Octopus Renewables – Final Results to 31 December 2025

24 March 2026

LEI: 213800B81BFJKWM2JV13

Octopus Renewables Infrastructure Trust plc

(“ORIT” or the “Company”)

Full Year Results

Disciplined capital allocation and active portfolio management in a challenging operating environment

Octopus Renewables Infrastructure Trust plc, the diversified renewables infrastructure company, announces its audited results for the year ended 31 December 2025 (“FY 2025”).

As at 31 December 2025 (FY 2025)(audited)

As at 31 December 2024 (FY 2024)(audited)

NAV per Ordinary Share (p)

93.8

102.6

Ordinary Share price (p)

61.1

68.0

Dividends declared per Ordinary Share (p)

6.17

6.02

Dividend cover

1.14x

1.24x

Net asset value (“NAV”) (£m)

494.8

570.4

Gross asset value (“GAV”) (£m)1

896.9

1,028.8

NAV total return in the year

-2.8%

+2.5%

Total shareholder return

-1.5%

-18.3%

Generation (including compensation from curtailment) (GWh)

1,304

1,240

Revenue (operational portfolio) (£m)

138.8

131.7

EBITDA (operational portfolio) (£m)

88.3

85.5

FY 2025 Financial Highlights

· Declared dividends of 6.17 pence per share (“pps”), meeting the FY 2025 target (FY 2024: 6.02pps)

o Increased for the fourth consecutive year

o Represents a dividend yield of 10.1% against the 31 December 2025 closing share price

· Dividends fully covered by cash flows generated from the operational portfolio

· In-line with progressive policy, increased dividend target of 6.23pps announced for FY 2026

· Approximately 88% of revenues fixed over the two-year period to December 2027

· Provides strong protection against near-term market volatility and supporting predictable cash generation

· NAV of £494.8 million (FY 2024: £570.4 million), reduction reflecting sector-wide valuation pressures, largely driven by lower power price and green certificate assumptions

· Cost of debt reduced to 3.3% at year-end (FY 2024: 4.0%) following several proactive measures taken

FY 2025 Operational Highlights

Overall operational performance improved year on year across all three key metrics

· Generation and revenue each grew by 5%, and EBITDA by 3%

· Reflects greater control over operational performance across the portfolio during FY 2025

· Value-enhancement programme launched across the portfolio to identify and deliver long-term value accretive opportunities

Ongoing active portfolio management

· In February 2025, the Company announced it committed an additional €3.4 million (£2.8 million equivalent) to Nordic Generation (“Norgen”), a specialist developer focused on the Finnish wind and solar market

· In June 2025, the conditional acquisition of ORIT’s sixth Irish solar site was announced

· In October 2025, the sales of interest in HYRO Energy Limited and stake in Simply Blue offshore wind platform were announced

· In December 2025, the Company announced the disposal of a 49% stake of its full ownership in the 67 MW Breach solar farm in Cambridgeshire, and the disposal of 51% (ORIT’s entire holding) in the 46 MW Crossdykes onshore wind farm in Scotland

Proactive debt management

· Revolving credit facility (“RCF”) maturity extended to June 2028 and size reduced from £270.8 million to £150 million

· Signed a new £100 million five-year term-loan facility and repaid £98.5 million on the RCF

Capital allocation strategy executed and ‘ORIT 2030’ announced

· ‘ORIT 2030’ a strategic roadmap for growth was announced in September 2025 with four objectives:

o Grow: Invest for NAV growth

o Scale: Build a larger, more investable company

o Return: Deliver attractive risk-adjusted total returns

o Impact: Scale with purpose and resilience

· Over FY 2025, ORIT completed asset sales totalling £74.3 million (including deferred components), against a stated target of £80 million. These disposals were agreed at or above carrying value.

· ORIT has now recycled a total of approximately £235 million since its capital recycling programme began in June 2023, the highest proportionate amount of the peer group compared to the Company’s size

· As at 31 December 2025, the Company had deployed approximately £26 million of its £30 million share buyback programme

· The remaining £4 million remains available to be used, subject to market conditions and capital allocation priorities.

Phil Austin, Chair of Octopus Renewables Infrastructure Trust plc, commented: “The year under review was characterised by disciplined capital allocation and active portfolio management in a challenging operating environment. Against a backdrop of power price volatility, higher-for-longer interest rates and evolving regulatory considerations, the Board remained focused on positioning ORIT for long-term resilience and growth, while continuing to deliver sustainable income to shareholders. Despite these actions the Company delivered a negative total return over the year, driven by sustained pressure on valuations.

“Whilst the prevailing discount remained a frustration the Company continues to focus its efforts on the actions that present the most effective means of supporting long-term shareholder value.

“FY 2025 marked a period of considered action across strategy, governance and cost management, all taken with shareholders’ interests firmly in mind and within the context of our ORIT 2030 strategy launched in September to guide the Company’s future direction.

“The ORIT 2030 strategic framework provides a clear structure for capital allocation and portfolio development over the medium term. The actions taken during FY 2025, particularly in relation to capital recycling, operational optimisation and capital structure discipline, are consistent with the early execution of this strategy.”

Annual Report and Accounts

To view the Company’s Annual Report and Accounts please visit ORIT’s website here:

There will be a virtual presentation for sell-side analysts today at 11am. Please contact Burson Buchanan for details on octopus@buchanan.uk.com.

The Company’s management team will also provide a live presentation via the Investor Meet Company platform, today at 1.30pm. The presentation is open to all existing and potential shareholders. Questions can be submitted at any time during the live presentation and a recording will be made available on demand after the presentation has concluded. Investors can sign up to Investor Meet Company for free here:

1.A measure of total asset value including debt held in unconsolidated subsidiaries, but excluding any outstanding equity or debt commitments.

2.The dividend target stated in this announcement is a target only and not a profit forecast. There can be no assurance that this target will be met, or that the Company will make any distributions at all and it should not be taken as an indication of the Company’s expected future results. The Company’s actual returns will depend upon a number of factors, including but not limited to the Company’s net income and level of ongoing charges. Accordingly, potential investors should not place any reliance on this target and should decide for themselves whether or not the target dividend is reasonable or achievable. Investors should note that references in this announcement to ‘dividends’ and ‘distributions’ are intended to cover both dividend income and income which is designated as an interest distribution for UK tax purposes and therefore subject to the interest streaming regime applicable to investment trusts.

About Octopus Renewables Infrastructure Trust

Octopus Renewables Infrastructure Trust (“ORIT”) is a London-listed closed-ended investment company incorporated in England and Wales focused on providing investors with an attractive and sustainable level of income returns, with an element of capital growth, by investing in a diversified portfolio of renewable energy assets in Europe and Australia. As an impact fund, ORIT is helping accelerate the transition to net zero by investing in green energy, whilst also contributing to a broader set of UN Sustainable Development Goals through its impact initiatives. ORIT’s investment manager is Octopus Energy Generation. Further details can be found at: www.octopusrenewablesinfrastructure.com.

About Octopus Energy Generation

Octopus Energy Generation is driving the renewable energy agenda by building green power for the future. Its specialist renewable energy fund management team invests in renewable energy assets and broader projects helping the energy transition, across operational, construction and development stages. The team was set up in 2010 based on the belief that investors can play a vital role in accelerating the shift to a future powered by renewable energy. It has a 14-year track record with approximately £7.0 billion of assets under management (AUM) (as at 31 December 2025) across 21 countries and with a total c.4.9 GW capacity under management. Octopus Energy Generation is the trading name of Octopus Renewables Limited. Further details can be found at: www.octopusenergygeneration.com.

Page number references in this announcement refer to pages in the Company’s simultaneously published Annual Report and Accounts.

Chair’s Statement

Introduction and overview

The year under review was characterised by disciplined capital allocation and active portfolio management in a challenging market environment. Against a backdrop of power price volatility, higher-for-longer interest rates, evolving regulatory considerations and ongoing geopolitical uncertainty, the Board remained focused on positioning ORIT for long‑term resilience and growth, while continuing to deliver sustainable income to shareholders. Despite these actions the Company delivered a negative total return over the year, driven by sustained pressure on valuations – primarily lower power price and green certificate assumptions, increased discount rates and the impact of the Renewables Obligation Certificate (“ROC”) indexation moving from the Retail Prices Index (“RPI”) to the Consumer Prices Index (“CPI”). In response to the proposed changes to ROC indexation, the Board made a formal submission to the consultation, emphasising that stable and predictable policy frameworks are critical to attracting long-term capital into renewables infrastructure, as well as maintaining investor confidence in the asset class.

As at 31 December 2025, the Company’s Net Asset Value (“NAV”) stood at £495 million, or 93.8 pence per Ordinary Share, compared with a market capitalisation of £322 million – a discount of approximately 35%. While parts of the global infrastructure market have shown signs of recovery, UK listed renewables continue to trade at elevated discounts, averaging approximately 39% across the peer group at 31 December 20251. ORIT’s discount reflects this broader sector de-rating, driven by higher interest rates, downward valuation adjustments and the uncertainty posed by the UK policy changes proposed by the UK Government late last year and confirmed in January. The Board is frustrated with the prevailing discount and continues to focus on the actions that present the most effective means of supporting long-term shareholder value.

Throughout the year, the Board worked closely with the Investment Manager, providing challenge and oversight while maintaining a clear focus on near-term priorities and long-term positioning for the Company. FY 2025 marked a period of considered action across strategy, governance and cost management, all taken with shareholders’ interests firmly in mind and within the context of the ORIT 2030 strategy which was formally launched in September to guide ORIT’s future direction. Details of these actions follow later in my statement.

Capital allocation, portfolio optimisation and gearing

During the financial year, there was a distinct focus on decisive capital allocation, with clear objectives set in March 2025. Over the 12-month period ORIT completed asset sales totalling £74.3 million (including deferred components), just shy of its target of £80 million. These disposals were agreed (including deferred components) at or above the assets’ net asset value and demonstrate the Investment Manager’s ability to successfully execute transactions in challenging market conditions.

Since the Company began recycling capital in 2023, it has sold seven assets for approximately £235 million at a weighted average uplift of 9%, representing one of the most significant programmes in the UK listed renewables sector relative to its NAV. Capital recycling remains a core component of ORIT’s strategy. By selectively realising assets to support goals to deleverage, as well as investing capital into opportunities with stronger growth potential, the Company can enhance portfolio resilience, improve capital efficiency and drive long-term value creation.

During the year, ORIT repurchased c.28 million Ordinary Shares for a total consideration of £19.2 million, increasing NAV per Ordinary Share by 1.4 pence. As at 31 December 2025, the Company had deployed approximately £26 million of its £30 million share buyback programme. The Board continues to assess buybacks alongside other strategic priorities, ensuring that capital is allocated in a way that supports long-term shareholder value while maintaining appropriate liquidity and a prudent capital structure.

Alongside asset sales, ORIT proactively addressed debt management during the period, with several measures significantly reducing the cost of debt to 3.3% at year-end (2024: 4.0%). While absolute debt reduced over the period, the downward pressure on valuations meant that the leverage ratio remained broadly flat year on year at 45% of GAV.

The Board and Investment Manager remain committed to gearing target of 40% over the medium term. However, shareholders should expect gearing to fluctuate around this level as we balance disciplined debt reduction with selective reinvestment alongside other actions that help us deliver our ORIT 2030 strategy, as detailed later in my statement.

1 Peel Hunt Investment Companies Data Sheet, 2 January 2026

Financial performance and dividends

Revenue quality remains a key strength of ORIT’s portfolio. Approximately 88% of revenues over the two-year period to December 2027 are fixed through power purchase agreements and government support schemes, providing strong protection against near-term market volatility and supporting predictable cash generation. This high proportion of contracted income continues to be market leading1 amongst peers across the listed renewables investment company sector.

While the year-end negative NAV return was impacted by multiple valuation headwinds, the underlying portfolio continues to deliver robust cash generation. The Board remains committed to its progressive dividend policy, with a core focus on ensuring that dividends are fully covered by operational cash flow on an annual basis.

The Company declared total dividends of 6.17 pence per share, meeting its FY 2025 target in full and representing an increase on the prior year. Dividends were fully covered by cash flows generated from the operational portfolio, with dividend cover of approximately 1.14x. An increased dividend target of 6.23 pence per share has been announced for the current financial year (“FY 2026”), reflecting confidence in the underlying cash-generating capability of the portfolio.

Operational performance and asset management

Total generation was 1,304 GWh, materially improved on the prior year, but slightly below budget as favourable solar conditions were offset by below-average wind speeds. Actions taken during the year included enhancements to asset availability, targeted remediation and maintenance programmes, blade optimisation initiatives and the progression of battery co-location opportunities at selected sites. These measures are expected to support more stable output and enhance returns over time. Active asset management also played a key role in mitigating controllable losses and managing operational risk as well as supporting improvements in underlying portfolio yield, reflecting the Investment Manager’s continued focus on targeted value-enhancing measures.

Through close oversight of contractors and targeted interventions at asset level, ORIT continued to maximise net energy production and improve performance consistency. Lifecycle management initiatives, including upgrades, repowering and hybridisation, are helping to extend asset life and future-proof performance across the portfolio.

Market context and portfolio resilience

Energy markets during the year continued to be shaped by power price volatility and revisions to external reference curves, particularly downward adjustments to medium- and long-term power price forecasts. These factors created valuation headwinds for renewable infrastructure assets across the sector. Regulatory outcomes also presented challenges, as illustrated by the UK Government’s decision to change the indexation applied to ROC revenues, which has placed further pressure on sector valuations.

Despite periodic shifts in global political rhetoric, European energy policy continues to demonstrate strong alignment between energy security, climate objectives and economic resilience. Renewable capacity is being built out across the continent as governments prioritise domestic energy supply and long-term infrastructure investment. ORIT operates within this supportive policy framework, which remains anchored in structural energy security and decarbonisation goals.

The accelerating build-out of data centres and increased electrification across economies – including AI-driven demand from hyperscale operators – is contributing to a structural increase in power demand, reinforcing the strategic importance of reliable renewable generation across Europe.

Against this backdrop, ORIT’s portfolio has demonstrated relative resilience. The high proportion of contracted and inflation-linked revenues has helped insulate cash flows from short-term market volatility, while diversification across geographies, technologies and asset stages has reduced concentration risk and smoothed performance through varying market and weather conditions.

The Board has maintained rigorous oversight of valuation processes and assumptions, all of which are subject to independent review and challenge. While short-term NAV movements reflect prevailing market conditions, the Board remains confident in the robustness of the valuation methodology and the long-term fundamentals of the portfolio, particularly in light of successful asset sales at or above net asset value, and benchmarking of comparable assets.

1 Peer-group analysis, Jefferies report.

Governance, oversight and board composition

Strong and proportionate governance remains central to ORIT’s ability to execute its strategy effectively. During the year, the Board devoted significant time to overseeing capital allocation decisions, valuation processes and risk management, while maintaining constructive challenge of the Investment Manager. A key development was the revision of the Company’s investment management fee arrangements, switching from NAV-based fees to a blend of market capitalisation and NAV, improving alignment with shareholders and delivering a reduction in ongoing costs. From the inception of this change on 1 November 2025, this has saved ORIT shareholders £150k, which equates to an approximate annualised cost saving of c.£1 million.

Non-Executive Director James Cameron will stand down from the Board at the forthcoming AGM in June 2026. The Board would like to thank James for his contribution and service. The Board does not intend to appoint a replacement at this time, reflecting a desire to maintain an appropriately sized Board and demonstrate cost discipline, while continuing to keep succession planning and skills coverage under regular review.

ESG and stewardship

Environmental, social and governance (“ESG”) considerations remain integral to ORIT’s approach to long-term value creation and risk management. ORIT is classified as an Article 9 fund, reflecting its core objective of contributing to environmental and social outcomes alongside delivering sustainable returns. ESG factors are embedded across asset management and capital allocation decisions, supporting portfolio resilience and alignment with the Company’s long-term objectives.

Alongside financial performance, ORIT continues to deliver tangible benefits in the communities where it operates. During the year, community benefit funds, local engagement initiatives and partnerships focused on education and skills supported positive social outcomes and helped strengthen long-term relationships around portfolio assets.

Strong governance and active stewardship underpin this approach. The Board maintains oversight of ESG risks and opportunities to ensure consistent standards are applied across the portfolio and that sustainability considerations are integrated into decision-making. Further detail on ESG performance, community initiatives and impact outcomes is set out elsewhere in this report.

ORIT 2030 strategy and outlook

ORIT’s 2030 strategic framework, announced in September 2025, provides a clear structure for capital allocation and portfolio development over the medium term. The actions taken during FY 2025 – particularly in relation to capital recycling, operational optimisation and debt management – are consistent with the early execution of this strategy.

Since the year end, geopolitical tensions in several regions have intensified, contributing to heightened volatility in global energy markets and further reinforcing the importance of secure and resilient domestic power generation across Europe. Over the medium term, ORIT’s diversified portfolio, contracted revenue profile and active asset management all provide important mitigants against prolonged market volatility. The Company remains focused on navigating this environment through selective capital recycling, disciplined reinvestment and the continued development of flexibility initiatives such as battery co-location, positioning the portfolio to adapt as market conditions evolve.

Looking ahead, while near-term market conditions are likely to remain uncertain, the long-term structural drivers for renewable infrastructure remain compelling. Policy initiatives such as Clean Power 2030, alongside the continued focus on energy security, decarbonisation and long-term demand for clean power, are supporting the need for new renewable capacity and creating opportunities for competitively priced projects. ORIT is well positioned to navigate this environment through its pan-European diversification, operational focus and clear strategic framework. Progress within the development pipeline during the year, including the award of a Contract for Difference in AR7 at one of our developers, reinforces the depth of opportunity available to the Company as market conditions evolve.

On behalf of the Board, I would like to thank shareholders for their ongoing support and the Investment Manager for their continued commitment. The Board remains focused on delivering long-term value through the execution of ORIT 2030 and driving actions to support NAV growth over time.

1 How do you assess ORIT’s overall performance in 2025, given the challenging backdrop for listed renewables?

2025 saw sustained pressure on valuations driven by higher discount rates and downward revisions to power price assumptions, alongside a more cautious investor backdrop. These valuation headwinds contributed to ORIT’s first year of negative NAV total return, reflecting market conditions.

For ORIT, this environment reinforced the importance of decisive action at the company level, including asset sales and capital recycling, alongside a continued emphasis on active portfolio management. Our core focus for the year has been on protecting income, maintaining balance sheet resilience and positioning the portfolio to support NAV growth over the long term.

While operational performance from the portfolio was below budget by 7%, there was a marked improvement over the prior year (below by 13%) (as highlighted on pages 24 to 29). On a weather-normalised basis, we were encouraged by the year-on-year improvement in the portfolio generation against budget; testament to the technical asset management that has been delivered and improvements made to availability. Overall output increased in the period, and the cash flows produced-supported by a high proportion of contracted revenues-allowed us to deliver fully covered dividends.

We are also pleased with how we tracked against the capital allocation objectives we set out earlier in the year. Against a challenging backdrop, we completed ~£74 million in asset sales – all at NAV or slightly above (at a time when many market participants have found disposals difficult) – and renegotiated portions of our capital structure to bring down the cost of debt.

2 What does active management mean for ORIT?

Active management for ORIT is about making deliberate, forward-looking choices rather than simply responding to events. On the asset side in 2025, this meant prioritising interventions with the greatest long-term impact, strengthening performance visibility and accelerating resolution of underperformance. On the financial side, it meant actively managing leverage, debt costs and liquidity to preserve flexibility in an uncertain environment. These decisions are often incremental rather than transformational in any single year, but collectively they shape the portfolio’s resilience, risk profile and ability to compound value over time. Our aim is not simply to manage assets, but to actively steward capital through the cycle.

3 How are you thinking about capital allocation and the role of construction in driving future NAV growth?

With capital scarce across the sector, efficient deployment has become paramount. Our approach is to be highly selective – protecting our capital structure first, funding high-conviction opportunities next, and returning capital where appropriate. Capital recycling has played an important role in this, allowing us to crystallise value, and as we move through our ORIT 2030 strategy, redeploy proceeds into areas with stronger growth potential. This might include increasing exposure to co‑located battery storage and repowering opportunities within the existing portfolio, where we can enhance asset flexibility, extend asset life and capture additional value from system volatility.

Looking forward, we are increasingly excited about investing more in construction – returning to what has historically been a core part of our strategy – through which we believe a meaningful portion of future NAV growth will be generated. Construction assets offer the opportunity to capture value through taking on construction risk and then managing the asset to operational stage through disciplined delivery and risk management. ORIT benefits from OEGen having deep expertise and experience in construction, and is well-placed to deliver on this higher-growth strategy which forms a core component of the ORIT 2030 strategic priorities.

4 How does ORIT’s platform support confidence in the long-term strategy, despite current sector challenges?

The listed renewables sector is in a challenging period, but we remain confident in the long-term fundamentals of renewable infrastructure. Demand for cleaner, lower-cost power, system flexibility and energy security continues to grow, irrespective of short-term market cycles. Through ORIT, we can add capacity and help meet these needs, delivering benefits for consumers while supporting the transition to net zero.

While the asset class is long-term in nature, delivering sustainable growth requires near-term agility and proactive portfolio management. We have demonstrated this through our actions during the year and remain confident that this approach will strengthen ORIT’s foundations for long-term value creation.

Furthermore, OEGen’s deep sector specialism gives ORIT access to more than 150 energy professionals across development, construction, asset management and optimisation. This scale and depth of expertise is increasingly important as the system evolves to require greater flexibility through storage, smart optimisation and co-located solutions, and positions ORIT to capture potential value-creation opportunities in areas such as battery storage. In addition, our proximity to the wider Octopus Energy group provides valuable insight into how renewable assets interact with end consumers and power markets in practice.

The ORIT 2030 strategy launched in September 2025 provides a clear framework for navigating the current environment that the sector is in. ORIT will place a strong focus on growth through strategic capital allocation, active management and value creation. While progress will not be linear, we believe this approach positions the Company to grow NAV sustainably as market conditions normalise, whilst continuing to offer a progressive dividend.

Operating Assets: Supporting Income

Top ten operating assets by capacity (pro-rata)

Site name

Technology

Country

Description

Pro rata capacity(MW)1

Start of operations

Remaining asset life (years)

Stake %1

Fidorfe2

Solar

Ireland

Fidorfe is a 68 MW solar farm that forms part of the operational Ballymacarney complex – the largest solar complex in Ireland. Fidorfe benefits from a 15-year fixed price offtake with Microsoft.

68

18/12/2023

38

100%

Ballymacarney2

Solar

Ireland

Ballymacarney is a 54 MW solar farm that forms part of the operational Ballymacarney complex that also benefits from a 15-year fixed price offtake with Microsoft.

54

18/12/2023

38

100%

Cumberhead

Onshore Wind

UK

Cumberhead is a 50 MW onshore wind farm in South Lanarkshire, Scotland. The site has a PPA with Kimberly-Clark.

50

31/03/2023

27

100%

Muckerstown2

Solar

Ireland

Muckerstown is a 48 MW solar farm that forms part of the operational Ballymacarney complex that also benefits from a 15-year fixed price offtake with Microsoft.

48

18/12/2023

38

100%

Harlockstown2

Solar

Ireland

Harlockstown is a 42 MW solar farm that forms part of the operational Ballymacarney complex.

42

23/09/2024

39

100%

Lincs

Offshore Wind

UK

Lincs Wind Farm is a 270 MW offshore wind farm located 8 kilometres (5 miles) off the coast of Skegness, England. ORIT and the Octopus Energy Generation-managed Octopus Renewables Infrastructure SCSp fund together own 31% of the windfarm through an SPV, which has a PPA with Centrica.

42

31/10/2013

23

15.50%

Suolakangas

Onshore Wind

Finland

Suolakangas is a 38 MW onshore wind farm in North Finland. The site has a 100% hedged PPA contract for 2026 with Eesti Energia and is investigating ancillary service potential for 2027.

38

29/12/2021

26

100%

Leeskow

Onshore Wind

Germany

Leeskow is a 35 MW onshore wind farm in Germany. The site holds a 20-year, fixed-rate EEG contract backed by the German state for full production.

35

30/09/2022

27

100%

Saunamaa

Onshore Wind

Finland

Saunamaa is a 34 MW onshore wind farm in North Finland. The site has a 100% hedged PPA contract for 2026 with Eesti Energia and is investigating ancillary service potential for 2027.

34

28/08/2021

26

100%

Breach3

Solar

UK

Breach solar is a ground-mounted, utility-scale solar farm with a capacity of 67.4 megawatts peak, located in Burwell, Cambridgeshire. The site has a PPA with Iceland Foods.

34

25/06/2024

38

51%

Note: Shaded rows indicate exited in the year.

1 As at 31 December 2025.

2 Note that these five sites are sometimes (in this report and elsewhere) collectively referred to as ‘the Ballymacarney solar complex’.

3 ORIT owned 100% of this asset until 30 December 2025, when it exited 49%. At year-end ORIT held (and continues to hold) 51%.

Remaining operating assets

Site name

Technology

Country

Pro rata capacity (MW)1

Start of operations

Remaining asset life (years)

Stake %1

Ermine Street

Solar

UK

32

29/07/2014

19

100%

Kilsallaghan2

Solar

Ireland

29

18/12/2023

38

100%

Abbots Ripton

Solar

UK

25

28/03/2014

28

100%

Cerisou

Onshore Wind

France

24

15/11/2022

27

100%

Wilburton 2 (Mingay)

Solar

UK

19

29/03/2014

18

100%

Westerfield

Solar

UK

13

25/03/2015

19

100%

Chisbon

Solar

UK

12

03/05/2015

25

100%

Ollieres 1

Solar

France

12

19/03/2015

29

100%

Arsac 2

Solar

France

12

05/03/2015

17

100%

Arsac 5

Solar

France

12

30/01/2015

16

100%

Wiggin Hill

Solar

UK

11

10/03/2015

14

100%

Ollieres 2

Solar

France

11

19/03/2015

28

100%

Chalmoux

Solar

France

10

01/08/2013

28

100%

Fontienne

Solar

France

10

02/07/2015

29

100%

Istres

Solar

France

8

18/06/2013

27

100%

Saint Antonin du Var

Solar

France

8

28/11/2013

28

100%

Cuges

Solar

France

7

17/04/2013

27

100%

Ottringham

Solar

UK

6

07/08/2013

29

100%

Charleval

Solar

France

6

26/03/2013

27

100%

La Verdière

Solar

France

6

27/06/2013

27

100%

lovi 1

Solar

France

6

17/07/2014

29

100%

lovi 3

Solar

France

6

17/07/2014

29

100%

Brignoles

Solar

France

5

26/06/2013

27

100%

Penhale

Solar

UK

4

08/03/2013

27

100%

Crossdykes3

Onshore Wind

UK

NA

30/06/2021

NA

NA

Note: Shaded rows indicate exited in the year.

1 As at 31 December 2025.

2 Note that these five sites (see prior page) are sometimes (in this report and elsewhere) collectively referred to as ‘the Ballymacarney solar complex’

3 ORIT owned 51% of this asset until 30 December 2025, when it exited its entire holding.

Weighted average remaining asset life by capacity

Technology

Years

Onshore wind

26.5

Offshore wind

22.7

Solar

31.4

Total

29.7

Developer Portfolio: Supporting Capital Growth

Our developer portfolio is a core driver of ORIT’s long-term growth strategy, providing the future pipeline of construction-ready projects that will underpin value creation across the decade.

Simply Blue Group

• 4% stake• Floating offshore wind• UK, Europe

2025 marked a pivotal year for Simply Blue as ORIT completed a partial sale of the floating offshore wind platform, reducing capital intensity while retaining a small position in the remaining projects. The transaction delivered c. £5 million proceeds to ORIT (£3 million upfront and £2 million through deferred proceeds), while governance and capital structure were significantly simplified. The 100 MW Salamander project achieved planning approval and secured a new lead partner to take it forward. In addition, the 100 MW Erebus project secured a Contract for Difference (CfD) in the UK’s AR7 auction in January 2026, marking a significant de-risking milestone for the platform. With ORIT now holding a small continuing interest, Simply Blue will no longer be included in the Company’s published pipeline metrics.

Nova sustainable fuels

• 22.5% stake• Sustainable e-Fuels• Canada

Following the carve-out of the e-Fuels business (Nova) from Simply Blue, Nova made strong progress on its Nova Scotia sustainable aviation fuel project during 2025. The project design was advanced and long-term supply of sustainable biomass was secured with a major forestry partner. The team is also preparing the next phase of funding, planned for 2026, to continue development. Nova remains well positioned as demand for low-carbon aviation fuels grows in North America.

Wind2

• 25% stake• Onshore wind• UK

Wind2 continued development activity across its 1 GW+ pipeline during the year. A number of planning submissions are now complete, and several sites are expected to reach determination during 2026. The first of these has been negative, with Kirkton being denied consent by the Scottish Minister. A number of projects in Wales and Scotland either received ‘gate 2’ offers as part of the grid reform process, or are expected to qualify for protected grid offers should they receive consent. This provides a pathway for ready-to-build status from 2029 onwards.

BLC Energy

• 100% stake• Solar and BESS• UK

BLC has maintained strong momentum, with five projects totalling 394 MW now submitted for planning approval and currently awaiting decisions. While the UK grid reform process has extended timelines across the sector, BLC’s focus on larger, higher-quality sites and their positioning within the reformed grid queue is expected to support improved delivery certainty. The most advanced BLC projects could reach ready-to-build status later this year, subject to the timing of final planning and grid outcomes. Post-period, an additional £1.2 million of funding was committed, taking the total commitment to £4.7 million.

Nordic Generation

• 30% stake• Solar and Onshore wind• Finland

Nordic Generation continued to progress its strongest projects, with the first targeting ready-to-build in 2026. The updated plan forecasts around 1 GW reaching ready-to-build by the end of 2030 after two sites were removed due to defence restrictions. The team is now focusing on advancing the most mature projects and supplementing the pipeline through selective acquisitions. Also during the year, Nordic Generation supplemented its pipeline through the transfer of project rights of three advanced onshore wind projects totalling up to 800 MW of additional capacity, supporting a more de‑risked route to delivery alongside its existing development activity.

HYRO

• 25% Stake• Green Hydrogen• UK

ORIT exited HYRO in 2025 following the sale of the Northfleet hydrogen project, receiving proceeds in line with valuation. HYRO will not feature in future developer reporting.

Metrics

5

c. 3.3 GW

2026

Developer investments

Combined pipeline of renewable projects

First project expected to reach Ready‑to-Build (“RTB”)

Figure 1: Breakdown of pipeline capacity by stage (GW)

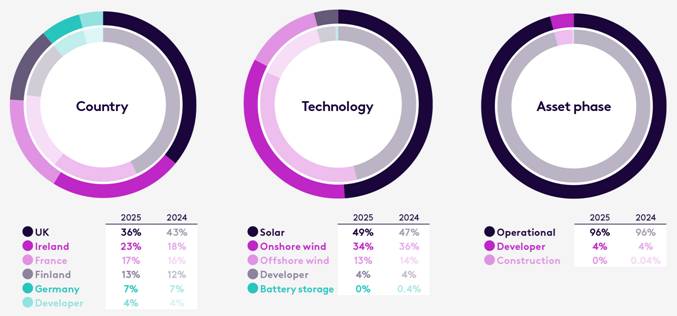

Portfolio composition on a total value of all investments and by MW basis in line with the Company’s investment policy as at 31 December 2025. The investments are valued on an unlevered basis and including amounts committed but not yet incurred.

Portfolio breakdown by total value of all investments (£m)

Year-on-year changes in country exposure primarily reflect the partial disposal of the UK Breach solar asset and the sale of ORIT’s 51% interest in the Crossdykes wind farm, reducing the UK weighting and increasing the relative share of continental European assets.

Technology mix movements primarily reflect the exit from the Woburn Road battery storage asset and modest rebalancing following the Breach and Crossdykes disposals.

Asset phase movements reflect the exit from the Woburn Road battery project, leaving no assets under construction at year end. Construction exposure is expected to increase over time as the ORIT 2030 strategy prioritising higher-growth construction investments is progressed.

Note: Outer ring as at 31 December 2025, inner ring as at 31 December 2024

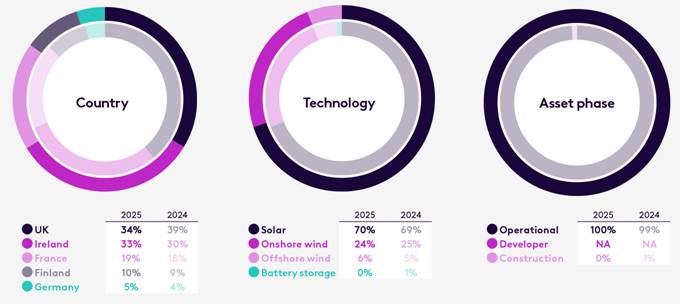

740 MW

Capacity owned

Portfolio composition broken down by MW of capacity pro rata for ORIT’s ownership on a current invested basis as at 31 December 2025

Portfolio breakdown by capacity (MW)

Year-on-year changes in country exposure primarily reflect the partial disposal of the UK Breach solar asset and the sale of ORIT’s 51% interest in the Crossdykes wind farm, reducing the UK weighting and increasing the relative share of continental European assets.

Technology mix movements primarily reflect the exit from the Woburn Road battery storage asset and modest rebalancing following the Breach and Crossdykes disposals.

Asset phase movements reflect the exit from the Woburn Road battery project, leaving no assets under construction at year end. Construction exposure is expected to increase over time as the ORIT 2030 strategy prioritising higher-growth construction investments is progressed.

Note: Outer ring as at 31 December 2025, inner ring as at 31 December 2024

£908m

Total value of all investments

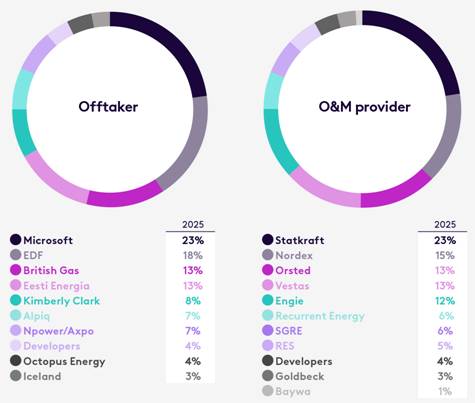

Portfolio composition broken down by offtaker and O&M providers as a percentage of total value of all investments as at 31 December 2025.

Having multiple offtakers offers advantages such as risk diversification and offers local expertise in ORIT’s key geographical markets.

A diversified group of O&M providers allows ORIT to leverage competitive pricing and specialised expertise.

Totals may not add up due to rounding

Capital Allocation in 2025

ORIT’s capital recycling programme, launched in 2023 as part of a broader capital allocation strategy, has remained a central focus over the financial year and in March 2025 ORIT set out three capital allocation objectives. Progress against each objective is outlined below.

Objective

2025 Update

Commentary

£20m buyback extensionAnnounced in March 2025, taking the programme to £30 million

£19.2m spent

Over the year the Company bought back 28,081,835 shares adding 1.4 pence to NAV per share. This brings the total to £26.0 million since the programme began.

Realise at least £80m from asset salesBy the end of FY 2025 to fund capital allocation initiatives together with making selected accretive investments

£74m realised

During 2025, the Investment Manager completed asset disposals generating proceeds of approximately £74 million (of which £4.3 million represent deferred components), in line with its capital recycling programme. These transactions support the underlying asset valuations and provide capacity to reduce debt and reinvest into higher-growth opportunities aligned with the ‘ORIT 2030’ strategy. ORIT continues to progress discussions with prospective buyers for additional assets and maintains its partnership with Tokyo Century through the Breach project.

<40% leverage targetBring total gearing down to below 40% GAV by year end

45%

The gearing ratio ended the year broadly flat year on year. However, over the period total debt reduced by £56.3 million to £402.1 million from £458.4 million. During the year, £100 million of borrowings were refinanced into a lower-cost facility, reducing the Company’s blended cost of debt from 4.0% to 3.3%. Disposal proceeds and portfolio cash generation were used to fund repayments across the Group’s revolving credit and project-level debt facilities. Despite the reduction in absolute debt, gearing was broadly unchanged as NAV and GAV also declined over the year. We continue to view c.40% gearing as an appropriate anchor for the Company, with further reductions expected as disposal proceeds are received and applied.

Company Developments During 2025

Portfolio activity – Investments

Portfolio activity – Exits

June

Conditional acquisition of sixth Irish solar siteAgreed to conditionally acquire a 32.6 MW Irish solar site for €27 million through a forward purchase agreement. This project, Irishtown, is the sixth at the Ballymacarney complex, and will increase total capacity by 14% to 274 MW. Construction is ongoing and progressing in line with the project plan. ORIT is expected to complete the purchase after operational testing in the second half of 2026. No capital is required until then.

December

Sale of stake in Breach solar and of entire holding in Crossdykes onshore windCompleted the sale of 49% of the 100% interest in Breach solar farm, and of the entirety of the 51% holding in Crossdykes onshore wind, with pricing at a modest uplift to holding value.

April

Simply Blue Group carve outSimply Blue Group’s Canadian sustainable fuel project was carved out to form Nova Sustainable Fuels (“Nova”), with new investment provided by two other funds managed by Octopus Energy Generation; ORIT retains a 22.5% stake in the Nova business.

October

Sale of Interest in HYROCompleted the sale of its entire interest in HYRO Energy Limited, a UK-based green hydrogen and e-fuels development platform, for a total expected consideration of £4.6 million, in line with the latest holding value. £2.6 million was received immediately, with the remainder contingent on the delivery of key construction milestones for HYRO’s first project, which has recently received planning consent.

March

Follow-on investment into BLC Energy LimitedMade a follow-on investment of £1.5 million into BLC Energy Limited (“BLCe”), a renewable energy development company, specialising in developing solar PV and co-located battery storage projects across the UK. This follows the initial investment on 31 July 2023, where ORIT secured preferential rights for development funding to the new pipeline. The new funding will support BLCe’s most advanced projects, leveraging the UK’s reformed grid queue process.

October

Sale of stake in Simply Blue’s offshore wind platformORIT’s investee company, Simply Blue, agreed to sell 80% of its offshore wind development arm to Kansai Electric, in line with ORIT’s valuation. The deal follows the carve-out of Nova and enabled partial repayment of ORIT’s shareholder loan, and leaves ORIT with a minority interest in the platform.

February

Norgen commitmentCommitted an additional €3.4 million (£2.8 million equivalent) to Nordic Generation (“Norgen”), a specialist developer focused on the Finnish wind and solar market and converted its existing holding into a direct 30% stake in the integrated Norgen development business.

MarchDebt managementThe Company signed a £100 million, five-year term loan facility on attractive terms, with net proceeds used to pay down the RCF. At the same time the RCF was reduced in size from £270.8 million to £150 million and the maturity extended to June 2028.

Portfolio Performance

Figure 3: Performance of Company’s underlying operational investments

Output1

Revenue

Opex

EBITDA

Operational portfolio

1,304 GWh

£138.8m

£50.4m

£88.3m

+5% vs 2024

+5% vs 2024

+9% vs 2024

+3% vs 2024

-7% vs budget

-4% vs budget

-1% adverse to budget

-6% vs budget

(2024: 1,240 GWh)

(2024: £131.7m)

(2024: £46.2m)

(2024: £85.5m)

Solar

537 GWh

£60.2m

£15.6m

£44.7m

+18% vs 2024

+15% vs 2024

+17% vs 2024

+15% vs 2024

-2% vs budget

-0.1% vs budget

-1% adverse to budget

+0.3% vs budget

(2024: 457 GWh)

(2024: £52.2m)

(2024: £13.3m)

(2024: £38.9m)

Onshore wind

615 GWh

£36.8m

£11.0m

£25.7m

+2% vs 2024

-9% vs 2024

+13% vs 2024

-16% vs 2024

-11% vs budget

-9% vs budget

-0.2% % adverse to budget

-13% vs budget

(2024: 631 GWh)

(2024: £40.3m)

(2024: £9.7m)

(2024: £30.6m)

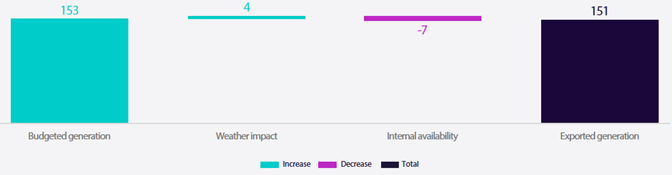

Offshore wind

151 GWh

£41.7m

£23.8m

£17.9m

-1% vs 2024

+6% vs 2024

+3% vs 2024

+12% vs 2024

-2% vs budget

-5% vs budget

-2% adverse to budget

-10% vs budget

(2024: 153 GWh)

(2024: £39.2m)

(2024: £23.2m)

(2024: £16.0m)

Note: Totals may not add up due to rounding.

1 Generation quoted is post-compensation (actual output + compensation for equivalent lost production ORIT is entitled to under curtailment and/or contractual mechanisms).

Commentary

Operations

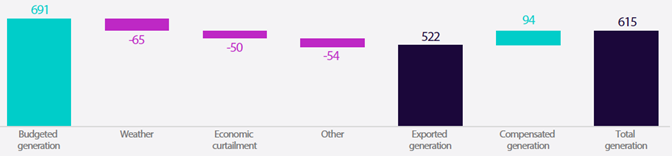

In 2025, ORIT’s compensated generation increased by 5.1% year-on-year (from 1,240 GWh to 1,304 GWh), but was 6.5% below budget, equivalent to a shortfall of 90.2 GWh.

On a weather-normalised basis (i.e adjusted for variations from expected wind and solar resource), portfolio performance in 2025 was 4.9% below budget. After further adjusting for Irish grid curtailment, generation was 2.6% below budget. This represents a material improvement compared with the prior year, when weather-normalised performance was 9.3% below budget, reflecting greater control over operational performance across the portfolio during FY 2025 compared to the prior year.

Revenues of £138.8 million were achieved in the year under review (2024: £131.7 million), representing an increase year-on-year driven by higher output, albeit 4% below budget. Overall Opex amounted to £50.4 million in the year (2024: £46.2 million), less than 1% adverse to budget. The resulting total EBITDA, across ORIT’s operational portfolio, was £88.3 million, slightly up on the previous year (2024: £85.5 million), but 6% below budget.

During FY 2025, ORIT benefitted from a full year of operations from the five Irish solar assets that were acquired in 2024, helping to increase solar output by 17.7% (from 456.6 GWh to 537.4 GWh) year on year.

Onshore wind generation dropped by 2.4% (or 17 GWh) over the same period; however, it is important to note that the 2024 generation included 67 GWh contributed by the Swedish wind asset, which was sold in Q3 2024.

Most of the variance versus budget in 2025 was driven by factors outside ORIT’s operational control, primarily grid curtailment in Ireland. This resulted in 52.5 GWh of lost generation, of which 17.3 GWh was compensated during the year. As noted in the 2025 Interim Report, there remains potential for the full curtailment losses to be compensated, subject to the outcome of the ongoing proceedings before the Court of Justice of the EU later this year, representing upside which is not included in the portfolio valuations. Adverse weather conditions were the second most significant factor, contributing to 23.6 GWh of lost generation. While solar irradiance was favourable, delivering an additional 36.9 GWh, this was more than offset by below-average wind speeds, which reduced output by 60.5 GWh.

Strong contractual protections across the portfolio mitigated much of the remaining losses. This was most evident in the onshore wind portfolio where, after adjusting for low wind conditions, total gross losses amounted to 104.3 GWh. Of this, 93.6 GWh was compensated under contractual arrangements, leaving only limited residual economic exposure. Across the whole portfolio, this includes discrete operational issues, several of which have now been resolved, including losses from lichen covering panels at the Arsac 2 and Arsac 5 solar sites in France and static bat curtailment at the Cerisou onshore wind asset, which has since been replaced with a dynamic system. Other items, including the repowering of the Cuges solar site after the shutdown, are scheduled to be addressed in 2026.

Improvements and optimisation initiatives

During the period, ORIT launched its dedicated Value Enhancement Programme (“VEP”), establishing a formal, portfolio-wide framework to identify and deliver long-term value accretive interventions. The programme targets hybridisation, co-location, repowering, life-extension and strategic upgrade opportunities, enabling systematic prioritisation of initiatives that enhance resilience and risk-adjusted returns. Early workstreams are already under way, including repowering assessments at the UK ROC solar assets, and hybridisation analysis at the Leeskow wind farm in Germany.

Operational excellence remains a central focus. A transformer-health triage process is being deployed across the UK solar fleet to support condition-based asset management, inform spares strategies and guide repowering decisions. On the wind portfolio, we partnered with a data expert to employ automated performance and component health monitoring. This is complemented by a new energy-yield benchmarking tool, enabling more granular diagnostics and continuous benchmarking of performance. Our compliance capability was further strengthened through the introduction of an automated Curtailment Compliance Tool to monitor alignment between National Grid instructions, site response and forecasting. Additionally, a Blade Management System, which integrates turbine-level analytics, structured annual inspections and centralised repair planning has been rolled out in 2025. A portfolio-wide blade-repair tender is currently in progress to secure consistent pricing and improved commercial terms.

Targeted interventions delivered measurable value, most notably at the Mingay solar farm in the UK, where the team worked with our partners to successfully convert an 83-day static DNO outage into a 35-day dynamic curtailment regime, materially reducing (1) the length of the downtime, and (2) the impact of the downtime by allowing partial export. ORIT continued to benefit from OEGen’s cross-fund scale and procurement leverage. A cross-fund initiative secured a recovery of nearly €2 million for defective modules for ORIT, following earlier unsuccessful stand-alone warranty claims. Similarly, OEGen’s coordinated engagement with two external asset managers – who oversee several ORIT sites as well as assets across the wider OEGen portfolio – is improving accountability, reporting quality and responsiveness. This collective approach strengthens commercial negotiation power, enhances issue-management processes and enables consistent delivery standards across ORIT’s assets.

Alongside these initiatives, the HSE programme continued to reinforce strong operational standards across the portfolio. Contractor and site audits were completed at Breach, with Cumberhead scheduled next, supporting contractor accountability, environmental compliance and the continued embedding of a robust safety culture.

Note: Totals may not add up due to rounding.

Figure 4: 2025 solar output variance to budget (GWh)

Figure 5: 2025 onshore wind output variance to budget (GWh)

Figure 6: 2025 offshore wind output variance to budget (GWh)

Case study

Protecting revenue through active curtailment management

In Q4 2025, the 19 MWp Mingay Farm was impacted by a grid outage to facilitate substation upgrade works by the distribution network operator, UK Power Networks (“UKPN”). The outage was originally expected to last over three months, posing a risk to revenue and breaching the project’s loan covenant, which restricts the duration of grid export interruptions. Through early and sustained engagement with UKPN, the outage period was successfully reduced to 45 days, running from 6 October 2025 to 19 November 2025. To minimise the impact, the asset management team implemented a dynamic curtailment strategy, enabling the site to export energy based on daily export limits issued by UKPN. Working closely with the O&M contractor, export caps were remotely adjusted each day to align with available grid headroom. As a result, the site exported c. 432 MWh, generating c. £85k in revenue, income that would otherwise have been lost under a zero-export scenario. This approach ensured compliance with lender requirements and protected revenues, without any additional capital expenditure.

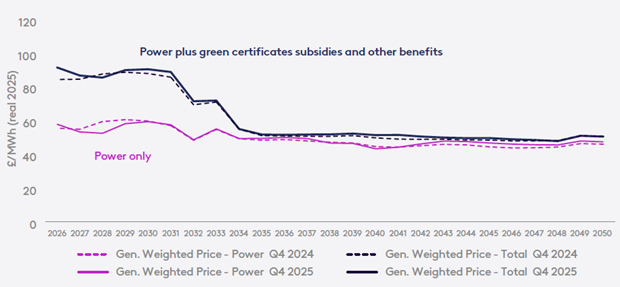

Generation-weighted price

The combination of forward market prices and independent long-term power price forecasts, together with the power purchase agreements (“PPAs”) which the Investment Manager has originated, make up the portfolio’s forecast power only generation-weighted price (“Power only GWP”). The total generation-weighted price, is derived by including subsidies and additional benefits, such as green certificates (“Total GWP”). The Power only GWP and Total GWP for the period to 2050 are shown in Figure 7. The curves are blended across the markets in which the portfolio’s generation assets are located, weighted by the portfolio generation mix and converted into £/MWh. On average, the graph shows power only GWP of £55.99/MWh (real 20) in the period 2026-2030 and £47.67/MWh in the period 2031-2050. Movements in the portfolio’s Power only GWP and Total GWP have been limited both due to the revenue hedges which the Investment Manager has proactively executed across the portfolio as well as the diversification exhibited across the portfolio.

Figure 7: Generation-weighted price forecast

A summary of the capture price discounts utilised in the assets’ valuations is presented below in Figure 8. The percentages are the average differences between the generation-weighted and time-weighted power prices. These assumptions are provided by third party advisors and use site-specific assumptions for onshore and offshore wind.

Figure 8: Baseload price and capture discount forecasts

Value

Market

Technology

Units

2025-2029

2030-2034

2035-2039

2040-2044

2045-2050

Baseload price

GB

£/MWh (real 2025)

72

72

68

66

Capture price discount

GB

%

25%

25%

25%

28%

Capture price discount

GB

%

11%

18%

21%

25%

25%

Capture price discount

GB

%

9%

17%

21%

23%

24%

Baseload price

FR

EUR/MWh (real 2025)

78

82

79

75

Capture price discount

FR

%

12%

12%

Capture price discount

FR

%

42%

41%

41%

43%

Baseload price

FI

EUR/MWh (real 2025)

49

63

65

66

65

Capture price discount

FI

%

17%

19%

22%

22%

22%

Baseload price

DE

EUR/MWh (real 2025)

82

78

Capture price discount

DE

%

25%

29%

Baseload price

I-SEM

EUR/MWh (real 2025)

89

89

Capture price discount

I-SEM

%

22%

23%

Note: Values in the above table are not shown where the relevant asset has no merchant exposure in three or more years in the relevant period.

Portfolio revenue forecasts

Figure 9 presents ORIT’s forecast revenues through to 2050, categorised by price structure. The revenues are categorised as fixed via either subsidy (Fixed – Subsidy) or fixed price PPA (Fixed – Power) and the variable revenues derive from power being sold on a merchant basis (Variable – Power) or from other sources of variable revenue (Variable – Other).

88% of ORIT’s forecast revenues for the 24 months up to 31 December 2027 are fixed, which represents an increase of four percentage points compared with ORIT’s position 12 months ago due to continued revenue hedging across ORIT’s Finnish and GB portfolio despite asset disposals (Breach and Crossdykes). On a present value basis 49% of the portfolio’s value derives from fixed price revenues and 51% from variable price revenues.

All of ORIT’s power price hedges continue to be structured on a pay-as-produced basis. This contrasts with other commonly observed hedge structures – such as baseload or fixed shape hedges – which require the asset to assume additional (often costly) risks, especially during periods of underproduction, given the need to buy back power at the market price in order to deliver under the hedge’s baseload or fixed shape generation profile.

ORIT’s portfolio continues to offer protection against inflation, owing to its high proportion of contractually inflation-linked revenues. These derive from subsidies and inflation-linked corporate PPAs which the Investment Manager has originated, such as the PPA between Breach solar farm and Iceland Foods. Over the 10 years to 31 December 2035, 43% of ORIT’s forecast revenues are inflation-linked. This is a 5 percentage point decrease compared with ORIT’s position 12 months ago, due to:

· Asset sales: sales of stakes in Crossdykes and Breach, both of which benefitted from inflation-linked corporate PPAs

· Regulatory updates: the outcome of the UK government’s ROC indexation consultation confirms that ROC buyout prices will be indexed to CPI, rather than RPI, from April 2026 onwards

· Contractual maturities: the natural progression of the 10-year look-forward period brings the expiry dates of inflation-linked subsidies and PPAs closer to the present.

ROC revenues have been adjusted based on the outcome of the recent UK government’s consultation on ROC indexation, specifying that from April 2026 onwards, indexation will be calculated against CPI rather than RPI. Of the forecast “Fixed – Subsidy” revenues for the 24 months up to 31 December 2027, 56% derive from the ROC buyout. This is equivalent of 28% of total revenues over 24 months, and 24% of total revenues on a ten-year look forward.

Figure 9: Fixed vs variable revenue forecasts (see page 29 of the annual report)

Figure 10: Revenue forecasts by inflation-linkage (see page 29 of the annual report)

Financial Review

The financial statements of the Company for the year ended 31 December 2025 are set out in the Company’s Annual Report. The financial statements have been prepared in accordance with UK-adopted International Accounting Standards in conformity with the requirements of the Companies Act 2006. In order to continue providing useful and relevant information to its investors, the financial statements also refer to the “intermediate holding companies”, which comprise the Company’s wholly owned subsidiary, ORIT Holdings II Limited and its indirectly held wholly owned subsidiaries ORIT UK Acquisitions Limited, ORIT Holdings Limited and ORIT UK Acquisitions Midco Limited.

Net assets

Net assets have decreased from £570.4 million as at 31 December 2024 to £494.8 million as at 31 December 2025, primarily due to a decrease in the fair value of the portfolio of assets as described in the Portfolio Valuation section. The net assets comprise the fair value of the Company’s investments and net current assets, as detailed in the table 16 on the right.

Income

In accordance with the Statement of Recommended Practice: Financial Statements of Investment Trust Companies and Venture Capital Trusts (“SORP”) issued in July 2022 by the Association of Investment Companies (“AIC”), the statement of comprehensive income differentiates between the ‘revenue’ account and the ‘capital’ account, and the sum of both items equals the Company’s profit for the year. Items classified as capital in nature either relate directly to the Company’s investment portfolio or are costs deemed attributable to the long-term capital growth of the Company (such as a portion of the Investment Manager’s fee).

Table 16: Results as at 31 December

2025

2024

£m

£m

Fair value of portfolio of assets

603.2

699.6

Cash held in intermediate holding companies

1.8

7.1

Bank loans and accrued interest held in the intermediate holding companies

-116.2

-151.2

Fair value of other net assets/(liabilities) in the intermediate holding companies

-3.4

5.8

Fair value of Company’s investments

485.4

561.3

Company’s cash

10.8

11.9

Company’s other net liabilities

-1.4

-2.8

Net asset value as at 31 December

494.8

570.4

Number of shares (million)

527.6

555.7

Net asset value per share (pence)

93.79

102.65

Details of the Company’s income can be found in the Statement of Comprehensive Income and supporting notes.

Ongoing charges

The ongoing charges ratio (“OCR”) is a measure, expressed as a percentage of average net assets, of the regular, recurring annual costs of running the Company. It has been calculated and disclosed in accordance with the AIC methodology, as annualised ongoing charges (i.e. excluding acquisition costs and other non-recurring items) divided by the average published undiluted Net Asset Value in the year. For the year ended 31 December 2025, the ratio was 1.22% (2024: 1.21%).

Debt

ORIT continues to actively manage its capital structure in line with its disciplined approach to capital allocation. During the year, £100 million of borrowings were refinanced into a lower-cost facility, reducing the Company’s blended cost of debt from 4.0% to 3.3%. Disposal proceeds and portfolio cash generation were used to fund repayments across the Group’s revolving credit and project-level debt facilities. Despite the reduction in absolute debt, gearing was broadly unchanged as NAV and GAV also declined over the year.

Table 17: Debt summary

2025

2024

Debt as % GAV

45%

45%

% hedged

75%

62%

Average cost of debt

3.3%

4.0%

Average remaining term

10

10

Dividends

During the year, interim dividends totalling £33.3 million were paid (2024: £33.5 million), equivalent to 6.13p per share. Post year end, a further interim dividend of 1.55p per share was paid on 27 February 2026 in respect of the quarter ending 31 December 2025 to shareholders recorded on the register on 13 February 2026. Consequently, dividends totalling £33.0 million have been paid in respect of the year under review. These dividends are fully covered from the operational cash flows of the underlying portfolios.

During 2025, the Company’s net cash flows from operations, of £61.3million pre scheduled debt amortisation, and £37.7 million post scheduled debt amortisation supported the payment of £33.0 million dividends to shareholders for the period, resulting in a dividend coverage of 1.86x and 1.14x respectively.

ORIT’s key portfolio characteristics of diversification, high proportion of fixed revenues and inflation-linkage help maintain a growing, covered dividend.

Following the year-end, in line with the Company’s progressive dividend policy, ORIT announced a further increase in the target dividend to 6.23p1 per ordinary share for the financial year from 1 January 2026 to 31 December 2026. This increase of 1.0% over FY 2025’s dividend target continues the Company’s progressive dividend policy, marking the sixth consecutive year the Company has increased its dividend target. The FY 2026 dividend target is expected to be fully covered by cash flow generated from the Company’s operating portfolios.

1 The dividend target is a target only and not a profit forecast. There can be no assurance that this target will be met, or that the Company will make any distributions at all and it should not be taken as an indication of the Company’s expected future results. The Company’s actual returns will depend upon a number of factors, including but not limited to the Company’s net income and level of ongoing charges. Accordingly, potential investors should not place any reliance on this target and should decide for themselves whether or not the target dividend is reasonable or achievable. Investors should note that references in this announcement to “dividends” and “distributions” are intended to cover both dividend income and income which is designated as an interest distribution for UK tax purposes and therefore subject to the interest streaming regime applicable to investment trusts.

Portfolio Valuation

£495mNet asset value(31 December 2024: £570m)

93.8pNAVper ordinary share(31 December 2024: 102.6p)

£897mGross asset value(31 December 2024: £1,029m)

£908mTotal value of all investments(31 December 2024: £1,029m)

The portfolio of assets is valued quarterly using a discounted cash flow (DCF) approach for operational assets, consistent with the International Private Equity Valuation Guidelines. Developer and early-stage investments are valued at cost or recent price of investment, with adjustments for material changes such as milestone outcomes, further investment rounds or other development that reflect progress or risks. The Company’s NAV therefore reflects movements in market power prices, inflation, discount rates, asset performance, contracted revenues, and development progress across the year.

Including the Company’s and its intermediate holding companies’ net liabilities (which mostly comprise Holding Company debt and cash), the total NAV as at 31 December 2025 is £494.8 million or 93.8 pence per Ordinary Share.

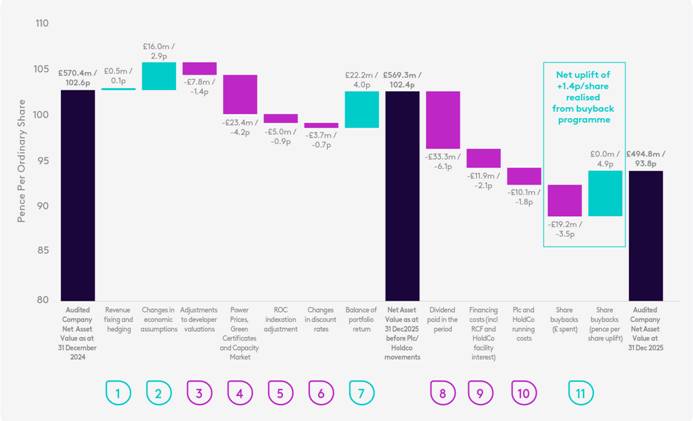

Figure 19: Plc NAV bridge

Movements in the fair value of the underlying portfolio of assets

1 Revenue fixing and hedging £0.5 million (+0.1p per share)

Additional revenue fixing during the year reduced merchant exposure and strengthened near-term cash flow visibility. The year saw ~100% hedging of Otso’s 2026 production and full hedging of UK ROC solar assets for April 2027-March 2028, both secured at attractive pricing relative to market forwards.

2 Changes in economic assumptions £16.0 million (+2.9p per share)

Movements in inflation, foreign exchange and tax produced a net uplift over the year. Higher short-term UK inflation supported inflation-linked revenue, while the weakening of sterling against the euro contributed to valuation gains that were partly offset by hedging. Finnish corporate tax reductions provide a small structural benefit.

3 Adjustments to developer valuations -£7.8 million (-1.4p per share)

For valuation purposes, the following platforms generated material adjustments during the year:

• Norgen: uplift following pipeline consolidation, improved visibility on RTB timing and progress across several priority projects;

• Simply Blue Group: write-down reflecting delays in offshore wind development, liquidity constraints and continued weakness in floating wind markets; and

• Conservative discounts applied to deferred consideration on sales of developer investments, reflecting time value and remaining uncertainty on delivery of milestones – these discounts are expected to unwind as milestones are achieved.

4 Power prices, green certificates and capacity market -£23.4 million (-4.2p per share)

Updating market revenue forecasts resulted in a net valuation reduction, driven mainly by more conservative long-term power price and Green Certificate assumptions, particularly in the UK.

• Power prices – Short-term forward prices fell marginally across ORIT’s core markets as lower gas prices and system fundamentals fed through to 2026-27 curves. Longer-term external consultant forecasts also reduced with adjustments reflecting updated expectations for renewable build-out, demand growth and commodity trends.

• Green Certificates – a negative movement followed the adoption of more conservative long-term green certificate curve more aligned with market pricing.

• Capacity Markets – updated forecasts reflected recent auction outcomes and updates to external long-term assumptions, with only minor valuation impact.

5 ROC indexation adjustment -£5.0 million (-0.9p per share)

The valuation reflects a £5.0 million reduction arising from the outcome of the UK Government’s consultation on the indexation of Renewables Obligation Certificates (“ROCs”), published on 28 January 2026. The Government confirmed that it will adopt option 1, switching indexation of the ROC buyout price from the Retail Price Index (“RPI”) to the Consumer Price Index (“CPI”) effective March 2026. ORIT has therefore reflected the full impact of this change on its NAV as at 31 December 2025.

6 Discount rates -£3.7 million (-0.7p per share)

The weighted average discount rate increased slightly during the year, reflecting elevated long-term interest rates and changes to the portfolio mix following asset sales in the year. Assumptions remain in line with market evidence for contracted renewables. Further information can be found on page 43.

Movements in the fair value of the Plc and holding companies

7 Balance of portfolio return £22.2 million (+4.0p per share)

The expected return on the portfolio of assets represented by the unwind of discounting contributed positively as future cash flows moved closer, but this was partially offset by lower-than-expected operational generation, especially weaker wind resource and uncompensated curtailment in Ireland, as well as updated near-term opex and capex assumptions.

8 Dividends paid -£33.3 million (-6.13p per share)

Dividends totalling £33.3 million in respect of Q4 2024 to Q3 2025 were paid during the 12-month period to 31 December 2025.

9 Financing costs -£11.9 million (-2.1p per share)

Financing costs (incl. RCF and HoldCo facility interest) reduced NAV. Repayment and refinancing into lower-cost facilities reduced RCF utilisation and lowered overall finance costs compared with the prior year.

10 Running costs (plc & HoldCo) -£10.1 million (-1.8p per share)

Management fees and corporate costs at the plc and HoldCo level.

11 Share buybacks -£19.2 million (+1.4p per share)

Share repurchases at a significant discount to NAV were accretive for shareholders on a pence per Ordinary Share basis.

Key valuation assumptions

See below a summary of the key inputs that drive ORIT’s portfolio value

Long-term inflation

Taxation

UK

2.25%1

=

25.0%

=

France

2.00%

=

25.0%

=

Ireland

2.00%

=

12.5%

=

Finland

2.00%

=

18.0%2

↓

Germany

2.00%

=

15.8%

=

↑ Positive change to valuation assumption

= No change

↓ Negative change to valuation assumption

Power price forecasts

Where not fixed under PPAs or hedged, we use forward market prices in the near term before transitioning to a blend of two independent consultants’ long-term forecasts. Capture prices are updated regularly to reflect cannibalisation effects. For solar, we apply generic country-level capture prices, while for wind we reflect site-specific curves to account for greater variation in output and pricing.

Asset lives and decommissioning

Operational lives are assessed on an asset-by-asset basis, taking into account lease terms, planning consents, extension rights and technical performance. We also include decommissioning and land restoration costs as end-of-life outflows, ensuring valuations capture the full lifecycle economics of each project. The valuations do not include any terminal value, despite the potential opportunity for repowering.

1 UK RPI (annual average): 4.0% during 2025, 3.25% to 2029 and then 2.25% from 2030 onwards. The RPI forecasts for 2026 to 2029 were revised upwards during the period from 3.0% to 3.25%.

2 Valuation movement reflects a planned reduction in Finland’s corporation tax rate from 20% to 18%, effective from 2027.

Discount rates

A range of discount rates are applied in calculating the fair value of the investments, reflecting factors such as the location, technology and lifecycle stage of each asset, as well as capital structure and the split of fixed and variable revenues.

As at 31 December 2025, the weighted average discount rate (“WADR”) implied by ORIT’s portfolio valuations was 7.8%, compared with 7.9% as at 30 June 2025. The marginal decrease over the second half of the year reflects portfolio composition changes following asset disposals and asset-specific adjustments, partly offset by updates to Renewables Obligation indexation assumptions.

The WADR does not include the expected return associated with development-stage assets or additional Company-level leverage. Including these elements results in an adjusted average discount rate of 8.2% as at 31 December 2025.

Table 20: Discount rate summary

31 December

30June

31 December

2025

2025

2024

UK Assets

Levered IRR (GBP)

8.1%

8.4%

7.6%

Gross Asset Value (GAV) (£m)

351

467

460

Asset Leverage %GAV

18%

35%

16%

European Assets

Levered IRR (GBP)

7.0%

7.5%

7.2%

Levered IRR (EUR)

6.5%

6.9%

6.6%

Gross Asset Value (GAV) (£m)

546

544

569

Asset Leverage %GAV

41%

43%

42%

Total Portfolio

Levered IRR (GBP)

7.8%

7.9%

7.4%

Levered IRR (local currency)

7.3%

7.5%

7.0%

Gross Asset Value (GAV) (£m)

897

1010

1029

Total Leverage %GAV

45%

47%

45%

Weighted average discount rate as at 31 December 2025

7.8%

(i) Return expected on the Company’s investments into development stage assets

0.3%

(ii) Increase in return associated with the additional leverage from the RCF

0.1%

Adjusted average discount rate as at 31 December 2025

8.2%

Portfolio valuation sensitivities

Details of these can be found in the notes to the financial statements on pages 106 to 108, but are summarised in Figure 21 below.

Figure 21: NAV sensitivities per ordinary share (see page 44 of the annual report)

Risk Management

Risk appetite and risk management

The Board determines the Company’s risk appetite in accordance with the Investment Policy, which sets clear boundaries around the types and levels of risk the Company is willing to accept to meet its investment objectives.