Editor Insights

Why the Time Might Be Right for High Yield Bonds

On your marks! With interest rates seemingly on their way down, a chase for yield could be about to begin. According to Invesco Bond Income Plus fund manager Rhys Davies, high-yield bonds sitting on yields of between 7 and 10% could offer a solution.

Frank Buhagiar

In recent years investors haven’t had to work too hard to make a decent return on their cash. Interest rates at levels not seen for decades have meant risk-free assets, such as government bonds and cash, have been offering competitive yields, particularly when compared to the long-run returns generated by riskier asset classes, such as equities. As highlighted in The Financial Times in in 2023, according to the results of a study carried out by Cambridge University’s, Elroy Dimson, world equities (ex-U.S.) generated returns of 5% in the 50 years to 2019. Who needs equities when parking your cash in a government bond can generate near-enough the same level of return?

But with interest rates now coming down in Europe and the UK, and expected to be cut soon in the U.S., government bond yields, which have already fallen to the 4% level in anticipation of lower rates, could move lower still. Alright for those investors who locked in the high yields on offer a year or so back. Not so, for those who didn’t. New investors, it would appear, are now faced with a dilemma – settle for the lower risk-free rates on offer or, in the chase for higher returns, accept the higher level of risk associated with asset classes such as equities. Or are they? For there is a third way. An asset class exists that pays a higher yield than risk-free government bonds, but comes with a lower level of risk compared to equities. The asset class, high-yield bonds.

Certainty of Income and Seniority

High-yield bonds do exactly what they say on the tin – they pay higher interest rates than investment-grade bonds. This way investors are compensated for the extra risk associated with lending to a company with a lower credit rating. A low credit rating is one that is below BBB- from ratings agencies Standard & Poors and Fitch, and below Baa3 from Moody’s.

High-yield bonds have much in common with their investment-grade/government-backed counterparts. And, as Invesco Bond Income Plus (BIPS) fund manager Rhys Davies explains no matter the type of bond, government-backed or high-yield, “a bond is a loan that creates two very important differences versus equities. The first is around income. So, bonds will pay an income through a coupon. That’s a contractual obligation that the company has to pay. Compare that to an equity. Equities will pay an income via a dividend and the company does not have to pay that dividend.” An issuer’s contractual obligation to pay an income, the first difference between corporate bonds and equities which, as Davies puts it, provides “that stability or that certainty of income.”

A second differentiator between bonds and equities is what Davies terms seniority. “So, bonds in a capital structure will rank ahead of equities. That matters should a company get into trouble. In theory, bondholders are able to take the keys, the ownership of a company from the shareholders in that situation.”

Riding High on Yield

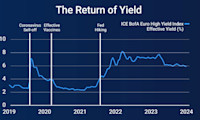

Of course, the price paid for certainty of income and seniority over equities is generally lower returns – the classic risk/reward trade-off. I say generally because, according to Davies, the returns on offer from high-yield bonds today are currently higher than they have been for years. As Davies explains, “After the repricing that we saw in bond yields in 2022, we are seeing a lot more yield in the market and especially in the high-yield bond market. So, many high-yield bonds today are paying yields and income of 7%, 8%, 9% even 10% which are levels that are far higher than we have seen for many years.”

Davies goes on to highlight the potential for capital appreciation in today’s bond markets. This is the second component of a bond’s yield, the first being income, and once again, has its origins in the reset of 2022. Bond prices are inversely correlated to yields. Back in 2022, when bond yields moved higher, prices moved lower. So much so that many bonds saw their prices move to below par, par being the level at which they will be redeemed. As bonds approach maturity, prices can therefore be expected to move towards par value, typically 100, thereby generating a capital gain. It is this pull-to-par effect that offers the potential for capital appreciation.

Risk management

The 7-10% yields on offer, just one half of the high-yield bond story though. The other, the extra risk involved, at least when compared with investment-grade bonds. Risk can be managed though. A portfolio, for example, could hold a mix of investment-grade and high-yield bonds to lower the overall level of risk. This is what BIPS does. The fund, which currently offers a 6.8% dividend yield, holds a portfolio of bonds with different credit profiles – as at April 2024, the fund held almost a third of its assets in investment-grade bonds.

Risk can also be managed by ensuring comprehensive due diligence on the issuers is constantly carried out. Gaining a deep understanding of the sectors in which the underlying companies operate, the risks and opportunities they face and critically their key financial metrics, all help manage the risks involved in lending to companies. As BIPS’ Davies explains, “What’s really important to us is looking at the cash profiles of the companies that we are investing in. We need to ensure they are going to be able to afford the interest that they have to pay us on our bonds.” Always important, but especially so in the current high-interest rate environment.

And based on BIPS’ performance over the past five discrete years, a period that included the pandemic as well as the re-emergence of inflation in the developed world, the fund’s focus on risk management has served the fund well in recent years. As the Association of Investment Companies’ graph below shows, BIPS has posted a positive NAV total return in four of the past five discrete years:

Certainly, Winterflood appears to be a fan. In January 2024, the broker wrote “In our view, the managers’ cautious approach is rational, given the uncertainty posed by economic conditions and the oft-cited ‘maturity wall’. Portfolio changes over time have measurably increased income and simultaneously decreased credit risk. Therefore, BIPS may be a suitable vehicle for investors looking to gain exposure to the High Yield market”.

Strike While The Iron Is Hot

BIPS may well be the right vehicle for investors looking to gain exposure to high-yield bonds, but is it the right time to build that exposure? Certainly, more and more investors were upping their weightings in the asset class earlier this year. According to Reuters article, Investors queued up for U.S. high-yield bond funds as rate cut hopes grow, between January and May this year, inflows to U.S. high-yield bond funds totalled $6.1 billion, the highest level seen in three years. Reasons cited, “the allure of higher yields, potential for price appreciation amid anticipated Federal Reserve rate cuts, and diminishing corporate credit risks.”

Now, interest rate cuts in the U.S. have, as yet, not been forthcoming, but this may change soon. The market is currently pricing in a high probability of interest rate cuts at the next Federal Reserve meeting in September – according to Winterflood’s morning note of 9 September “Markets are pricing in a 73% chance of a 25bps cut on 18 September”.

And, as the Reuters article explains, interest rate cuts would be good news for high-yield bonds, “Analysts expect that lower interest rates, stemming from potential Fed rate cuts, would benefit high-yield bond issuers by enhancing liquidity and easing the cash flow constraints that have intensified due to the Federal Reserve’s previous rate hikes.” So, with U.S. interest rates seemingly set to fall, the time could well be right for high-yield bonds.

££££££££££££££££

Yield 6.6% trades at small premium to NAV

Leave a Reply