GL

Investment Trust Dividends

GL

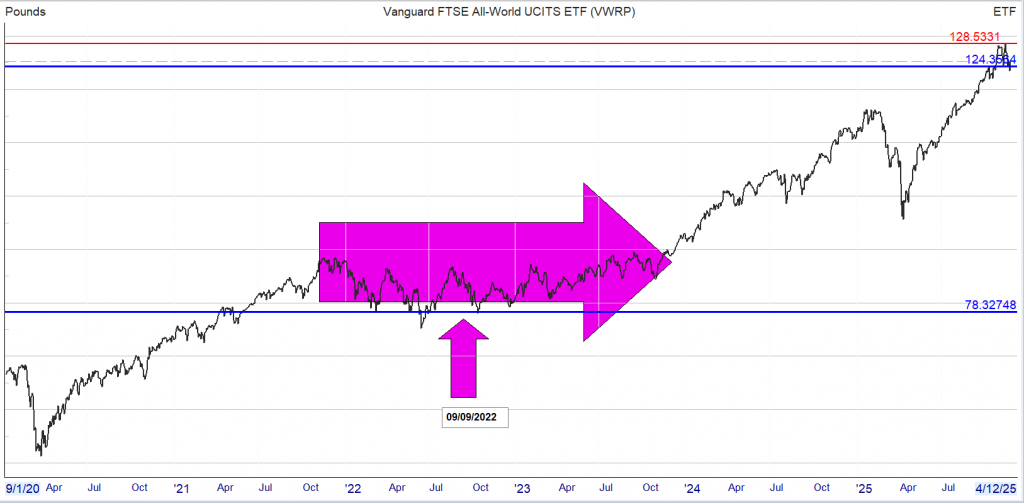

If instead of starting the Snowball, you invested 100k in VWRP your portfolio would be worth £150,426. Whilst it’s very high risk to invest all your capital into one share as you can see from the chart, you made nothing, zero zilch, nothing for 2 years at the arrow.

But the growth is not too shabby, so maybe one day when Mr. Market gives you the opportunity you could buy the sister share VWRL that pays a small dividend and pair trade it with a higher yielder.

The comparison is that you would use the fund to pay your ‘annuity’ using the 4% rule.

Income for 2025 £6,017

The Snowball 2025 £9,175

The gap between the two should grow, especially when (not if) markets roll over.

Stephen Wright takes a look at the power of dividend shares to turn a small regular monthly investment into much bigger long-term returns.

Posted by Stephen Wright

Published 24 November

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

A lot of so-called passive income strategies actually involve a lot of work, but dividend shares are a rare exception. They really are a way of earning money while you sleep.

The average long-term return from the FTSE 100 is around 6.8% a year. And this means the amount you need to invest to target a £1,000 monthly income might be less than you think.

The biggest thing when trying to figure out how much is needed to target £12,000 a year is how long do you have? It’s a simple question, but the answer is hugely important.

To earn that amount next year, you’ll probably need to invest at least £184,615. And dividend tax means the amount is actually likely to be quite a bit higher than this.

For investors with more time though, the amount they need comes down. Another route involves investing £1,000 a month at 6.5% for 12 years.

That mean splashing out a total of £144,000. And another advantage is that – unless the rules change – you can do this in a Stocks and Shares ISA and not have to pay tax on dividends.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

In general, having more time is a big help. Looking even further ahead, the average FTSE 100 return is enough to turn £200 a month into something generating £12,000 a year after 30 years.

That’s a total of £72,000 invested. So someone looking for a £1,000 monthly passive income straight away has to find an extra £112,615 compared to someone with a 30-year time horizon !

Whatever the strategy, earning durable income means finding quality shares to buy. And fortunately for investors, the UK stock market has a number of high-calibre names.

One example is Associated British Foods (LSE:ABF). A 3% dividend yield means investors will need some growth to reach a 6.5% annual return, but I think they have a decent chance.

The company’s main asset is Primark and it’s fair to say that the budget fashion retailer has faltered recently. In the UK, a tough backdrop caused like-for-like sales to fall 3.1% in its 2025 fiscal year.

That’s bad and this is an ongoing risk in a relatively saturated market. But things look much more positive in the US, where I think there’s a lot for scope for future growth.

The US has suspended its de minimis exemption for goods coming from China and Hong Kong. And that should make it harder for online competitors like Shein and Temu.

I think that gives Primark a big opportunity. And while Associated British Foods has been talking about the possibility of separating Primark, I hope it doesn’t with what I see as a potential opportunity.

Right now, the only way to invest in Primark is by buying shares in Associated British Foods. And I think the US division’s potential is currently being overshadowed by the weak UK sales.

I think this is a reflection of the wider UK stock market. There are some really interesting opportunities for investors, but they aren’t always in plain sight — even in the FTSE 100.

ABF of no interest for the Snowball on several levels.

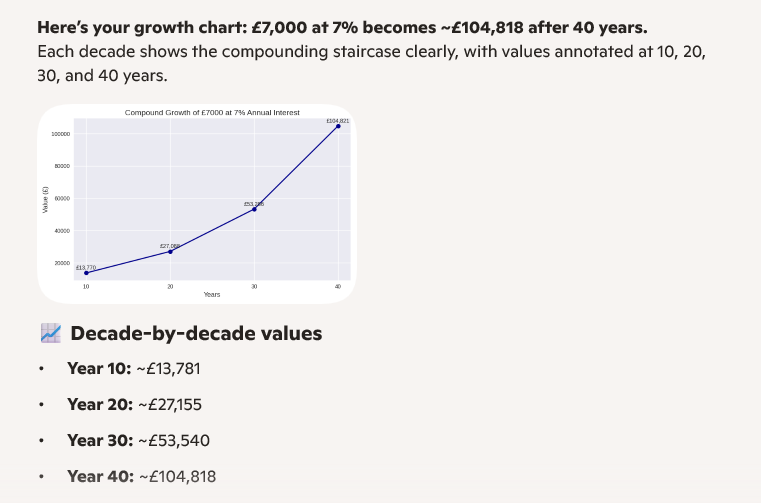

The first 10 years nearly double the money, but the real magic happens later.

Now it’s unlikely you have 100k to invest in your Snowball or have 40 years until you want to use your dividends to pay your bills but you do have the ability to add new funds to your Snowball, knowing that you should compound more than at the end of your journey than at the start.

The current blended yield for the Snowball is 11%, which should help the Snowball to grow faster than the table above.

Thursday 27 November

3i Group PLC ex-dividend date

Alliance Witan PLC ex-dividend date

AVI Global Trust PLC ex-dividend date

BlackRock World Mining Trust PLC ex-dividend date

Fidelity Special Values PLC ex-dividend date

Great Portland Estates PLC ex-dividend date

HICL Infrastructure PLC ex-dividend date

Land Securities Group PLC ex-dividend date

Worldwide Healthcare Trust PLC ex-dividend date

This may change your view.

Here’s the proof, from our friends at Hartford Funds.

Hartford looked at the years between 1960 and the end of 2024, which included everything: the inflation of the ’70s, economic crashes in 2001 and 2008 and, of course, the pandemic.

Here’s what they found: if you’d put $10,000 in the S&P 500 in 1960, you would have had $982,072 at the end of the period, based solely on price gains.

That’s not bad: a 9,721% increase.

It shows you why most folks only think about share prices when they invest. After all, with a gain like that, it’s tough to get excited about a dividend that dribbles a few cents your way every quarter.

But here’s the thing: when you reinvest your dividends, the magic of compounding kicks in. The difference is shocking: your $10,000 would have grown to $6,399,429, or more than $5.4 million more than you’d have booked on price gains alone!

That’s a 63,894% profit.

It’s a crystal clear example of how critical dividends are. And you can grab stronger profits if you buy stocks whose dividends aren’t just growing but accelerating.

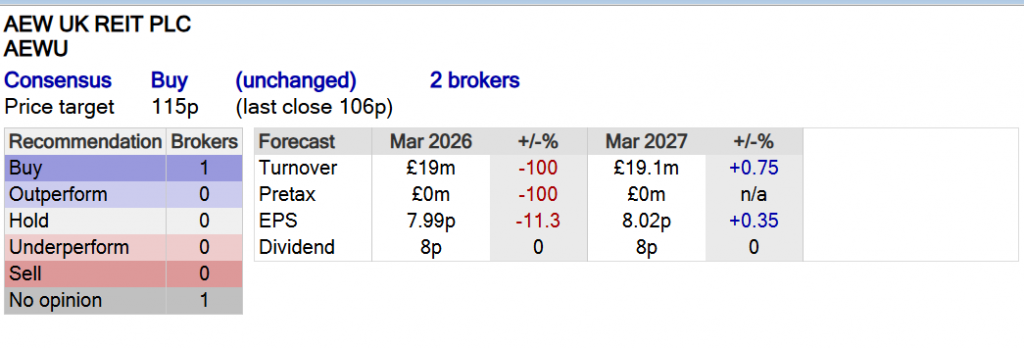

21 November 2025

AEW UK (AEWU) real estate investment trust says commercial property capital values are “at their lowest point” in its 10-year history, providing the £165m top performer, which won a QuotedData Investors’ Choice award last month, with plenty of attractive opportunities if only it could raise more money.

At the end of September, AEWU had £13.2m of cash but aside from the £5m it keeps as a buffer, the rest has been earmarked for refurbishments and property improvements.

With the company maxed out on its £60m borrowing facility, chair Robin Archibald said the board was “actively exploring with its advisers” how to raise cash and grow the fund.

Archibald said: “The investment manager has conviction in the current buying opportunities seen in the UK commercial real estate market, and believes that now is an ideal time to deploy capital, as property values are at their lowest point since the company’s IPO.

He said AEW fund managers Laura Elkin and Henry Butt expect that “any acquisitions made in the near term would yield strong performance and shareholder returns in the future.”

All this could imply a share issue if the stock returns to trading to a small premium, or even a bid for a weaker rival in a sector that has already contracted from several mergers and acquisitions.

AEWU shares currently stand 1.9% below net asset value, the narrowest discount in a peer group where shares on average trail 23% below the value of their property investments.

Half-year results today showed AEWU’s NAV per share dipped just over a penny to 109p in the six months to 30 September as 4p of dividends, capital expenditure on its properties and falls in the value of some buildings, such as offices, weighed.

With the quarterly dividends included, however, the company made a 2.7% total underlying investment return, down from 10% a year ago, with real estate transactions slowed by the uncertainty around next week’s delayed Budget. Buoyed by its strategy of buying higher-yielding, smaller assets, the total property return was 3.2%, ahead of the 3% of its MSCI real estate funds benchmark.

The dividend was once again slightly uncovered with earnings per share of 3.91p, down from 4.43p this time last year. However, the company has consistently maintained a 2p per share quarterly payout since launch in 2015, providing some reassurance on its commitment.

Shareholders enjoyed a 11.4% total return as the shares recovered from April and closed their discount. Over one and 10 years AEWU currently leads the sector with 20.4% and 138.9% total returns. Over five it ranks second behind Schroder Real Estate (SREI) which has returned 100% and is being stalked by LondonMetric Property (LMP) which has bought an 11% stake.

The portfolio has 34 properties, the latest addition being the £11.1m acquisition of a the Freemans leisure park in Leicester which was bought with the proceeds of the sale of retail park in Coventry last December.

Its biggest weighting of just over 37% is to industrial properties which saw a like for like 2.3% gain in the half year. High street retail, which accounts for 20.5% of assets, gained 1.2%, while retail warehouses rose 2.2% to make up 13.6% of the portfolio. Offices, the smallest sub-sector at 10.8%, fell 5.2% as the sector continues to struggle on a dearth of transactions.

Mark Hartley explains how real estate investment trust rules provide big benefits to shareholders, making them attractive to income investors.

Posted by Mark Hartley

Published 23 November

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Real estate investment trusts (REITs) are a specific fund type that focus on buying and letting property. They’ve long been popular among passive income investors due to rules that help ensure steady dividend returns.

They also offer simplified exposure to the real estate market without the high cost and risk of direct investment. Let’s have a look at the pros and cons of this unique investment option.

REITs give investors access to large-scale property development projects in residential, commercial and industrial spaces. The relatively low initial investment, combined with an experienced management team, makes them particularly attractive for beginner investors.

What’s more, the rules require them to distribute at least 90% of their taxable income to shareholders annually. This typically leads to high and consistent dividend yields, which is attractive for income-focused investors.

Moreover, they have far higher liquidity than standard real estate, trading on major stock exchanges where the shares can be bought and sold easily.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

While the rules result in higher yields, they also limit retained capital for further investment. This can result in slow or even negative growth, which could eat into returns during weak market periods.

They’re also highly sensitive to interest rate fluctuations, which can limit profits during high-rate periods. In addition, they typically include ongoing management fees which must be accounted for when calculating potential returns.

AEW UK (LSE: AEWU) is an up-and-coming REIT that started life just 10 years ago. Its strategy is to buy assets with shorter leases, aiming to exploit re-letting and redevelopment opportunities. It’s an interesting angle — but one with the added risk of tenant departures and higher vacancy rates.

It’s also very small, with a £167m market-cap, putting it at higher risk of volatility. The advantage being that the market tends to undervalue small-cap shares. As such, it has a net asset value (NAV) of 109p per share with shares currently trading at only 103p.

The past decade has dealt its fair share of ups and down but despite everything, it’s grown about 30% since Covid. Analysts expect the current growth trajectory to continue, with the average 12-month price target up 10%.

Importantly, its 7.6% yield isn’t only above average but is well covered by both earnings and cash flow. What’s more, its balance sheet looks healthy, with only £59.9m in debt against £174.4m in equity.

Earnings took a dive in 2022 but have made an impressive recovery, posting £24.34m in profit in 2024. Revenue in 2024 dipped slightly from 2023 but has been steadily increasing over the long term.

Whether investing in REITs, growth stocks or dividend shares, the key to building a solid passive income stream is a long-term mindset.

Investors who are quick to panic sell at the first sign of trouble often regret it down the line. No investment journey is smooth, and stomaching the ups and down is part of the ride.

But steady and reliable income stocks can help ease the turbulence. The key is picking the rights ones. With steady growth, a clean balance sheet and a impressive track record, I think AEW UK REIT is one worth considering.

Current yield 7.5%

Contrarian Investor

Turn Your Portfolio Into a Monthly Income Machine Discover the safe, simple way to lock in steady monthly dividends up to 11% right now! You’ve no doubt heard pundit after pundit say that you need at least a million dollars to retire well. Heck, we’ve all heard it so often, I bet it’s the first number most people think of when someone says “retirement savings”! Let me explain why this endlessly repeated fallacy is dead wrong. You’ll actually need a lot less than that. I’m talking about just $600,000 here. And in some parts of the country you could do it on less: a paid-for retirement for just $500,000. Got more? Great. I’ll show you how you can retire well on your current stake. I know that’s a bit tough to believe with the big hikes in the cost of living we’ve seen in recent years, but stick with me for a few moments and I’ll walk you straight through it. The key is my “9% Monthly Payer Portfolio,” which lets you live on dividends alone—without selling a single stock to generate extra cash. And you’ll get paid the same big dividends every month of the year – so that your income and expenses will once again be lined up! This approach is a must if you want to quickly and safely grow your wealth and safeguard your nest egg through the next market correction, too! This isn’t just a dividend play, either: this proven strategy also positions you to benefit from 10%+ price upside potential, in addition to your monthly dividends. That’s the Power of Monthly Dividends We’ll talk more about that price upside shortly. First, let’s set up a smooth income stream that rolls in every month, not every quarter like the dividends you get from most blue-chip stocks. You probably know that it’s a pain to deal with payouts that roll in quarterly when our bills roll in monthly. But convenience is far from the only benefit you get with monthly dividends. They also give you your cash faster—so you can reinvest it faster if you don’t need income from your portfolio right away. More on that a little further on. First I want to show you … How Not to Build a Solid Monthly Income Stream When it comes to dividend investing, many “first-level” investors take themselves out of the game right off the hop. That’s because they head straight to the list of Dividend Aristocrats—the S&P 500 companies that have hiked their payouts for 25 years or more. That kind of dividend growth is impressive. But here’s the problem: these folks are forgetting that companies don’t need a high dividend yield to join this club—and without a high, safe payout, you can forget about generating a livable income stream on any reasonably sized nest egg. Worse, you could be forced to sell stocks in retirement—maybe even into the kind of plunges we saw in March 2020 or throughout 2022—just to make ends meet. That’s a nightmare for any retiree, and leaning too hard on the so-called Aristocrats can easily make it a reality: the ProShares S&P 500 Dividend Aristocrats ETF (NOBL), which holds all 69 Aristocrats, still yields just 2% as I write this. Solid Monthly Payers Are Rare Birds … You can certainly build your own monthly income portfolio, and the advantage of doing so is obvious: you can target companies that pay more than your average Aristocrat’s paltry payout. Trouble is, only a handful of regular stocks pay in any frequency other than quarterly, so we’ll have to patch together different payout schedules to make it happen. To do that, let’s cherry-pick a combo of well-known payers and payout schedules that line up. Here’s an “instant” 6-stock monthly dividend portfolio that fits the bill:Procter & Gamble (PG) and AbbVie (ABBV) with dividend payments in February, May, August and November.Target (TGT) and Chevron (CVX), with payments in March, June, September and December.Sysco (SYY) and Wal-Mart Stores (WMT), with payments in January, April, July and October.Here’s what $600,000 evenly split across these six stocks would net you in dividend payouts over the first six months of the calendar year, based on current yields and rates:  You can see the consistency starting to show up here, with payouts coming your way every single month, but they still vary widely—sometimes by $1,275 a month! It’s pretty tough to manage your payments, savings and other needs on a lumpy cash flow like that. And the bigger problem is that we’re pulling in $18,300 in yearly income on a $600,000 nest egg. That’s not nearly enough for us to reach our ultimate goal of retiring on dividends alone, without having to sell a single stock in retirement. We need to do better. Which brings me to… Your Best Move Now: 9%+ Dividends AND Monthly Payouts This is where my “9% Monthly Payer Portfolio” comes in. With just $600,000 invested, it’ll hand you a rock-solid $48,000-a-year income stream. That could be enough to see many folks into retirement. The best part is you won’t have to go back to “lumpy” quarterly payouts to do it! Of all the income machines in this unique portfolio, nearly half pay dividends monthly, so you can look forward to the steady drip of income, month in and month out from these plays. That’s How This Grandma Makes $387,000 Last Forever A while back, I was chatting with a reader of mine who manages money for a select group of clients. He’d been using my Monthly Payer Portfolio to make a client’s modest savings – a nice grandmother who came to him with $387,000 – last longer than she ever dreamed: “She brought me $387,000,” he said. “And wants to take out $3,000 per month for 10 years.” The result? The last time I’d spoken with him, it had been over seven years since she started her $3,000 per month dividend gravy train. In that time, she’d taken out a fat $252,000 in spending money. And that nest egg? She was still sitting on more than $258,000 after seven years and $252,000 worth of withdrawals. Grandma’s Monthly Dividend Gravy Train  Her investments pay fat dividend checks that show up about every 30 days, neatly coinciding with her modest living expenses. And the many monthly dividend payers she bought dish income that adds up to 8% (or more) per year. There’s no work to it; these high-income investments provide a “dividend pension” every month. I’m ready to give you everything you need to know about this life-changing portfolio now. Let’s talk about Grandma’s secret – her high-yielding monthly dividend superstars (which even have 10%+ potential price upside to boot!) Monthly Dividend Superstars: 9% Annual Yields With 10%+ Price Upside, Too Most investors with $600,000 in their portfolios think they don’t have enough money to retire on. They do – they just need to do two things with their “buy and hope” portfolios to turn them into $4,000+ monthly income streams:Sell everything – including the 2%, 3% and even 4% payers that simply don’t yield enough to matter. And, Buy my favorite monthly dividend payers.The result? More than $4,000 in monthly income (from an average annual yield just over 8%, paid about every 30 days). With potential upside on your initial $600,000 to boot! And this strategy isn’t capped at $600,000. If you’ve saved a million (or even two), you can just buy more of these elite monthly payers and boost your passive income to $6,660 or even $13,320 per month. Though if you’re a billionaire, sorry, you are out of luck. These Goldilocks payers won’t be able to absorb all of your cash. With total market caps around $1 billion or $2 billion, these vehicles are too small for institutional money. Which is perfect for humble contrarians like you and me. This ceiling has created inefficiencies that we can take advantage of. After all, in a completely efficient market, we’d have to make a choice between dividends and upside. Here, though, we get both. Inefficient Markets Help Us Bank $100,000 Annually (per Million) Fortunately for you and me, the financial markets aren’t 100% efficient. And some corners are even less mature and less combed through than others. These corners provide us contrarians with stable income opportunities that are both safe and lucrative. There are anomalies in high yield. In an efficient market, you wouldn’t expect funds that pay big dividends today to also put up solid price gains, too. We’re taught that it’s an either/or relationship between yield and upside – we can either collect dividends today or enjoy upside tomorrow, but not both. But that’s simply not true in real life. Otherwise, why would these monthly payers put up serious annualized returns in the last 10 years while boasting outsized dividend yields? For example, take a look at these 5 incredible funds that pay monthly and soar:  This is the key to a true “9% Monthly Payer Portfolio” – banking enough yields to live on while steadily growing your capital. It’s literally the difference between dying broke and never running out of money! But I’m not suggesting you run out and buy these funds. |

These shares have outperformed the FTSE 100 this year and offer a higher yield. Analyst Robert Stephens thinks they’re one to own as returns on cash savings accounts decline.

19th November 2025 08:38

by Robert Stephens from interactive investor

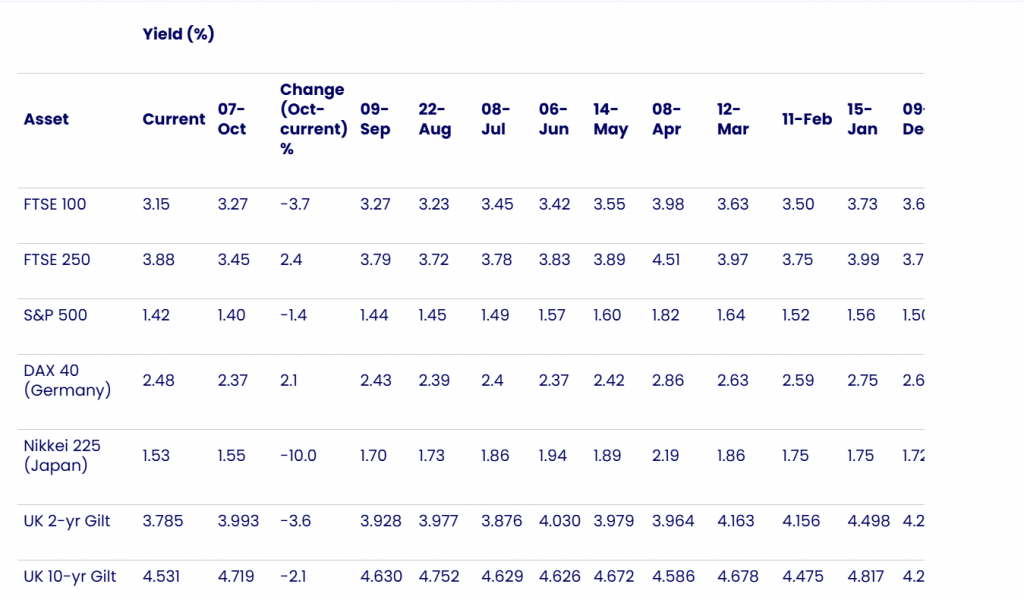

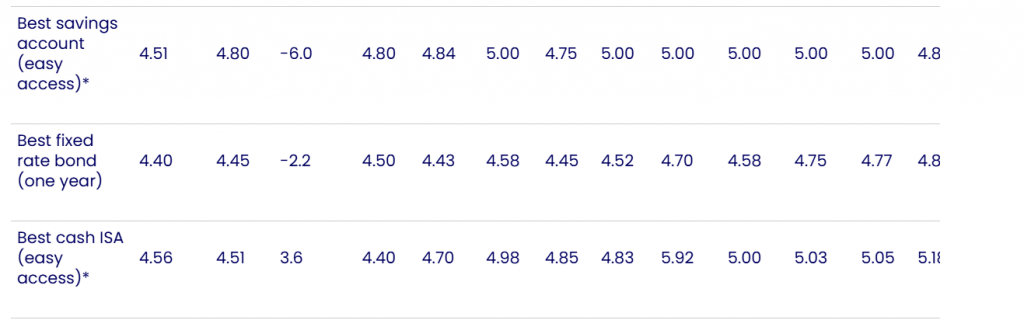

Yields across mainstream asset classes have declined over recent months. For example, easy-access savings accounts now offer little more than 4.0% excluding bonuses following a 75-basis point cut to the Bank Rate since the start of the year.

Similarly, falling interest rates have supported fixed-income prices. This has contributed to a fall in the yield on 10-year gilts, for example, which is down by around 20 basis points to 4.4% year to date.

Additionally, the FTSE 100 has surged by 15% since the start of the year. Its performance has been boosted by continued monetary policy easing not just in the UK, but across developed economies including the US and eurozone, given its overwhelming reliance on the global economy (over 80% of FTSE 100 members’ sales are generated from outside the UK). As a result of its recent surge, the UK’s large-cap index now yields just 3.2%.

The recent trend of falling yields is likely to continue in future. While UK inflation is currently 180 basis points in excess of the Bank of England’s 2% target, the central bank said in November that it believes the annual rate of price changes has now peaked. According to its forecasts, inflation will gradually fall to target during the first half of 2027.

When combined with an unemployment rate that currently stands at 5%, its highest since May 2021, and economic growth that amounted to just 0.1% in the third quarter of the year, this suggests further interest rate cuts are ahead.

Falling rates are likely to prompt continued decline in the income return of cash savings accounts. In theory, further monetary policy easing should also lead to a rise in government bond prices, which could prompt a continuation of falling gilt yields. And with lower interest rates likely to be implemented not just in the UK but also in the US, where the Federal Reserve expects inflation to fall to 2% by 2028, the outlook for the world economy is set to improve. This should support the FTSE 100’s future performance, thereby having the potential to further suppress its dividend yield.

In terms of portfolio positioning, cash savings accounts are set to become an even less worthwhile means of generating an attractive income. Indeed, income investors who rely on them are likely to experience a substantial decline in their spending power even amid falling inflation.

While a looser monetary policy should boost bond prices, thereby providing scope for capital gains in the medium term, a heightened level of UK political and economic uncertainty could weigh on government bond prices. For instance, reaction to the upcoming Budget and any subsequent changes to fiscal policy remain a known unknown that may prompt heightened volatility in gilt prices.

As a result, income seekers may wish to continue to focus on dividend stocks rather than fixed income or cash alternatives. While the FTSE 100 index currently offers a yield that is around 120 basis points lower than that of 10-year gilts or easy-access cash savings accounts, its members provide scope for significant dividend growth amid falling interest rates and an increasingly upbeat global economic outlook.

Source: Refinitiv as at 18 November 2025. Bond yields are distribution yields of selected Royal London active bond funds (as at 30 September 2025), except global infrastructure bond which is 12-month trailing yield for iShares Global Infras ETF USD Dist as at 14 November. SONIA reflects the average of interest rates that banks pay to borrow sterling overnight from each other (14 November). Best accounts by moneyfactscompare.co.uk refer to Annual Equivalent Rate (AER) as at 18 November. *Includes introductory bonus.

Over the long run, it would be wholly unsurprising if a diverse portfolio of UK large-cap shares provides income seekers with a positive real-terms increase in their spending power. This contrasts with the fixed income offered by bonds, which is set to decline in real terms, and a likely fall in the income return from cash savings accounts.

Although the FTSE 100’s past performance suggests that its future returns could prove to be highly volatile, its earnings multiple of under 18, versus a figure of 27.6 for its US peer (S&P 500), suggests it is not yet overvalued. Alongside improving operating conditions for its members amid likely global interest rate cuts, this indicates that it could deliver further capital gains alongside inflation-beating income growth in the coming years.

GSK’s 30% share price rise since the start of the year means it now has a yield of 3.6%. While the global pharmaceutical firm still has an income return which is 40 basis points greater than that of the FTSE 100 index, some income seekers may feel it now lacks dividend investing appeal having started 2025 with a yield of roughly 4.5%.

However, the company’s shareholder payouts are set to rise at a relatively fast pace over the coming years as a result of its improving financial performance. Recently released third-quarter results, for example, included an upgrade to profit guidance for the full year. GSK

GSK now expects to deliver earnings per share (EPS) growth of 10-12% versus a previous forecast of 6-8%.

Higher profits should ultimately translate into rising dividends, given that the firm aims to pay out between 40% and 60% of earnings to shareholders. Having already announced dividend payments for the first three quarters of the current year, shareholder payouts are on track to rise by 4.9% for the full year. This is 110 basis points ahead of an elevated inflation rate and gives a forward yield of 3.6%. A consensus forecast of a double-digit rise in profits next year is set to have a further positive impact on dividends.

As with any pharmaceutical company, there are no guarantees that GSK’s product pipeline will deliver on its potential. However, the company is boosting the chances of it doing so by spending a larger proportion of revenue on research and development (R&D).

In the first three quarters of the current year, for instance, it spent 21.5% of total sales on R&D. This is up 2.5 percentage points on the same period of the previous year. When combined with the firm’s improving financial performance, it means that R&D spending was up 20% versus the same nine-month period from the previous year.

Given its solid financial position, the company is well placed to further invest for long-term growth. Although its net debt-to-equity ratio is relatively high at 92%, the firm’s defensive characteristics mean this figure is by no means excessive.

Meanwhile, net interest cover of 17.8 in the first nine months of the year suggests the company could overcome even a material fall in profits should it ultimately experience difficulties in replacing today’s top-selling drugs, for example.

Clearly, an upcoming change in CEO and ongoing geopolitical risks, notably rumours regarding tariffs on pharmaceuticals, are uncertainties facing the business. They could weigh on investor sentiment and act as a drag on future share price performance.

However, even after its share price surge over recent months, GSK trades on an earnings multiple of just 11.2, and less than 11 on a forward basis. This is more than a third lower than the FTSE 100 index’s price/earnings (PE) ratio and indicates that there is a wide margin of safety present which provides scope for a further upwards rerating over the long run. This is especially the case given the company’s upbeat earnings profile and solid fundamentals.

As a result, GSK appears to offer long-term investment appeal. Its encouraging financial performance and strong earnings growth potential could equate to inflation-beating dividend growth that more than adequately compensates investors for a relatively modest yield. And with upward rerating potential and a rising bottom line, the stock’s total return prospects also appear to be relatively favourable.

Robert Stephens is a freelance contributor and not a direct employee of interactive investor.

© 2026 Passive Income Live

Theme by Anders Noren — Up ↑