But experts claim there are still reasons to back real estate, especially with the prospect of interest rate cuts in the coming weeks.

Big themes for investors include the return-to-the-office and the rise of online shopping.

Daniel Austin, chief executive and co-founder at specialist property lender ASK Partners, said: “The 2025 Autumn Budget offered limited stimulus for the housing market and, persistent headwinds such as sticky inflation, higher for longer interest rates, elevated construction costs, and slow planning processes continue to impact development viability.

“But there are still reasons for cautious optimism. The UK economy is forecast to grow by 1.4% this year. This is expected to outperform the eurozone and should support investor confidence.

“The UK also remains an attractive destination for global capital, with ongoing interest from the Gulf, Southeast Asia and deepening UK United States investment links, particularly through the technology sector.”

Here are the emerging trends in real estate for 2026 and how to invest in them.

Prime offices

Many companies are reducing remote working and getting staff to be in the office more frequently.

Austin suggests businesses are competing for modern, energy efficient and amenity rich workplaces that support hybrid working.

He said: “Best-in-class offices in central London continue to achieve strong rents and stable yields.”

The rise of build-to-rent

The UK housing market continues to be hit by a lack of supply.

The government is pushing planning reforms through parliament to boost development but there are also fears that landlords could exit the market due to new rental regulations and higher taxes.

Build-to-rent – developments typically run by large institutional landlords – may fill that gap, providing an opportunity for investors. You may already have some exposure to this through your pension.

Austin said: “With so many smaller landlords exiting the sector due to increased costs and regulatory complexity, professionally managed rental formats are becoming more important. Build-to-rent and co-living are particularly well positioned to serve younger, mobile workers who seek affordability, connectivity and community. Mid-market suburban and commuter belt schemes may outperform prime central locations, especially in areas benefiting from new infrastructure such as the Lower Thames Crossing.”

Storage and logistics

Demand for storage and logistics is being driven by the growth of online retail as well as the growing adoption of artificial intelligence, cloud services and high-performance computing.

This means there is more demand for industrial sites to store goods for online deliveries and also hard drives to power cloud software.

Austin said: “Growing adoption of artificial intelligence, cloud services and high-performance computing is placing unprecedented pressure on power capacity and suitable land, making data centres an increasingly strategic real estate category.

“The combination of long-term contracted income, critical infrastructure status and limited supply of appropriate sites means this segment is likely to remain strong. Mixed-use industrial schemes that accommodate logistics, data infrastructure and urban services will offer particularly attractive, income-led opportunities in 2026.”

Hotels and hospitality

The transformation of under-utilised office buildings into hotels are creating new avenues for investors, according to Austin.

He said: “The asset class continues to appeal to private investors and family offices seeking income diversification and long-term value.”

Income producing operational real estate

Operational real estate, including healthcare, specialist care, education and supported living can provide stable and inflation-linked income streams.

Austin said: “Demographic shifts, including an ageing population and rising demand for specialist services, support the long-term resilience of these sectors.”

How to invest in real estate

Unless you are a property developer or landlord who can afford to build or manage one of these assets, one of the most common ways to gain exposure to real estate assets is through real estate investment trusts (REITS) or property funds.

Oli Creasey, head of property research at Quilter Cheviot, said: “The REITs own a portfolio of properties worth a certain value, and shares in the companies are traded on stock exchanges throughout the day.”

Most specialise in a particular sub-sector.

Creasey highlights Derwent London and GPE for development and ownership of London offices, while Big Yellow and Safestore are self-storage specialists.

Investors can get access to health care developments through Primary Health Properties and Target Healthcare, which owns senior living centres.

Meanwhile, Unite Group backs student accommodation, while Grainger does general residential rental.

For buyers not looking to specialise, Creasey says there are several funds that buy REITs but use them to create a more diverse portfolio including Columbia Threadneedle;s Property Growth and Income as well as TIME’s Property Long Income and Growth funds.

There are also funds that create a diverse portfolio around a thematic approach such as Schroder’s Global Cities fund which invests in REITs worldwide that own assets located in the top cities globally, while Gravis’s Digital Infrastructure fund invests in REITs that are aligned with the ongoing technology revolution.

Ben Yearsley, director of Fairview Investing, suggests a broad based fund or trust that then leaves the sector and stock decisions to the fund manager is better than trying to gain direct exposure.

His favoured option is the TR Property investment trust managed by Marcus Phayre-Mudge.

Yearsley said: “It has a mix of UK and European property shares.

“Valuations are cheap and no one is interested on the sector. In addition with no speculative development in the past decade there are shortages of good quality property in many areas.”

For a sustainable option, Daniel Bland, head of sustainable investment management at EQ Investors, suggests the Schroder BSC Social Impact Trust, which backs social housing.

Investors Hate This Market (and They’re Dumping This Great 9% Payer)

by Michael Foster, Investment Strategist

Today we’re going to talk about a subject that might seem a little outside the dividend plays we normally discuss.

But as you’ll see, this topic – a big shift in how Americans feel – is the main reason why some of our favorite high-yielding closed-end funds (CEFs) are woefully underpriced, like one equity-focused 9%-yielder with an incredible track record.

Let’s start with that unlikely topic: Happiness. It matters because, as we’ll see, how happy Americans are ties directly into investing behavior in very predictable ways.

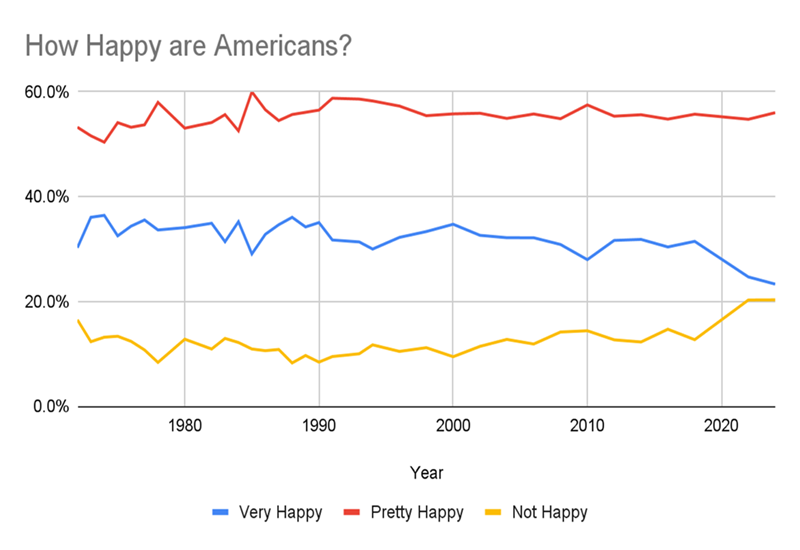

Source: CEF Insider This chart shows the results of the General Social Survey, from the University of Chicago’s National Opinion Research Center. It’s one of the oldest studies of Americans’ views on different social, political and cultural issues.

When asked “How happy are you?” the majority feel pretty happy. That’s been true since the survey started asking this question in 1972.

But look at the yellow line, showing how many Americans are not happy. It reached a new high in 2022 and is stuck there. Similarly, the percentage who are “very happy” has fallen to a new low and is trending further down.

If these trends continue, the percentage who say they’re unhappy will climb above those who are very happy for the first time in history. That’s a big psychological shift, and markets haven’t caught on to it yet.

Consumers Get the Blues

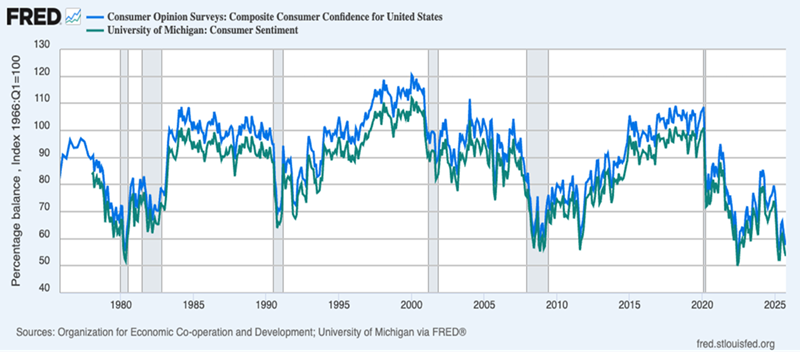

Now let’s get into why this trend is a financial risk. This chart is our first stop.

Here we have two measures of consumer confidence, one from the University of Michigan (in green) and one from the OECD (in blue). As you can see, these tend to drop during recessions (the gray sections above) and rise after, which makes sense.

There are exceptions, like in 1992 and in 2011, when consumer confidence cratered following the recessions that preceded them. Back then, consumers clearly worried that recent bad times would return.

But we’re now five years out from the last recession, and consumer confidence is stuck below where it was even during the pandemic! In other words, people feel worse about the economy now than they did when they were literally in quarantine.

That’s strange, and it demands a closer look because, at least economically, it makes no sense. Unemployment is much lower than it was during the pandemic and remains historically low. Incomes and wealth are rising, breaking trends that lasted two generations, as we’ve recently discussed.

So we’re left with one conclusion: People are just more miserable than they used to be, and it’s causing them to respond more negatively to surveys than they used to.

This makes sense, since the pandemic’s aftermath sent inflation soaring and AI has boosted worries about many things, including job loss.

The Data Has Changed. Wall Street Hasn’t

This all matters because people who make major economic decisions rely on data like this. I know because I spent over a decade consulting with hedge funds and investment banks on how to create just these sorts of studies.

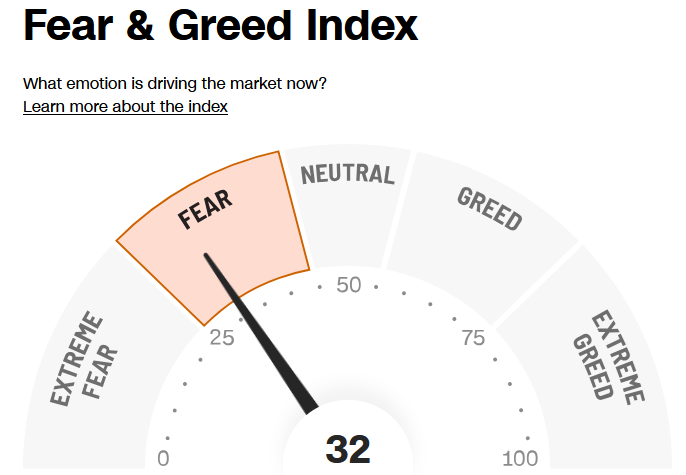

This ties into our income (and portfolio value) in two ways. First, a lot of survey-driven research is less reliable than it used to be – including the oft-cited CNN Fear & Greed Index.

Source: CNN.com For a while now, it’s been saying that investors are fearful. But if so, why have stocks climbed to near all-time highs? This index clearly needs adjusting, because what counts as “fear” is now a lower number than it used to be.

As a result of this shift, negative attitudes are no longer useful indicators of when a selloff will start.

Of course, this also means that when the market sells off because everyone’s worried that attitudes are souring, we contrarians get a chance to profit. Consider how the market tanked in 2022 because most investors expected a recession, but then no recession came. Or how tariff worries sent markets into freefall in April, but nothing major has happened since.

Selling because the market is getting fearful doesn’t work anymore, but buying when the market has whipped itself into a frenzy does.

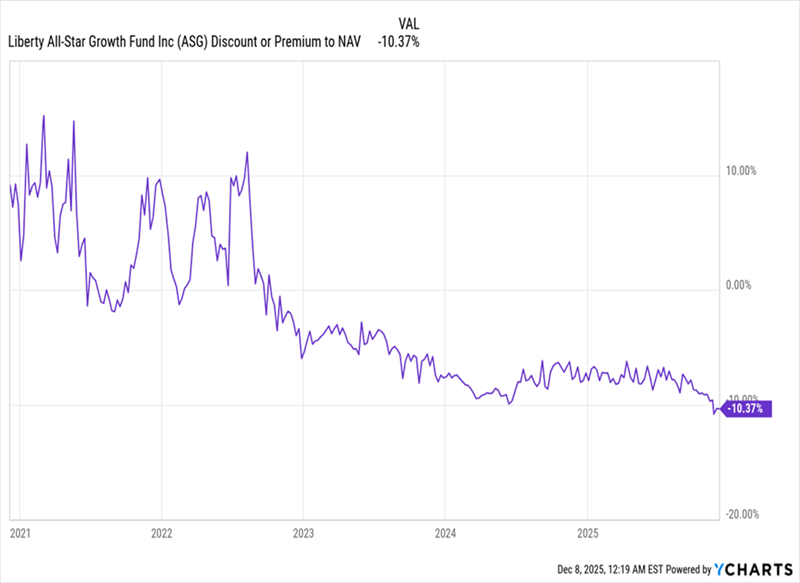

ASG: The Poster Child for Our New Pessimistic Era We see this playing out with CEFs, where discounts to net asset value (NAV) are deeper because risk-averse investors, who tend to be most interested in CEFs, pull back when sentiment sours. A broad drop in happiness, then, can make them more cautious, sending CEF discounts to deeper levels than the fundamentals justify.

As a result, the Liberty All-Star Growth Fund (ASG) has seen its discount drop below 10% in 2025, far below the last decade’s average of a 2.2% discount. That’s despite the fact that ASG has earned a 10.2% annualized return in that time and yields 9% today.

It’s a CEF Insider holding I talk about a lot because, despite the “growth” in its name, it pays us that 9% dividend (which does move around a bit, as it’s tied to the fund’s NAV). ASG also holds a nice mix of large- and mid-cap stocks. Top holdings range from Apple (AAPL) to New York State retailer Ollie’s Bargain Outlet Holdings (OLLI).

Eventually, history suggests that CEF investors will realize we live in a new era where sentiment is lower than it used to be, simply because these are more pessimistic times.

At that point, they’ll likely see that these discounts have gotten too wide and bid them up. If we buy ASG today, we’d be nicely positioned to beat them to the punch – and collect that rich dividend while we wait for this to happen.

GCP says ‘now attractive time to invest’ as net asset value picks up

Thursday, December 11, 2025

GCP Infrastructure Investments Ltd on Thursday announced an unchanged annual dividend as it posted a higher net asset value total return, with material policy support for infrastructure meaning that ‘now is an attractive time to invest.’

The firm is advised by Gravis Capital Management Ltd, the closed-ended investment company aiming to pay dividends and preserve capital from exposure to UK infrastructure debt and similar assets.

GCP said net asset value per share as at September 30 fell 3.6% to 101.40 pence from 105.22p a year prior.

NAV total return for the financial year ended September 30 was 3.1%, higher than 2.2% in financial 2024.

The company said: ‘The main factors driving asset valuations during the year included project specific factors, renewables generation and changes to discount rates applied by the company’s independent valuation agent.’

The dividend for financial 2025 was 7.0p, unchanged from a year ago.

Looking ahead, GCP said: ‘The recent UK autumn budget is unlikely to have a material impact on the company. Investors remain concerned by the UK’s long-term prospects and have generally been reducing allocations to long-duration UK exposure, which has impacted demand for the company’s shares.

‘The combination of interest rates and material policy support for infrastructure means now is an attractive time to invest, whilst maintaining an awareness of the political risks. The opportunity to lock-in attractive risk adjusted returns given the interest rate backdrop and invest early in some of the new sectors the UK government is supporting is something the company has done successfully during its 15 year life.’

GCP shares were 0.6% higher at 71.09 pence each on Thursday morning in London.

Copyright 2025 Alliance News Ltd. All Rights Reserved.

This year marks the Company’s 15th anniversary since IPO and I would like to take this opportunity to thank shareholders for their ongoing support. During this time, the Company has delivered a total NAV return of 185.2% and has achieved the objectives set out at IPO of generating income, preserving capital and diversifying across a range of asset classes.

The Company continues to pay a stable and sustained dividend, underpinned by an operational and diverse portfolio of UK infrastructure assets, paying a dividend of 7.0 pence per share in line with the target for the 2025 financial year. I am pleased to confirm that the same target1 is reaffirmed for the forthcoming financial year.

The objectives of the capital allocation plan have progressed, albeit slower than hoped or anticipated. The Company has generated total disposal and cash proceeds of c.£80 million from the realisation of various renewables assets, and portfolio equity exposure has been materially reduced. Leverage has been reduced from £104 million at the time of the announcement of the plan to £20 million at 30 September 2025 and furthermore, £35.6 million has been returned to shareholders through the buyback programme. The Investment Adviser is actively progressing transactions that, if completed, would materially complete the objectives set out in this plan.

Following publication of this annual report, and completion of the capital allocation plan, the Company intends to engage with shareholders early in 2026 to propose a future strategy for the recycling and use of capital.

1.The dividend target set out above is a target only and not a profit forecast or estimate and there can be no assurance that it will be met.

GCP current dividend yield 9.9%.

If you have a dividend re-investment plan, it’s your duty to check the fcast for next year and if the fcast dividend is paid.

Dividends went out of style in the pandemic. It’s great to see them back, says Rupert Hargreaves

“The true investor… will do better if he forgets about the stock market and pays attention to his dividend returns.” – Benjamin Graham

Dividend income has always been one of the key contributors to equity-market returns, especially in periods of volatility or bear markets. In the 1970s and 2000s, both periods of significant market volatility for the S&P 500, virtually all of the index’s returns came from income, according to data compiled by Bloombergand Guinness Global Investors. In the 1970s, the index recorded growth of 76.9%, with 17.2 points coming from price appreciation and 59.7 from dividend income. In the 2000s, the index fell by 24.1%, but dividends added 15 points for a total return of -9.1%.

The longer one stays invested, the more critical dividends become. Guinness Global’s data, going back to 1940, reveal that, over rolling one-year periods, the total contribution from dividend income to total return was just 27%, but that number grew to 57% over a rolling 20-year period. They also reveal that $100 invested at the end of 1940, with dividends reinvested, would have been worth approximately $525,000 at the end of 2019, versus $30,000 with dividends paid out. In this period, dividends and dividend reinvestments accounted for 94% of the index’s total return.

Get 6 free issues + a free water bottle

Stay ahead of the curve with MoneyWeek magazine and enjoy the latest financial news and expert analysis, plus 58% off after your trial.

The same trend has been observed in the UK. Between 1 January 2000 and 31 December 2019, the FTSE 100delivered an average annual return of just 0.4%. However, if you include dividends, the index has actually returned 122% over the same period (or 4% a year), according to Schroders’ calculations.

Headwinds for dividend stocks during the pandemic

Still, there’s a reason the figures presented only go up until 2019. Since the pandemic, this relationship has broken down. The latest data from S&P Global show that, since 1926, dividends have contributed about 31% of the total return for the S&P 500, while capital appreciation has contributed 69%. That’s mostly down to the performance of the past five years.

Since the end of 2021, dividend stocks, as defined by the S&P 500 Dividend Aristocrats index – S&P 500 constituents that have followed a policy of increasing dividends every year for at least 25 consecutive years – have produced a total return of just 9% a year compared with 15.6% for the broader S&P 500 index. This decade, dividends have added just 12% to the S&P 500’s total return, the lowest contribution on record, says Hartford Funds.

As Ian Lance, co-manager at the Redwheel and Temple Bar Investment Trust, notes, equity returns have been “driven by a positive re-rating of equities, particularly in the US and particularly in technology stocks”. Dividend stocks were also hit disproportionately hard in the pandemic years. During 2020, $220 billion of dividends were either cut or paused, according to Janus Henderson.

Research by Goldman Sachs found that more than 80% of US dividend exchange-traded funds (ETFs) underperformed the S&P 500 during the 2020 equity drawdown period, and half of them did not bounce back as strongly as the index in the subsequent recovery.

Dividend stocks also “tend not to perform well when interest rates rise”, as Alan Ray, investment trust research analyst at Kepler Partners, notes. “Investors drawn to conservatively managed dividend-paying companies when interest rates were close to zero now find they can buy ‘risk-free’ UK gilts with yields of 4% or 5%, or even just keep cash in a savings account,” says Ray.

When to trust the dividend yield

Despite the headwinds for dividend stocks over the past five years, history shows they can be a safe haven in periods of volatility and uncertainty. What’s more, many income stocks are now trading at relatively undemanding valuations compared with their growth peers, suggesting there’s a bigger margin of safety with these equities in the event of a market downturn.

There’s no official definition of what makes a good income stock, but there’s one thing most of the research on the topic agrees on, and that’s a correlation between yield and quality, or rather the lack of it. While a dividend stock with a high yield might seem attractive as an income play, more often than not the yield is a reflection of traders’ doubt about the sustainability of the payout.

As Martin Connaghan, co-manager of Murray International Trust, notes, “there is no point in being drawn in by a high dividend yield… because that yield is most likely unsustainable and hence false. Stocks that have, on the face of it, very high yields can be vicious value traps if dividends are subsequently cut.”

In fact, research shows that, rather than chasing high yields, investors should instead look to companies offering yields around the 2% to 4% mark. Yield itself should not be used as a gauge of quality. The best way of evaluating the sustainability and quality of a dividend payout is to analyse the quality of cash flows. In business, cash is king. Cash flow gives a good indication of management’s approach to capital allocation.

As Imran Sattar, portfolio manager of the Edinburgh Investment Trust, notes, “For stocks with higher yields it is important to understand the sustainability of that dividend, how much the dividend is covered by earnings and free cash flow, or ongoing capital generation in the case of a bank… and also to think about whether there is anything on the horizon that could change the cash-flow dynamics such as an increased need for investment.”

This view is echoed by Connaghan, who says, “The ability to sustain and grow dividends is essential. Companies with a high cash-conversion ratio, dividend cover and free cash-flow yield should be in a much stronger position to do this.”

Free cash flow is generally defined as the cash flow generated by operations, excluding the costs of running the business and capital expenditures. In a traditional capital allocation framework, if a firm has free cash to spend, it should first reinvest it back into its operations if it can achieve an attractive and sustainable return on investment. If this opportunity is not available, the company should use the money to reduce debt, and if it has no debt, return the money to investors.

Cash flow figures give us a real, unabridged version of what management is doing with a company’s funds. Investors often turn to earnings before interest, tax, depreciation and amortisation (Ebitda) as a proxy for cash flow, as that’s the metric companies usually like to present. However, this ignores essential business costs, such as the replacement of capital equipment, interest on debt and taxes.

Similarly, a simple dividend cover calculation, which generally takes earnings per share divided by the dividend per share, also provides a misleading picture. Earnings per share do not account for all capital expenditure, particularly on long-term assets, which can be extremely costly for capital-intensive companies. When a company pays a dividend, the money leaves the business. That means the capital must be truly surplus to requirements to prevent problems emerging at a later date.

History is littered with companies that have paid out too much during the good times and have struggled with weak balance sheets and a lack of shareholder support in the bad.

The best dividend stocks

The best dividend stocks are those in companies that strike a balance between operational costs, including capital expenditures, and prudent balance-sheet management, along with sensible dividend policies. And they avoid the damaging concept of a “progressive dividend policy”. Progressive policies envisage the dividend rising steadily year after year. They are designed to provide security for investors. In fact, they do the opposite.

Companies always have and always will go through cycles, and making a commitment to increase a dividend year after year, no matter what, forces management into wrong decisions. It’s difficult to cut a dividend when such a policy is in place, which often puts firms in difficult positions, having to pay out more than they can afford.

Some of the most sensible dividend policies are based on small regular payouts, with annual special dividends based on profit throughout the year. This gives more flexibility, allowing management to announce additional distributions as needed without putting undue stress on the balance sheet. Managers can also choose to alternate between dividends and share buybacks, the latter being easier to turn on and off depending on the business environment.

FTSE 100 insurance giant Admiral is an excellent example. Car insurance can be a volatile and unpredictable business. It moves between a hard market when insurance prices are rising and profits are plentiful and a soft market where competition intensifies, prices fall and insurers have to stomach big losses. Managing a business through this cycle requires financial flexibility and a strong balance sheet, so Admiral cannot afford to commit itself to an unsustainable dividend policy. Instead, it commits to distribute 65% of its post-tax profits annually as a regular dividend, supplementing these distributions with special payouts.

For example, for the first half of the year, Admiral declared a regular dividend of 85.9p per share and a special dividend of 29.1p per share, for a total distribution of 115p, or 88% of post-tax profit. This was a pretty hefty interim distribution for the group. In 2021, a bumper year following the pandemic, which forced a change in driving habits and a substantial reduction in accidents, the company’s annual dividend payout reached just under 280p per share. However, in the following years, as drivers returned to the road and started crashing into each other, the company reduced its distribution in line with falling profits. For the 2023 financial year, it paid out just 103p across both its interim and final dividends.

Another example is CME Group. It pays a regular quarterly dividend, equivalent to a yield of about 2% per year. It supplements this with a special distribution at the end of the year based on annual trading performance. Last year, for example, the company paid out four regular dividends of $1.15 per share and one final special dividend for the year of $5.25.

The perils of a regular dividend policy became all too clear in the mining sector back in 2016. That year, commodity prices slumped as China’s previously meteoric growth started to splutter to a halt, leaving mining giants such as BHP, Rio Tinto, Glencore and Anglo American in a difficult position. Not only had these companies made a commitment to hefty, regular, progressive dividends based on past profitability, they had also spent and borrowed heavily to fund growth.

As commodity prices and revenue plunged, something had to give. BHP cut its interim dividend by 75%, the first cut since 1988, and abandoned its progressive dividend policy. Rio also slashed its dividend in half and Glencore was forced into a messy restructuring involving a $2.5 billion cash call, as well as a dividend cut.

In another example, BT had to cut its dividend in 2020 when management realised the company needed to spend more on its fibre build-out to keep up with the competition. This was a big blow for income investors as prior to the cut BT was often touted as one of the UK market’s top income plays.

Where to hunt for dividend income

Sensible capital allocation is a good indicator of dividend quality, as is the overall quality of the business. Quality can be defined in many different ways. Warren Buffett summed it up quite well in his letter to shareholders of Berkshire Hathaway in 1996: “Your goal as an investor should simply be to purchase, at a rational price, a part interest in an easily-understandable business whose earnings are virtually certain to be materially higher five, 10 and 20 years from now.”

To put it another way, a quality company is one that has a strong competitive advantage and a long runway for growth. A strong competitive advantage also typically translates into higher-than-average profit margins, providing the company with ample cash to invest in marketing, growth and debt repayment, and to return funds to shareholders.

James Harries, co-manager at STS Global Income & Growth Trust, says the best income stocks are “predictable, resilient, high-quality businesses” you can “say something sensible about on a five-,seven- and 10-year view”. That often means sticking with the companies that he describes as “steady as she goes” – they often “grow slower, but [grow] more persistently”.

A great example of the strategy, and a recent addition to the portfolio, is Nike. “It’s the highest quality global sports brand,” notes Harries, and though the company is going through some turbulence, “I’m pretty confident that we’re buying a really high-quality asset at a very attractive valuation”. Nike is one of the best-known and valuable consumer brands in the world, boasts a gross profit margin of more than 40%, and has billions of dollars in net cash on the balance sheet. It’s also rewarding shareholders, with $591 million in dividends in the first half of 2026 and $18 billion returned via share buybacks since June 2022.

The utilities sector can also be a good place to hunt for income. “Often a utility company operates in a regulated sector that is supported by a long-term concession contract, which will stipulate the return that can be generated over the life of the concession,” notes Jacqueline Broers, co-portfolio manager at Utilico Emerging Markets. As a result, cash flows can be more “resilient” and “predictable” than those of other sectors. “All of which translates into a more sustainable long-term dividend payout.”

Broers highlights the example of IndiGrid Infrastructure Trust, which owns 41 power projects comprising 17 operational transmission projects, three greenfield transmission projects, 19 solar generation projects, and battery energy storage (BESS) projects located across 20 states and two union territories in India. The average remaining contract life on the company’s transmission assets is just under 26 years, with contracted revenues underpinning the company’s dividend yield of about 10%.

The other advantage utilities tend to have is the prohibitive replacement cost of their assets. Take UK-based National Grid, which owns the majority of the UK’s high-voltage transmission network, comprising thousands of miles of cables and transmission stations. Building these assets from the ground up would be virtually impossible today, not to mention the vast cost. That gives the company a robust competitive advantage.

Utilities aren’t the only companies that can have such an edge. Connaghan points to the likes of Grupo ASUR, a Mexican-listed airport operator with 16 assets across Central and Latin America. “Its key asset is Cancun airport and the company has seen its passenger numbers increase by a compound annual growth rate of 6% over the last 35 years,” he says. “Such was the financial strength of this business in the earlier part of this year that in April, they announced two 15-peso special dividends in addition to a regular dividend of 50 pesos. This put the stock on a 14% dividend yield.”

The fund manager also highlights the likes of Enbridge, a Canadian pipeline business which transports and stores natural gas and oil through its network, which spans North America. The company has grown its dividend for 30 years in a row. “This type of business is far less exposed to the underlying shifts in the commodity prices themselves, as 98% of its Ebitda comes from assets backed by either regulated returns or take or pay agreements,” he notes.

Investment trusts for dividend income

The structure of an investment trust lends itself to income investing. Not only do they give investors access to a well-diversified portfolio of income stocks, but they can also pay dividends out of both capital and income, unlike ETFs and other open-ended investments. That means trusts are more likely to be able to sustain their dividends in periods of market volatility. Trusts with a global mandate also have far more flexibility in where they can invest so they can pick the best income, quality and growth plays in the world.

JP Morgan Global Growth and Income (LSE: JGGI), Murray International (LSE: MYI), Scottish American (LSE: SAIN)and STS Global Income & Growth (LSE: STS) all have a global mandate. Ecofin Global Utilities and Infrastructure (LSE: EGL) has a global mandate within its utility sector. Others, such as Law Debenture (LSE: LWDB)and Temple Bar (LSE: TMPL), have a UK focus, but with some international holdings.

My Top 6 Dividend Stocks for 2026 (Buy Now, Don’t Wait)

Brett Owens, Chief Investment Strategist Updated: December 3, 2025

Let’s get our 2026 dividend shopping finished ahead of time, shall we?

Come January, we’ll have plenty of company from vanilla investors, rushing to “figure out the new year.” Trends. Predictions. Buy this!

But there’s no reason to wait. We already know some of the key dimensions of 2026. Interest rates, for one, are on their way down. Fed Chair Jay Powell has delivered two rate cuts to end the year, with more to follow.

Whether or not Powell personally delivers them doesn’t matter to us. Powell is on his way out. But the Fed show will go on, with a ringmaster ready to roll.

Kevin Hassett isn’t some mystery bureaucrat drifting into the big chair. He’s been broadcasting his playbook for two decades. Hassett spent the 2000s arguing that the Fed moves too slowly, waits for too much data and leaves too much growth on the table. He quipped that the Fed should “cut early and cut often” because market confidence is a policy tool, too.

Now, he gets to run the show. And he’s being appointed by an administration that wants mortgage rates lower yesterday, housing market activity and growth charts that point up. Hassett knows the assignment—cut early and often!

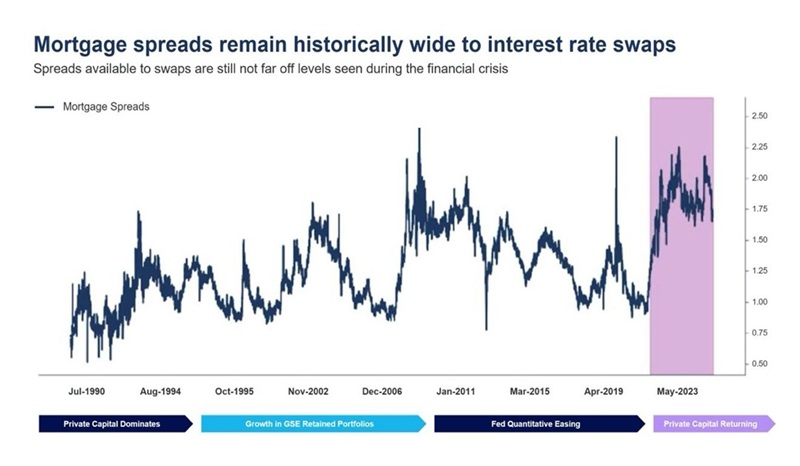

When this happens, mortgage REITs Annaly Capital (NLY) and Dynex Capital (DX) are going to run. These stocks yield 12.3% and 14.7% respectively, but these dividends are merely a generous appetizer for the main course of price appreciation. Annaly and Dynex both boast portfolios that are perfectly positioned for the dawn of the Hassett era. They own government-backed mortgages that rise in value as long-term rates fall. Few companies benefit more from falling rates than these two.

Annaly and Dynex are sneaky bargains with mortgage spreads—the difference between the 10-year Treasury yield and mortgage rates—just coming down from manic levels. Over the last 20 years, the Great Financial Crisis, 2023 bond meltdown and 2024 mortgage-rate spike delivered the greatest “spreads” in which it was a great time to be an mREIT buyer:

Mortgage Spreads Ease from Manic Levels

The spread is the engine of profit for Dynex and Annaly, and the engine rarely runs this hot. Both firms loaded up on cheap “agency” mortgage-backed securities when spreads were peaking. These are government-guaranteed bonds backed by Fannie Mae and Freddie Mac. No subprime surprises or commercial property problems here.

Spreads have been easing with mortgage rates coming down all year. The administration wants them lower. With each tick down, Annaly and Dynex portfolios gain in value.

Now 2026 won’t just be about cheaper money. It will be the first commercial year of “Applied AI”—where AI moves past the hype stage and starts showing up in margins, product cycles and cash flows.

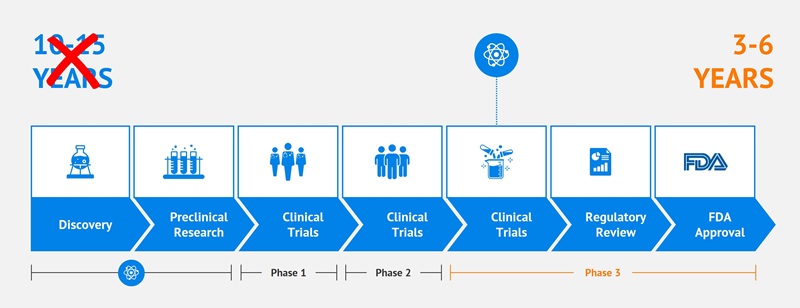

Historically, it has taken 10 to 15 years to develop a new drug. Every month matters because patents last only 20 years. The faster a company gets a drug to market, the more “gravy” months and years it enjoys with monopoly pricing power.

When patents expire, the generic versions hit the market. And the profit party is over for the original blockbuster.

AI, however, is extending the sales calendar starting in 2026.

Drug discovery cycles are already compressing. From 10 to 15 years, they will soon approach six years or less. Industry experts, in fact, are saying three to six years will be the new normal. Whoa! That can be a decade or more monopoly pricing!

No, AI isn’t replacing scientists—it’s multiplying them. These models run overnight, on weekends, forever. They eliminate dead ends and push more viable drug candidates into trials.

In the years ahead, pharma will have more shots on goal, resulting in more drug candidates and approved medications. And by getting these drugs to market faster, these companies will have more time to monetize the winners.

Profits are about to pop. BlackRock Health Sciences Term Trust (BMEZ) yields an elite 8.6%, owning some of the most innovative drug development companies on the planet. BMEZ is a neat way to buy them at a discount to their net asset value, with an enhanced dividend.

Pharma’s pick-and-shovel provider is also well positioned. A current of new pharma money will flow upstream into the company supplying the labs.

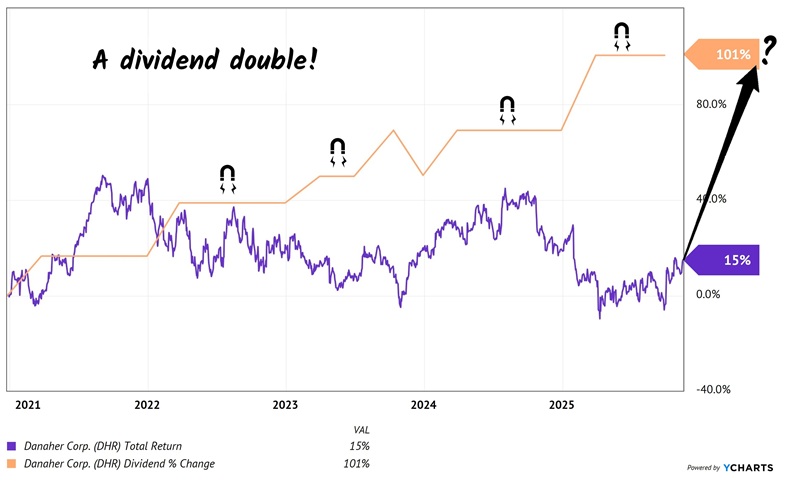

That’s Danaher (DHR), the quiet go-to company in life sciences and diagnostics. Danaher doesn’t sell drugs. It sells the tools, the instruments, the purification systems, the diagnostics, and, critically, the consumables that pharma needs to move discoveries from idea to lab to clinic to market.

No consumables, no experiments. No experiments, no drugs.

And because Danaher doesn’t sell drugs itself, it avoids the political circus entirely.

Consumables are the big catalyst here—they are the “razor blades” that labs burn through every day, and AI-driven R&D means more experiments, not fewer. That’s the first place we’re seeing gains at Danaher.

And its dividend? A phat double in a mere five years! When a payout pops 100% and a stock price rises only 15% over the same time period, saying the stock is “due” for a rally is an understatement.

Danaher’s Dividend Magnet is Due

Danaher’s management treats shareholders to regular raises, and these generous hikes add up.

Of course AI itself is a tremendous power hog. Every time ChatGPT generates a response, it pulls from enormous racks of servers running in data centers. Those servers draw electricity on the scale of small cities.

The servers are fed by the “boring” utility stocks owned by Reaves Utility Income Fund (UTG). Our closed-end fund yields 6.2%

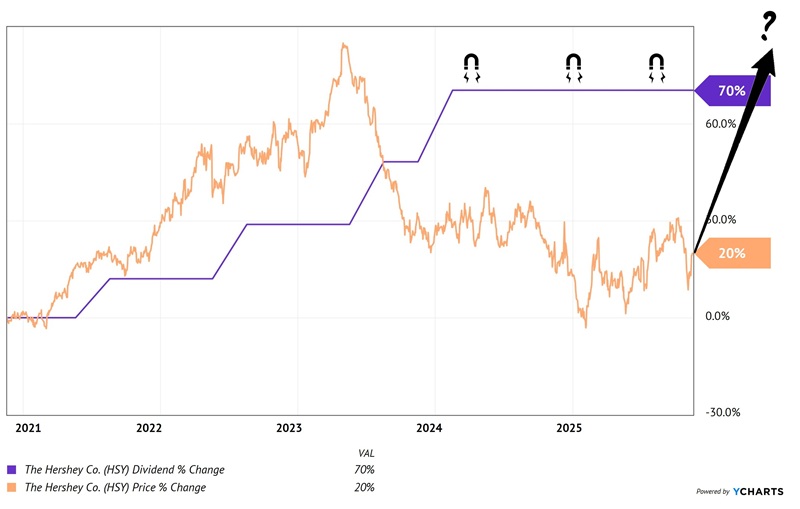

Finally, on a completely different topic from interest rates and Applied AI, let’s talk about chocolate. Hershey Foods (HSY) deserves our attention. This is an American icon that pulled back when cocoa prices exploded, input costs spiked and margins compressed.

But Hershey didn’t lose its competitive moat just because cocoa had a tantrum. The brands are as dominant as ever—Reese’s, Hershey Bars, Kit Kat, Kisses, Twizzlers—the whole candy aisle lives under this roof.

Even as cocoa kept rising, Hershey’s cash flow rebounded. Management quietly rolled out a two-year efficiency plan, pushing automation deeper into the production lines and tightening costs. They raised prices across the portfolio. And consumers, as they almost always do, kept buying their comfort food.

What we’re really buying here is the return of the dividend magnet. Hershey raised its payout 70% during a five-year period where the stock meandered. That is the kind of “magnet gap” we love to pounce on!

Hershey’s Dividend Magnet is Due

With input costs easing, restructuring savings flowing, and a beaten-down share price that’s starting to rally, Hershey is primed for a rebound.

Megatrend stocks like these are the secret to retiring on as little as $500K. The “suits” that say we need $2 million or more are talking their own book. Their “safe” strategies are failing while we income investors secure our own dividend-powered retirements with megatrend stocks like these

Source:

Source:

Source:

Source: