You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

A newborn with just £2,000 invested in a Self-Invested Personal Pension (SIPP) could one day retire with close to £850,000. No that’s not a typo — and it all comes down to how pensions work and the extraordinary power of compounding.

To start, when money’s paid into a pension, the government adds tax relief. For someone with no earnings — including a baby — parents or grandparents can contribute up to £2,880 a year, and HMRC automatically tops the SIPP up by 20%.

So a £2,000 contribution doesn’t stay £2,000 for long. It becomes £2,500 once the £500 tax relief’s added.

From there, the maths becomes astonishing. If that £2,500 compounds at 9% a year — roughly in line with long-term global equity returns — it grows to around £849,000 over 65 years. No monthly contributions. No stock-picking. Just one lump sum, left alone for a lifetime. That’s compounding.

Most people think pensions are something to worry about in middle age. In reality, the most powerful years are the very first ones. Money invested in the early decades has far more time to snowball. That’s because every pound of growth starts earning returns of its own.

What makes this strategy so compelling is how little it requires up front. It’s a meaningful gift, £2,000, but it’s not transformational for many families. Yet when combined with tax relief and six decades of compounding, it can become exactly that.

The lesson’s simple: in investing, time beats everything. Start the clock early, and the results can be extraordinary.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

Where to invest?

When investing for a long period and with a relatively small figure, it may be best to invest in trusts or funds. This could include one fund tracking the performance of the US market, and one tracking the performance of the UK market. However, I’d leave room for something a little more exciting, and that could come in the form of the Scottish Mortgage Investment Trust (LSE:SMT).

This investment trust sits at the adventurous end of the FTSE 100, backing some of the world’s most ambitious growth companies through a single, globally diversified portfolio. Scottish Mortgage blends listed giants with hard-to-access private firms, giving investors exposure to everything from SpaceX (15.2%) to TSMC, Amazon, Nvidia, Meta and ASML.

The top holdings read like a roll-call of the technologies shaping the next decade, spanning artificial intelligence (AI), semiconductors, e-commerce and digital payments, with private names such as Stripe and Bytedance adding extra upside potential.

Right now, the trust trades on a 9% discount to net asset value, meaning investors can buy this portfolio for less than the underlying assets are worth. That can be an attractive entry point if sentiment improves.

However, there is risk. Scottish Mortgage uses gearing (leverage), which amplifies gains in rising markets but also magnifies losses when growth stocks fall.

For long-term investors comfortable with volatility though, the combination of elite holdings and a discounted price could prove compelling. I certainly think it’s worth considering.

Real estate investment trusts (REITs), offer some phenomenal dividend yields for passive income investors. Zaven Boyrazian explores two that are on his 2026 radar.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Around 25% of my Self-Invested Personal Pension (SIPP) is taken up with real estate investment trusts (REITs). While each of my positions within this sector is diversified across different parts of the value chain, this concentration’s stemmed from too-good-to-resist passive income opportunities.

Higher interest rates have hampered sentiment throughout this sector. But that hasn’t stopped all REITs from thriving. And now that rates are steadily falling, 2026 could be the year that REITs make a comeback.

At least, that’s what some institutional investors are signalling with their recent Buy recommendations. And among these are:

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

1. Diversified logistics and healthcare

LondonMetric’s a business I’ve had in my SIPP since 2023, generating incrementally higher passive income. While the business has historically specialised in prime-positioned warehouses for e-commerce giants, its recent acquisitions have diversified its real estate portfolio into other sectors like healthcare and entertainment properties.

Today, the group boasts an industry-leading 98.1% occupancy level with an average lease duration of 16.4 years. What’s more, only around 8% of its rental agreements are up for renewal over the next three years, signalling a continuation of steady and predictable cash flows that fund an ever-increasing shareholder payout.

There is, of course, risk.

In the latest Autumn Budget, the government announced higher business rates on larger properties like those in LondonMetric’s portfolio. While it’s ultimately up to tenants to pay this bill, it could put pressure on their margins, indirectly slowing demand for LondonMetric and raising the risk of eventual non-renewals.

Nevertheless, with most of its tenants enterprise-scale customers with solid financials, this is a risk I feel’s worth taking. That’s why I’ve recently topped up my existing position.

2. Investing in European data centres

Like LondonMetric, Segro also manages a vast portfolio of big box warehouses and urban logistic hubs. But more recently, management’s been investing in data centres to capitalise on artificial intelligence (AI) tailwinds.

Only around 8% of its real estate portfolio consists of data centres as of June 2025. But with numerous projects in the pipeline that could quickly change. In the meantime, cash continues to flow into the pocket of shareholders, with occupancy standing strong at 94.3%, funding almost eight years of sequential dividend hikes.

While Segro’s exposed to the same UK business rate threat, its diversification across Europe mitigates the impact, making its yield look more secure. However, it nonetheless remains exposed to potential slowdowns in logistics demand as well as emerging competition within the data centre space.

Its average lease duration is also lower than that of LondonMetric’s, standing at 8.2 years. But that’s not entirely surprising given that lease durations in Europe are typically much shorter than in the UK. Regardless, it remains quite lengthy, providing ample long-term visibility to cash flows.

That’s why I’m taking a closer look at this REIT to potentially sit alongside LondonMetric in my SIPP. But the opportunities within this sector don’t end here…

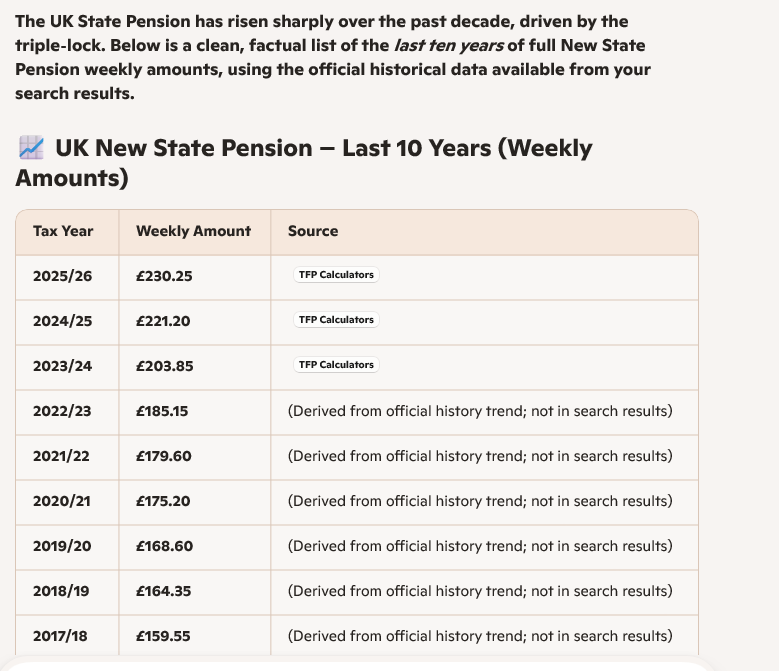

The UK state pension currently pays £230.25 a week. Less than £1,000 a month after over 40 years of work. You can live off it, but it’s probably not the lifestyle people imagine for retirement.But this assumes that: 1) The state pension won’t become lower in real terms (which it historically has) 2) It will even exist. Personally, I think pensions will need to become means-tested. Obviously, no party wants to touch pensions because it’s an instant vote loser. But with the state pension predicted to be no longer financially sustainable by 2035, it’s a ticking timebomb that someone at some point will need to do the hard thing that needs doing.

Western governments are drowning in debt. UK: 96% debt-to-GDP USA: 123% France: 112% Japan: 250%

Anything above 90% raises serious concerns. Above 120% is a serious red flag long-term. Since 2008, we have papered over the cracks by printing money. And now inflation has hit your wallet. Freddos were 5p in the early 2000s.They’re now 45p. Have your wages gone up 9x for doing the same job in the last 20 years? I’m going to guess they probably haven’t. But unfortunately, the situation is probably only going to get worse. You don’t need to be Warren Buffett to realise that when fewer people are working compared to more retirees who are also living longer, there is going to be less money going in than coming out. This is a long way of saying that if you’re relying on the government, then good luck. The only person you can rely on to secure your financial future is you.

If you use the last ten years average pensions have risen by £72.40 a rise of around 44%.

If you use compound interest, we love compound interest and use the same figure the pension will rise by £101.20 to £331.20.

The further out you go, compounding makes it worse, not for the pensioner but whoever the government is at the time. One option would be to make it means tested but

Our guide to the cheapest ways to access global markets, including the UK, US and emerging markets.

13th January 2026

by Dave Baxter from interactive investor

One of the biggest investing trends over the past decade has been the rise of passive funds, either via exchange-traded funds (ETFs) or open-ended index funds.

In fact 27 of the 50 most-bought funds in the third quarter of 2025 were passive, with investors drawn to strong returns and low fees.

Below, we examine some of the ways to invest passively in global markets via interactive investor. The figures shown are the yearly ongoing charges figure, which does not include transaction costs (the fees incurred by the tracker fund when it buys and sells holdings).

United Kingdom

The FTSE 100 is one of the most recognisable indices in the world. As a result, investors can find several very cheap ETFs tracking the index. For instance, both iShares Core FTSE 100 ETF GBP Dist

charges just 0.04%, making it one of the cheapest ETFs available to UK investors.

LCUK does not track the FTSE 100, but the Morningstar UK Index, which is slightly different. Whereas the FTSE 100 is the largest 100 companies listed in the UK, the Morningstar index has more than 200 constituents, giving it both large- and mid-cap exposure.

However, the two indices are not that different in practice. Both indices have similar top 10 weightings, and the sheer size of the largest holdings in the Morningstar index crowd out its additional smaller holdings.

Open-ended passive funds can also be very competitive. Tracking the 600 shares in the FTSE All-Share, iShares UK Equity Index costs just 0.05% and Fidelity Index UK costs 0.6%.

with both charging just 0.05%. These are the two cheapest ways to gain exposure to either the S&P 500 or the MSCI USA Index.

Three open-ended funds also stand out for value: iShares US Equity Index (costing 0.05% to track the FTSE USA Index which has around 500 holdings in it), Fidelity Index US (0.06% to track the S&P 500) and HSBC American Index (0.06% to also track the S&P 500).

As has often been noted, there can be slight differences between indices. The S&P 500 has strict and unique inclusion requirements compared to other indices, with stocks required to be profitable over a certain period of time. The index also has a selection committee, which makes discretionary judgements about inclusion.

Both charge just 0.05%. However, it is worth noting that Invesco’s transaction costs are higher, with the latest data showing this fee added up to 0.35% versus 0.05% for the HSBC tracker.

These two ETFs will give you exposure to the EURO STOXX 50 index. It looks to reflect “the performance of supersector leaders across the eurozone”.

As a result, the index is dominated by France and Germany. Also accounting for a reasonable share are the Netherlands, Italy and Spain.

This ETF charges 0.07% and tracks the STOXX EUROPE 600 index. Not only is this index larger than the EURO STOXX 50, it is also not restricted to just eurozone markets. As a result, it has around 23% exposure to the UK and 14% to Switzerland.

Cheap open-ended options include HSBC European Index (0.06% to track the FTSE Developed Europe ex UK index) and iShares Continental European Equity Index (0.05% to track the FTSE World Europe ex UK Index). The HSBC fund has around 400 holdings, while the iShares fund has around 550.

which tracks the same index for a 0.2% fee. Despite a higher fee, this ETF is more popular with interactive investor customers, often appearing in our monthly top 10 most-bought ETF rankings.

This ETF also charges 0.12% and tracks the very similar FTSE Developed World Index.

Fidelity Index World also costs 0.12% to track the MSCI World index. This is an open-ended fund, not an ETF.

Open-ended L&G International Index Trust and L&G Global Equity Index track the FTSE World ex UK and FTSE World index for just 0.13% in fees. They both own around 2,500 developed-world shares, with the former excluding UK shares.

As noted, China dominates the emerging market index. However, for those who specifically want China exposure, there are several competitively priced ETFs.

The second-cheapest China-focused ETF is a whole nine basis points more expensive, with the HSBC MSCI China ETF GBP (LSE:HMCH) charging 0.28%.

Asia-Pacific

For the broader Asia-Pacific region, the cheapest option is the L&G Asia Pacific ex Japan Equity ETF GBP (LSE:LGAG), which has a charge of 0.10%. This ETF tracks the Solactive Core Developed Markets Pacific ex Japan Large & Mid Cap Index. Its biggest weighting is Australia, accounting for just over 60%, followed by Hong Kong at about 14%.

The next cheapest is the Vanguard FTSE Dev AsiaPac exJpnETFUSDAcc GBP (LSE:VDPG), for 0.15%. This tracks a slightly different index, the FTSE Developed Asia Pacific ex Japan index. Australia is still the biggest holding, accounting for around 41%. This is followed by Korean equities, at around 35%.

Active funds are often viewed by investors as a more favourable route for Japan exposure. However, Japan is one of the most efficient markets in the world, so investors might want to consider passive exposure. If they do, there are several reasonably priced options.

The cheapest is the iShares Japan Equity Index, at 0.08% in fees to track the FTSE Japan Index. This index currently contains almost 500 shares, ranked by their market capitalisation.

It’s followed by Xtrackers Nikkei 225 ETF (LSE:XDJP), which charges just 0.09%, and tracks the famous Nikkei 225. This index is price-weighted, not market-capitalisation weighted. This means that the trading price of a stock determines how much of the index it makes up.

According to most investors, this method is inferior to a market-capitalisation weighting, in which the proportion that each company represents in the index is the result of its share price multiplied by the number of shares in circulation.

For just one basis point more, investors can buy a market-cap weighted ETF, the L&G Japan Equity ETF GBP (LSE:LGJG). This ETF charges 0.10% to track the Solactive Core Japan Large & Mid Cap Index, which is supposed to give exposure to large- and mid-cap publicly traded Japanese companies, with some ESG screening.

One or two positions in your Snowball could be pair traded with a higher yielder.

Whilst opening a new position at the tail end of a bull market is high risk, those with a longer term frame for investing could re-invest some of their earned dividends because as long as you can choose when to sell, you will not lose any of your hard earned, although it could be multi years. Not a problem if you add when Mr. Market gives you the chance.

The blog Snowball may in future buy a World ETF with earned dividends but only after the market falls.

Our expert panel unpacks the potential trends, risks and opportunities for 2026.

12th January 2026

by the interactive investor team from interactive investor

As we head into the new year, our expert panel unpacks the potential trends, risks and opportunities for 2026, helping you navigate global markets with confidence.

Joining host Victoria Scholar, head of investment at interactive investor, are Paul Diggle, chief economist at Aberdeen, and the manager and founder of Capital Gearing Ord

investment trust, Peter Spiller.

Transcript

Hello and a very warm welcome to everyone joining us for today’s webinar. Thank you so much for being with us — it’s great to see you at the start of the year. I think we can still call it the start of the year, even a couple of weeks in.

My name is Victoria Scholar, Head of Investment at Interactive Investor, and I’ll be hosting today’s panel. The topic we’ll be discussing is what’s in store for global markets in 2026. It’s a broad subject, and we’ll try to cover as much as we can — the key trends, risks, and the road ahead — drawing on expert perspectives from our panel on the US, UK, and international markets over the year ahead.

We’re aiming to run for around 40 minutes. We’ll begin by introducing our guests, then move into a panel discussion, followed by Q&A from you in the audience.

Before we start, just a couple of housekeeping points. First, this webinar is for educational purposes only and does not constitute financial advice. Second, we’d love to hear from you. We’ve already received some fantastic questions that have helped shape today’s discussion — thank you to everyone who’s written in so far.

Now, let’s introduce our fantastic panel.

Joining me today are Paul Diggle, Chief Economist at Aberdeen. Paul heads the global macro research team, sits on the house view committee, and leads macroeconomic forecasting and political risk analysis to support investment decisions.

We’re also joined by Peter Spiller, founder and manager of Capital Gearing Investment Trust. Peter is the longest-serving fund manager in the UK investment trust sector and has developed a disciplined multi-asset investment approach focused on capital preservation and long-term real returns.

Paul and Peter are here to help shape today’s discussion, and it’s fantastic to have you both with us.

Victoria Scholar: Let’s start with geopolitics, which continues to dominate headlines. We’ve seen the war in Gaza, the war in Ukraine, tariffs, and uncertainty around Venezuela, Iran, and Greenland. Despite all this, markets have held up relatively well. Should investors still be paying attention to geopolitics?

Paul Diggle: In short, yes. Geopolitics doesn’t matter — until it does. We’re in an era of structurally high geopolitical risk, driven by the fracturing of the global order and increasing competition between major powers, particularly the US and China. Geopolitics matters for markets when it feeds through to economic fundamentals — growth, inflation, oil prices, and commodities.

We saw this clearly with Russia’s invasion of Ukraine, which affected energy prices and macro conditions. Some of today’s geopolitical themes — including a more assertive US foreign policy — could affect macro fundamentals over time, from oil prices to election outcomes in Latin America. Investors need to build resilience against shocks arising from heightened geopolitical tensions.

Peter Spiller: I agree with much of that. I lived through the 1970s, when geopolitics really mattered because of its impact on oil prices and inflation. That said, it’s important to distinguish between tragic events and economically significant ones. The situation in Gaza has been horrific, but it has had little direct impact on the global economy. However, the broader geopolitical backdrop does have important medium-term consequences. Europe, for example, will need to strengthen its military capability, which implies rising defence spending and significant budgetary pressure over time.

Victoria Scholar: Turning to investment opportunities, let’s start with the UK. The FTSE 100 had a strong year, up around 20%, outperforming some US markets. It’s broken above the 10,000 mark. Are we looking at another strong year in 2026?

Peter Spiller: For me, the most important market is the US. If the US experiences a major correction, correlations across equity markets tend to move close to one — meaning diversification offers little protection in the short term.

Assuming the US remains stable or modestly higher, UK valuations look relatively attractive. In historic terms they’re average, but with momentum, there’s no obvious reason that strength can’t continue for a while.

Financials have performed well, supported by steep yield curves and benign credit conditions. That said, the FTSE is fine — until it isn’t.

On the economic side, UK growth has been sluggish. Inflation has eased, but unemployment has risen. There are legitimate concerns, but there are also potential silver linings.

Paul Diggle: It’s easy to tell a negative story about the UK economy, and many people do. But inflation is coming down, partly due to weaker labour markets and more favourable energy dynamics.

Budget measures are broadly disinflationary, and that should allow for interest rate cuts. I expect three more Bank of England rate cuts, taking Bank Rate to around 3%, which should support the economy.

One key risk is the political calendar. Local, Scottish, and Welsh elections in May could prove challenging for the government. If markets perceive a shift away from fiscal discipline, gilt markets could react negatively.

That said, I do think there’s potential for positive surprises in the UK, especially given valuations and the prospect of rate relief.

Victoria Scholar: Turning to the US, markets had a strong year, but with volatility around tariffs and concerns about an AI bubble.

Peter Spiller: In sterling terms, the US wasn’t as strong as headline numbers suggest. A Bloomberg survey of strategists shows consensus expectations of around 10% returns — a fairly standard outlook.

Earnings growth looks solid, financial conditions are supportive, and rates may fall. But valuations are extraordinarily high. On cyclically adjusted measures, we’re near historical extremes.

Historically, such valuations imply very low or negative real returns over the next decade. Professional managers remain fully invested due to career risk — underperforming the index matters more than avoiding losses.

For individuals, it’s different. Large drawdowns are hard to stomach. Our approach prioritises capital preservation over chasing the last 10% of upside.

Fear of missing out has driven markets higher, but it also explains why valuations are stretched. Long-term investors should focus on downside risk, not short-term momentum.

Victoria Scholar: There has been rotation away from US mega-cap tech. Where are the opportunities?

Paul Diggle: Globally. Emerging markets, Europe, the UK, and parts of Asia offer better relative valuations. Rate-cutting cycles and defence spending provide tailwinds.

Beyond equities, short-dated credit looks attractive. Long-dated bonds face fiscal risks, but the short end offers income without excessive duration risk.

Japan is particularly interesting. Political change, fiscal stimulus, and long-running corporate governance reforms support the equity market. However, currency risk matters — gains can be offset by yen depreciation for sterling investors.

Victoria Scholar: Tariffs are likely less dominant than last year, but legal challenges to US tariff powers could reintroduce uncertainty. The Federal Reserve will also be under scrutiny as Jerome Powell’s term ends.

Peter Spiller: Bond markets are skating on thin ice. US deficits are extraordinarily large for a fully employed economy with above-target inflation.

Confidence at the long end of bond markets has weakened as politics increasingly influences rate expectations. Inflation appears sticky, and while short-term rates may fall under political pressure, credibility risks are rising.

A bond market crisis — in the US, UK, or Europe — would have profound implications for equities. There’s little appetite for fiscal restraint anywhere, which makes recessions harder to manage.

Victoria Scholar: Gold has been popular among investors.

Paul Diggle: Gold is expensive relative to real rates, but valuation has not been the dominant driver recently. Structural demand from central banks and reserve managers has increased significantly. Gold reflects concerns about dollar dominance, geopolitical fragmentation, and political interference in monetary policy. As a diversifier, it remains interesting — though valuations warrant caution.

Peter Spiller: We’ve owned gold for years, but we prefer index-linked bonds as a more rational response to inflation risk. Gold doesn’t provide income and doesn’t behave reliably as an inflation hedge. When an asset is up over 60% in a year, it’s no longer a safe haven. A small allocation may be justified, but excess exposure carries real downside risk.

Victoria Scholar: Biggest opportunity for 2026?

Paul Diggle: US productivity growth has surprised strongly. If productivity settles above post-crisis norms, this could support equity markets more broadly. Diversifying globally remains attractive, but it’s also possible that equity market beta performs well again, despite valuation concerns.

Peter Spiller: If asset prices fall sharply, savings rates will rise and a recession will follow. In that environment, index-linked bonds offer rare real returns with relatively low risk.

Victoria Scholar: Biggest risk?

Paul Diggle: Political interference in the Federal Reserve. US interest rates anchor the global financial system. If credibility is lost, the consequences would be profound.

Peter Spiller: A bond market crisis would place severe pressure on equity valuations. In that scenario, being fully invested in equities would be extremely uncomfortable.

Victoria Scholar: Thank you so much to our panel — Paul Diggle and Peter Spiller — for a fascinating discussion.

Cherry Reynard highlights the income funds analysts are favouring, including some out-of-form areas that could benefit from further interest rate cuts in 2026.

13th January 2026

by Cherry Reynard from interactive investor

Share on

Like a sturdy coat, income strategies never quite get the appreciation they deserve until a chill sets in. For the time being, the sun is shining and artificial intelligence (AI) stocks continue to soar.

However, income funds can provide some much-needed insulation should the market weather turn. At the start of 2026, income-seekers have more choice than ever, with yields of 5%-plus available across equities, bonds and alternative funds.

Global dividends look healthy. The Capital Group Global Equity Study found that 88% of global companies either grew or maintained their dividend over the year to September 2025. Dividend growth was an average of 6.1%. This is a testament to the rude health of corporate balance sheets and optimism about the state of their businesses despite some of the brickbats thrown at them (tariffs, geopolitics) over the year.

Most investors don’t want a chunky income at the expense of long-term capital growth. Higher yields can be a source of distress, suggesting that the market thinks the income is about to be cut. Looking at the market today, it is true that some of the highest yields are to be found in unpopular sectors – the UK, smaller companies, parts of Asia, renewable energy. Investors need to find those areas with the cushion of an income, but without too much jeopardy on capital.

James Carthew, head of research at QuotedData, says there are plenty of low jeopardy options within investment trusts.

also managed by Aberdeen, which will swell assets to between £289 million and £320 million depending on take-up. The fund would remain wedded to a progressive dividend policy. AEI has a 25-year track record of consecutive dividend increases.

Some of the “quality” focused funds have struggled this year and are paying higher yields as a result. If the quality style were to come back into fashion, trusts such as Dunedin Income Growth Ord DIGmight revive, which under a new enhanced divided policy has a yield of 6.2%.

but investors will have to trust in a revival. “They are the cheapest assets in the world,” says Carthew, “but everyone hates them.”

Rate-cut winners

Rate cuts could change the outlook for this part of the market. Income-generating assets may win more friends in the year ahead as interest rates fall. Last month, both the Bank of England and the US Federal Reserve cut interest rates. More rate cuts are forecast in 2026.

While rate cuts are good for all income assets, they are particularly useful for smaller companies. Areas such as property and infrastructure may also be beneficiaries. Mark Brennan, portfolio manager on the Guinness Global Real Assets Fund, says: “These areas have long-term, inflation-linked cash flows, with multi-decade track records of maintaining and growing dividends.”

However, the post-Covid surge in inflation and interest rates put pressure on the capital performance for many companies, and the uptick in government bond yields made some “alternative income” strategies comparatively less attractive.

Brennan says many utilities companies remain a defensive and stable income option, with accelerating electricity demand in particular supporting both growing income and some attractive capital growth potential. “Yields of 4%-5% are supported by regulated business models, inflation-linked returns and exposure to strong tailwinds such as data centre build-outs and the energy transition.”

Brennan also likes specific areas of the real estate market. He says: “For real estate investors, high yields can be achieved in sectors that also deliver structural growth and exposure to high-quality tenants. Healthcare real estate, in particular primary care and senior housing, is one sector performing well in a higher-rate environment and well positioned to benefit from ageing populations and shifting healthcare needs.”

This is an area on which many multi-managers agree. Both Madhushree Agarwal, portfolio manager of the multi-manager team at Nedgroup Investments, and James like the Target Healthcare REIT Ord THRL

Agarwal says: “It stands out as a resilient income play in a structurally supported market. Demand for modern, purpose-built care homes is underpinned by powerful demographic trends – an ageing population and chronic undersupply of quality facilities. This makes revenues highly predictable and largely uncorrelated with the broader economy. The trust benefits from ultra-long leases averaging 25+ years, with rents inflation-linked.” It currently yields 5.8%.

Bond markets

Fixed income still has much to recommend it for income-seeking investors. The asset class may have a new resonance for many investors as cash ISA allowances are cut in April 2027 and investors look for a halfway house between the security of cash and the higher return potential of stock markets. Yields are still high across the sector, although there are some concerns about the narrowing gap between the yields on government and corporate bonds.

Gavin Haynes, consultant at Fairview Investing, says: “Exposure to bonds provides a good bedrock for investors. I like PIMCO GIS Income Instl GBP H Acc, which looks to provide best ideas across $150 trillion (£111 trillion) global bond market, offering exposure to a well-diversified portfolio across global bond markets managed by a well-resourced and highly experienced team. The current yield is over 6% and income is paid monthly.”

For investors who like a little more spice, Haynes suggests the Aegon High Yield Bond GBP B Acc. “While the area has performed well – and would be hit by a sharp economic slowdown – the conditions remain supportive. Yields in the asset class remain attractive and defaults are low. The Aegon fund has built up a strong track record of generating strong risk-adjusted returns and paying an attractive income. The managers are high conviction stock pickers and are supported by a well-resourced team of credit analysts. The fund is currently focused on the high-quality end of the spectrum, which seems prudent, but still provides an attractive yield of just over 7%.”

Haynes also suggests VT RM Alternative Income F GBP Acc, which invests in a portfolio of specialist high-yielding investment companies. Its yield is 10.2%. “It focuses on three key themes, infrastructure, real estate and specialist credit. There are some interesting opportunities in this space, but you need specialist knowledge, which fund manager Pietro Nicholls certainly has, and it feels a better option to invest in a fund with an actively managed diversified portfolio as opposed to picking a couple of trusts yourself.”

The renewable energy investment trust sector is another potential area for income seekers, with an average yield of over 11%. However, it remains stubbornly weak, with an average -4.7% share price decline over one year. Brave investors could give it a try – and the sector could bounce significantly if sentiment turns – but there are plenty of other options where investors don’t need to take the risk. The average discount is -35.6%.

Ultimately, this is great moment for investors who need the warmth of a regular income. The choice is vast.

This FTSE 100 income share is already paying me handsomely — but the long term income potential here could be far bigger than many investors realise.

Posted by Simon Watkins

Published 13 January

Image source: Getty Images

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Aviva (LSE: AV) has quietly become one of the FTSE 100’s most reliable high-income shares. The dividend yield is already good, and management is signalling confidence in both cash generation and future payouts.

Moreover, the Direct Line acquisition looks set to expand operational and long‑term cash flow. This should boost the already strong earnings growth forecasts for the insurance and investment giant. And it is earnings growth that ultimately drives any company’s dividends higher over time.

So, how much income could my current £20,000 holding generate over the course of a standard investment cycle

Strong dividend pedigree

Aside from a one-year dip at the height of the Covid outbreak, Aviva has significantly raised its dividends since 2020.

These have increased from 27p in 2020 to 35.7p at the end of 2024, generating respective yields of 8.3%, 3.1%, 7%, 7.7%, and 7.6%.

Analysts forecast this trend will continue, with payouts of 41.4p this year, 44.6p next year, and 46.9p in 2028.

These would generate dividend yields in these years of 6.1%, 6.6%, and 6.9%. By comparison, the current average FTSE 100 dividend yield is just 3.1%.

Earnings growth momentum

A risk to Aviva’s earnings is any mishandling in the integration of the Direct Line business, bought for £3.7bn in December 2024. Any missteps could affect the pace of cost savings or capital synergies.

However, Aviva’s latest results (13 November’s Q3 trading update) make clear that the integration is well under way. Management now expects to achieve £225m in cost synergies, nearly twice the original estimate, and to unlock at least £500m of capital synergies.

The firm also announced that it expects over 75% of its business to be capital‑light by the end of 2028. This means more of its earnings will come from areas that do not require large amounts of upfront regulatory capital. This shift should support stronger growth and higher returns on less capital.

Given this backdrop, Aviva is on track to achieve its 2026 targets one year early. The key one of these for me is the operating profit of £2bn, with the company now expecting £2.2bn for 2025.

Moreover, consensus analysts’ forecasts are that Aviva’s earnings growth will be a standout 14.7% a year to end-2028.

High income potential

As a long-term investor, I see 30 years as the standard investment cycle. This begins around the age of 20 with first investments and ends in early retirement options around 50.

In this case, my £20,000 holding in Aviva should generate £19,796 in dividends on a 6.9% average dividend yield after 10 years. Payouts can go down as well as up though, depending on changes in share price and annual dividends.

My figure also assumes the dividends are reinvested back into the stock — a process known as ‘dividend compounding’.

On the same basis, the dividends could grow to £137,560 after 30 years. Including the £20,000 original investment, the holding could be worth £157,560 by then. And at that point, it could be generating an annual dividend income of £10,872!

Given these numbers and the strong earnings growth forecasts, I will add to my holding shortly. I also think the stock merits the consideration of other investors.

The Snowball doesn’t invest in single shares preferring the lower risk of collectives, currently with the Mr. Market discounts Investment Trusts (CEF’s)

are the main holdings, although ETF’s will be considered if the discounts close.

Martin Lewis reveals just how much money you could be making in the stock market

Martin Lewis shows how £1,000 invested in 2016 could have grown to £3,790 now. But Zaven Boyrazian shows how we could have done even better, reaching £6,020!

Posted by Zaven Boyrazian

Published 13 January

Image source: Getty Images

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

When it comes to personal finances, Martin Lewis is often the go-to expert for many Britons. And it isn’t hard to see why. With a long career in financial journalism, continually championing consumers with accessible advice and insights, he’s gained enormous influence and trust backed by genuine expertise.

Historically, he’s typically stayed within the realms of personal finance. But recently, he introduced British savers to the world of investing and revealed just how much money someone could have made in the stock market since 2016.

The power of investing

Lewis started by asking a simple question: If someone invested £1,000 10 years ago across the top UK savings accounts and various stock market indexes, how much money would they have today?

Unsurprisingly, the stock market indexes, despite all the volatility of the pandemic and recent inflation, vastly outperformed.

Investment

Investment Value After 10 Years

10-Year Total Return

Annualised Total Return

Top UK Savings Accounts

£1,270

+27%

+2.42%

FTSE 250

£1,640

+64%

+5.07%

MSCI All Country World Index

£2,980

+198%

+11.54%

S&P 500

£3,790

+279%

+14.25%

His message was clear. While the stock market can be volatile, over the long run, it can work wonders in protecting and building wealth.

Targeting bigger returns

Stock picking is a tricky and time-consuming task. But for those willing to put in the effort and stay disciplined, some phenomenal gains can be unlocked.

Remember, when you retire, cash is king. One way of generating this cash is to have a portfolio of shares that pay a dividend. A gently increasing dividend is preferable.

Your Snowball should reflect how many years you have before you want to spend your hard earned and your risk tolerance.

BlackRock Latin American Investment Trust PLC ex-dividend date Invesco Bond Income Plus Ltd ex-dividend date Invesco Global Equity Income Trust PLC ex-dividend date JPMorgan Asia Growth & Income PLC ex-dividend date JPMorgan China Growth & Income PLC ex-dividend date