The number of investment companies hitting 52-week high discounts reached double digits last week – the first time that’s happened in over three months. But which sector contributed a third of the names on the list?

By Frank Buhagiar

We estimate there to be 12 investment companies that saw their share prices trade at 52-week high discounts over the course of the week ended Friday 13 September 2024 – three more than the previous week’s nine.

Four of this week’s 12 herald from the renewables sector. It has been a while since that happened. Back in Q1 2024, renewable investment companies were regular contributors to the 52-week high discount list. That was when the higher-for-longer interest rate narrative dominated market sentiment – as well as making financing more expensive, higher interest rates lead to higher discounts rates which are used to value a company’s assets. Higher discount rates equal lower valuations.

So, with interest rates now coming down in the UK and Europe and with the first cut expected possibly this week in the U.S. why the sudden jump in renewable 52-week high discounters? Might be down to news this week from Aquila European Renewables (AERS) that its long-running strategic review failed to find a buyer willing to pay an acceptable price for the company. AERS will now hold a continuation vote at the next AGM which could lead to the fund being wound up.

The AERS news, which was released on 12 September, good for a slight narrowing in the fund’s share price discount. Not for the likes of Atrato Onsite Energy (ROOF), Ecofin US Renewables Infrastructure (RNEW) and HydrogenOne Capital Growth (HGEN) though, the share prices of which all set new year-high discounts the next day. Could it be a size issue? AERS already on the small side with a market cap of £260 million (total assets of over £500 million), so too Gore Street Energy Storage (GSF) on £288 million (total assets of over £500 million), but the other three all have sub-£100 million market caps and total assets of between £100 – £200 million. Are they just too small to register on the radar of larger peers – not big enough to move the needle and all that

And don’t forget it was only on 9 September that RNEW announced its own strategic review had failed to find a buyer for its assets and that it too would be proposing a managed wind down of its own. Looks like some sub-scale funds might just be too small to be of interest to the big players. And if that’s what the market thinks then share prices could lose any potential bid froth they may have once had baked in. Take away any takeover excitement/potential and share prices may well lose a prop and discounts could widen. Now, having just said that, what price a renewables takeover announcement hitting the screens in the next few days to blow this theory out of the water ?

Four investment trusts closed last week. How many more will go?

By: Elliot Gulliver-Needham

Investment Reporter

The number of investment trusts on the market has fallen to new lows.

Last week, four separate investment trusts handed in their notice, announcing they would be shuttering.

Aquila European Renewables, Ecofin US Renewables, Gulf Investment Fund and Keystone Positive Change, all said they would be liquidating, as the number of trusts on the London Stock Exchange continued to dwindle.

The number of investment trusts has fallen to its lowest level in years for a number of reasons, including high discounts, pressure on small trusts, and ongoing issues around cost disclosure.

However, almost all of the trusts last week said they would be closing for a simple reason: Performance.

Why did the investment trusts close?

With a total of ten mergers announced so far this year, far above the four last year and five in 2021 and 2022, more trusts are feeling the need to combine and get big to stay afloat.

What might be more worrying for investors, however, is the events of this week, with funds simply shuttering rather than finding an eligible buyer.

Selling off assets can take years, and ultimately can signal to the market that the trust was never worth backing in the first place.

Three of the trusts that announced they would be pursuing a closure last week have suffered a period of very poor performance, especially the two renewable focused trusts, which had fallen 43 and 11 per cent over the last year.

While Keystone is up more than seven per cent over the last year, it is still down 21.3 per cent over the last five years.

Gulf Investment Fund, which only controls £96m in assets, decided to pursue a wind down due to its small size.

All of the trusts also cited their discounts, which is a problem throughout the sector. Just 26 investment trusts on the market are trading at a premium, with their share prices sitting above the value of their underlying assets.

This is naturally pushing investors to question whether they might get more value by simply selling off the assets of the fund, getting back their full value rather than sitting on an average 14 per cent discount.

However, performance in the sector is picking up. The average trust’s share price is up more than 17 per cent in the last year, or 45 per cent over the last five.

Out of the 366 trusts tracked by the Association of Investment Companies, only 85 funds have seen their share price fall over the last year, with 42 falling by double digits in the time period.

The fact that all of the trusts that are closing have issued below average performance may suggest a winnowing effect for the better, cutting out the funds that have failed to match their peers.

Trust

Share price over last year

Share price discount to underlying assets

Ecofin US Renewables Infrastructure

-43.1 per cent

-45.9 per cent

Aquila European Renewables

-11.21 per cent

-21.9 per cent

Keystone Positive Change

7.8 per cent

-7.1 per cent

Gulf Investment Fund

6.1 per cent

-4.8 per cent

Source: Association of Investment Companies

The news followed four other trusts indicating they would be departing the main market the week before, though three of these were due to being bought out.

Tritax Eurobox and Balanced Commercial Property Trust both received takeover bids, while Aurora announced it would be absorbing fellow trust Artemis Alpha. However, JP Morgan’s Global Core Real Assets did fail its continuation vote, meaning it will also be shuttering.

“On the whole, I feel the rationalisation of the sector is healthy, after all the returns on three of these four funds have undoubtedly disappointed investors,” said James Carthew, head of investment company research at Quoteddata.

“However, I believe that Gulf Investment along with Tritax EuroBox and Balanced Commercial Property Trust… may be missed in time. It would not surprise me if similar vehicles relaunched in a few years.”

Artemis Alpha Trust PLC ex-dividend date Fidelity European Trust PLC ex-dividend date Oakley Capital Investments Ltd ex-dividend date Patria Private Equity Trust PLC ex-dividend date Regional REIT Ltd ex-dividend date Triple Point Energy Transition PLC ex-dividend date Unite Group PLC ex-dividend date

Change of Name to Foresight Environmental Infrastructure Limited

At the Company’s AGM held on Friday 13 September 2024, shareholders voted in favour of the resolution to change the Company’s name to Foresight Environmental Infrastructure Limited (“FGEN”).

As such, the change of name became effective on Monday 16 September 2024.

Further, the Company’s stock market ticker will become “FGEN”, effective as of 08:00 a.m. on Tuesday 17 September 2024. In conjunction, the Company’s website will also change to https://www.fgen.com/

The Company’s ISIN, SEDOL, and CUSIPs will remain unchanged and its Legal Entity Identifier (LEI) remains 213800JWJN54TFBMBI68.

Shareholders should note that their shareholdings will be unaffected by the change of name. Existing share certificates should be retained as they will remain valid for all purposes and no new share certificates will be issued.

The ‘screaming buy’ investment trusts, according to James Calder

16 September 2024

The City Asset Management CIO explains why some areas are now too cheap to ignore.

By Jonathan Jones,

Editor, Trustnet

Investors are “not good” at timing markets, but there is one area that is a “screaming buy”, according to James Calder, chief investment officer at City Asset Management.

He is coming off “the worst two years” of his career, after rising interest rates hammered his portfolio in 2022 and 2023, but is back on the upswing so far in 2024.

“Even during the global financial crisis, it was frightening but central banks did their best to prevent total collapse. They were your friends,” he said.

“In the past couple of years central banks did their best to stamp out inflation but that meant raising interest rates and skirting with recession, which hurt certain areas of the market.”

Yet, with the Bank of England and European Central Bank already embarking on their own interest rate-cutting cycles and the Federal Reserve likely to follow suit this week, things could be turning around for the better.

In particular this could help out unloved areas in the investment trust space that he described as “long-duration hard assets” such as infrastructure and renewable energy.

These trusts are “still on substantial discounts” but should provide investors with “reasonable upside and a decent yield” from here, Calder said. “These all just look incredibly cheap. There is latent value there. They are a screaming buy at this point.”

However, he noted that investors who wish to take advantage should “have a seven-year time horizon” at least, as they will “never call the top or the bottom”.

The selections below offer investors “reasonable upside and a decent yield” based on their current prices.

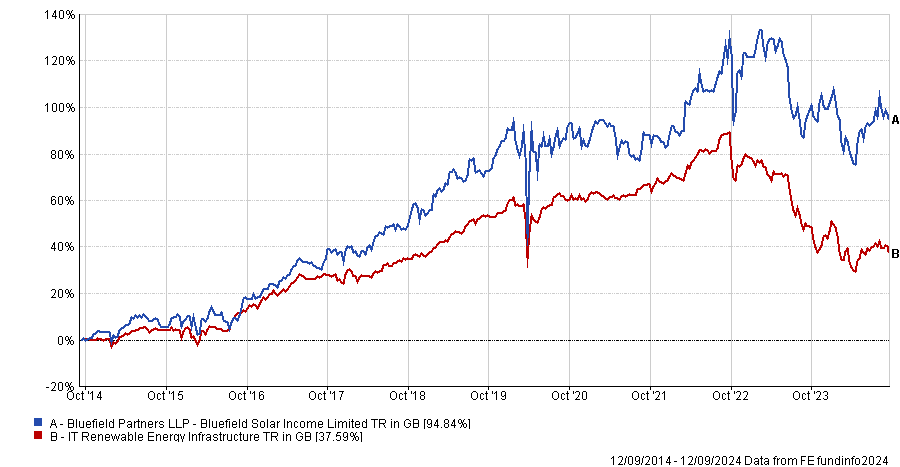

His first choice is in the environmental space, where he likes Bluefield Solar Income. The trust has a market capitalisation of £626m and has been the second-best performer in the 21-strong IT Renewable Energy sector over the past decade. There are only six trusts with a track record that spans that far, however.

It is also second versus 11 peers over five years and is fourth out of 19 in the sector over three years – all top-quartile efforts. It currently yields 8.5% and is on a discount of around 18.6%.

“It doesn’t have a lot of debt and the dividend is covered. Yield is going to provide a big chunk of your returns but the discount should come in as interest rates come down,” said Calder.

Performance of trust vs sector over 10yrs

Source: FE Analytics

Another option could be The Renewables Infrastructure Group, added. The £2.6bn trust is on a 22.7% discount and yields 7%. It has had a strong year, making 4.4% at a time when the IT Renewable Infrastructure peer group has averaged a 7.5% loss, and has consistently been an above-average performer in the sector over three, five and 10 years.

The trust has had an active period, according to Andrew Rees, an associate at Deutsche Numis, who said following the investment company’s interim results last month, it has “made strong progress” on disposing assets with almost £190m of sales at an average 10% premium to book value. It also announced a £50m share buyback programme.

“This remains an attractive entry point for a portfolio that is diversified by both geography and technology managed by an experienced team,” he said.

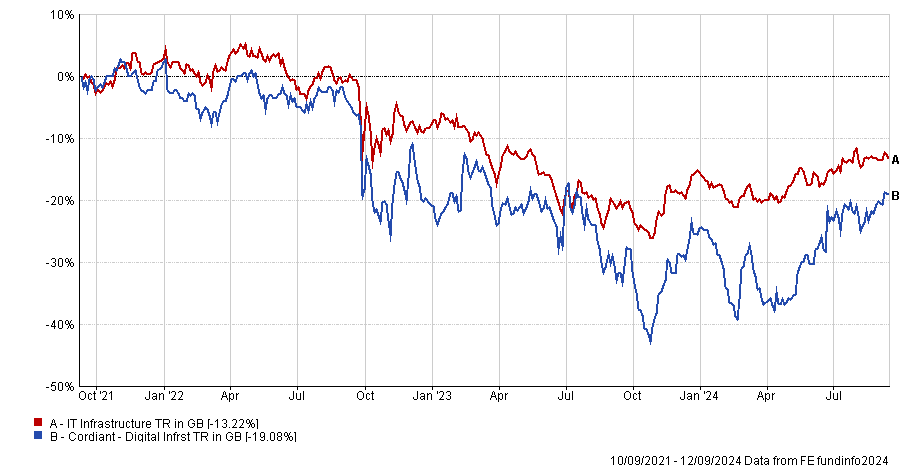

It was one of three infrastructure trusts Calder recommended. Another was Cordiant Digital Infrastructure, a selection he said “might raise some eyebrows”.

The trust invests in mobile towers, data centres and network cables – all things required in the new artificial intelligence (AI) and technology era, but Cordiant Digital Infrastructure has struggled despite this.

It has been the worst performer in the IT Infrastructure sector over three years and second-worst over 12 months, beating only the Digital 9 Infrastructure trust.

These are the only two trusts of their kind in the sector, with the majority of their peers investing in more traditional infrastructure projects, and Calder said Cordiant had been “dragged down” by its main rival.

Performance of trust vs sector over 3yrs

Source: FE Analytics

“It has been tarred with the same brush as the other one in the sector,” he said, despite having much stronger potential for both net-asset value (NAV) and share price gains.

“The trust’s manager is buying shares which is always a very good sign. He has the courage of his own convictions, which gives us confidence,” said Calder.

The third infrastructure pick was HICL Infrastructure, which has been a middling performer in the IT Infrastructure sector over one, three, five and 10 years, failing to beat the average return in the sector over any time period. However, the fund has a market capitalisation of £2.6bn and its size was a draw for the fund selector.

In its interim update in July, the trust was in line with expectations, according to Rees, and provided an update on the regulator Ofwat’s dealings with portfolio holding Affinity Water. It is the largest position in the trust and is in negotiations over its business plan. Rees noted that a positive outcome should allow Affinity Water to make payouts to its investors by December, which “should continue to improve HICL’s dividend cover from 1.05

If you’ve been keeping a close eye on share tips 2024, then don’t miss this weekly round up of the top stocks to consider for your portfolio each week.

The MoneyWeek share tips 2024 guide pulls together some of the best UK stocks from some of the top share tipsters around.

As well as the UK financial pages, we look at publications across the pond for investors who want to diversify their holdings internationally.

End of Summer Sale Limited-time offer

Try 6 free issues, then save an extra 10% on a Print + Digital subscription. Plus get a free financial eBook (worth £18.75).

From investing in UK equities, European stocks, to finding the best performing stocks in the S&P 500 – here are our top share tips of the week.

This list is updated weekly on a Friday.

Share tips 2024: top picks of the week

Five to buy

1. Teck Resources (NYSE: TECK) The Telegraph Teck Resources has sold off its oil and coal arms in order to focus on low-carbon metals such as copper and zinc. It received $7.3 billion from the coal sale, allowing it to pay down debt, return capital to shareholders, and invest in copper and zinc assets. Prospective buyers should be mindful of likely currency conversion charges on any share purchases, as the group is listed in Canada and the US. But Teck is poised for growth thanks to a focus on metals used in the global energy transition. $43

Currys (LON: CURY) The Times Currys has over 700 stores, mostly in the UK. The electrical retailer recently rejected two takeover offers because the board believed they undervalued the company. Sales have grown in the UK and Ireland, although the Nordic market continues to pose problems. Currys has been reducing its debt. Bulls are hoping that Currys will profit from the next upgrade cycle for smartphones and personal computers. With the shares trading at a significant discount to their peers, there may be further takeover interest. 80p

Knights Group (LON: KGH) This is Money Aim-listed Knights Group was one of the first law firms to go public. Unlike traditional practices, it separates business management from legal work, a strategy that has underpinned rapid expansion. Knights has been through tough times, but the firm is back on track. With almost 1,100 lawyers, the firm is benefiting from a recent uptick in corporate dealmaking and aims to double sales to £300m in five years. “Shares should move higher, and dividends are rising too.” 125p

Foresight Solar Fund (LON: FSFL) Shares Foresight Solar Fund invests in solar and battery storage assets in the UK and overseas. With a target dividend of 8p for 2024, Foresight Solar Fund offers an 8.6% yield and has launched a £50m share buyback programme. Foresight argues that its UK sites consistently outperform peers in the conversion of solar irradiation into electricity. Despite challenges related to bolstering production overseas, Foresight’s second-quarter net asset value (NAV) increased, and cash flow proved resilient. Plans for asset sales, debt reduction, and a focus on total returns enhance Foresight’s prospects. 94p

Freeport-McMoRan (NYSE: FCX) Investors’ Chronicle Freeport-McMoRan’s Grasberg mine in Indonesia is one of the world’s largest copper and gold mines. Despite past tensions with the Indonesian government, Grasberg makes up most of Freeport’s operating profits. Long-term projections for copper suggest a potential supply deficit by 2040, leading to possible price increases. The US firm is focusing on innovative mining techniques and negotiating with the Indonesian government to extend mining permits. “This is a good time to get in.” $40

One to sell

I3 Energy (LON: I3E) The Telegraph Gran Tierra Energy’s bid for Canadian UK-listed oil and gas firm I3 Energy is an opportunity to book a “modest” profit. Gran Tierra offered one of its shares for every 207 shares owned in I3, 10.43p per share in cash, and a 0.2565p dividend. This adds up to 13.6p a share and may result in I3 shareholders having a 16.5% stake in Gran Tierra. I3’s shares trading at a discount to the offer price suggests that some investors doubt the bid will be successful, even though I3’s board recommends it. Sell. 12p

The rest…

easyJet (LON: EZJ) The Times EasyJet recently narrowly avoided relegation from the FTSE 100 thanks to a lastminute surge in the stock. Despite recovering sales, profits, and dividends after Covid, the budget carrier’s shares are still trading below 2019 levels. EasyJet aims to generate over £1 billion in pre-tax profit in the next three to five years, with a focus on the holiday business. This division ensured that third-quarter pre-tax profits rose by 16%. The shares are volatile, but reasonably priced. Hold (482p).

Golden Prospect Precious Metals (LON: GPM) This is Money Golden Prospect Precious Metals owns stakes in over 40 companies, “many of which would be hard to access for individual investors”. Most of its capital is focused on ten companies, led by Australian Emerald Resources, whose shares have soared tenfold since 2020. The firm’s long-term performance has been healthy, yet the stock trades at just 35.3p even though assets are valued at 45.5p. The discount should narrow as the portfolio “continues to deliver”, making Golden an “attractive buy” (35.3p).

Rightmove (LON: RMV) Shares Shares in Britain’s biggest property portal Rightmove surged on takeover interest from Australian property listing firm REA, which is controlled by media tycoon Rupert Murdoch’s NewsCorp. REA has until 30 September to make a formal bid or walk away. Investors should “hold on for now” as REA’s move looks “opportunistic”. For a bid to be successful, it would have to be at a premium to the share price. Analysts at Panmure Liberum suggest a 60% premium, while Berenberg has estimated a take-out price of 830p (654p)

As this year’s income is assured, it’s time to start to plan for next year’s income. There will be 1k to re-invest at the end of this month, so the 3 Trusts under consideration are BSIF, JLEN, SUPR.

sssinstagram Hiya! Quick question that’s completely off topic.Do you know how to make your site mobile friendly? My web site looks weird when viewing from my apple iphone.I’m trying to find a theme or plugin that might be able to resolve this problem.If you have any recommendations, please share. Appreciate it!

Sorry I can’t help, if anyone can I will update later.

Artemis Alpha and Aurora to merge; Balanced Commercial Property to be acquired by Starwood; Tritax EuroBox to be taken over by Segro; while abrdn UK Smaller Companies Growth to hike dividend by an inflation-busting 9.1%.

Frank Buhagiar

Aurora and Artemis Alpha to Combine

Aurora (ARR) and Artemis Alpha (ATS) are set to become the latest two investment trusts to join forces in the interests of gaining scale. As per ARR’s press release of 02 September 2024, the two funds have agreed to merge with Aurora to be the continuing vehicle. ATS shareholders will be offered a cash option for up to 25% of their shareholding, subject to a 2% discount and an illiquidity discount of 20% on unquoted investments. The tie-up already has the support of shareholders holding 31.6% of ARR and 31.5% of ATS (31.5%). If all goes ahead, the fund will be renamed Aurora UK Alpha.

Liberum: “We think this is a smart combination of portfolios with significant overlap that should benefit from the greater scale it will achieve. We think the combination would be likely to deliver the increased liquidity noted in the deal drivers, with good potential for a higher share price rating too.”

Balanced Commercial Property Agrees Takeover

Balanced Commercial Property (BCPT) to be acquired by private investment firm Starwood Capital Group in a recommended cash offer of 96p per BCPT share. That’s a 21.5% premium to the undisturbed trading price of 79p before the commencement of the strategic review in April. It’s also an 8.7% discount to BCPT’s last reported (unaudited) NAV per share of 105.1p as at 30 June 2024.

BCPT Chairman, Paul Marcuse, “Over the course of the Strategic Review, we have undertaken an open consultation process with shareholders. We note that a significant proportion of the share register expressed to us a clear preference for a liquidity event, either via a sale or a managed wind-down.” Well, shareholders certainly got their liquidity event.

Tritax EuroBox Recommends All Share Offer

Tritax EuroBox (EBOX), as with BCPT above, clearly got the memo, announcing on the very same day that it too had agreed to a takeover, this time by Segro (SGRO). Unlike with BCPT, the deal is to be paid for in SGRO shares not cash – for each EBOX share held, shareholders will receive 0.0765 New SGRO Shares. EBOX shareholders will also receive a 1.05 pence per share dividend. Based on the SGRO closing share price of 880.0 pence as at 3 September 2024, the transaction values each EBOX share at 68.4 pence. That’s a 27% premium to EBOX’s undisturbed share price of 53.8 pence as at 31 May 2024 and a 14% discount to EBOX’s last reported IFRS NAV and EPRA NDV per share of 93.9 cents as at 31 March 2024.

Numis: “The offer is being recommended by the Board; however the absence of significant irrevocable undertakings beyond the Board (0.08% of share cap) does leave the door open for another party to potentially submit a higher counter offer, including Brookfield who currently have an existing PUSU deadline of 26 September.” In other words, watch this space.

Dividend Watch

Finally, after the excitement of the above three deals, some news from the more sedate world of dividends. abrdn UK Smaller Companies Growth (AUSC) is increasing its full-year dividend to 12p per share, 9.1% ahead of 2023’s payout. That’s inflation-busting with room to spare. Who said dividends were more sedate.

On your marks! With interest rates seemingly on their way down, a chase for yield could be about to begin. According to Invesco Bond Income Plus fund manager Rhys Davies, high-yield bonds sitting on yields of between 7 and 10% could offer a solution.

Frank Buhagiar

In recent years investors haven’t had to work too hard to make a decent return on their cash. Interest rates at levels not seen for decades have meant risk-free assets, such as government bonds and cash, have been offering competitive yields, particularly when compared to the long-run returns generated by riskier asset classes, such as equities. As highlighted in The Financial Times in in 2023, according to the results of a study carried out by Cambridge University’s, Elroy Dimson, world equities (ex-U.S.) generated returns of 5% in the 50 years to 2019. Who needs equities when parking your cash in a government bond can generate near-enough the same level of return?

But with interest rates now coming down in Europe and the UK, and expected to be cut soon in the U.S., government bond yields, which have already fallen to the 4% level in anticipation of lower rates, could move lower still. Alright for those investors who locked in the high yields on offer a year or so back. Not so, for those who didn’t. New investors, it would appear, are now faced with a dilemma – settle for the lower risk-free rates on offer or, in the chase for higher returns, accept the higher level of risk associated with asset classes such as equities. Or are they? For there is a third way. An asset class exists that pays a higher yield than risk-free government bonds, but comes with a lower level of risk compared to equities. The asset class, high-yield bonds.

Certainty of Income and Seniority

High-yield bonds do exactly what they say on the tin – they pay higher interest rates than investment-grade bonds. This way investors are compensated for the extra risk associated with lending to a company with a lower credit rating. A low credit rating is one that is below BBB- from ratings agencies Standard & Poors and Fitch, and below Baa3 from Moody’s.

High-yield bonds have much in common with their investment-grade/government-backed counterparts. And, as Invesco Bond Income Plus (BIPS) fund manager Rhys Davies explains no matter the type of bond, government-backed or high-yield, “a bond is a loan that creates two very important differences versus equities. The first is around income. So, bonds will pay an income through a coupon. That’s a contractual obligation that the company has to pay. Compare that to an equity. Equities will pay an income via a dividend and the company does not have to pay that dividend.” An issuer’s contractual obligation to pay an income, the first difference between corporate bonds and equities which, as Davies puts it, provides “that stability or that certainty of income.”

A second differentiator between bonds and equities is what Davies terms seniority. “So, bonds in a capital structure will rank ahead of equities. That matters should a company get into trouble. In theory, bondholders are able to take the keys, the ownership of a company from the shareholders in that situation.”

Riding High on Yield

Of course, the price paid for certainty of income and seniority over equities is generally lower returns – the classic risk/reward trade-off. I say generally because, according to Davies, the returns on offer from high-yield bonds today are currently higher than they have been for years. As Davies explains, “After the repricing that we saw in bond yields in 2022, we are seeing a lot more yield in the market and especially in the high-yield bond market. So, many high-yield bonds today are paying yields and income of 7%, 8%, 9% even 10% which are levels that are far higher than we have seen for many years.”

Davies goes on to highlight the potential for capital appreciation in today’s bond markets. This is the second component of a bond’s yield, the first being income, and once again, has its origins in the reset of 2022. Bond prices are inversely correlated to yields. Back in 2022, when bond yields moved higher, prices moved lower. So much so that many bonds saw their prices move to below par, par being the level at which they will be redeemed. As bonds approach maturity, prices can therefore be expected to move towards par value, typically 100, thereby generating a capital gain. It is this pull-to-par effect that offers the potential for capital appreciation.

Risk management

The 7-10% yields on offer, just one half of the high-yield bond story though. The other, the extra risk involved, at least when compared with investment-grade bonds. Risk can be managed though. A portfolio, for example, could hold a mix of investment-grade and high-yield bonds to lower the overall level of risk. This is what BIPS does. The fund, which currently offers a 6.8% dividend yield, holds a portfolio of bonds with different credit profiles – as at April 2024, the fund held almost a third of its assets in investment-grade bonds.

Risk can also be managed by ensuring comprehensive due diligence on the issuers is constantly carried out. Gaining a deep understanding of the sectors in which the underlying companies operate, the risks and opportunities they face and critically their key financial metrics, all help manage the risks involved in lending to companies. As BIPS’ Davies explains, “What’s really important to us is looking at the cash profiles of the companies that we are investing in. We need to ensure they are going to be able to afford the interest that they have to pay us on our bonds.” Always important, but especially so in the current high-interest rate environment.

And based on BIPS’ performance over the past five discrete years, a period that included the pandemic as well as the re-emergence of inflation in the developed world, the fund’s focus on risk management has served the fund well in recent years. As the Association of Investment Companies’ graph below shows, BIPS has posted a positive NAV total return in four of the past five discrete years:

Certainly, Winterflood appears to be a fan. In January 2024, the broker wrote “In our view, the managers’ cautious approach is rational, given the uncertainty posed by economic conditions and the oft-cited ‘maturity wall’. Portfolio changes over time have measurably increased income and simultaneously decreased credit risk. Therefore, BIPS may be a suitable vehicle for investors looking to gain exposure to the High Yield market”.

Strike While The Iron Is Hot

BIPS may well be the right vehicle for investors looking to gain exposure to high-yield bonds, but is it the right time to build that exposure? Certainly, more and more investors were upping their weightings in the asset class earlier this year. According to Reuters article, Investors queued up for U.S. high-yield bond funds as rate cut hopes grow, between January and May this year, inflows to U.S. high-yield bond funds totalled $6.1 billion, the highest level seen in three years. Reasons cited, “the allure of higher yields, potential for price appreciation amid anticipated Federal Reserve rate cuts, and diminishing corporate credit risks.”

Now, interest rate cuts in the U.S. have, as yet, not been forthcoming, but this may change soon. The market is currently pricing in a high probability of interest rate cuts at the next Federal Reserve meeting in September – according to Winterflood’s morning note of 9 September “Markets are pricing in a 73% chance of a 25bps cut on 18 September”.

And, as the Reuters article explains, interest rate cuts would be good news for high-yield bonds, “Analysts expect that lower interest rates, stemming from potential Fed rate cuts, would benefit high-yield bond issuers by enhancing liquidity and easing the cash flow constraints that have intensified due to the Federal Reserve’s previous rate hikes.” So, with U.S. interest rates seemingly set to fall, the time could well be right for high-yield bonds.