City of London

Disclaimer

Disclosure – Non-Independent Marketing Communication

This is a non-independent marketing communication commissioned by City of London. The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

CTY appears well-set to continue to deliver on its objectives…

Overview

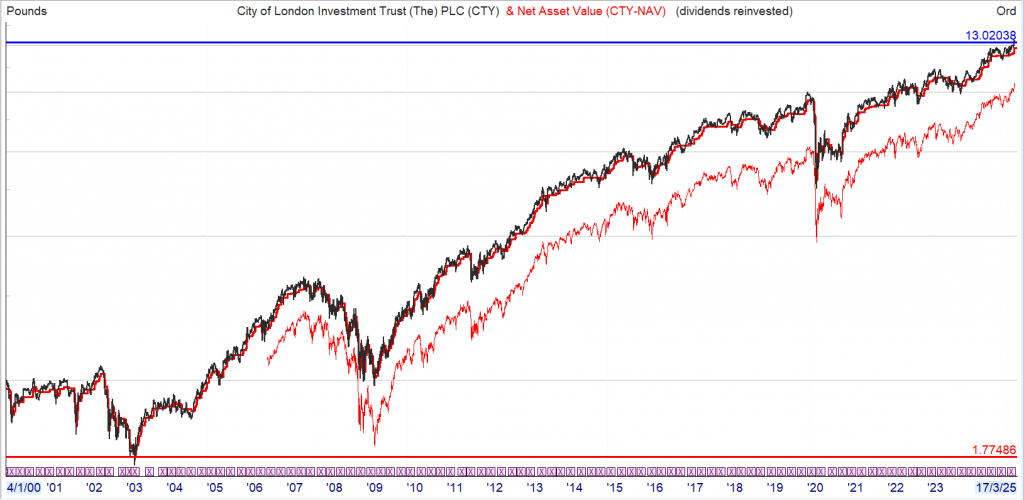

City of London Investment Trust (CTY) aims to deliver income and capital growth through a cautious investment strategy that is typically focussed on larger UK-listed equities. Job Curtis has been the trust’s manager over the past 33 years, a tenure that gives him huge experience with which to navigate markets and economic cycles.

It is his success in delivering steady outperformance over the long term, as well as CTY’s unrivalled track record of delivering successive dividend increases for 58 years, that has allowed the trust to build a strong following amongst investors, enabling it to grow and benefit from economies of scale. The most recent OCF is 0.37%, which makes CTY highly competitive.

With a mix of higher yielding stocks as well as lower yielders that have higher growth potential, Job remains convinced of the quality and attractive valuations of the companies in the CTY portfolio. It is this backdrop that has led Job to gently increase Gearing to c. 8% currently.

As at 31/01/2025 CTY’s NAV had outperformed the benchmark over one, three and five years. As we discuss in the Portfolio section, the strong track record comes not from any investment heroics, but in our view is more a result of Job’s risk-averse approach to stock picking. Job likes to ensure that CTY is always exposed to a broad spread of investments, which is complemented by Job’s valuation-based investment framework, focussed on quality companies but sometimes with a contrarian tilt. Generally, capital invested in each company corresponds not only to Job’s estimation of the share price relative to fair value, but also his confidence in the quality and future trajectory of the dividend.

Analyst’s View

CTY is the biggest and cheapest trust of its peer group, with the longest track record of dividend increases (of any trust): in every sense the superlative of the UK Equity Income sector. The dividend yield is currently 4.7%, well ahead of the benchmark and peer group average, and the board’s clear focus on discount control means that historically the share price has closely reflected the characteristics of the NAV – something that can’t be said of some investment trusts. Additionally, low-cost long-term gearing should confer a steady advantage to the trust over many years to come. As such, in our view CTY continues to be advantageously set up to deliver on its income and capital growth objectives for shareholders.

These attractive characteristics have not been missed by investors, and over the past ten years CTY has issued shares at a premium to NAV, boosting returns for existing shareholders and leading to economies of scale and a progressively lower OCF. Indeed, over the decade to 30 June 2024, the share count has increased by a total of c. 76%. However, over much of 2024 and so far in 2025, CTY’s shares have traded at a small discount in absolute terms, a symptom of negative market sentiment towards the UK. In our view, for long-term investors wishing to take advantage of the inevitable cyclicality of sentiment, CTY is worthy of consideration. Indeed, as the chairman observes in the recently announced interim report, the dividend yield of 4.7% Portfolio section means shareholders are “paid to hold on” until the UK sees a change in sentiment, and potentially an improvement in valuations.

Bull

- Very low OCF of 0.37%

- Consistency and experience of manager who has delivered long-term outperformance of the FTSE All-Share Index in capital and income terms

- Track record of 58 years of progressive dividend increases

Bear

- Cautious approach means that NAV can underperform in some market conditions

- Income track record highly attractive, so manager might risk long-term capital growth in trying to maintain it

- Structural gearing can exacerbate the downside

££££££££££££££££££

GEARING

The company borrows money at x and re-invests hoping to make xx. In a rising market it’s a positive but in a falling market it’s a negative.

Either way u receive and enhanced dividend.

Leave a Reply