Top Wall Street exec warns of 1929-style crash – but only after massive gains in the short term

Story by Isabel Keane

A top Wall Street executive is warning of a 1929-style crash, where the stock market will go up significantly before crashing catastrophically, just as it had at the start of the Great Depression.

Mark Spitznagel, the hedge fund manager behind Universa Investments who made $1 billion in a single day for his clients during the 2015 “Flash Crash,” says he is seeing similarities to 1929, the year of the Wall Street crash, he told the Wall Street Journal

Spitznagel, a protege of “Black Swan” author Nassim Nicholas Taleb, is known for hedging tail risks, or strategies that lose some money most of the time but earn big when the market collapses.

“I’m the crash guy — I remain the crash guy,” Spitznagel told the Journal.

Spitznagel is warning individual investors against making hasty changes to their portfolios, noting those who can’t buy tail-risk protection will still make positive returns in the long run if they don’t sell.

“The biggest risk to investors isn’t the market – it’s themselves,” he said.

Spitznagel sees a strong rally ahead, with short-term gains potentially pushing the S&P stock index up to as high as 8,000 points, a 20 percent gain from today’s level, according to the report.

However, he expects the rally to eventually lead to a big, 1929-style crash, meaning there would be a large and potentially catastrophic downturn following the gains.

Spitznagel believes this, in part, because every time the market or economy runs into trouble, the Federal Reserve steps in to save it with moves such as low interest rates or bailouts.

If a major sellout is looming, as Spitznagel says, large gains now would not be out of the norm, according to the report. Since 1980, the S&P 500 has returned 26 percent annualized in the 12 months preceding the start of a bear market, or a sustained market downturn.

The last 12 months’ rally has been twice as high as that average ahead of the 1929 peak, according to the report.

Both individual and professional investors typically increase their stocks during times like today, according to the report. Strategists at State Street said that institutional investors’ exposure to equities has reached its highest since November 2007, just before a vicious bear market.

“The markets are perverse,” Spitznagel told the outlet. “They exist to screw people.”

Whilst no dividend is one hundred percent secure, there are a few checks you can take before you risk your hard earned.

Let’s use SUPR as the working example

Dividend History

A progressive dividend

A hold or a small reduction is acceptable, subject to the yield available.

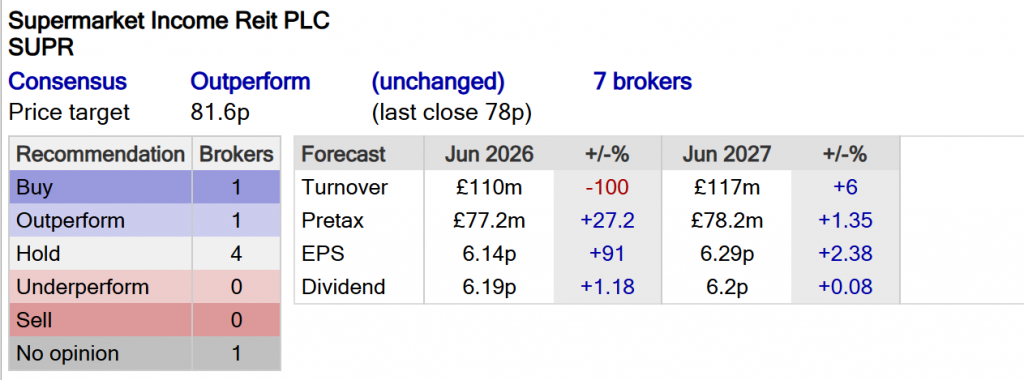

Broker Targets

Does anyone agree with your analysis ?

What does the company say

The Company’s properties earn long-dated, secure, inflation-linked, growing rental income. SUPR targets a progressive dividend and the potential for long term capital growth.

17/09/25

Your duty

To check when the next dividend is announced around the beginning of October.

Target

Current yield. On a 10k investment you should earn £785, gently increasing.

You can re-invest your dividends either back into SUPR or another high yielder.

In roughly ten years you should have received all your capital back as income and as long as the company isn’t taken over and keeps paying a dividend you will have achieved the holy grail of investing of having a company that pays you income at a cost of zero, zilch, nothing.

Not only that you should have another position paying you dividends.

Investing.com — Goldman Sachs has raised its S&P 500 forecasts, saying robust earnings growth should drive further gains even as valuations remain elevated.

The bank now expects the index to reach 6800 by year-end, 7000 in six months, and 7200 over the next 12 months, implying returns of 2%, 5%, and 8% respectively from current levels. The revision reflects Goldman rolling forward its 3-, 6- and 12-month return forecasts.

Earnings growth is seen as the key driver. Goldman projects S&P 500 EPS to rise 7% in both 2025 and 2026, with earnings accounting for the majority of this year’s 14% total return.

The bank said EPS growth has contributed 55% of returns so far in 2025, compared with 37% from valuation expansion and 8% from dividends.

“With long-term interest rates relatively stable, earnings should remain the primary driver of equity upside going forward,” strategists led by David Kostin said in a note.

The upgrade comes after the Federal Reserve delivered its first rate cut since 2024, lowering the funds rate by 25 basis points. Goldman’s economists expect two more cuts this year and two more in 2026, leaving the terminal rate at 3–3.25%.

While the policy shift has helped valuations expand, the Wall Street bank sees current multiples as broadly fair, with real 10-year Treasury yields unlikely to fall much further without a deterioration in the economic outlook.

Investor positioning remains light despite record highs, with Goldman’s Sentiment Indicator at -0.3. The bank said this adds to the near-term upside case if the macro backdrop stays supportive.

Historical trends also reinforce the view, as the S&P 500 delivered median six-month and 12-month returns of 8% and 15%, respectively, in past cutting cycles where growth continued.

Goldman highlights that Information Technology and Consumer Discretionary sectors have historically led in similar environments, while high-growth and high-volatility stocks tend to outperform.

Rate-sensitive trades, however, may fade, with the bank preferring exposure to firms carrying high floating-rate debt, which directly benefits from lower borrowing costs.

Overall, Goldman expects U.S. equities to extend gains, supported by steady growth, accommodative Fed policy, and earnings momentum.

“An accommodative Fed and an economy that accelerates into 2026 should allow the market to maintain its current multiple,” the strategists said.

Dividend investing has been a fantastic wealth-creating and learning experience for me.

However, I have my fair share of regrets as well.

I detail 7 of my biggest regrets from my dividend investing journey.

tolgart/iStock via Getty Images

I love pursuing a blend of dividend growth investing, high-yield investing, and value investing. This is because I believe that high-yield stocks are the easiest to value accurately, given that long-term growth is one of the hardest things to project in a company. Businesses that are not big growth companies but instead deliver the vast majority of their returns via dividend payments are the closest things to bonds in terms of value, which inherently are much easier to assess.

Then the question simply becomes a matter of whether they can sustain their dividend payout, generate a little bit of growth as equities, and beyond that, capture valuation-multiple expansion and use market volatility to your advantage. Insisting on some dividend growth also helps drive capital appreciation as well as provide an income stream that can keep up with inflation over time.

Finally, value investing is extremely important, especially when dealing with slower-growth, higher-yielding stocks, because if you do not buy on a value basis, you are unlikely to get attractive total returns. When a company is growing very slowly, it is rare that the market gets irrationally exuberant about it. While this approach has served me very well and has enabled me to outperform the S&P 500 (SPY) and the Schwab U.S. Dividend Equity ETF (SCHD) over time, I have had my fair share of regrets along the way. In this article, I will detail seven of my biggest regrets in my dividend investing journey.

Regret 1

One of the biggest regrets is not paying proper attention to the balance sheet of the company. When investing in dividend stocks, especially high-yield dividend stocks, it is tempting to simply look at payout ratio, and if the payout ratio is low, it is tempting to think that the dividend is very safe, even if other aspects of the business, such as its balance sheet, are on questionable footing. The thought goes that even if the business suffers a bit, it has such a large cash flow buffer that it is unlikely to cut the dividend. In fact, many times, management will reiterate that the dividend is a top priority for them, even if their balance sheet is running into trouble.

I learned this the hard way with companies like Algonquin Power & Utilities (AQN), Lumen Technologies (LUMN), and NextEra Energy Partners (XIFR), as all three were stocks where their dividends were fully covered by cash flows, and management repeatedly emphasized to investors that their dividend was extremely important to them as part of their capital allocation strategy. However, in all three cases, their balance sheets were in very bad shape, ultimately forcing them to cut dividends several times, in the case of AQN, and outright eliminate them in the case of LUMN and NEP. Fortunately, in the case of LUMN and NEP, I sold well ahead of the dividend cut and avoided major losses, but in the case of AQN, I did not, and I got burned badly.

Regret 2

Another important lesson is the durability and defensiveness of the business model. A classic example was the Class A and C mall REITs like CBL Properties (CBL), Washington Prime Group (WPG), and Pennsylvania REIT (PEI) in the lead-up to COVID-19. All those businesses had significant dividend coverage ratios, what appeared to be considerable cash flow visibility, and even pretty strong balance sheets for mall REITs. However, their businesses were not durable, as they were disrupted by e-commerce, leading to many of their assets entering into death spirals that ultimately overwhelmed them and forced them into bankruptcy. Fortunately, I did not get burned, but I was tempted to dip my toe in several times. Instead, Class A mall REITs like Simon Property Group (SPG), which had much higher quality and better-located assets along with a stellar balance sheet, weathered the storm and survived.

Another example of a business that had a fairly durable model but was not defensive enough to sustain its dividend was Hanesbrands (HBI). It had a very low payout ratio and seemed like a bargain, but its business was cyclical, and it got hit by a perfect storm of macro headwinds and a cyberattack that forced it to eliminate its dividend. Dow Inc. (DOW) is another example, as it had a decent balance sheet and good dividend coverage but was hit by a long industry downturn, forcing it to slash its dividend. I avoided getting burned by that one, though I hold industry peer LyondellBasell (LYB), which has held up better and even continued to grow its dividend, though its payout is on increasingly shaky ground, and I expect a cut if the industry does not turn around soon.

Regret 3

A third regret is chasing yield. Sometimes the dividend coverage looks comfortable, the balance sheet appears solid, and the business model looks quality, but the yield is still unusually high. The market rarely gives away high yields without reason. Where there is smoke, there is often fire. An example of this right now is United Parcel Service (UPS). While UPS insists its dividend is rock solid, with a strong balance sheet and clear moat, it faces a challenging turnaround, uncertainty from tariffs, and shifting trade flows. It may work out, but I believe chasing it now is too much like yield-chasing rather than sound fundamental investing.

Regret 4

A fourth regret is underestimating the importance of dividend growth. It is tempting to think that a stock with a high yield does not need much dividend growth. However, the power of compounding works best when yield and growth work together. High yield provides a floor for the stock price, while growth protects the dividend, the balance sheet, and the business model. Whirlpool (WHR) and Leggett & Platt (LEG) are examples of stocks that had too much dependence on dividend growth but eventually cut payouts. On the flip side, mortgage REITs (MORT) like Arbor Realty Trust (ABR) and Annaly Capital (NLY), as well as business development companies like FS KKR Capital (FSK), lure investors with sky-high yields but cannot grow dividends much at all due to paying out nearly all earnings, while being highly interest-rate sensitive and dependent on financial engineering. Covered call ETFs like the JPMorgan Nasdaq Equity Premium Income ETF (JEPQ) also look attractive with high yields but have limited growth due to capped upside from selling calls.

Regret 5

A fifth regret is not fully understanding what type of dividend stock I was investing in. Cyclicals require careful timing, strong balance sheets, and should not be held forever. Stalwarts are my bread and butter, providing higher yields and more sustainability, though with slower growth. Long-term compounders, like Apple (AAPL), Microsoft (MSFT), Blackstone (BX), and Brookfield Asset Management (BAM), are innovators that continually extend growth runways. These are the ones I am least likely to sell, as they deliver the compounding power that drives long-term wealth.

Regret 6

Another regret I have is over-weighting a single sector. It is easy to become overconfident that a single sector has everything going for it, and while that may be true in the short term, unforeseen circumstances can torpedo investment theses. For example, I was very bullish on midstream (AMLP) heading into COVID and ended up getting hit quite hard initially because energy prices collapsed, and with them, the prices of many of my investments. My conviction did not waver, and I doubled down, ultimately making all the money back and much more coming out of COVID. That being said, while I like midstream stocks such as MPLX (MPLX), Energy Transfer (ET), and Enterprise Products Partners (EPD), and believe that they check my boxes for what makes an ideal investment, it is still important to maintain proper diversification so that if such an event happens again, I am not overexposed and suffering massive losses in a short period of time.

Regret 7

Last but not least, one of my regrets is not being suspicious enough about a stock. If the investment story looks great and everything seems to check out, I still need to remain highly suspicious. This harkens back to not chasing yield as well as not being overweight in a single sector, but it is also a broader principle for investing. The reality is that Mr. Market is often wrong, but he is never stupid. That means there is always a good reason for how he prices a stock, and it is important to identify what the bear case is for any stock before buying it.

Investor Takeaway

High-yield investing is a great way to combine the best qualities of dividend growth investing and value investing and has helped me to achieve significant long-term total return outperformance

The ‘4pc rule’ on pension withdrawals can be broken with the right investments

Ed Monk

If there’s a superstar in the world of retirement planning, it’s William Bengen. His “4pc rule” has helped countless people avoid running out of money in retirement.

Mr Bengen, an American financial planner, conducted a detailed analysis of a huge number of hypothetical retirement scenarios in a range of economic circumstances to arrive at his rule.

He found that even investors who retired at the worst possible time would be able to fund a 30-year retirement if they limited withdrawals to 4pc of their savings in the first year of retirement and increased them in line with inflation thereafter.

Some would be able to withdraw more each year, fund a retirement longer than 30 years or even leave at death a large sum to pass on to their children.

In the three decades since he published his original research, Mr Bengen has continued to refine his rule as further data was released, enabling him to improve his analysis. Much like Mr Bengen, those applying his rule should keep an eye on the markets and inflation to ensure their plan remains sustainable.

Here, Telegraph Money explains how to use it:

How much of your pension fund can you safely withdraw?

The rule is simple: if a retiree were to withdraw 4pc of their pension pot in the first year of their retirement and then increase withdrawals by the annual rate of inflation, their pension pot would last them no less than 30 years.

He modelled his rule from 1926 onwards, meaning that even accounting for “worst case scenarios”, such as the Wall Street Crash and Great Depression, the pot would not run out.

But with a further 31 years of refinement, Mr Bengen has discovered that savers can afford to increase their withdrawals if they plan appropriately.

Years after creating the ‘4pc rule’, William Bengen discovered that savers can afford to increase withdrawals with planning Credit: Supplied

His research relates to American investors, but the broad principles also should apply to the UK.

It states that if a pension pot is invested 50-50 between large-cap US stocks and US Treasuries, a saver can draw down their pot starting at 4pc. However, if they add a broader range of assets, including international stocks and smaller US companies, they can safely increase their withdrawals to 4.7pc of the initial pension pot.

pension drawdown

How to manage falling markets

If you do plan to fund retirement from a pot of money invested partly in shares, your biggest fear may be a bear market. After all, pension providers allow you to look up the value of your pot every day, and in a bear market, that value will be falling, perhaps dramatically. In those circumstances, it may well feel reckless not only to maintain your withdrawals at a predetermined rate, but to increase them every year in line with inflation.

Advertisement

But when Mr Bengen looked at the figures, he found that the tendency of markets to recover was enough to prevent permanent damage to retirement income from a bear market in the early years of retirement, even at initial withdrawal rates as high as 7.2pc.

In a research paper commissioned by Fidelity International, he said: “Although bear markets can have painful effects on portfolios in the short term, they are usually followed by recoveries, which enable the portfolio to regain its former value and then some.

“The lesson here is that in the event of a ‘normal’ bear market in stocks, taking no action [i.e. maintaining withdrawals in line with the plan] might be the best strategy.”

He did, however, warn that this reassuring conclusion might not apply to particularly severe bear markets.

Recommended

How to manage inflation

Rather than bear markets, what retired investors should really fear is a severe or prolonged bout of inflation, Mr Bengen said. When he modelled the effects of such an inflationary period – specifically, 4.6pc in the first year of retirement and rising to 10.2pc in the seventh year, before a slow decline – for a saver who started with a withdrawal rate of 5.5pc, he found that the saver could not afford to just carry on with the planned withdrawals.

Doing that would result in the withdrawals quickly becoming unsustainable, putting the saver on course to run out of money well before 30 years had passed. In this scenario, what Mr Bengen called a “draconian” 28pc cut in withdrawals in the sixth year would be required to restore the plan’s sustainability.

He added: “How many of us could contemplate a 28pc reduction in withdrawals from our retirement accounts in mid-retirement?

“For many, it would be a severe blow. And, even given this harsh reduction, we can’t be sure it will be sufficient if inflation persists at a high level.

“This underscores the observation that inflation is the greatest threat to the lifestyles of retirees.”

We should emphasise that if the saver had instead stuck to the original 4pc rule and not opted for first-year withdrawals of 5.5pc, all would have been well.

Mr Bengen concluded: “A retirement withdrawal plan requires active management. Adjustments may have to be made during retirement, although not all deviations from the plan require immediate action.

“Bear markets come and go, and many can be safely ignored. However, high, sustained inflation may be the justification for panic.”

Recommended

When to reduce withdrawal rates

Mr Bengen’s method for reassessing withdrawal rates might require a moment to understand but is simple in principle.

It involves the calculation at the start of retirement of what each year’s withdrawals will be as a percentage of the theoretical value of the pot each year, assuming steady inflation and investment growth at historically average rates.

You then compare, as retirement progresses, that hypothetical withdrawal rate with the actual one. The actual figure, calculated each year, is your actual withdrawal, in pounds, divided by the actual value of the pot at the beginning of that year.

The two withdrawal rates – the hypothetical and the actual – are bound to differ because variations in inflation will affect the amount you withdraw each year, while the value of the pot will, in practice, fluctuate from year to year in line with the financial markets.

It is this difference between the hypothetical and the actual withdrawal rates that you need to pay attention to. Small, brief gaps are nothing to worry about, but a wide and prolonged gap is a sign that withdrawals may be unsustainable.

Ed Monk is an investment writer at Fidelity International. Mr Bengen’s new book, A Richer Retirement: Supercharging the 4pc Rule to Spend More and Enjoy More, analyses more withdrawal scenarios.

Heya are using WordPress for your site platform? I’m new to the blog world but I’m trying to get started and create my own. Do you need any html coding expertise to make your own blog? Any help would be really appreciated! https://keslaser.com.ua/vodinnya-v-doshch-i-tuman-yake-svitlo.htm

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

The content of this article is provided for information purposes only and is not intended to be, nor does it constitute, any form of personal advice.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Turning excess savings into a second income can be a very good idea. Even for someone starting from scratch, it’s possible to earn some good returns with enough time.

As things stand, someone in the UK aged 30 has 38 years before becoming eligible for the State Pension. And that’s a long time to build up an investment portfolio.

Should you buy Supermarket Income REIT plc shares today?

Property

Historically, property has been a very good source of extra income for UK investors. But higher taxes and greater regulation have made things more complicated in recent years.

Enter real estate investment trusts (REITs). These are companies that own and lease properties (which might be hospitals, offices, warehouses, or other buildings) to tenants.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

In exchange for tax exemptions, REITs return 90% of their income to shareholders as dividends. And this gives investors a different way to earn income by investing in property.

There’s been a lot of interest in the UK REIT sector recently in terms of takeovers and acquisitions. But I think there are still some opportunities that are worth checking out.

Supermarkets

When it comes to leasing buildings, supermarkets probably aren’t the first type of property that people think of. But Supermarket Income REIT (LSE:SUPR) is worth a closer look.

As its name suggests, the company leases a portfolio of around 55 supermarkets across the UK. And its largest tenants include Aldi and Lidl as well as Tesco and Sainsbury.

The nature of the grocery market means the firm’s tenant base is relatively concentrated. While its rent collection metrics are impressive, investors shouldn’t overlook this risk.

A 7.85% dividend yield, however, goes some way to offsetting the risk. And investing regularly at that rate of return for 38 years can have some impressive results.

Regular investing

Investing £100 each month for 38 years and earning a 7.85% annual return results in a portfolio that generates £19,293 a year. Starting from nothing, I think that’s a strong result.

The situation with Supermarket Income REIT might be even better. Since the majority of its leases are linked to inflation, investors might expect an extra 2% in annual rent increases.

There is, however, no guarantee the stock will trade with a 7.85% dividend yield every month for the next 38 years. If the share price rises, the equation could look very different.

In that case, investors aiming to turn £100 a month into something that eventually returns £19,293 a year would need to look elsewhere. But that might not be such a bad thing.

Diversification

One of the benefits of regular investing is it allows for gradual diversification. Over time, different stocks come in and out of fashion for various reasons.

Buying each month should give an investor a chance to take advantage of different opportunities as they present themselves. And this creates a diversified portfolio over time.

For someone starting from scratch, buying shares and reinvesting dividends could be a good long-term strategy. And I think REITs are a good place to start looking for opportunities.

Investing £100 monthly for 38 years at a 7.85% annual return builds into something quite powerful thanks to compound interest. Let’s break it down: 📈 Investment Summary

Monthly contribution: £100

Duration: 38 years

Annual return: 7.85% (compounded monthly) 💰 Final Value Estimate Using monthly compounding, your investment would grow to approximately: £291,000