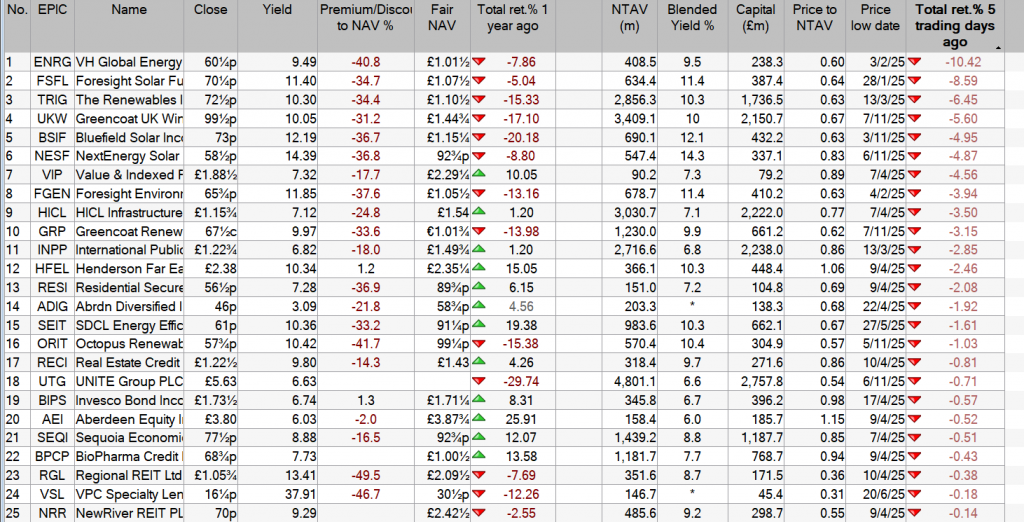

Investment Trust Dividends

I’ve tried to deal AIRE but it’s restricted trading, although you can buy 3,000 shares. The problem being you could build a position but be locked in when you want to sell, so not a suitable share for the Snowball. I will look for something to buy over the weekend.

I’ve sold the shares in PHP for a profit of £333.00, mainly because PHP was bought xd and dividends are the only consideration for the Snowball.

The replacement share is going to be Alternative Income AIRE, most probably.

Christopher Ruane explains how a Stocks and Shares ISA can be used as part of a strategy to try and earn a four-figure monthly passive income.

Posted by Christopher Ruane

Published 6 November

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Ever thought of stuffing a Stocks and Shares ISA with dividend shares as a way to earn passive income?

Lots of people do.

It also means that passive income can hopefully be earned from proven blue-chip companies. That sounds genuinely passive to me, compared to some other approaches people use.

How much might such a plan earn?

It is a bit like asking how long is a piece of string. The amount of passive income a Stocks and Shares ISA can generate in the form of dividends depends on three factors: how much is invested, for how long, and at what dividend yield.

£1k a month equates to £12k per year. At a 5% yield, that would require an investment of £240k. At a 7% yield, it would require a bit less than £172k.

That may make it sound as if higher yields are the thing to go for. But no dividend is ever guaranteed to last, so when looking for shares to buy, it is always important to look at the likely source of any future dividends, not just the current yield.

Both 5% and 7% are above the current FTSE 100 yield. But I think 7% is a realistic target in today’s market.

Not everyone has a spare £172k in their Stocks and Shares ISA that would let them get going straight away. That is fine – it is also possible to start from zero, by making regular contributions.

Putting £20k a year into the ISA and compounding at 7% annually, it would take just 7 years to hit the target size of close to £172k.

It could also be done with smaller contributions, though it would then take longer.

One share I think investors should consider is Legal & General (LSE: LGEN). The FTSE 100 financial services firm has an 8.9% dividend yield.

It also aims to grow its dividend per share each year. The sale of a large US business ought to generate cash to help do that, though I see a risk that it could also leave a gap in the company’s profit generation ability compared to previously.

But with its strong brand, long history, large customer base, and proven cash generation ability, I think there is a lot to like about Legal & General.

Over the long term, I am hopeful it can use those strengths to keep generating more cash than it needs to run its business – and hopefully distributing lots of it as dividends.

05 November 2025

This is a non-independent marketing communication commissioned by Invesco. The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

KEPLER

BIPS uses the investment trust structure to maximise the potential in high-yield bonds.

Overview

Invesco Bond Income Plus (BIPS) is designed to offer an attractively high yield with a diversified, risk-conscious approach. The investment trust structure allows the manager, Rhys Davies, to invest in a diversified set of high-yield bond markets, including into some smaller and less liquid areas, and to boost the yield by taking on gearing rather than extra credit risk. Meanwhile, the ability for the board to build up revenue reserves makes it easier for it to provide a smooth income output (see Dividend).

Rhys can invest in high yield globally, but focusses on the UK and Europe, supplemented by the best ideas from Invesco’s large US-based credit teams. He runs a portfolio very diversified by issuer, and uses his and his team’s expertise in subordinated bank debt to provide a boost to the yield without taking excessive credit risk (see Portfolio). Currently, this allocation to subordinated financials is balanced by a large position in lower-yielding, investment-grade debt. Overall, Rhys is positioned cautiously, waiting for opportunities to take advantage when high valuations recede — as he did to good effect during the tariff tantrum of April 2025. Nonetheless, the portfolio yield is c. 7.5%, reflecting Rhys’ ability to generate income without leaning on credit risk. Board and manager agree a dividend target at the start of each year, with 2025’s 12.25p per share equivalent to an ongoing share price yield of 7.0%.

Strong demand for the shares means the trust has tended to trade on a premium for the past three years and the board has issued substantial amounts of shares to meet demand, which has contributed to BIPS having the lowest charges in its sector by some way. Nonetheless, the shares still trade on a small premium of 1.5% at the time of writing.

Analyst’s View

BIPS has strong credentials to be the first option considered for any high-yield bond allocation. It uses the features of the investment trust structure well to its advantage, providing an edge over open-ended funds or ETFs. Rhys doesn’t have to keep cash on hand for outflows, and so can remain fully invested. In fact, he tends to run with a geared position, boosting the yield and the capital growth potential. He also invests in more specialist and less liquid areas like subordinated financial debt and some small issue bond deals, providing off-benchmark allocations that passive options can’t. The annual dividend target provides some visibility on the yield, while revenue reserves provide some protection in the event that market yields fall. Invesco’s large credit teams in Europe and the USA allow Rhys to manage a broad and diversified portfolio with prudently managed issuer and geographical risks.

Rhys’s cautious outlook doesn’t prevent the trust from offering a high yield while also having some built-in beta to any price appreciation that would come from falling interest rates, with a duration of 3.8 as of the end of September. This interest rate sensitivity is spread across the three key geographies, and so if UK rates remain high while European and US rates continue to fall, the portfolio will still benefit. We think that, given how narrow credit spreads are right now, BIPS’s approach, which allows a high yield to be earned without leaning on credit risk, is highly attractive.

Disclosure – Non-Independent Marketing Communication

This is a non-independent marketing communication commissioned by City of London Investment Trust (CTY). The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

KEPLER

A strong year of stock picking puts CTY well ahead of the benchmark.

Overview

City of London Investment Trust (CTY) aims to deliver income and capital growth. Job Curtis has an impressive tenure of 34 years managing the trust, giving him a depth of experience rarely matched. In particular, the last financial year illustrated the benefits of his active, stock-picking approach. That said, this is a cautious investment strategy that is arguably well suited to extending CTY’s unrivalled 59 year run of progressive dividend increases.

Job seeks to spread risks – both in terms of capital and income generation – across the portfolio. This has protected CTY against many sector-specific issues that have arisen over the years, but also in our view complements Job’s valuation-based investment framework, which favours quality companies, and sometimes has a contrarian tilt towards identifying new ideas. Job aims to balance any lower yielders in the portfolio by also investing in steady, highly resilient dividend payers with strong balance sheets. As we highlight in the Portfolio section, this means that CTY is exposed to a range of different types of companies, with varying growth and income characteristics.

Behind the headline-grabbing Dividend Hero moniker, CTY continues to deliver on a NAV total return basis too. CTY has delivered outperformance of the benchmark over one, three, five and ten years.

CTY’s dividend represents a yield of 4.25%. Whilst the dividend increase last year of 3.4% was a shade behind that of UK CPI at 3.6%, the board has stated that it understands the importance of growing the dividend in real terms through the economic cycle and long term. CTY has delivered real dividend growth over ten and twenty years, as we discuss in the Dividend section.

Analyst’s View

CTY has established itself as the leading trust in the UK Equity Income sector, a result not only of its long history of dividend increases over the past 59 years, but also because it has delivered good total returns to shareholders too. As a result, it has won investors’ confidence over time, issuing shares and growing organically so that it now dominates the UK Equity Income sector in terms of size, meaning good liquidity for investors and low Charges.

CTY’s 2025 dividend equates to a dividend yield of 4.25%. Not only is this attractive in absolute terms, so too is the fact that shareholders can derive an element of reassurance that comes with knowing CTY has a 59-year track record of delivering consecutive annual dividend increases. However, this is no UK domestic play – the majority of CTY’s portfolio revenues are derived overseas. Job sees the UK equities he owns as ‘global growth at a discount’. Job expects takeovers of UK companies to continue, highlighting the value available in the UK market.

CTY also provides reassurance in another way – the share price has tended to move in a relatively narrow band with regard to the NAV. As we discuss in the Discount section, a subtle change in wording means the board has underlined its commitment to try to protect shareholders from the discount widening out. As well as its other attractions, the tight discount has been fundamental to allowing CTY to grow organically in the past through share issuance. With this move, shareholders can continue to have confidence in continued good liquidity, and that the share price should follow the NAV. In our view, CTY appears well placed to continue its leadership within the UK Equity Income sector.

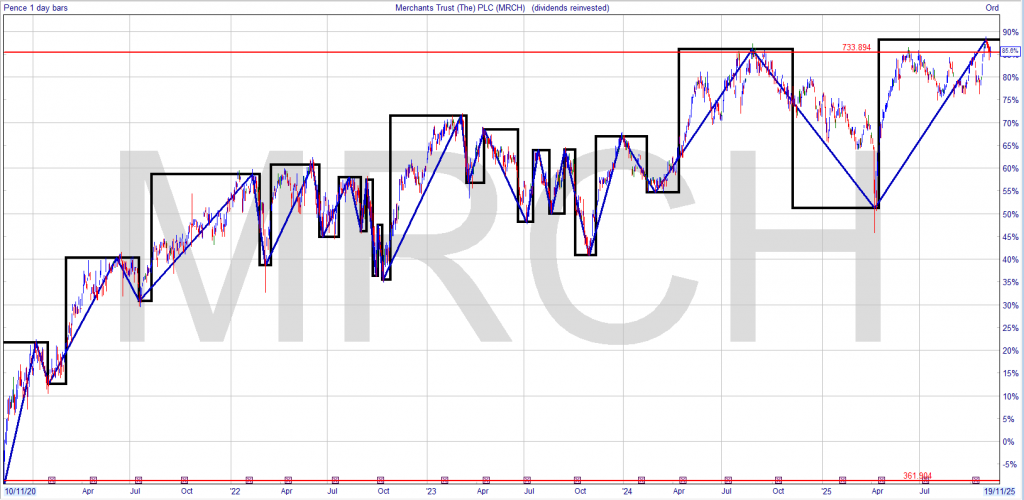

A Trust to research for ‘pair trading’.

7 Nov ’20 – 08:14 – 5 of 580 Edit | 0 0 |

If u bought 10k of MRCH yielding 8%, it’s easier to switch

to a cash equivalent so £800 pa.

If u assume the dividend is unchanged over 10 years

but the share price doubles, u will still earn £800 pa

but it will only now yield 4%

(still 8% on buying price)

If u sold your MRCH shares say roughly 20k plus dividends earned

of 8k and re-invested in a share say a Renewable yielding 6%

your dividend would rise to £1,680 pa

If the share price doesn’t rise keep re-investing in MRCH for as long

as they don’t change their dividend policy, your dividend take

after 10 years would be £1,440, more if the share price fell as

the yield would rise.

Above is a post that I made 5 years ago, note the yield on MRCH today 5.1% and the yield on the renewables sector.

(“GCP Infra” or the “Company”)

Company update and Net Asset Value

6 November 2025

Net Asset Value

GCP Infra announces that at close of business on 30 September 2025, the unaudited net asset value (“NAV”) per ordinary share of the Company was 101.40 pence (30 June 2025: 102.14 pence), a decrease of 0.74 pence per ordinary share. The NAV takes into account cash, other assets, accrued liabilities and expenses and leverage of the Company attributable to the ordinary share class.

Forvis Mazars, the Company’s independent valuation agent, applied a sector-wide increase of 25 bps to the discount rates applicable to the Company’s renewables portfolio to reflect their view of market conditions for this asset class, including as a result of the expectation of delays to interest rate reductions and persistently high yields for benchmark long duration UK fixed income exposures. This has resulted in a negative movement of 0.38 pence per ordinary share.

Updates to forecast electricity prices, driven by higher futures forecast in the short-term, led to an increase of 0.08 pence per ordinary share, net of hedging. Actual generation across the renewable energy portfolio, net of the valuation effect of unwinding discount rates and project specific updates across the whole portfolio led to a net decrease of 0.31 pence per ordinary share.

During the period the Company has, following independent advice, updated its assessment of the level of curtailment and constraint for two onshore wind projects in Northern Ireland that participate in the Irish Single Electricity Market. This has resulted in a negative movement of 0.41 pence per ordinary share.

A summary of the constituent movements in the quarterly NAV per ordinary share is shown below.

| NAV analysis (pence per share) | NAV | Change |

| 30 June 2025 | 102.14 | |

| Q3 2025 power price forecasts (net of hedging) | 0.08 | |

| Actual generation net of discount rate unwind and project specific updates | (0.31) | |

| Northern Irish wind asset curtailment forecast | (0.41) | |

| Sector-wide discount rate changes | (0.38) | |

| Share buyback accretion to NAV | 0.28 | |

| 30 September 2025 | 101.40 |

Capital allocation

The Board reconfirms its commitment to the Company’s capital allocation policy set out in the 2024 Annual Report and Accounts, continuing to prioritise repayment of leverage, as well as reducing equity-like exposures and exposures in certain sectors, whilst also facilitating the return of £50 million of capital to shareholders. At 30 September 2025, the Company had £20 million (30 June 2025: £43 million) outstanding under its revolving credit arrangements, representing a net debt position of c. £8 million (30 June 2025: c. £36 million) which compares to the Company’s unaudited NAV of £849 million (30 June 2025: £864 million).

Further supporting the capital allocation policy, the Company bought back 8,937,270 ordinary shares in the quarter, contributing a 0.28 pence per ordinary share increase to NAV. In aggregate, the Company has purchased c. £23 million of shares since announcing the capital allocation policy.

The Company continues to progress transactions to dispose of assets in those sectors targeted in the capital allocation policy. If completed, such transactions would enable the Company to complete the capital allocation policy objectives of returning at least £50 million to shareholders and reducing the Company’s outstanding debt to nil. Further announcements will be made in due course, including as part of the Company’s annual report and financial statements, which are due to be published in December 2025.

Renewable Subsidy Indexation

The Company notes the recent publication by The Department for Energy Security and Net Zero of a consultation regarding potential changes to the indexation methodology applied to feed-in-tariffs and the buy-out price under the renewables obligation (the “Proposals”). The Company intends to respond to the consultation setting out objections to the Proposals: long-term investors rely on a stable policy environment and the Proposals, if implemented, would either deter future investment or increase the risk premium of future investment in projects that rely on long-term policy support. If implemented, under options one and two of the Proposals, the impact on the Company’s NAV would be a decrease of 0.46 and 1.19 pence per ordinary share respectively.

Portfolio

The Company’s portfolio continues to perform materially in line with the Company’s expectations. The Company’s mature, diverse and operational portfolio provides defensive access to stable and predictable income. It is the view of the Investment Adviser that the long-term and structural demand for infrastructure, and particularly infrastructure debt, offers investors an attractive exposure to an asset class whose performance is not correlated to wider markets and benefits from long-term and partially inflation protected income.

Octopus Renewables Infrastructure Trust plc

(“ORIT” or the “Company”)

Statement re Government consultation on ROC and FiT indexation methodology

Potential impact on Company estimated to be limited

Octopus Renewables Infrastructure Trust PLC, the diversified renewables infrastructure company, notes the consultation published by the UK Department for Energy Security and Net Zero on 31 October 2025 proposing potential changes to the inflation indexation methodology used in the Renewable Obligation (“ROC”) and Feed-in Tariff (“FiT”) schemes from next year.

The consultation outlines two potential approaches. Broadly:

1. An immediate (at the next annual adjustment in March 2026) switch from Retail Price Index (“RPI”) to Consumer Price Index (“CPI”) for ROC buyout price indexation and FiT tariff uplifts, bringing the date forward from 2030

2. A temporary freeze in ROC buyout price indexation at the 2025/2026 level, with effect from April 2026, followed by a gradual realignment with CPI

The Investment Manager has conducted analysis on the potential impact on the ORIT portfolio should either scenario be implemented. Given ORIT’s diversified portfolio and limited exposure to ROC-linked revenue (less than 30% of forecast revenues in each of the next five years), the estimated indicative (and limited) impact on net asset value (“NAV”) per share is outlined in the table below. ORIT does not have any UK FiT revenues.

| Scenario | Estimated impact on ORIT’s NAV per Share |

| 1 – Immediate (from March 2026) switch from RPI to CPI for ROC buyout price indexation and FiT tariff uplifts | c.-1.1p |

| 2 – Temporary freeze in indexation at the 2025/2026 level, followed by a gradual realignment with CPI | c.-3.9p |

The Investment Manager will continue to monitor the process closely and will provide a further update once the consultation is concluded.

With the final dividend for the year now declared the fcast is no longer a fcast.

2025 Income earned will be £11,635.00

There may be a small contribution for TMPL but not going to make much difference to the total.

Current income to be received £1,735 which will be re-invested to earn more income starting in 2026.

With a dividend re-investment plan you fail by the month and not the year it’s your duty to monitor your plan.

© 2026 Passive Income Live

Theme by Anders Noren — Up ↑