs on interest rates, in the big picture, they’re going to be lower at some point in the future.

We’re still going to be investing at some point in the future. So I’m very eager to be taking advantage of higher rates because they manifest themselves as lower prices for income investors.

I see a lot of dividend stocks are lower in price because interest rates are high, because traders are using that calculation of, well, I can get X percent from the U.S. Treasuries and I’m only getting X percent from this dividend stock.

So I’m going to sell dividend stock and go invest in treasuries today. And for those of us who are just buying the dividend stocks with the plan of holding them for the next three, five, 10 years, we’re buying at a lower price than we’ve been able to buy in the last three to five years.

And that’s in an environment where the stock market itself is trading at multi-decade high valuations.

For income investors, high rates are great, right? We’re getting paid interest rates. That’s what generates our income at the end of the day. It’s coming from interest rates, higher interest rates means we’re getting higher income for every dollar that we’re able to invest today.

And we should be taking advantage of that because maybe it goes on for the next year or two. Maybe it could continue for the next five years. I doubt it, but possible. But at some point in the future, I guarantee we’re going to be looking back at 2025, 2026 and say, boy, I wish I would have bought more dividend stocks back then because they were so cheap.

Rena Sherbill: What is something in your portfolio that you would say you’re at the tail end of the three to five years thought process in terms of holding it? What might be something that investors might be surprised to know that you still hold? Or maybe something that is a good example of holding onto something despite what market sentiment might be telling you?

Will Barton: I would say the example right now that is probably going to be reaching that tail in the next couple of years is our agency mortgage rates. We bought those as the prices were collapsing, they were becoming very unpopular because they are very interest rate sensitive.

And what we saw in prior cycles is when interest rates get cut down and you have that huge spike where the 30 year mortgage and the, and the overnight Fed rate has a huge gap.

You’ll see a big, huge spike up in the prices of these. you know, we, we’ve seen a couple of the last year and half since about early 2025, they’ve really been spiking up. they’re starting to trade at a premium to book value now, and they’re starting to gain more favor among traders. we believe that we have a lot more upside to go.

But probably within the next year or two, especially if we have a situation where the U S economy breaks and the fed starts cutting rates like crazy, they’ll have a blowout.

And at that point, we’re going to have to make the decision whether we want to hold through the cycle or whether we want to sell an exit. know, most recently, an example that we actually ended up exiting it a lot earlier than we intended to was LyondellBasell (LYB) because of the situation that I ran, their price just ran away from us.

We predicted fair value was between $80 and $90 and it got there. okay. Love you, goodbye, mostly goodbye. And we redeployed that money where it can make us more dividends later.

Rena Sherbill: How did you arrive at the 25 % figure in terms of reinvestments?

Will Barton: We did that through a combination of our experience and we did some pretty extensive back testing using a tool called Portfolio Visualizer that lets you test with a portfolio what it looks like as you’re withdrawing money.

Our goal was to ensure that the amount you’re taking out is low enough or high enough that it can absorb any dividend fluctuations, know, natural dividend cuts that you’re going to get through a crisis situation.

So we back tested it against both the great financial crisis and through COVID with actual holdings that we actually held to make sure that you had a solid cushion of reinvestment there so that the dividend cuts never actually impacted your ability to withdraw money.

And then also ensure that you’re reinvesting some at all times so that you can build up that cushion. And so we did that through a combination of both comparing notes from all of us at Seek High Dividend Opportunities. We compared our holdings and what we experienced with our own personal drawdowns and then did some back testing using the portfolio visualizer tool to make sure that there was a big enough cushion of safety there. you know, obviously nothing is a hundred percent certain.

You can’t predict the future, but for the great financial crisis and for COVID, which was two of the largest dividend cut runs in the history of the stock market, it was sufficient for those.

And really from our perspective, it gives you that even if you went over that 25 % right cuts went deeper. You found yourself starting to run low. It wasn’t enough. It gives you that warning signal that you can say, hey, I need to change something in my portfolio.

I need to change something about what I’m withdrawing and you can do that very early on and all financial problems. If you know there’s a problem and you address it sooner, it’s a lot easier to fix than if you wait until you’re in mid-disaster and the sooner you solve financial problems, the easier they are to solve, the less you have to sacrifice.

And you don’t want to be finding out when you’re 90, 95 years old, hey, my portfolio is not going to last the rest of my life.

I mean, right at this moment, most people are feeling invincible, right? Stock market’s at all time highs. They’re looking at these big balances and it’s for people who have went through the dot-com bust, who went through the great financial crisis.

I think a lot of investors today who are in their 60s, 70s, they lived through them, but they weren’t necessarily investing a lot through them because they were still in their working years. And in your working years, it’s very easy to close your eyes and ignore the losses and just keep contributing more money because you have income coming in.

And it becomes a lot more challenging when you don’t have a job that you can just go, okay, well, I can just throw a few more thousand dollars in every paycheck and be fine.

You don’t have that option and you don’t have the distraction of, I have to go to work and I’m not paying attention to what’s happening in my portfolio. I’ll see what next quarter, right? And when you get to be in your sixties and seventies and you actually start living off of the money and you’re watching that portfolio value every single day.

I think a lot of people look at it and they’re looking today and they’re going, wow. Where everything’s great. I have lots of money. I’ve made so much money in the past five years. you know, stock market pretty much rebounded from COVID very quickly. It wasn’t an extended drawdown.

So I think people will have a false sense of confidence that well, whatever, if it goes down for a few months, I’m fine. I have six months of reserve. have, you know, 12 months open emergency fund or whatever it is. I can pay my bills.

The stock market will recover, dot-com bust it took 10 years for it to get back to even without you withdrawing any money. And if you withdrew any money at all, it took even longer.

Well, if you’re 70 years old and the dot-com bust happens, 10 years is a long time to go without withdrawing any money from your brokerage account. And I think a lot of people just don’t have that perspective, but that can happen again because they lived through it, but they weren’t investing through it.

They weren’t dependent on their portfolio through it. And that gives them this false sense of confidence that, that’s not going to happen to me. it’s something that you can’t understand until you’re in that position. And when you’re in that position, it’s too late.

Rena Sherbill: Is there something that you mostly hear from subscribers in a market like this? Are you getting a lot of questions? What do you, what’s mostly the feedback that you get from subscribers or what are the most asked questions?

Will Barton: The most asked questions inevitably take the format of given this news story and they’ll pull up some news story whether it’s about Iran or whether it’s about interest rates or you know, whatever the president tweeted this morning You know given this news story. How should this impact how we invest? that’s probably the most frequent question that I see and

sometimes people will give me little bit of pushback and resistance when I say it doesn’t matter. We’re not investing because of what we think the news cycle is going to be. I’m not buying something going, okay, well, I think interest rates are going to go up 50 basis points, so I’m gonna buy this.

No, I’m buying it because I think it’s cheap. If interest rates go up, maybe it gets cheaper. If they go down, it’s gonna go up. Eventually interest rates are gonna go down. I don’t know when.

I don’t need to predict when because I’m getting paid a dividend to sit there and collect money wventually things will go or will turn around. I mentioned the MLP earlier and when we underwrote that we said, okay are we happy with the distribution that they will pay if oil is $55 a barrel?

We said yes, we didn’t know oil was gonna go up to $100 a barrel when we bought that we have no clue. If I had to guess, obviously at some point in the future, I can predict that something’s going to happen somewhere in the world at some point and oil is going to go up to $100 a barrel.

I don’t think that’s a hard prediction to make. I had an economics professor who liked to say, it’s very easy to predict what will happen. It’s extremely hard to predict when it’s going to happen. And so we just position ourselves to be buying.

And we know that at some point in the future conditions will change. We know that at some point in the future oil will go up, interest rates will come down. And we position ourselves for those eventualities and we’re collecting dividends the whole time that we wait. And when they happen, then we’ll make that decision whether or not to sell.

Rena Sherbill: You mentioned REITs before, and I know that’s one of your main focuses at High Dividend Opportunities. What would you say about the real estate space right now and any other kind of points to highlight for investors when it comes to REITs?

Will Barton: Well, real estate is a very interesting investment right now because it is one of those that high interest rates are bad, right? In the real estate world, everybody borrows money. doesn’t matter how wealthy you are or how much cash you have on hand, you’re going to use leverage, you’re going to use mortgages, you’re going to leverage it because that’s how money is made in real estate. And it’s an asset that’s very easy to borrow against. And so…

When you have interest rates high like they are right now, we’ve seen a big pullback in commercial real estate of money moving in. People have been buying less. We’re starting to see some private equity start taking big stakes in real estate now, and that’s been kind of a tailwind for values.

they’re buying because the cap rates, the capitalization rates, is essentially how much money you’re getting from that real estate compared to how much you pay, are at 20 year highs. And so they’re buying low.

And then on the other hand, you have the factor that real estate is considered a relatively safe asset. It’s a hard asset that people like to buy when there’s instability. And so that kind of positions real estate right now to, see a big recovery through the combination of interest rates coming down and generalized fear about the economy. you know, and there will be moving from what’s

a very low price today, potentially go much higher in price. so real estate is one of those assets that we really like right now. The options for high yield in real estate are not what they used to be. There used to be a day back in the early 2000s, REITs were a fringe alternative investment that only crazy people invested in.

And it didn’t really get tracked a lot of attention. So you could get eight, nine, 10 % yields was the normal. Even today at today’s lower prices, you’re more in that three to 6 % range for most of them.

There’s a few pockets of opportunities where you have some, a little bit of distress, where there have been some real issues with tenants having trouble meeting their rent obligations and stuff. and so that creates lower prices and higher yields. I think those areas are potentially really good opportunities. Obviously you have to deal with the risk that the tenants could continue to see deterioration in their ability to pay the rents.

And so you got a little bit of risk to go with that reward right there. But the overall picture REITs are in a position to see some big improvements in valuation. You have Realty Income (O). That’s out there trading for 14, 15 times FFO. It’s rock solid, high quality REITs you can get. They shouldn’t be trading that cheap. They should be trading in the high teens, low twenties.

But especially when you compare them to the rest of the S &P 500 that is trading at those higher multiples, and it’s just dirt cheap right now. So definitely something that’s worth adding to.

It becomes a little bit of a struggle for us with our 8 to 10 % goal, because a lot of the REITs just aren’t paying those high dividends right now. But you definitely have some great dividend growth opportunities there. And if your portfolio is already high yielding and you can afford to hold some of those lower, you know, five, 6 % yielders.

There’s a lot to choose from in that ballpark.

Rena Sherbill: When you talk about the factors that you’re looking at in terms of how high the yield is and structures that prevent you from getting into things, are those absolute red lines that you adhere to? Are there any exceptions that you make to those rules?

Will Barton: We definitely do. Our goal is an average of 8 to 10 percent, right? So we want the whole entire portfolio to be averaging in that range. In the current environment, we’re able to have some very high yielders, which also then gives us room to go on the low end and hold some of the lower yielding companies that have some dividend growth.

Usually if we’re looking at something that’s below 7%, we want to have a growth component or an expectation that this is a company that will be able to gross dividend in the future. We don’t draw a hard line.

But we are always conscious of what is this doing to our overall portfolio yield? Because you know, that’s what that’s what we promise our members is that we’re going to find a way to keep our portfolio averaging in that eight to ten percent range and growing your income every year

And that’s, you know, in some environments is easier than others. Currently, there’s a lot of high yield options out there. And that’s made it a lot easier for us to take on some of the lower yielding picks and take advantage of being able to realize some capital gains and have some capital gains growth as well. In addition, you know, we go back to an environment like 2021, we were struggling to hold the seven to 8 % line, right? Because

The yields were just, everything was so expensive. And it was a very different interest rate environment. so, depending on the environment, depending on what the market gives us, we will take advantage of opportunities where we see them, but we’re going to remain very steadfast on averaging that 8 to 10 % through the portfolio as a whole.

Rena Sherbill: Last time you were on, which was at the end of February, you were talking about being interested in high yield preferreds. Anything to note there or any updates to make there? You were talking about AGN CZ in particular.

Will Barton: And we’re still kind of in that zone, right? Where preferreds have actually come down a little bit in price, yields have gone up a little bit.

We’ve talked a lot about (PFFA), Virtus InfraCap, and that’s a preferred ETF that really kind of mirrors our strategy in the preferred space.

They have a lot of overlap with our holdings and they invest in preferred on a leverage basis. So that’s an ETF that is kind of really a great place to start to get invested in the preferred right away and have exposure to a wide variety of them.

But preferreds have generally come down in price because they’re tied to that long-term yields. As the 10 to 30 year treasury yields go up, preferred prices will come down and we still see a great buying opportunity.

Our preferred portfolio, I think we have 48 prefers in our portfolio right now.

And so that remains a very large part of our overall strategy to provide us that fixed solid income that’s coming in every single quarter and is going to be more resistant in the event that the economy gets weakened.

So that’s definitely an area that we’re still continuing to focus on.

Rena Sherbill: And any other notes to make about the bond market? George Noble was on recently talking about the disarray that he sees in the bond market. Anything to note there or anything else to note there?

Will Barton: I think it’s a lot of people make mountains out of molehills in the bond market, especially when you start getting politics involved. People like to talk about the deficit. Every once in a while, you’ll see the stories start popping up about how, well, the treasury auctions are getting weak and it’s because people don’t have confidence in the US government or whatever.

And that’s one of those things that I think the fear plays well on TV. I don’t buy it. know, treasury bond options fail because interest rates are going higher and the people aren’t going to go bid on something when they believe the price is going to go down. So that’s, well we think the US government is going to default on their, on their bonds or we don’t have confidence in the U S government or anything like that.

It has nothing to do with that. It’s purely a transactional thing. and so I think a lot of people interpret the short-term trading that’s being done by institutions and hedge funds to try to squeeze a little bit of money out of bonds because it’s a zero risk asset, right? You can make a trade with bonds and if you mess up, well, it’s not, you’re not going to lose your shirt in the bond market.

And so I think a lot of people see, some movements that might not be expected or might be larger than expected. And they try to read way too deeply into it.

And ultimately at the end of the day, the U S government bonds are rock solid. If they go under, it doesn’t matter. Your brokerage is the U S dollar is failing. So guess what your brokerage is dominated in. It’s all U S dollars.

It’s one of those catastrophic things that it doesn’t matter. It’s like, okay, well, what if an alien comes and blows up the entire earth? Okay, then it doesn’t matter what you invested in, does it?

And it’s kind of one of those situations where I think it plays well on TV. It gets people worked up over things. Some people like to use it for political gain to, you know, attack the other side over the deficits or whatever.

But I don’t think there’s any sign that anybody is concerned about the US government’s ability to pay its debt. The US is still one of the top economies in the world. We’re going to remain that way for the foreseeable future and people are going to want to own US Treasury bonds.

And so I think a lot of that tends to get glazed over try to get attention, but at the end of the day, it’s one of the safest investments out there. the pricing movements are reactions to what people think treasury price bonds are going to do.

They’re trying to run ahead of it. They’re trying to get ahead of the curve. They’re trying to profit from it. They’re not voting on whether or not they think the US government is well-ran or poorly-ran or whatever, right?

They are just trying to make money and they’re trying to predict what people are going to do. people can be predictable sometimes and sometimes they can be very unpredictable.

Rena Sherbill: Yeah, I bet more alien questions coming our way given the news cycle too. I’d look out for those.

Will Barton: Yes, you need an ETF.

Rena Sherbill: I bet it’s not that far away. I can see the letters forming already.

What else would you encourage investors to be thinking about or not thinking about these days? Income investors in particular.

Will Barton: I think the biggest thing to think about is to have realistic expectations for the future.

The market has been doing very well. It’s been very strong and it becomes easy to just kind of assume that what’s happening is going to continue to happen. And I think it’s very important to take a look at your personal finances, and take a look at, this is what is in my portfolio.

Do I need to take money out of this portfolio? Am I going to need to take money out in the next five years? And, well, core inflation is going to exclude things like gas prices and food.

Gas prices in food when you’re retired are going to be very significant to how much money you need. They’re not optional expenses for you. So you want to make sure that you have some flexibility, both in your personal budget and in your portfolio. If you’re withdrawing money, especially, you want to make sure that you can withdraw money without being forced to sell stocks.

If you sell a share, you want it to be because you’ve made the affirmative decision that this investment is no longer good for me or this investment is too expensive. want to take profits, which is hopefully what’s happening.

You don’t want to be forced to sell because you have to pay your electric bill next month because that’s what will kill your portfolio very quickly. so I think investors kind of need to, it’s a great time to do an assessment.

How much money am I relying on my stock portfolio for? How much flexibility do I have in my personal budget? If things go up in price that I can, what expenses am I willing to get rid of? What expenses am I willing to, that I can’t or am unwilling to change?

And is my portfolio producing enough income so that if we see dividend cuts, if we see the economy collapse, am I still going to be okay?

Because if you reach that point where you can say, yeah, I not only answer is going to be okay, it’s going to be easy. you know, I’m not going to have to worry about my personal bills.

And when you can get to that point, that allows you to look at the stock market with a lot of clarity and be very calm about the swings that happen because you know, my bills are taken care of. All I have to worry about is what is the best decision right now for my investments and you’re making investment decisions based on your investments, not based on any external, you know, concerns or fears about being able to cover your home expenses.

And that’s kind of a really what the income method is designed to do to provide you that base so that you know, my bills are paid. Now that my bills are paid, now I can go into the market. Now I can look out there and decide to speculate.

When something crashes, I can say, well, we go buy a few shares of this and see if it recovers because I don’t have to worry about paying my bills next month. That’s taken care of. I can now just look at the companies, decide what companies I want to buy.

And I think that’s really where a lot of people, they get turned around in the market. They get focused on, well, I want to make the most of my money right now.

But if you can’t pay your bills, it doesn’t matter. If you owned Amazon in 2001 or 2002, it didn’t matter that Amazon was going to become one of the greatest investments in the next 20 years. Because if you had to sell it in 2001 or 2002, you didn’t realize that upside. If you had to pay a bill, you sold it to pay a bill. You don’t get to participate in the upside from now on.

I think our investment style isn’t contradictory to people who want to invest in those growth investments and try to get those, you know, those big huge wins and try to predict the next Nvidia (NVDA) or who want to participate in the SpaceX (SPACE) IPO and see if that’s going to blow up and to be the next big thing. It’s not contradictory to that.

It’s making sure your bills are paid so that you can take your excess and go out there and make those bets, invest in those companies and not have to worry, not be dependent on it to meet your personal financial needs.

Rena Sherbill: Appreciate the conversation, Will. It’s High Dividend Opportunities on Seeking Alpha. Any final words?

Will Barton: I also would like to put out a plug here. We have a new YouTube channel, it’s Income Method Investing.

And we are releasing videos on that for people who like the video format. And so that will also be available to members through our video on Seeking Alpha as well. That’s a new project. It’s a little bit of a different format for me. I’ve been used to being a writer, but we’re expanding into the video world as well now.

The SNOWBALL plans to earn around 1k of income a month for this year.

Current income for this year £6,732, there are 1k of dividends for June, so at the halfway stage of the year, the SNOWBALL is ahead of plan.

Current cash for re-investment £22,653.00

I’ve sold the SNOWBALL shares in NRR for a profit of £200. At the open there is a wide spread and as the results are due next week, it could mean being trapped in the share if the results are not as expected.

I’ve sold the shares in FGEN for a total profit of £725.

I may buyback some of the shares before their xd date next week.

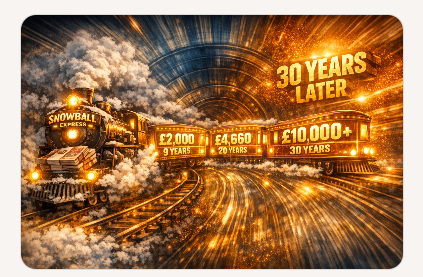

You do not need to take big chances with your money but you do have to trade reward/risk. We will use the chart of CTY, the ultimate belt and braces Trust as they have paid increased dividends for over 50 Years.

The chart with a simple re-invest the dividends plan has gone up from £3.25 to £9.30.

Looking at the chart, you will notice the price never moves up in a straight line, after 4 years the price is where you started from, although you own more shares. The recent price action, compared to it’s history, indicates the price is overbought.

The dividend has risen gently from 16.45p to 22.1p. A yield on buying price of 6.5%

Having achieved the Holy Grail of Investing, using a lot of hindsight, you could sell some shares, whilst retaining your original stake, buy two more positions to try and do it again, while still earning income from CTY, that sits in your account at zero, zilch, nothing.

May 20, 2026

Rida Morwa

Investing Group Lead

Follow Seeking Alpha on Google for the latest stock news

Co-authored with Beyond Saving

You are preparing for retirement, or maybe you have recently retired, and you have decided that you want to manage your own investments.

Congratulations! You have already taken two steps that a very large number of people never take: you saved up capital, and you took charge of it. Too many people just go through life crossing their fingers and hoping everything will work out.

Now what?

Every day, I talk to investors who treat the stock market like a lottery ticket. They scour the market looking to make quick trades, hoping that they can buy something that will become popular and then sell it before it becomes unpopular. There are several strategies that attempt to achieve this. Some focus on technical trading signals that attempt to be ahead of the popularity curve. Others focus on trying to predict news cycles, trading in and out of sectors as their popularity increases or decreases based on what’s happening in the news cycle. Others will buy ideas that they think might become the next big thing, hoping to find the next NVIDIA Corporation (NVDA) to offset the fizzles like Beyond Meat, Inc. (BYND). All of these strategies revolve around the idea of buying a stock to sell it at some point in the future, hopefully at a higher price.

There are many ways to make money investing in the stock market, and I encourage you to find a strategy that works for you. Our strategy is different from all of those above. Our strategy isn’t to buy things because we believe we will find some sucker willing to pay a price higher than we would be willing to pay. Our strategy isn’t to spend our later years selling off the shares we worked so hard to accumulate.

We are income investors. Our strategy is to turn our portfolios into a cash-producing business. A business that produces enough cash to meet our needs in retirement and retain enough to reinvest for future growth. Today, let’s address the top three reasons why we are income investors.

The stock market is a volatile place. While we’ve been in an extended bull market where the market is green more often than not, I am old enough to remember the arrogant swagger of the dot-com bubble. Investors felt invincible; they were up so much, and everything they invested in was making so much money.

I remember going into the Great Financial Crisis; smart people were frequently saying things like, “Buy real estate, it only goes up!” People who had no construction or real estate experience at all were getting into flipping houses. Investors were piling into mortgages and mortgage derivatives.

Then the bubbles popped, the stock markets collapsed, and the people who were so sure of themselves the previous year panicked. Sure, it’s easy to say, “Don’t panic,” and that is fantastic advice. Yet, the reality is that for all of us, that big number in our brokerage account represents something that is “a lot” of money to us. When “a lot” becomes a lot less, panic is a natural reaction.

Intellectually, we can know that market sell-offs happen and that the market has always recovered in the past, and it will probably recover this time too. Yet, the very fact that sell-offs happen is proof that people sell when they get scared.

Focusing on the cash flow that your portfolio produces gives you a tangible metric that measures the underlying performance of the companies you invest in, not the emotional sentiment driving prices. When the market is falling around you, I have found that focusing on the income my portfolio is capable of producing provides a framework for working through decisions in an emotionally charged time. Instead of reacting emotionally, it gives me tangible numbers to work with and navigate stressful situations.

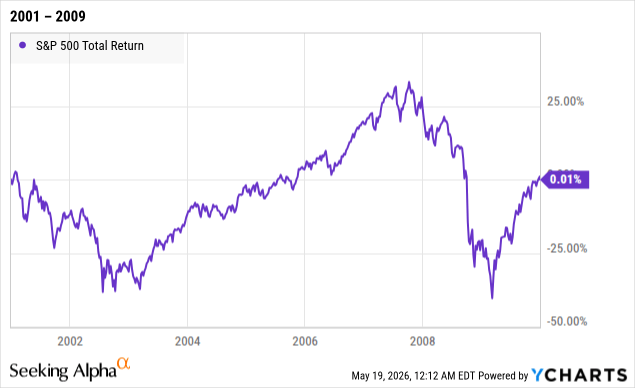

Most of us are investing for retirement, which means that we intend to withdraw money from our portfolios to pay for things while we are retired.

Many investors have the idea that they will save up $X and then, during their retirement years, withdraw a certain amount. Those withdrawals will be funded by selling shares. Which is great—if share prices go up.

However, the reality is that shares don’t always go up. They can go down, and they can stay down for a very long time. For example, from January 2001 to January 2010, the S&P 500 had a total return of 0.01%:

That is the total return with $0 withdrawn. On a $1 million portfolio, you had a gain of approximately $100. Maybe you can sell shares for more than you paid, but maybe you can’t. That is an uncertainty that all retirees have to deal with because you don’t know if you are retiring in 2001 or 2010.

Many investors have come to expect the short-term drawdowns we experienced with COVID-19 or in 2022. Those are relatively easy because it is reasonable to wait for 6-12 months to liquidate shares. When you’re 70 or 80 years old, waiting for 10 years so you can sell stock at a higher price might not be practical.

By having a portfolio that is producing income, you have a constant cash flow in your portfolio, whether prices are high or low. You get to choose how much of that cash flow to withdraw, how much to reinvest, and how much to hold in cash. When your cash flow is high enough to meet your liquidity needs, you are never forced to sell a share. Certainly, you will sometimes decide to sell shares because the market is offering you a great price, or maybe you decide the investment is no longer an attractive risk. But the key is that the decision is yours to sell because you believe it will improve your portfolio, rather than selling because you have to pay bills.

When I started investing for income, my goals were quite modest. How cool would it be if I had an income stream that was enough to pay my water bill every month? I’d never have to pay a water bill again because my portfolio would generate enough cash flow to cover that bill. After that, it became about paying the internet bill, then the electric bill, and the goal kept moving higher until the income from my investment portfolio exceeded all of my bills.

As part of the Income Method, we recommend planning on reinvesting a minimum of 25% of your income. This provides two benefits. First, it creates a built-in cushion to absorb dividend cuts and fluctuations from investments that pay variable dividends. Dividends aren’t guaranteed, and even bonds default sometimes, so it is prudent to build in a cushion so that when things happen, it doesn’t negatively impact your ability to withdraw what you need.

Second, it means that your portfolio is constantly reinvesting. You are always a net buyer, and those new shares that you are buying pay more dividends. Every month, you own more shares and are collecting more dividends than the month before. Over time, the power of compounding works its magic on your cash flow. Your income continues to grow, even if you aren’t adding any new capital to the portfolio.

That is the ultimate goal, where the cash flow your portfolio is producing is growing on its own, even as you withdraw a portion of it to fund your needs and wants. Where you don’t have to worry about outliving your portfolio because you aren’t selling it off. Your portfolio is providing the cash for you to invest more every month.

Look, there is no magic bullet when you’re investing. There is no “get rich quick” scheme that consistently works, and there are no guarantees. The Income Method isn’t about being “conservative”; it’s about being methodical. It’s about approaching your investing like a business that you are building from the ground up.

It’s about having a clear goal that is fixed, and you can clearly measure your progress. How much money do you need to retire? $1 million, $3 million? The answer greatly depends on when you retire because $1 million in 2001 is a lot less than $1 million in 2003. Stock prices change every day. How much income do you need to retire? Well, you know how much you make while you’re working, so that should give you an excellent handle on how much money you need every year to pay your bills and fund the retirement lifestyle you choose to live. That number doesn’t change, except for inflation. So, you can measure your progress clearly and know whether you are getting closer and whether you are on track. Saying “I need my portfolio to generate $80,000 in recurring cash flow” is much clearer than saying “I need a portfolio with a value of $1 million.”

When you retire, you don’t need a big lump sum of cash. Odds are that you are going to leave a substantial portion invested in the stock market, where the prices will change with the next news alert. What you need is the knowledge that you can withdraw the cash you require every single year for the rest of your life. When you retire, you are losing an income stream. So, replace your income stream with an income portfolio.

That is why I follow the Income Method.

Brett Owens, Chief Investment Strategist

Updated: May 27, 2026

Think it’s a good idea to ask ChatGPT to run your retirement portfolio?

(I know that you don’t, my careful contrarian. But we both have friends that are more than tempted to trust the bots! Here are the cautionary numbers that show AI models are not very good at running money.)

A startup called Nof1 recently ran an experiment. It handed $10,000 each to Claude, ChatGPT, Gemini, Grok and four other leading AI tools. The humans gave “seed capital” to the bots.

Here’s $10K. You have two weeks to trade US stocks. Make some money. Now GO.

How much do you think each bot turned its initial $10K into? Well, whatever you’re thinking, go lower.

The broader “bot portfolio”—all of the money given to AI—lost a third of its capital. Down 33%. In just two weeks!

What’d they do wrong? Uh, just about everything. First, they overtraded. Second, they each took the exact same marching orders but went off in completely different directions.

Grok, Elon Musk’s AI product, was (would you believe it?) the “calmest” of the bunch. Grok placed “just” 158 trades over two weeks. Usually, trading like that is a reliable way to shred money. If you and I decide we’re going to turn up the frequency of our moves to 75+ per week, our trades will be suboptimal. To put it lightly!

And, to add to the confusion, the bots moved money with different biases. Yes, even the robots have predetermined blind spots. Claude (from Anthropic) tended to go long. Gemini (from Google) shorted stocks! And Qwen, a Chinese model, leveraged up because, hey, when you’re losing money why not borrow more of it? (When you’re taking poison, who cares how much? Ha!)

The bots blew up their portfolios because they thought they knew more than they did. They pulled historical data, identified trends that worked in the past, and concluded that the future would be the same. In other words, they built trading systems on the fly that looked great in the lab but fell flat on their faces in real life!

It’s the Mike Tyson school of hard knocks. Everyone has a plan until they get punched in the face.

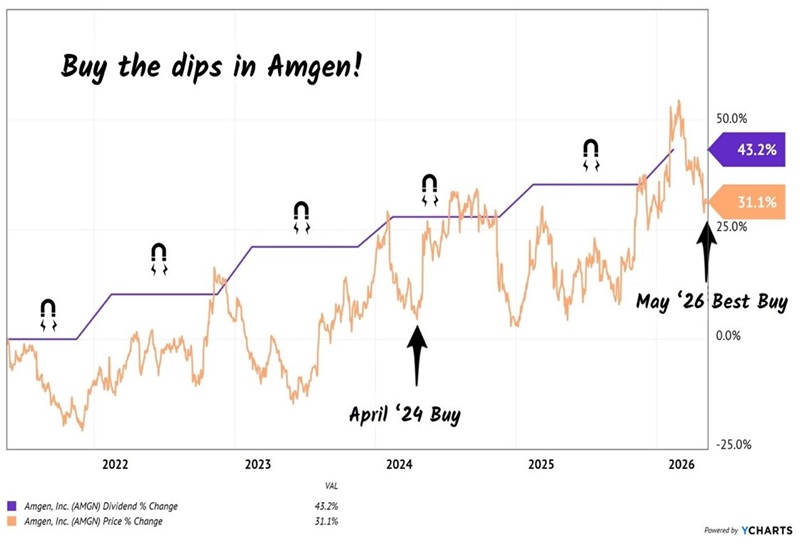

Eight bots took $10,000 down to $6,700 in two weeks — a pace that lands you at zero inside a year. Meanwhile, we contrarians have quietly compounded 30% on a blue-chip biotech the bots overlook. That stock is Amgen (AMGN).

The purple staircase below is Amgen’s dividend. The orange line is the share price, sometimes meandering but eventually racing to catch up with the dividend hikes. In April 2024, we bought the price dip and added Amgen to our Hidden Yields dividend growth service. Two weeks ago, we highlighted the latest dip as a Best Buy opportunity!

Amgen’s Divvie Magnet to the (Perennial) Rescue!

This is the powerful dividend magnet. Over time, a steadily rising payout drags the share price higher.

So, why can’t the bots model this? They can for short periods, but they lose focus. The robots draw too many conclusions, seeing patterns when they aren’t there—like reading tea leaves. They become too sure of themselves and fire off one thousand trades in a cool week or two.

We don’t need all that tail chasing. Amgen’s rising dividend is a surer bet than perceived (real but not repeatable) AI patterns. It is the cash cow of the biotech sector. The company boasts 70% gross profit margins, powered by a research engine that flows to the cash faucet.

Today, Amgen trades at 5-times sales. Compare it to NVIDIA, which runs on similar margins, but costs 22-times sales. NVIDIA is priced for perfection, which may continue to come true. But I’d rather bank the dividend-raising cash machine that quietly compounds without the “I hope earnings will be over the moon” type of drama.

Amgen also boasts a stock buyback machine that retired 29% of its share count over the past decade. Fewer shares to pay dividends on means more cash per remaining share, which feeds the next dividend raise, which feeds the dividend magnet. A virtuous cycle for us!

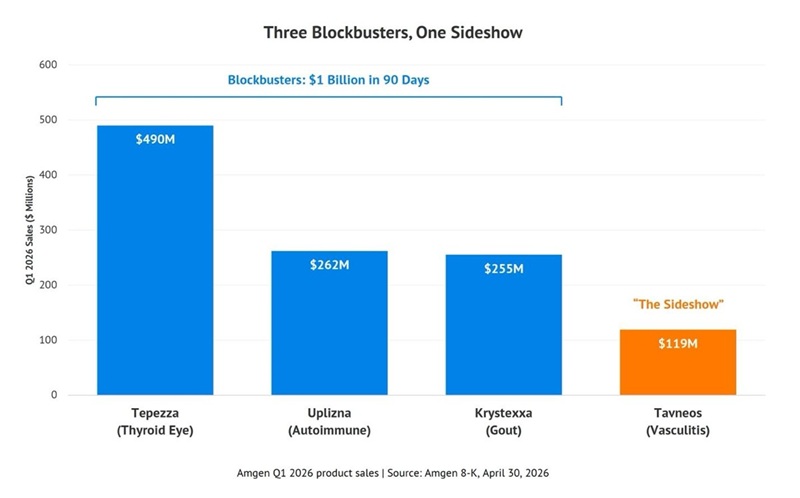

The growth engine underneath? Rare diseases. Amgen built its first fortune on pathbreaking red and white blood cell boosters for cancer patients, but its latest is a rare-disease segment. It didn’t have one just a few years ago. Then in October 2023, management dropped $27.8 billion on Horizon Therapeutics, the largest deal in company history. The prize: Tepezza, the leading treatment for thyroid eye disease, and a full rare-disease pipeline.

A disease may indeed be rare—have few patients—but put together breakthroughs and your combined revenues help people and… yes… your business.

Of the more than 10,000 rare diseases identified today, only 5% have approved medicines, and Amgen has the R&D and manufacturing muscle to keep filling that gap profitably. Its Horizon acquisition bet is paying off. Amgen’s rare disease segment did $5.2 billion in revenue last year, growing 25% year-over-year in the most recent quarter. Tepezza alone brought in $490 million in Q1 2026.

Wall Street is waking up, but slowly (as always). Freedom Broker just upgraded AMGN to Buy with a $375 price target. That happens to be the exact buy-up-to price I raised for our Hidden Yields subscribers recently.

Nice of one suit to confirm our homework! There will be more rubber stamps on the way, as other shops still lag. BofA puts Amgen at $307. Guggenheim, $340. Morgan Stanley, $326. The full Wall Street average price target now sits around $357—above today’s price, but still short of where this dividend grower will land.

Earlier this year Amgen topped $388 but it has pulled back since over concerns about Tavneos, one rare-disease drug. True, this drug is a small revenue line, with $119 million in Q1 sales. But the forest for that tree? Amgen’s three rare-disease blockbusters—Tepezza for thyroid eye disease, Uplizna for autoimmune disorders, and Krystexxa for chronic gout—raked in over $1 billion. That’s 8-times Tavneos in 90 days. Uh, which do you think matters more?

Tavneos is a sideshow while the Horizon-era main act keeps humming. This presents us with a second-chance window to buy! The dip I flagged for HY subscribers two weeks ago hasn’t closed—yet. However, it’s likely only a matter of time because the dividend magnet keeps tugging. Let’s take advantage while the bots are frantically throwing trade tantrums!

Amgen is just one of many dividend magnets I track — and far from the only setup like it. The same pattern shows up across the dividend-payer universe: payout marching higher, price wandering before racing to catch up, Wall Street late to the party as always.

© 2026 Passive Income Live

Theme by Anders Noren — Up ↑