I’m really impressed together with your writing abilities as smartly as with the structure for your blog. Is that this a paid subject or did you modify it yourself? Anyway keep up the nice high quality writing, it is rare to peer a great weblog like this one today..

£££££££££££

WordPress currently charge £7.20 per month, although this was discounted for the first 6 months.

The above portfolio is what a de-accumulation portfolio might look like, yours may be different. This information is being repeated as new readers join the blog to follow the Snowball, welcome all. When the next market crash arrives u should be ready.

Working Example

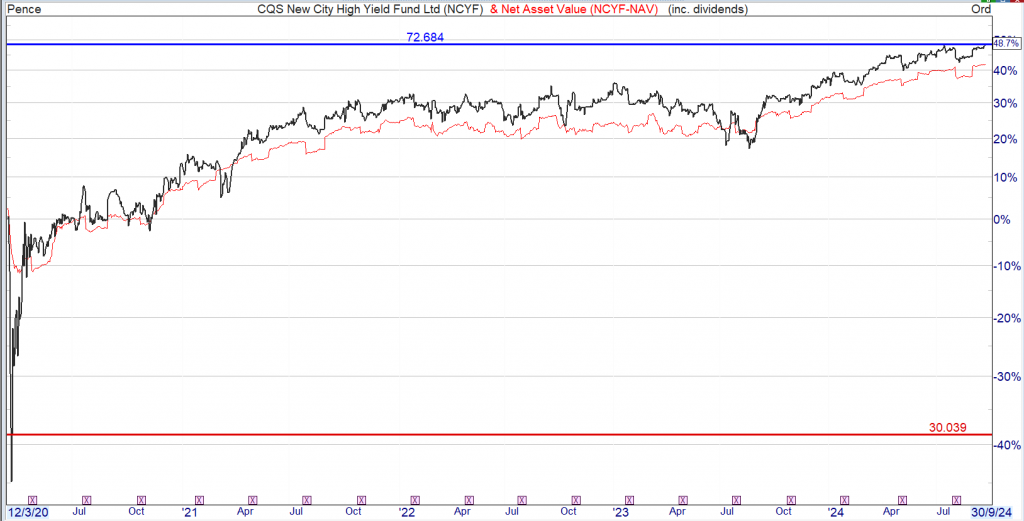

If u bought at 30p for the yield, as the price may have continued to fall

2020 dividend 4.46p a yield of 14.9%

This years expected dividend 4.5p a yield of around 15% on the buying price but as the price rises the yield falls so a running yield of 8.57%

If u include the dividends earned but not re-invested in the Trust u have more than doubled the amount u invested. Of course the one consideration u would have needed funds to re-invest and as most Trusts fell in unison, I’ll leave that with u to come up with a solution.

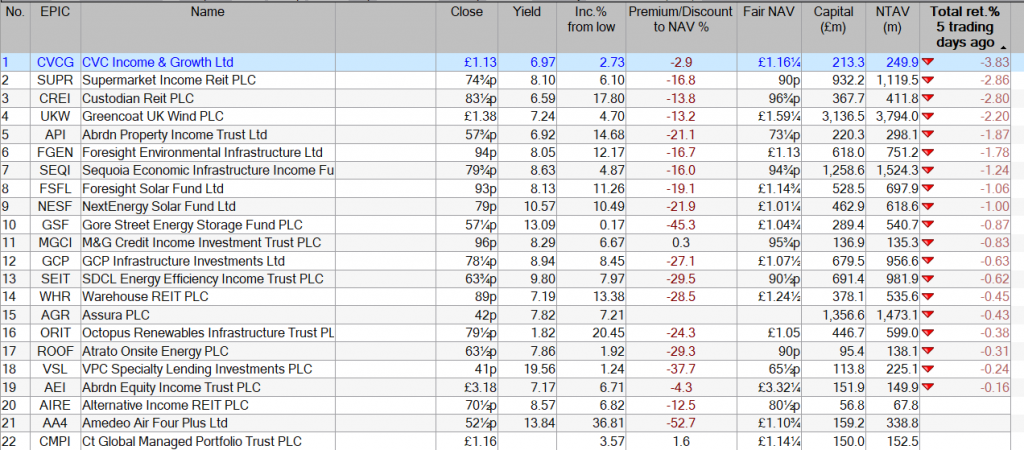

The current planned dividends for the GetRichSlow Snowball portfolio. As always best to DYOR as mistakes can creep into published information. If u are nearing your de-accumulation stage, ‘secure’ dividends are more important than owning Trusts trading at a discount to NAV.

Keystone Positive Change considers merger with open-ended equivalent; Gulf Investment Fund proposes a wind up; and PRS Reit makes up with its shareholders.

Frank Buhagiar

Keystone Positive Change Looking to Scale up

Keystone Positive Change (KPC) announced it’s considering implementing a transaction in the near term to address the size of the Company, the low liquidity in the Company’s shares and the discount at which they have been trading, while enabling Shareholders to retain exposure to a global impact strategy. Might sound like that’s a lot to achieve in one transaction, but among the options being considered by the Board is rolling the fund’s assets into the £1.8 billion Baillie Gifford Positive Change Fund, an FCA authorised open-ended investment company. One advantage here is that the two Baillie Gifford funds are “substantially” invested in the same portfolio of listed equities.

The Board is seeking shareholder feedback on the potential rollover. Activist investor and 17% shareholder Saba Capital presumably will be among those providing feedback, that is if they haven’t already.

JPMorgan: “a rollover into the open-ended version of the strategy makes sense in that it would eliminate the discount, and enable those who believe in the strategy to remain invested. But we would expect a 100% cash exit to be offered alongside a rollover option.”

Gulf Investment Fund Wind up on the Cards

Gulf Investment Fund’s (GIF) Board intends to put forward proposals to shareholders to wind up the company. As per the fund’s press release, this follows the launch of a tender offer for up to 100% of each shareholder’s holding in the company. Problem is, the tender appears to have been so popular that the fund received irrevocable commitments covering so many shares that if accepted would have resulted in “the minimum size condition in respect of the Tender Offer (being a post Tender Offer share capital of not less than 38,000,000 Shares) not being met.” Because of this, the tender will no longer proceed. Hence the wind-up proposal.

PRS Reit Makes up with Shareholders

PRS Reit (PRSR) has settled its differences with the shareholders who recently called for a general meeting to be held. The requisitioners wanted shareholders to be given the opportunity to vote on resolutions calling for two directors, including the current chairman, to be replaced with Robert Naylor and Christopher Mills, both of Hipgnosis Songs sale fame. A week, clearly a long time in the investment trust world for the build-to-rent REIT announced an agreement has since been reached that will see the requisitioners withdraw their Requisition Notice.

In return, Robert Naylor and Christopher Mills will be appointed to the Board as non-executive directors while current Chairman, Steve Smith, who was nearing the end of his term anyway, will step down and be replaced, on an interim basis, by Senior Independent Director, Geeta Nanda.

Winterflood: “This appears to be a positive outcome for PRSR shareholders, with most of the changes proposed by the requisitioning shareholders, which clearly had the support of a significant number of institutional investors, being implemented by the Board without the need for convening a GM, thereby saving some costs. Robert Naylor and Christopher Mills have notable experience in extracting shareholder value after being appointed to investment trust Boards, for example conducting the sale of Hipgnosis Songs Fund (SONG) to Blackstone earlier this year. We therefore expect them to have a significant impact on the upcoming strategy review.” Just goes to show, it’s good to talk.

The Results Round-Up – The Week’s Investment Trust Results

No shortage of results this week. Among those reporting, a private equity fund that would have made investors £2.2m had all ISA allowances and dividends been invested in the trust between 1999-2023; and another with a portfolio that reminds its own investment managers of Hans Christian Andersen’s Ugly Duckling story.

ORIT has had a busy half-year. The company acquired a large solar complex in Ireland, secured a PPA (power purchase agreement) for its Crossdykes onshore wind farm, and made a follow-on £5.9 million investment to develop its pipeline of offshore wind and sustainable fuels projects. As for the financials, NAV total return came in at +2% while the dividend target for the year was raised by 4% to 6.02p.

Liberum: “We maintain our BUY rating with a 115p TP and continue to be encouraged by the high level of earnings visibility, strong dividend cover, three-year track record of a CPI-linked uplift to the dividend, diversified portfolio, execution of the capital recycling programme and attractive discount to NAV.”

HydrogenOne Capital Growth (HGEN) on the Rise

HGEN’s share price stole the show over the half-year period, up +7.8% compared to NAV per share’s +0.6%. Progress was made at the portfolio company level too with an aggregate £76 million in revenues generated, that’s +44% year-on-year growth. What’s more, so far this year, investors have backed HGEN’s portfolio companies to the tune of €670m.

Winterflood: “NAV per share +0.6% to 103.6p (pre-announced), driven by valuation uplifts at multiple private investments and lower discount rates, with offsets from fees and FX.”

Greencoat Renewables’ (GRP) Proactive Management

GRP’s NAV per share for the half year came in at 112.1 cents, a little off H1 2023’s 113.2c. Despite this, operating cashflows funded €33 million in debt repayments as well as a €25 million share buyback. Meanwhile “proactive revenue management” has increased contracted revenues to 77% of the total for the 2024 – 2028 period, providing a high level of visibility.

Jefferies: “The results once again highlight GRP’s conservative valuation assumptions, coupled with significant capital allocation flexibility driven by the portfolio’s high level of contracted cash flow generation.”

HgCapital Trust (HGT) Tops the Charts

HGT’s +6.4% NAV total return for the half year was trumped by the +12.7% share price return. Over 10 years, share price total return now stands at +20.0% p.a. and for the third year in a row, the private equity fund tops the Association of Investment Companies’ (AIC) list of funds that would have made investors more than £1m had the full annual ISA allowance been invested in the same trust each year between 1999 and 2023. Together with reinvesting dividends into HGT shares, this would have generated a tax-free amount of over £2.2m as at 31 January 2024!

JPMorgan: “We see no reason to change our Overweight recommendation, with HGT the only pure play listed way to invest in leading private European profitable software and services companies”.

Pacific Horizon (PHI) Focused on the Horizon

PHI’s +4.8% NAV per share total return for the full year was a little behind the MSCI All Country Asia ex-Japan Index’s +6.8%. Tables turned over five years: NAV total return stands at +96.1% compared to the index’s +17.0%. Chairman Roger Yate’s thinks there’s more to come: “There remains a wealth of opportunities for the patient investor. Based on the encouraging macroeconomic trends and stock-specific opportunities, there is every reason to be optimistic about the long‑term prospects for the portfolio.”

JPMorgan: “Shareholders have suffered from a de-rating of the shares that had been trading on a premium between mid-2020 and early 2022 reflecting its strongest period of performance. The current 10.7% discount feels fairer, and is broadly in line with most peers.”

Nippon Active Value Fund’s (NAVF) Beats the Non-Benchmark

NAVF posted a +6.9% NAV increase for the half year. The MSCI Japan Small Cap Index (sterling terms) was largely flat, which means since the fund’s 2020 launch, NAV is up +89.2% compared to the index’s +16.7% return (sterling terms with dividends reinvested). Not that NAVF has a benchmark. As Chair Rosemary Morgan explains “Our strategy does not target any index. Our focus remains on medium and small capitalised companies, where we can build up significant stakes to enable productive engagement with their management.” So, “Even if investors’ focus shifts to opportunities away from Japan, we are confident that our activist approach will continue to perform well.”

Winterflood: “Managers believe that due to the majority of the portfolio being ‘domestic-facing, with little exposure to export or currency-led industries’, they are less impacted by a stronger Yen than portfolios composed of large international businesses.”

AVI Japan Opportunity’s (AJOT) Hidden Gems

AJOT’s “unique brand of constructive engagement and high-quality research” delivered a +7.7% NAV per share total return (sterling terms) for the half year, easily trumping the MSCI Japan Small Cap Index’s -0.2% sterling return. According to Chairman Norman Crighton, there should be more to come “The lack of research coverage of small-cap companies relative to large-caps continues to present us with abundant opportunities. Foreign investors have predominantly allocated their capital into larger companies with greater liquidity rather than taking time to uncover small-cap opportunities.”

Numis: “AJOT is our preferred pick and features on our recommended list”.

Petershill Partners’ (PHIL) Clean Sweep

PHIL reported a clean sweep of growth for the half year: $146m total income (H1 2023 $138m); $128m Adjusted EBIT (H1 2023 $120m); and $94m Adjusted Profit After Tax (H1 2023 $68m). PHIL’s Ali Raissi-Dehkordy and Robert Hamilton Kelly put the strong showing down to the alternative asset management firms in which the fund invests raising $14 billion of fee-eligible assets between them. Along with the growth in fee-paying AuM (assets under management), this has translated into higher gross management fees. Rounding off the solid numbers, the fund announced a special dividend.

JPMorgan: “We think the solid H1 print is reassuring, and the special dividend will be taken positively by investors today. We are Overweight.”

Foresight Solar Fund (FSFL) on Track to Hit Dividend Target

FSFL reported a 114.9p NAV per Ordinary Share at the half-year stage, a little down on the 118.4p reported six months earlier. The difference is largely down to lower-than-budgeted generation due to poor weather and a fall in power price forecasts. Despite this, the fund remains on course to hit its 8p per share dividend target for 2024 and 1.4x dividend cover.

Investec: “The shares currently offer a dividend yield of 8.5% and we estimate a prospective steady state return of c.10%. We maintain our Buy recommendation.”

Murray Income’s (MUT) Patience Delivers

MUT’s full-year NAV per share total return came in at +9.9%, a tad behind the FTSE All Share’s +13.0%. But, as the investment managers point out, “Our investment process encompasses a patient buy and hold approach” and it’s a process that has delivered over longer timeframes – over five years, annualised NAV per share has beaten the FTSE All-Share Index by +0.2%. As for what type of companies the fund buys and holds, these are “high-quality companies with robust competitive positions and strong balance sheets, which are led by experienced management teams capable of delivering premium earnings and dividend growth.”

Winterflood: “Performance benefited from stock selection in Consumer Discretionary and Telecommunications sectors and overweight exposure to Industrials and Technology sectors. This was offset by negative stock selection in Industrials, Financials, and Consumer Staples sectors.”

Ruffer’s (RICA) Ugly Duckling

RICA posted a +1% NAV total return for the full year in line with the aim to deliver positive NAV total returns. No one-off either. 2024 sees RICA chalk up 20 years, during which the wealth preserver has generated an annualised total NAV return of +6.9%. That’s a little behind the FTSE All-Share’s +7.4%. However, as Chairman Christopher Russell points out, RICA has achieved this “equity-like return with bond-like volatility and a positive return when equity markets have suffered a significant down-draft.”

Speaking of down-drafts, the investment managers “believe investors are complacent and we have arguably never seen an equity market as crowded, narrow, and myopic as the one we see today.” No surprise then that the portfolio has been positioned defensively. So much so, it brings to mind “Hans Christian Andersen’s Ugly Duckling story. It is a portfolio filled with unloved assets – shunned, even derided by other investors. But assets whose worth will become starkly apparent in time – as they turn to swans.”

Winterflood: “Equity upside drove returns (+3.0%), supported by gold and precious metals exposure (+2.0%), commodities (+1.8%) and cash and short-dated bonds (+1.6%), while protection strategies (-3.2%), Yen exposure (-2.2%) and long-dated inflation-linked bonds (-0.8%) detracted.”

City of London (CTY) Delivers Across the Board

CTY’s latest year was neatly summed up by the opening paragraph of Chairman Sir Laurie Magnus’ full-year statement “City of London produced a net asset value (NAV) total return of 15.6% outperforming the FTSE All-Share Index total return of 13.0%. The City of London’s NAV total return has exceeded the FTSE All-Share Index over 1, 3, 5, and 10 years. The dividend was increased for the 58th consecutive year and fully covered by earnings per share.” Not much more to say.

Numis: “We continue to view City of London IT as a solid option for investors seeking income from UK equities

Disclaimer Disclosure – Kepler Non-Independent Marketing Communication

This is a non-independent marketing communication commissioned by M&G Credit Income. The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

Overview MGCI has delivered strong returns over the past year… Overview M&G Credit Income (MGCI) is a highly flexible fixed income fund, able to invest across public and private debt markets in pursuit of a high yield. Unlike many funds that offer such a high yield, it does so without taking on a lot of credit risk or gearing up. Nevertheless, it currently offers a 9.1% dividend yield from a portfolio of investment-grade quality.

The portfolio has delivered strong returns over the past year, c. 11% on a NAV total return basis (see Performance). This has been mainly due to the high income generated, while there have also been capital gains on some investments as spreads in public debt markets have tightened. Demand has generally remained high for the shares, with the trust frequently trading on a small premium in recent months and the board issuing into the market.

Manager Adam English reports that he has been seeing an increasingly attractive pipeline of private debt opportunities, and he has been reinvesting profits into them. These should allow him to boost the income being generated by the portfolio while spreads are less attractive in public markets – the key advantage of the flexible structure.

Private debt is mostly floating rate, and MGCI tends to run with 70–80% in floating-rate debt. This means that income rises or falls as UK interest rates do, with a lag. The Dividend is therefore likely to fall slightly over the coming months, as the target is 400bps over SONIA (an interbank rate that closely tracks the base rate). However, Adam expects the yield to remain high, with rates set to fall slowly and risks to the upside still around.

Analyst’s View We think MGCI’s high yield and low NAV volatility should be appealing to many income-seeking investors. The spread of 400bps over what is effectively a cash rate should remain, even if we see the absolute yield fall gradually as interest rates do. This should be highly attractive versus the yields available on other income-paying investments such as high yield bonds, which carry greater credit risk and duration, and many alternative assets in the investment trust space, which use high levels of gearing to generate their yield.

MGCI seems to be well suited to the current economic environment, and we think absolute returns should remain high for some time to come. While economic growth remains weak in the UK and its key trading partners, serious recession looks unlikely. Inflation has proven relatively resilient, thanks in part to economies performing better than feared. As a result, it looks likely that rate cuts in the UK and US will be gradual and well-ordered, which would keep the income paid out by the trust high. Meanwhile companies’ ability to service their debts should remain resilient, which would create a strong outlook for credit risk. We note that Adam reports a steady flow of attractive deals in the private debt space, which speaks of a healthy market and healthy corporate sector and should mean the manager has plenty of opportunities to maintain the yield and quality of the portfolio.

Bull High yield linked to interest rates, with average investment-grade quality credit Offers access to private debt markets, providing attractive risk/return characteristics and diversification NAV should prove resilient due to many defensive characteristics

Bear Complexity makes it harder for investors to understand exposures Limited capital gain potential, including from duration Rate cuts will reduce portfolio income, absent offsetting investment decisions.

££££££££££££

Loans are at the riskier end of investing so if u are investing u need a higher yield for the risk. Here the Trust trades around its NAV so maybe better for a De-Accumulation stage or to reduce the risk if paired with a higher yielder in your Accumulation stage.

If your savings plan is for your retirement (accumulation stage) u will have the following three choices when that day arrives.

Option One.

Buy an annuity.

The biggest risk is the unknown amount. It could be

Canada Life figures show the 65-year-old with a £100,000 pension pot could buy an annuity linked to the retail price index (RPI) that would generate a starting annual income of £3,896. That’s up from £2,195 in the New Year following a 77% spike in rates this year. Oct 22

You have to surrender all your hard earned, so not a good outcome, unless markets have crashed and interest rates are near to double figures. Of course the value of your portfolio will most probably have crashed so the benefit may not be that great.

Option two.

Use the 4% rule.

Invest for capital growth hoping for growth of around 7%, depending on your skill level. If u buy a tracker there will be several years of flatlining where your capital will most probably fall and when u want to start spending your hard earned keep everything crossed the market hasn’t crashed before u need the cash.

Option Three.

Buy Investment Trusts that pay a dividend and use those dividends to buy more Investment Trusts that pay a dividend, the accumulation stage. When u enter your de-accumulation stage switch into the safest yields available.

Accumulation stage. Trusts that pay a high dividend and better if trading at a discount as u may be able to book profits to re-invest to earn more dividends.

De-Accumulation stage. Income is most important and making a profit is less of a consideration.

Remember with Compound Growth, u should make more income in the final few years than in most of the early years, so the sooner u start the better chance of a better retirement.

But as always best to DYOR as it’s your hard earned.