Bluefield Solar (LON: BSIF), the London listed UK income fund focused primarily on acquiring and managing solar energy assets, is pleased to confirm that following the first stage of National Energy System Operator’s (‘NESO’) grid reform process, the Company received Gate 2, Phase 1 offers on c. 660MW of its development pipeline.

NESO’s grid reform process is a major overhaul of how energy projects connect to Britain’s electricity grid, designed to clear a huge backlog, prioritise ‘ready to go’ projects, and align the system with the UK’s Clean Power 2030 goals. It replaces the old first come – first served queue with a readiness and strategic alignment based system, removes stalled projects, and introduces a new process to accelerate delivery.

Receipt of a Gate 2, Phase 1 offer means that projects have had their connection date confirmed as being between 2026-2030 and so have attained a highly protected status in the queue of projects to be connected to the grid. The technology split across the Gate 2, Phase 1 offers for the Company’s development pipeline is c. 540MW solar PV and c.120MW BESS.

Bluefield Solar is also pleased to confirm that it has received Gate 2, Phase 2 offers on c. 560MW of its development pipeline, split between c. 185MW PV and c. 370MW BESS. Receipt of a Phase 2 offer means projects have been allocated a grid connection date between 2031-2035.

This means of the Company’s c. 1.34GW pipeline, over 90% has received Gate 2 offers. The remaining 9% of the pipeline that was allocated Gate 1 offers corresponds to 125MW BESS. Projects allocated Gate 1 offers will need to re-apply for new grid offers to re-enter the grid queue, upon which connection dates offered will depend on application of NESO’s strategic alignment criteria. The Company is also able to confirm that projects which have been allocated Gate 1 offers have not been allocated any value within the Company’s NAV to date.

The success of the grid reform process is testament to the strategy designed and implemented by the Investment Adviser in 2020 and has resulted in the Company having a highly valuable pipeline.

Update on Formal Sale Process

The Strategic Review and Formal Sale Process announced by the Company on 5 November 2025 continues in line with the Board’s expectations. The Company will provide a further update when it issues its interim results in early March 2026 unless there are any material developments in the meantime.

My Market Forecast for 2026 (and a “17%-Off” Dividend to Play It)

by Michael Foster, Investment Strategist

I’m a contrarian at heart – but sometimes even contrarians have to go along with the mainstream opinion.

This (as much as it pains me!) is one of those times. You see, like most of the pundits out there, I expect another strong year for stocks in 2026. I see a roughly 12% gain for the S&P 500 this year, to be exact.

That bothers me. A lot.

I know that four strong years in a row is rare, indeed. But that’s what the data is telling me, and I’m not going to argue with it.

Still Plenty of Cheap CEF Dividends Out There – Even in This “Pricey” Market

Now this doesn’t mean there’s a lack of bargains waiting for us in our favorite income plays: 8%+ closed-end funds (CEFs). Far from it!

The beauty of CEFs is that there are always some of these funds trading at unjustified discounts to net asset value (NAV, or the value of their underlying portfolios).

At times like this, I look for CEFs with deep discounts and strong returns. We love “disconnects” like that because they give us a clear way to ride the stock market’s momentum without buying in at nosebleed levels.

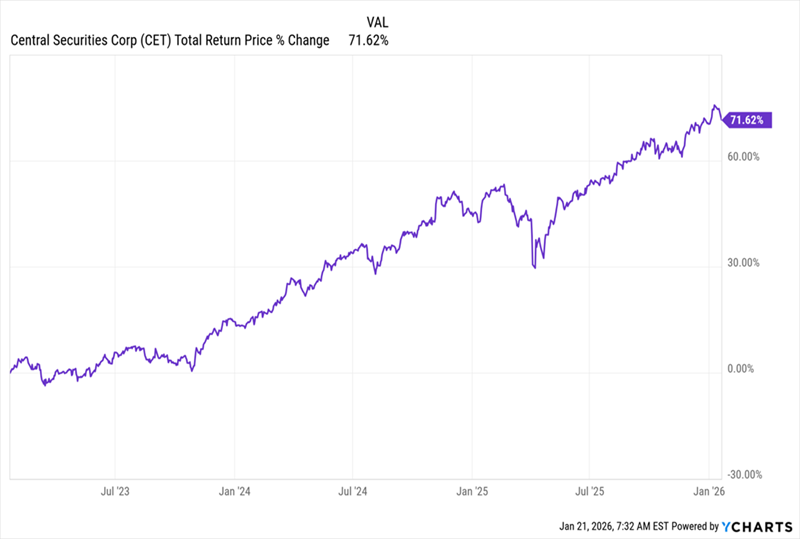

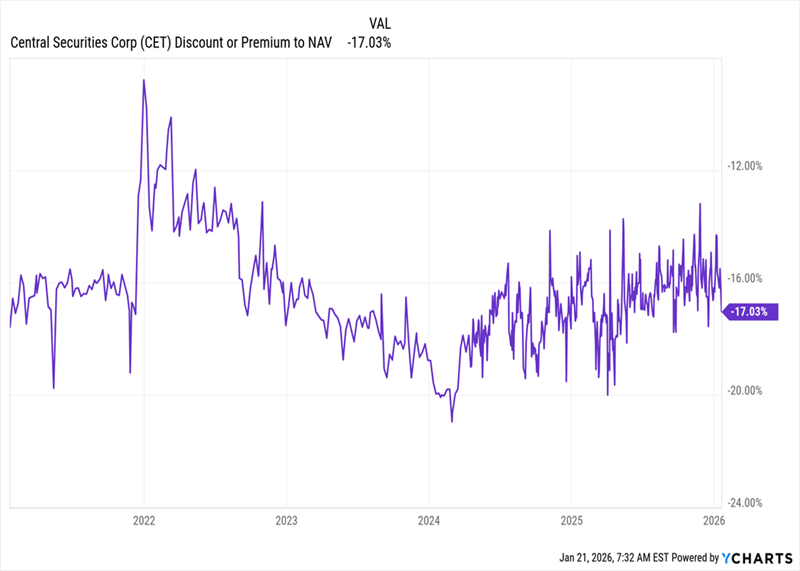

A CEF like the Central Securities Corporation (CET) is a good example. It trades at a 17% discount (so for 83 cents on the dollar, in other words!) while focusing on high-quality public firms with big margins and strong cash flows: Alphabet (GOOGL), Progressive Corp. (PGR) and Amazon (AMZN) are its top stock positions.

That makes it a great way to ride another strong market year while gleaning a 5.3% dividend that grows with the fund’s portfolio returns, as management pledges to pay “substantially all net investment income and realized capital gains” as dividends.

But let’s back up for a second, because we need to talk about the data behind my bullish call here, before we get too far into this smartly run fund.

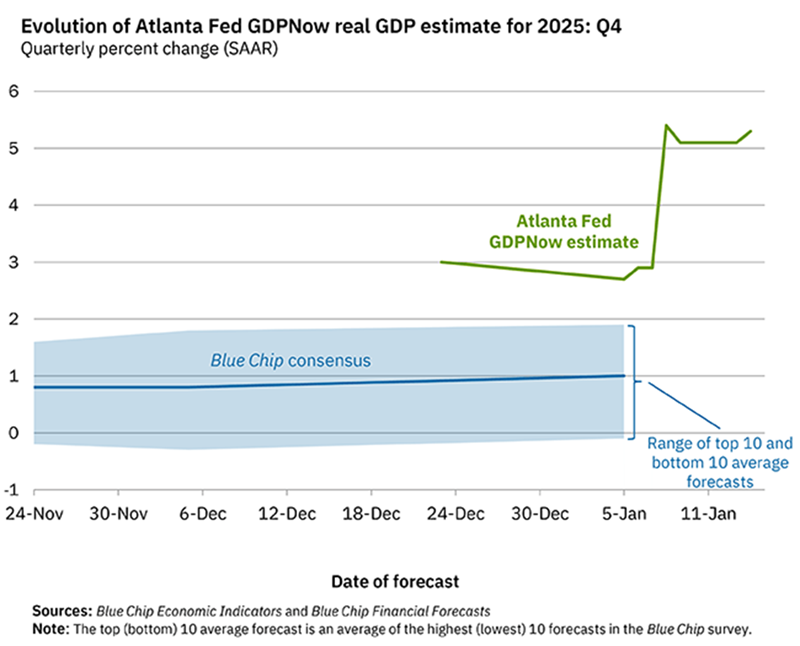

Real-Time Indicator Says Something Shocking

One of the most eye-catching things I’ve seen lately is the Atlanta Fed’s GDPNow indicator, the most up-to-date measure of economic growth we have.

As of now, it’s pointing to an incredible 5% gain in GDP in the last quarter of 2025. That’s far ahead of the roughly 1% growth most economists are calling for.

Now, that 5% call may end up being way too bullish (and, indeed, I expect it to). But the key point is that expectations for growth are strong, driven mainly by big companies investing for the future (yes, AI investment is playing a role here).

More spending on big projects means more money going to other firms and to workers, who then spend in the economy. This, in fact, might explain why our worst economic indicator is suddenly turning around.

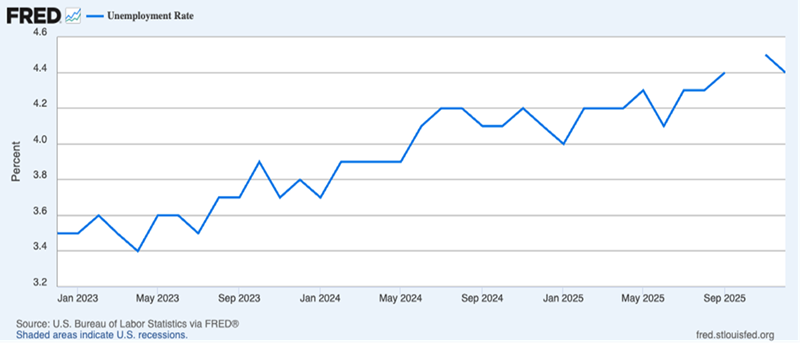

The labor market is the economy’s weak spot now, with unemployment rising since the start of 2023. Note, however, that stocks have soared since, with about a 78% gain in just three years. So this by itself isn’t necessarily bad for the market.

Moreover, as you can see above, the unemployment rate, which peaked at the end of 2025, looks like it’s beginning to fall (the gap in the chart above is due to a lack of jobs data during the government shutdown).

A small move like that does not signify a trend, so let’s look at a couple other labor measures to see if we can get a more complete picture.

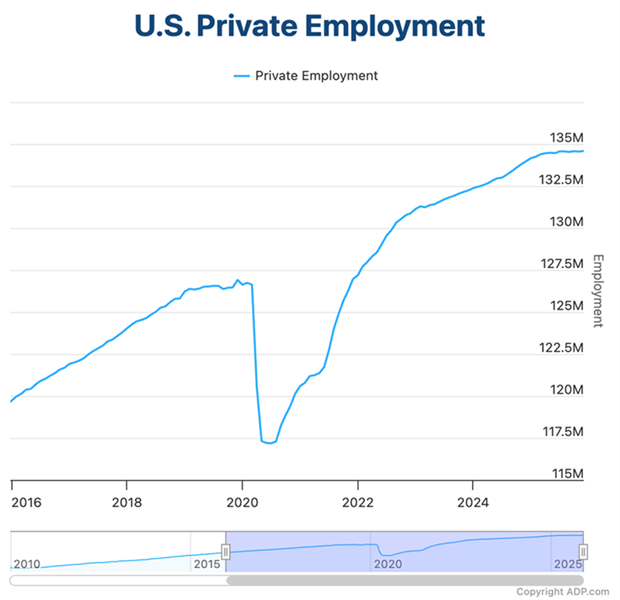

Here we see the total number of people in private employment in the US, according to ADP. Before the pandemic, that was about 126.6 million people, or 38.2% of the population. Afterward, that rose to 134.6 million, or 39.6% of the population.

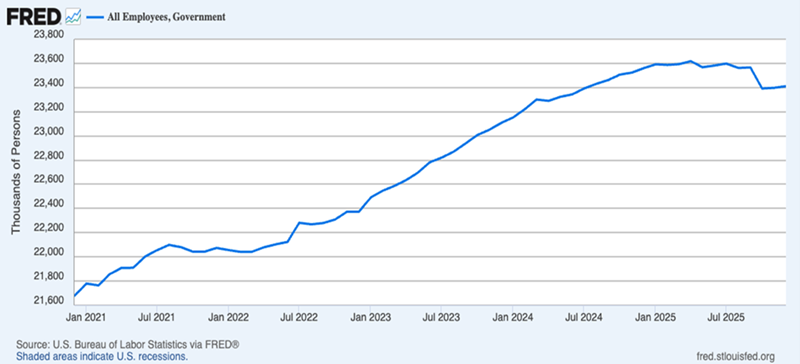

This data is also a bit noisy, though, and it doesn’t show government-employee numbers. Fortunately, we do have more reliable data on that front.

It’s true that the total number of government employees peaked in mid 2025, but the decline since has been small and had fully transpired by October 2025, when the shutdown and DOGE layoffs took effect. Since then, Uncle Sam’s workforce has started to grow again.

Put together, we see that both public and private labor markets are showing no alarming signs – and these are the biggest risks to the economy in 2026.

To be sure, things could (and likely will at some points) get upset by unpredictable shocks. But there is one predictable shock that could upset stocks: earnings.

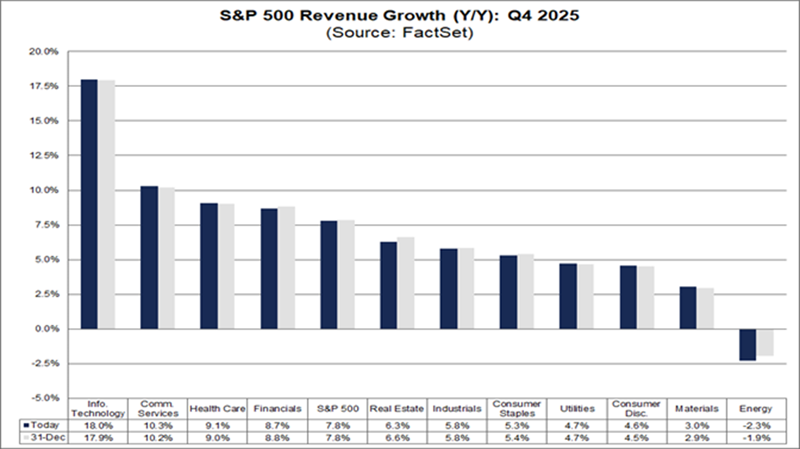

So far, earnings have been okay, but what’s really key is sales, which rose 7.8% across S&P 500 companies in the fourth quarter. That, again, is a sign the economy is doing well.

This brings me back to CET, which has delivered a solid return over the last three years, as markets moved away from the aftereffects of the pandemic and looked more toward the future, including productivity gains from AI.

CET’s Solid Gains At the same time, CET’s discount to NAV has been unusually generous, although that discount has been fading (in its usual up-and-down fashion) since bottoming out at over 20% about two years ago.

CET’s Big Discount Begins to Evaporate That’s the discount setup I hinted at off the top: a markdown that’s wide now, and has momentum as it moves back toward par.

That sets up the fund to rise with the market in 2026, and to grab an extra bounce from its closing discount. Moreover, we can look forward to dividend growth as management “translates” its portfolio gains into payouts (those payouts typically come as a smaller dividend paid in June and a larger one in December).

And with all signs pointing to another strong market year in 2026, that’s a very sweet setup for anyone looking for income and growth.

Mortgages form the backbone of home affordability in America and represent an expense that cannot be cut without catastrophic household consequences.

Utilities are in heavy demand, and operators can raise prices without losing customers.

We discuss our top picks from these non-negotiable expenses, offering yields of up to 7.5%.

Looking for more investing ideas like this one? Get them exclusively at High Dividend Opportunities.

Co-authored with Hidden Opportunities

Every new year almost always begins the same way, with resolutions. We plan to eat better, lose weight, exercise more, sleep more, read more, save, and invest more. The goals are diverse, and we set out with the best intentions, aiming to create a better version of ourselves.

Yet, once the calendar flips, reality quickly reasserts itself. Despite the intentions being good, our time constraints don’t magically disappear, and our habits and priorities don’t magically reorganize themselves. Life keeps moving at the same pace it always has, and keeping up that New Year’s resolution requires serious effort. This isn’t a secret, and it is why the second Friday of January is often considered “Quitters Day,” when the energy and the momentum behind the resolutions tend to fade.

You may be interested to know that cancelling streaming services like Netflix (NFLX) is typically a popular New Year’s resolution as part of the general household audit for many consumers. Amidst rapidly rising costs of goods and services, a wider pursuit of resolutions to find areas to cut expenses wouldn’t be surprising. Yet, there are a few places where the expenses are unavoidable and must be made, even to maintain a modest lifestyle and well-being.

Without fail, you will pay your mortgage and your utility bills. These expenses won’t take a break, whether your resolution to optimize spending stays strong or wanes. Let us dive into our top picks that benefit from this necessity.

Pick No. 1: MTBA – Yield 6%

Owning a home has historically been regarded as a symbol of success and forms an important pillar of the American dream. Out of 85.6 million owner-occupied homes, 51.6 million (60%) have outstanding mortgages. It is fair to say that mortgages are a helping hand for millions of Americans to realize their dream. At the end of September 2025, household mortgage balances totaled $13.07 trillion, representing 82% of all household debt.

That simple mortgage you took from your favorite bank isn’t that simple after all. The bank doesn’t hold it on its balance sheet for 30 years, only to collect interest from you. Banks sell the loan to aggregators, which happen to be government-sponsored enterprises like Fannie Mae, who pool hundreds of thousands of mortgages together to form a security known as MBS (mortgage-backed security). When homeowners make principal and interest payments, the loan servicer collects them and passes them through to investors.

Who are these investors?

U.S. banks, depository institutions, and the Federal Reserve happen to be the largest investors in agency MBS.

Why would these institutions invest in mortgage-backed securities? Isn’t there a risk of mortgage default?

Fixed-rate agency MBS securities are guaranteed by government-sponsored institutions like Fannie Mae, Freddie Mac, and Ginnie Mae. These securities hold 30-year, 20-year, and 15-year mortgages that were securitized by these agencies. So, even if individual borrowers default, these agencies would guarantee payments to investors.

Agency MBS are AAA-rated and present exceptionally safe investments with negligible default risk, making them at par with U.S. Treasuries.

Agency MBS are only available to institutions, which means as an individual investor, you can only buy them through diversified funds or mortgage REITs. The latter often use leverage, which makes them highly sensitive to interest rates. Diversified funds, on the other hand, present a wide range of options for investors.

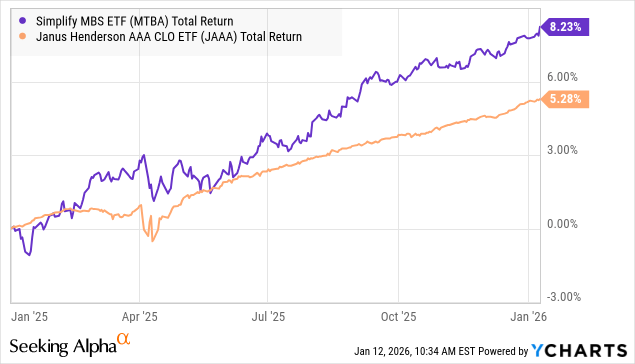

Simplify MBS ETF (MTBA) is an ETF that invests in Agency MBS with no leverage. This fund focuses on buying newer MBS, which typically carry higher coupons and pay higher yield to maturity, and shorter durations of 3-4 years.

In 2025, MTBA gained due to greater inflows of institutional capital into MBS, as spreads to Treasuries tightened. This resulted in MTBA delivering better total returns than our frequently discussed AAA-CLO ETF—Janus Henderson AAA CLO ETF (JAAA).

Looking ahead, there is room for further tightening in agency MBS spreads, and MTBA offers a low but steady CD-beating 6% yield with no credit risk.

With MTBA, you are partly funding the American dream of homeownership while collecting low-risk monthly distributions.

Pick No. 2: UTF – Yield 7.6%

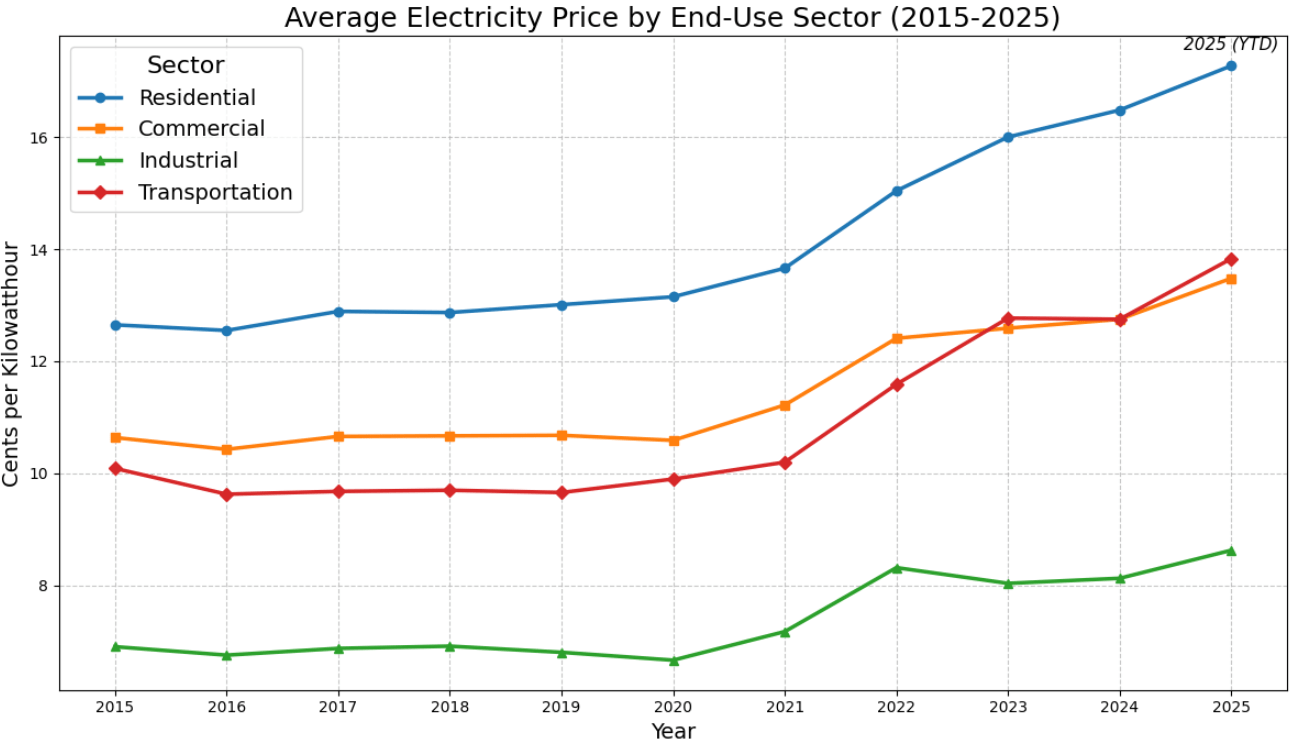

Utility costs continue to outpace inflation, driven by heavy demand from big tech data center ambitions. The U.S. power grid is aging and inadequate for the soaring demand, making the unit costs higher for every sector, with the residential base experiencing the worst effects.Data Source

Author’s Creation.

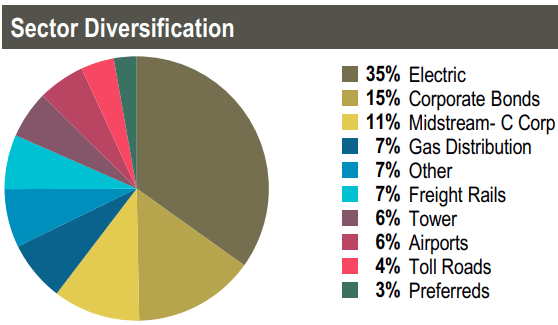

Cohen & Steers Infrastructure Fund (UTF) is a CEF (closed-end fund) dedicated to investing in infrastructure, as its name suggests. The fund’s assets are invested across electric utility, midstream, gas distribution firms, freight rail, towers, etc. The fund has a notable allocation into fixed-income securities from these essential sectors. In fact, energy (electricity, gas, and midstream) represents almost 50% of the portfolio. Source

Fact Sheet

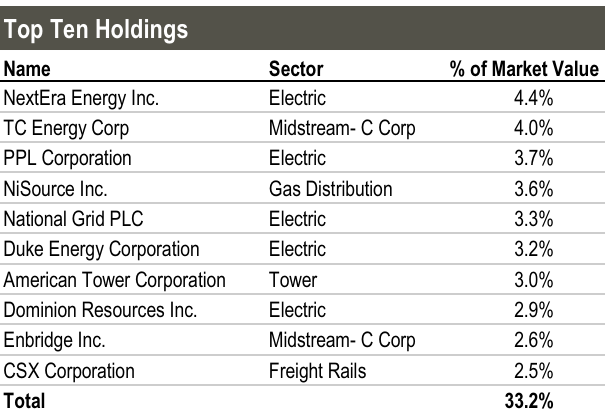

UTF’s top holdings are some of the largest global corporations in their respective subsectors, with a notable callout that they aren’t direct competitors in major business areas. Rather than serving as direct competitors, these firms occupy separate geographic or industrial niches and often act as complementary partners within the infrastructure supply chain. UTF’s top 10 holdings represent a third of the CEF’s invested assets.

Fact Sheet

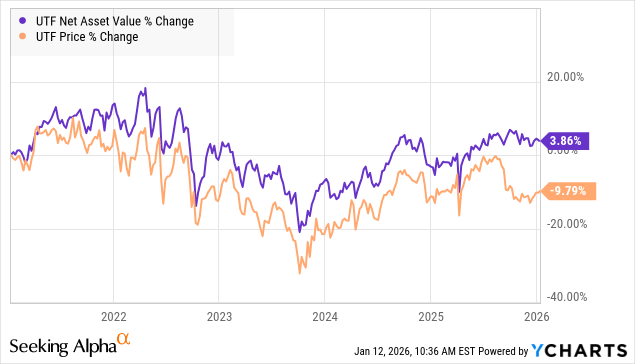

If you look at UTF’s price and NAV performance, they have been in unison over the past five years, climbing together in the near-zero economy, being weighed down due to the headwinds from rate hikes, and a predictable recovery with rate cuts. And there is one place where they clearly break the pattern, in Fall 2025.

This is when UTF announced a rights offering, which was completed in October, resulting in the issuance of 14.9 million shares to raise $353 million in proceeds. The offering led to a 15% dilution to shareholders, and the entire process led to a +10% drop in the CEF’s price, despite NAV remaining relatively steady. So what happened? Value remained the same, but investors’ perception of that value changed, creating an opportunity.

Despite a steady NAV level over the five-year period marked by volatile interest rates, UTF has distributed steady monthly income to shareholders, amounting to $9.30/share, which has mostly been tax-friendly, in the form of Long-Term Capital Gains and Qualified Dividends.

Looking ahead, infrastructure projects will be expensive due to the natural effects of inflation on materials and labor—creating a steep barrier for competition. Existing infrastructure is aging and inadequate, but companies owning them are best positioned to maintain and slowly expand those assets while enjoying powerful asset monetization. With UTF, you can be a beneficiary of this strength, with 7.6% yields.

Conclusion

MTBA and UTF are two very different securities. One leans on structured, government-backed cash flows from millions of people pursuing their American Dream; the other draws income from real assets that provide critical services. Their drivers are different, their risks are different, and that is precisely how we like to invest.

At High Dividend Opportunities, we build portfolios with this sort of contrast by design. Rather than relying on a single sector or macro outcome, we combine complementary income sources to generate reliable cash flow across any market cycle. Summer or winter, bull or bear market, high or low-interest rates—I need my dividends, and I need them now.

Rates will move, politics will shift, narratives will change, and volatility will return, but our simple yet disciplined, diversified income strategy allows us to stay invested, stay flexible, and continue getting paid along the way. This is the beauty of our income method and the power of income investing.

The AI Bubble Is Overblown (But This 10.6% Dividend Wins Either Way)

Michael Foster, Investment Strategist

Is 2026 going to be the year the AI “bubble” finally bursts?

Maybe my use of quotes there tipped you off to my true opinion: Worries about an AI bubble are vastly overdone.

And today we’re going to grab a 10.6%-paying closed-end fund (CEF) that wins either way: If I’m wrong and there is an AI bubble (that pops), cash will flow into it. If not, that’s fine: We’ll happily collect its growing 10.6% payout.

From Silicon Valley to Wall Street

Of course, the AI CEOs agree with me that there is no AI bubble: Sam Altman, Elon Musk and the heads of Microsoft (MSFT), Meta Platforms (META), Alphabet (GOOGL) and Oracle (ORCL) are all bullish and willing to spend trillions on the tech.

But another group also agrees that AI-bubble fears are overdone: a cadre of hedge funds and institutional investors that regularly hold tech titans like Musk, Zuckerberg and friends accountable—and know the “plumbing” of the tech world even better than the billionaire set does.

You can see what I’m talking about here in the fight between Elon Musk and institutional investors over the latter group short-selling stocks like Tesla (TSLA). Musk has complained about this repeatedly, but this short selling does give companies an incentive to do better, so their stocks don’t end up shorted. A kind of accountability emerges as a result.

Coatue and the Tech Hedge Fund World

All of this brings me to Coatue Management. It’s a tech hedge fund that began during the dot-com bubble and not only survived but grew from $45 million in assets at its launch to about $70 billion today.

Over that time, Coatue has shorted many tech stocks, so it has experience in keeping corporate managers from getting tied up in indulgent behaviors that lose money for investors. Coatue also has plenty of experience with bubbles.

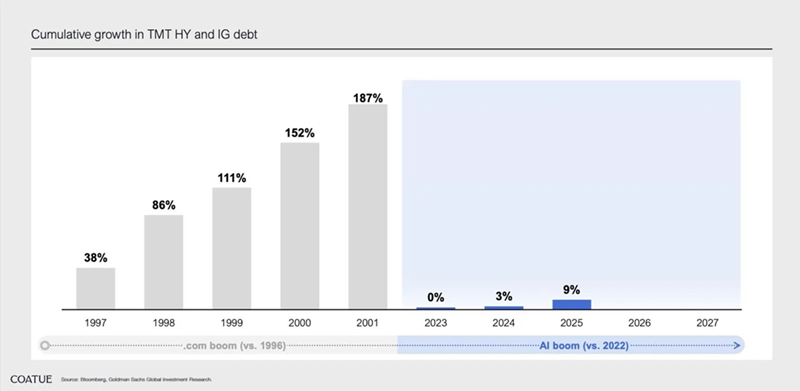

So when Coatue dismisses talk of an AI bubble, we should listen. And that’s exactly what it did late last month, when it posted this chart:

Here we see that over the last three years, there has been surprisingly little growth in the amount of money invested in corporate bonds issued to fund the tech, media and telecom sectors. (That’s the “TMT” in the title—those are the companies like Google, Microsoft, Meta and Oracle.)

The 0%, 3% and 9% gain in total debt issuances from 2023 to 2025 in these sectors suggest the bond market is not overly exposed to AI, and that there’s still a lot of room for debt to grow. Also, the comparison with the dot-com boom’s surging debt growth (on the left side of the chart) tells us the current situation is likely not a bubble—at least not yet.

To be sure, private debt and creative financing of some AI projects means a lot of AI borrowing isn’t shown on this chart. But that was also true of the dot-com era. And estimates of both again show we’re far from a bubble today.

But even if we were, the fact remains that corporate bonds are not overly exposed to AI. Moreover, bond holders tend to demand more discipline around costs.

The AI Hedge Move

If the corporate-bond market isn’t overly exposed to AI, then any volatility prompted by AI-bubble worries will likely drive cash from stocks to corporate bonds. That makes the corporate-bond market the perfect hedge for anyone worried about a selloff.

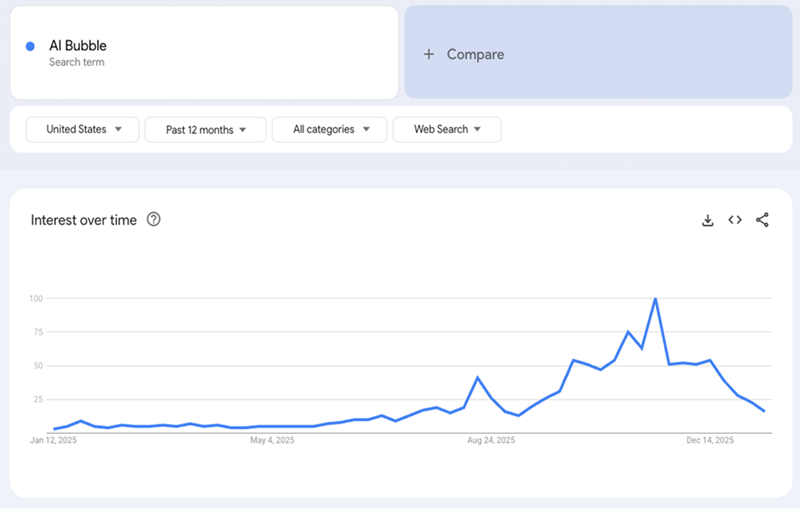

There’s just one thing: AI bubble fears are fading and have been since they peaked in November, at least according to internet search traffic.

AI Bubble Fears on the Backburner—for Now

I know what you’re thinking. “Markets are calm. AI bubble fears are fading, so why worry about this now?” The low fear means the market is not pricing in the potential of investors looking to hedge against AI in the future. That’s left corporate bonds cheaper than they should be.

In other words, we can buy into bonds now that the market isn’t hedging, wait for any stock volatility to boost demand for said bonds, then sell those bonds to investors.

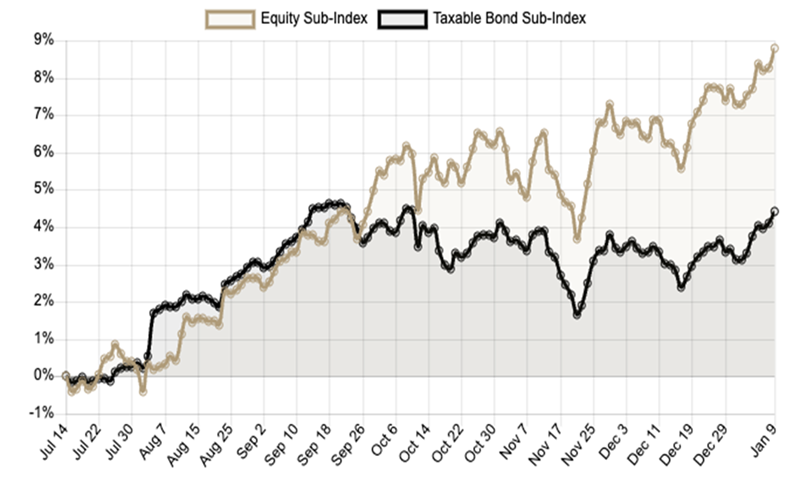

Take a look at this chart.

Bond CEF Underperformance Highlights Our Opportunity Source: CEF Insider

I started 2025 bullish on corporate bond CEFs until September, when we sold three of these funds from our CEF Insider portfolio.

The reason is in the chart above: September was when CEF Insider’s corporate-bond-fund subindex (in black) began lagging its equity-fund subindex (in brown). So CEF Insider focused more on equity funds, which have outperformed since.

Now that bond funds are on sale, and stand to gain on any short-term worries over an AI bubble, it’s time to cycle back to some of them. But how? Through a CEF, of course!

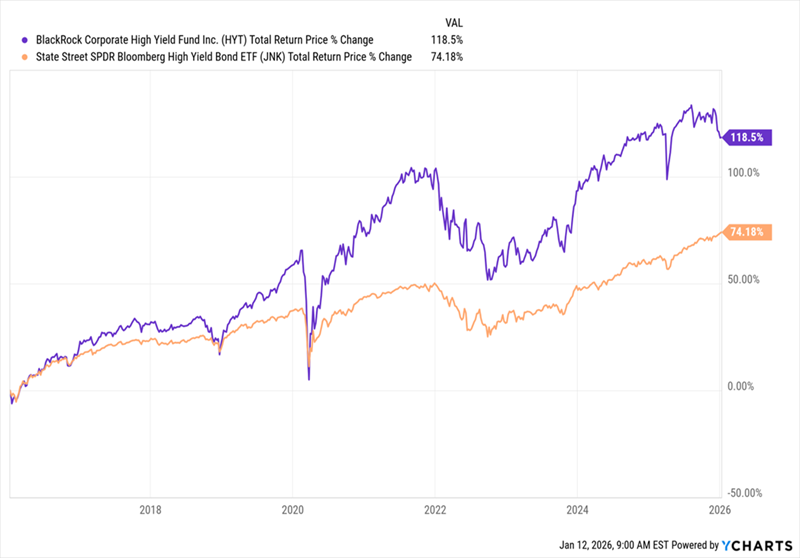

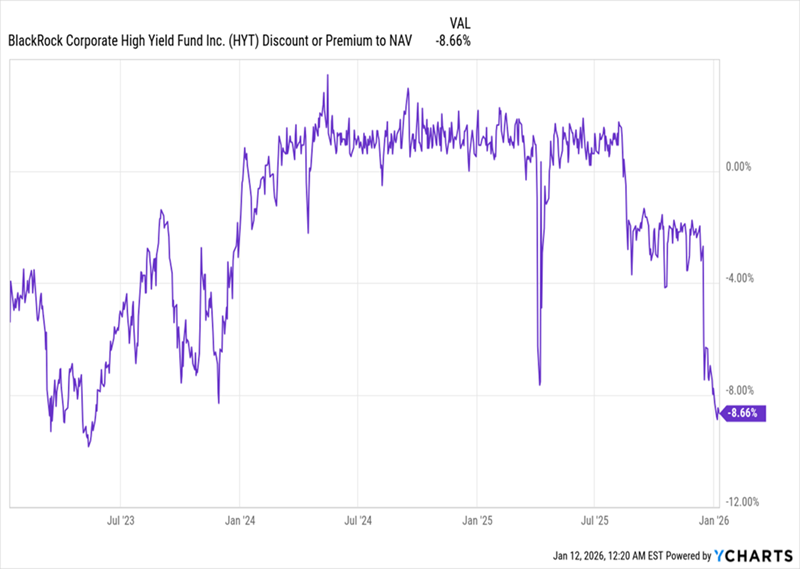

Buying corporate bonds individually is difficult, and bond ETFs typically underperform. But a CEF like the BlackRock Corporate High Yield Fund (HYT) is a great way to buy in, both now and over the next few weeks.

HYT Clobbers Its Benchmark

HYT yields 10.6% today and has raised its payout around 11% in the last decade. That’s in contrast to the corporate-bond benchmark SPDR Bloomberg High Yield Bond ETF (JNK), which has actually seen payouts fall a bit. Even better, HYT (in purple above) has outperformed JNK (in orange).

An even better reason to buy HYT is that today’s low bond demand means the CEF is especially cheap:

A Sudden Discount Appears

In the last six months, HYT’s discount to net asset value (NAV) has dropped to levels not seen since 2022 and 2023, after a long period of trading around par. This is an opportunity for us, putting short-term upside on the table if the fund’s discount evaporates again, like it did at the end of 2023.

With that in mind, buying HYT now is a solid value play, with demand for a hedge against an AI bubble waiting in the wings. And then, of course, there’s the 10.6% dividend.

From 12% Yields, 14% Gains to the Next Dividend Train Leaving the Station

Brett Owens, Chief Investment Strategist Updated: January 21, 2026

When we buy dividend stocks, we’re looking for more than just the dividend. Price gains are preferred as well.

Greedy? Nah. Not if we time our buys right. It is possible to have our payouts and watch our stocks go up, too.

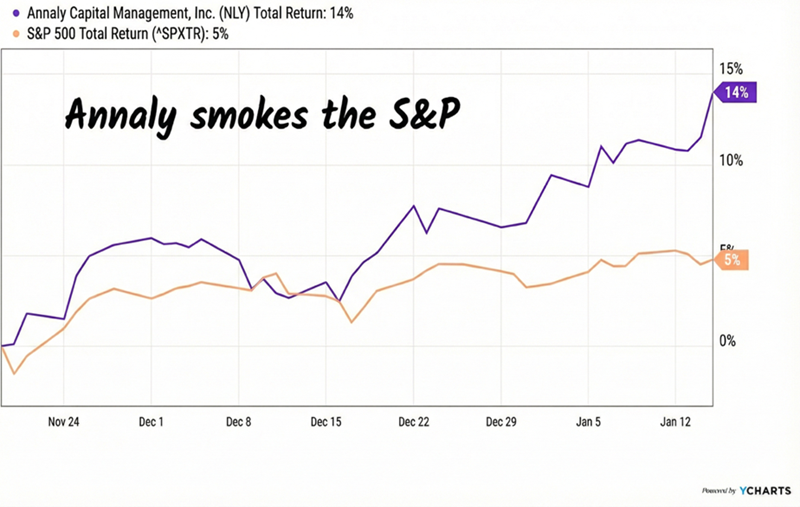

Two months ago, we recommended Annaly Capital (NLY) in these pages. Annaly dished a safe 12.9% dividend, well-funded by income. And the mortgage REIT (mREIT) had upside potential to boot.

Vanilla investors were worried about a recession, missing a time-tested maxim of income investing: As rates fall, REITs rise. This “rate-REIT seesaw” was about to tip and catapult Annaly’s price higher.

Here’s why. Annaly is a “financial landlord” which owns government-backed mortgages that rise in value as long-term rates fall. Those mortgage bonds that are essentially locked in at higher rates. So, as mortgage rates drop, the mREIT’s stash turns into a lucrative collector’s edition.

The stock was an interest rate trade rolled up in a tasty 12.9% payout wrapper. And rates drop anytime investors merely worry about a recession. It doesn’t matter if the slowdown comes to fruition or not!

I liked the trade so much that we doubled down a couple of weeks later, this time highlighting Annaly peer mREIT Dynex Capital (DX) as an additional play. Dynex paid 14.7% at the time and its management team was salivating over historically high mortgage spreads.

Since then, mortgage rates have dropped because the administration wants them lower to boost affordability and housing economic activity. With each tick down, Annaly and Dynex portfolio gained in value—exactly as we discussed.

Annaly has returned 14% in two months (115% annualized!) since its feature here in Contrarian Outlook:

Annaly Rallies 14% in 2 Months

Dynex has been solid too, rewarding investors with 5% gains (56% annualized) since we doubled down on mREITs.

If you bought these stocks, congratulations! If you missed them, rather than “chase” while they’re hot, let’s talk about the next income play.

We hear about AI nonstop. Chips. Models. Software.

But AI’s real constraint isn’t code. It’s electricity.

Every prompt, model update, and shiny new app runs on racks of servers in data centers. They don’t sip power. They chug it, huffing and puffing 24/7. And demand is rising far faster than supply.

Now Washington is stepping in.

Last week, the Trump administration and several Northeastern governors agreed on an unprecedented plan: force tech giants to fund new power plants themselves. The idea is simple. If Amazon, Microsoft and Alphabet want massive data centers, they’ll sign 15-year contracts to pay for the electricity—whether they use it or not.

That does two critical things for investors.

First, it sends the message that regular Americans won’t foot the bill for AI’s power binge. Data centers usually mean higher rates for residential and business users around them.

Second—and more important for us—the power proposal would create long-term, contract-backed revenue for power generators, grid infrastructure and utilities. This is exactly the kind of predictable cash flow income investors crave.

The proposal would support roughly $15 billion in new power plant construction, backed by guaranteed revenue contracts. This means utilities can borrow (usually at favorable rates) to build the additional electricity generated to keep rates down. Which boosts utility profits.

Reaves Utility Income Fund (UTG) gives us a diversified basket of these power companies to play this, with a nice payout! UTG is a closed-end fund built for income investors like us. We buy it, collect a 6.3% dividend paid monthly and don’t need to sweat individual utility earnings events thanks to the diversified portfolio.

A Steady 6.3% Dividend, Paid Monthly

The timing for UTG is ideal from a rates standpoint, too. Its utility holdings are bond proxies, which means they trade inverse to interest rates. As rates continue to decline, this group will rally as investors move cash from money market funds into it, likely boosting UTG’s price, adding to the total return.

AI chips need juice. UTG owns the power brokers that provide it. It’s the next “dividend train” about to leave the station. Don’t miss it.

The Snowball has a comparison share VWRP, with the same starting date of the Snowball, current value £152,766.00

Not too shabby performance, so although the ETF pays a dividend, VWRP is an accumulation Trust but the dividend is minimal but could be an option for part of your portfolio when the market sells off.

The current comparison.

VWRP using the 4% rule would provide a ‘pension’ of £6,110

The Snowball returned income for 2025 of £11,914.00 and the 2026 target is 10k.