Option one.

Buy an annuity.

When the day arrives and you want to start to spend some of your hard earned, you could buy an annuity. The gamble is there is no way of knowing what the income will be.

Canada Life figures show the 65-year-old with a £100,000 pension pot could buy an annuity linked to the retail price index (RPI) that would generate a starting annual income of £3,896. That’s up from £2,195 in the New Year following a 77% spike in rates this year.

Oct 22

You have to hand over all of your hard earned, so not an option for the SNOWBALL.

Option 2.

Use the 4% rule. For further information use the search facility above.

The SNOWBALL has a comparative share VWRP for passive investment where the value is £158,788, not too shabby.

Option 3.

Your Snowball.

The current fcast income for the SNOWBALL IS between 10 and 11%.

Lets say income of 10% p.a.

Using the comparison share the income would be £6351 p.a.

If we plan ahead

Let’ say income of 18% p.a.

The comparative share VWRP, would have to have a value of £450 k.

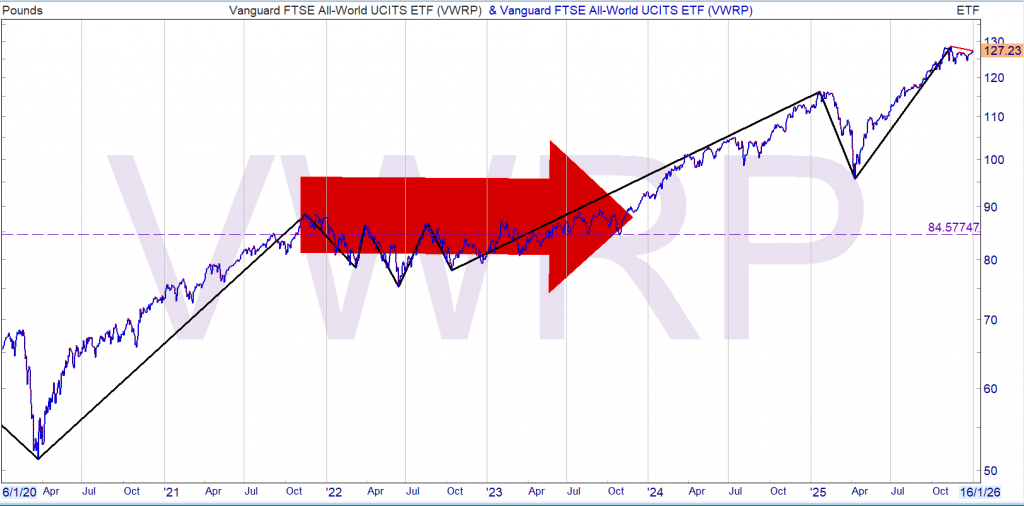

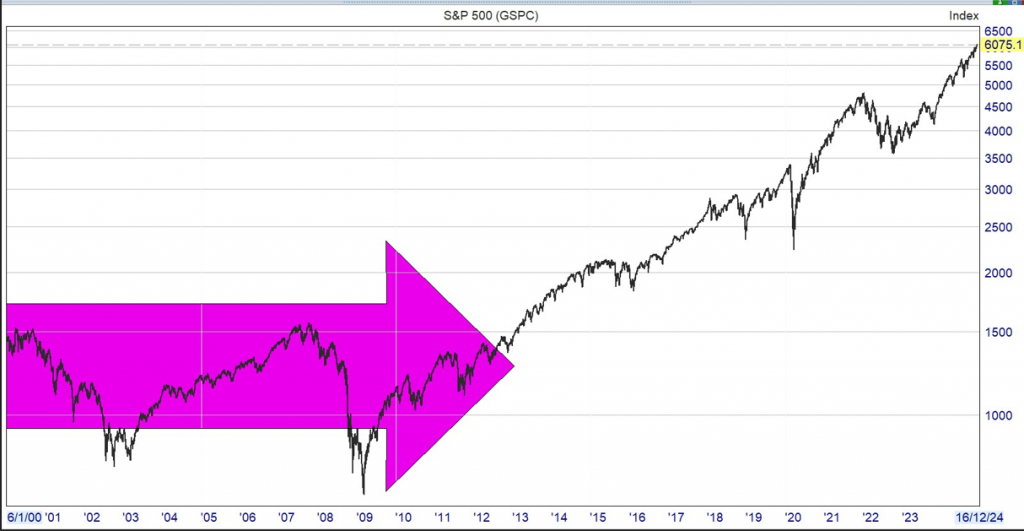

After periods of out performance, comes under performance, not if but when.

An option could be to have part of your Snowball in a passive investment as if you can choose the time when to sell, you may not make a huge profit but you shouldn’t lose any of your hard earned, maybe drip feed some of your dividends after the price has fell. Not advice, as you alone are responsible for your Snowball.

There are several fcasts for a repeat of

but as always

GL.

Leave a Reply