AI Economy’s Quiet Winners Yield Up to 11.7%

Brett Owens, Chief Investment Strategist

Updated: October 8, 2025

The manic market just dumped business development companies (BDCs), again. These three dividend stocks paying up to 11.7% are poised to bounce back when sanity returns.

BDCs, which lend money to small businesses, are on the “outs” with the Wall Street suits after multiple soft jobs reports. The spreadsheet jockeys fret about an unemployment-induced economic slowdown and miss the real story: small businesses are making more money than ever thanks to AI.

Here is what’s actually happening in the Main Street economy:

- Employers—especially nimble small business owners—are implementing AI to streamline and even run their operations.

- With AI tools, fewer humans are needed.

- So, we are seeing soft jobs reports as companies rationally prioritize automation over human hiring.

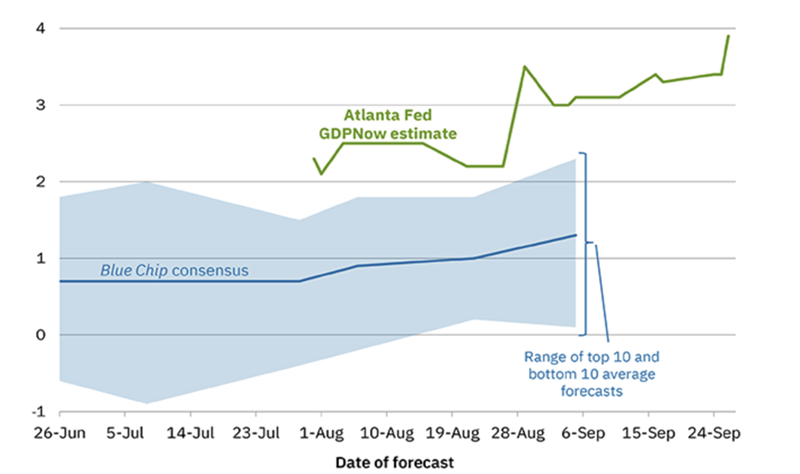

Small business profits are popping. While the unemployment numbers scream slowdown, the actual economy is booming. Check out the Atlanta Fed’s most recent GDPNow estimate—it’s up almost 4%!

Atlanta Fed Says Economy is Cookin’

We’ve been on this beat for months here at Contrarian Outlook. Automation is not slowing the economy. It is making it leaner and wildly profitable. While payrolls cool, output keeps rising. That’s no recession—it’s an efficiency boom!

This is music to BDCs’ ears. These lenders profit when Main Street’s cash flow swells.

So, we thank knee-jerk sellers for giving us a deal on FS Credit Opportunities (FSCO), which yields 11.7% today. FSCO has been around for 10+ years but only traded publicly as a closed-end fund for the last two. CEF investors loathe newness, so FSCO fetched a discount to net asset value (NAV) until recently.

Portfolio manager Andrew Beckman and his team are skilled at “layering” credit—structuring loans with different levels of protection—so that FSCO is positioned to get paid back first even if credit conditions worsen. It’s an ideal fund to own if you were worried about the economy. This cash cow keeps collecting through slowdowns.

FSCO extends high-quality loans that are not subject to the daily whims of the public markets. These are private credit vehicles held by sophisticated investors who don’t care about recent job reports—they want their yield!

As do we income investors.

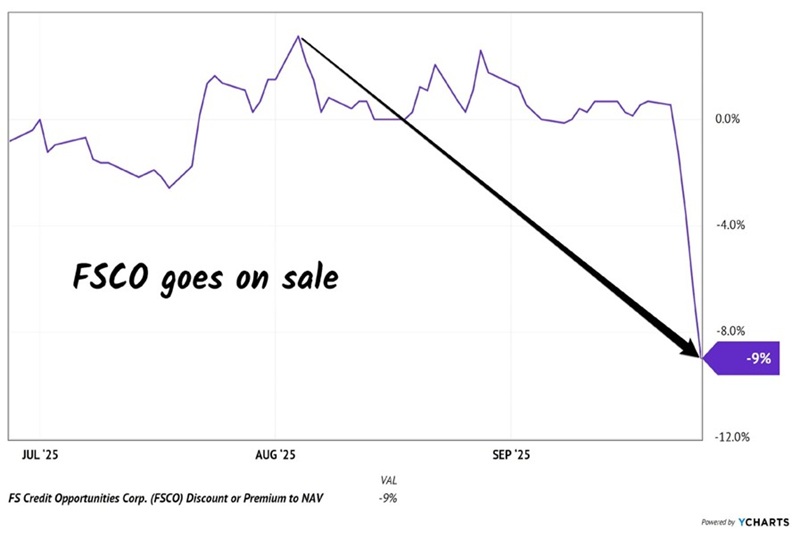

The vanilla dividend chasers finally found their way to FSCO this summer, sending it to a record 3% premium to NAV. But these weak hands fled when FSCO paid its monthly dividend (uh, the price drops because you just got paid, people!) and weak employment numbers weighed on the BDC sector.

The result? FSCO slipped from a 3% premium to a nifty 9% discount last week. Investors panicked but the strength of FSCO’s loans didn’t change:

FSCO Shares Went on Sale

FSCO continues to post strong credit metrics and cover its payout comfortably. Its high loan yields led Beckman and his management team to raise the monthly dividend multiple times this year:

FSCO Pays Monthly, Raises Often

FSCO looks good here, and it’s not alone. Ares Capital (ARCC), the largest BDC in America with $22 billion in assets, is killing it.

Ares is the big bully on the block—it sees the best deals before anyone else. And it shows. Non-accruals—loans that aren’t paying—remain a mere 2% of the portfolio, a hefty 20% below the industry average of 2.5%. No wonder ARCC’s net investment income (NII) has consistently covered its quarterly dividend, now $0.48 per share, with a small surplus each quarter!

And this bully loves economic turbulence. It thrived in 2020, growing book value through the Covid panic while smaller rivals stopped lending. And we have evidence that the punier BDCs are retrenching again, leaning into existing borrowers rather than pursuing new loans.

When the smaller fish throttle back, the bully turns up the volume. ARCC yields 9.5%, a payout supported by current income. That’s a rare combo of yield and quality in this market. We’ll keep collecting the digital checks.

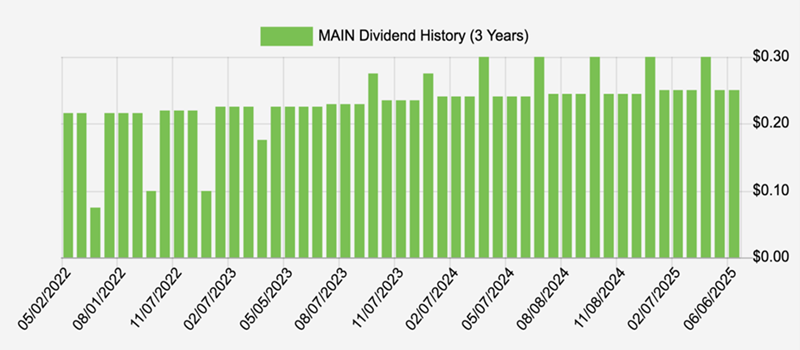

Last but not least, Main Street Capital (MAIN), is the steadiest grower in BDCLand. Not only has it paid monthly since 2008—hasn’t missed a beat—but it also adds quarterly “specials,” rewarding shareholders when portfolio income exceeds expectations.

MAIN invests in small, privately held businesses—between $25 million and $500 million in annual revenue—and takes both debt and equity stakes. This dual role lets it profit as a lender and as a partial owner when its companies thrive.

In the main, MAIN’s portfolio remains broad and balanced—about 190 companies across diverse industries, with no single position over 4%. That diversity keeps MAIN steady through economic cycles.

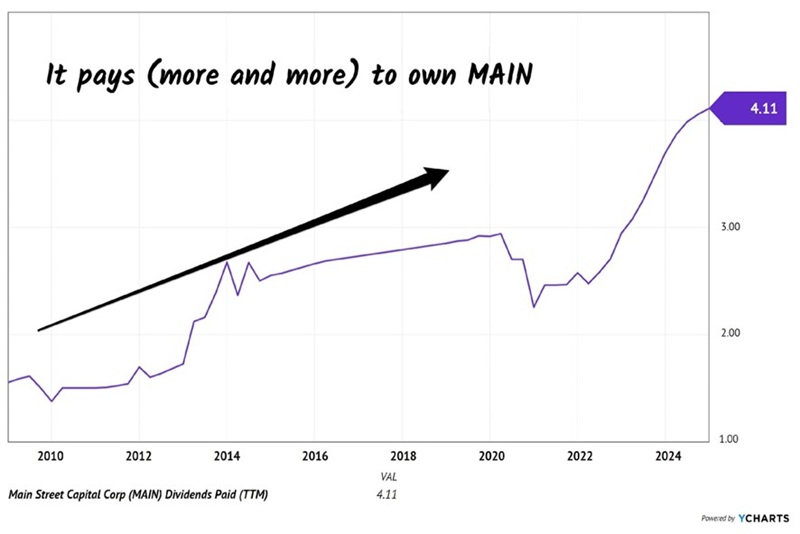

Since 2009, total annual dividends have jumped from $1.50 to more than $4 per share, a 170%+ climb that few serious dividend payers can match. The current yield sits around 6.8% today:

MAIN Regularly Raises Its Monthly Dividend

MAIN currently pays a generous 6.8%, with the majority delivered through dependable monthly payments. Check out this pretty payout picture:

MAIN pays monthly while ARCC “only” dishes its dividend quarterly.