Disclaimer

This is a non-independent marketing communication commissioned by Columbia Threadneedle Investments. The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

Portfolio

CT Global Managed Portfolio aims to provide investors with a long-term savings vehicle consisting of two share classes: CMPI, which aims to deliver a growing income alongside capital appreciation, and CMPG, which focusses solely on maximising capital growth. Once a year, shareholders have the option to switch between share classes at net asset value without incurring UK capital gains tax. This enables those not investing through a tax-exempt account to adjust their investments over time in line with their needs without triggering a tax liability.

Both portfolios consist exclusively of investment companies, which managers Adam Norris and Paul Green regard as best-in-class and select on a bottom-up basis. That said, they also incorporate macroeconomic views into their investment process to identify both strategic and tactical opportunities. For this purpose, they can leverage Columbia Threadneedle’s significant in-house resources, benefitting from input provided by the multi-asset team.

Adam and Paul have been increasing their exposure to risk assets in recent months. They are constructive on the outlook for corporate earnings growth, and while they remain mindful of potential headwinds, such as higher oil prices driven by ongoing geopolitical tensions in the Middle East and possible changes in trade tariff rates, they highlight supportive policy measures across several regions, including the ‘One Big Beautiful Bill’ in the US, alongside stimulus packages in Germany and Japan, as well as likely steps to bolster economic growth in China.

One area they have added to across both share classes is Asia and emerging markets, where they see attractive valuations, strong earnings growth potential, and a weakening US dollar as tailwinds. Since our previous update (published on 14/10/2025), they have topped up their positions in Fidelity Emerging Markets (FEML) and Mobius Investment Trust (MMIT), both held within the CMPG portfolio. They have also introduced Invesco Asia Dragon (IAD) into both portfolios, highlighting its style-agnostic approach. Its managers, Fiona Yang and Ian Hargreaves, invest in companies they view as undervalued relative to fundamentals or where they believe the market underestimates earnings growth potential. In addition, IAD funds its dividend from both capital reserves and income generated by its portfolio companies, targeting a payout of 4% of NAV per year. This gives the trust the flexibility to invest in companies offering low or no dividend yield but stronger long-term growth potential, while still being able to deliver an attractive income, making it compatible with CMPI’s mandate.

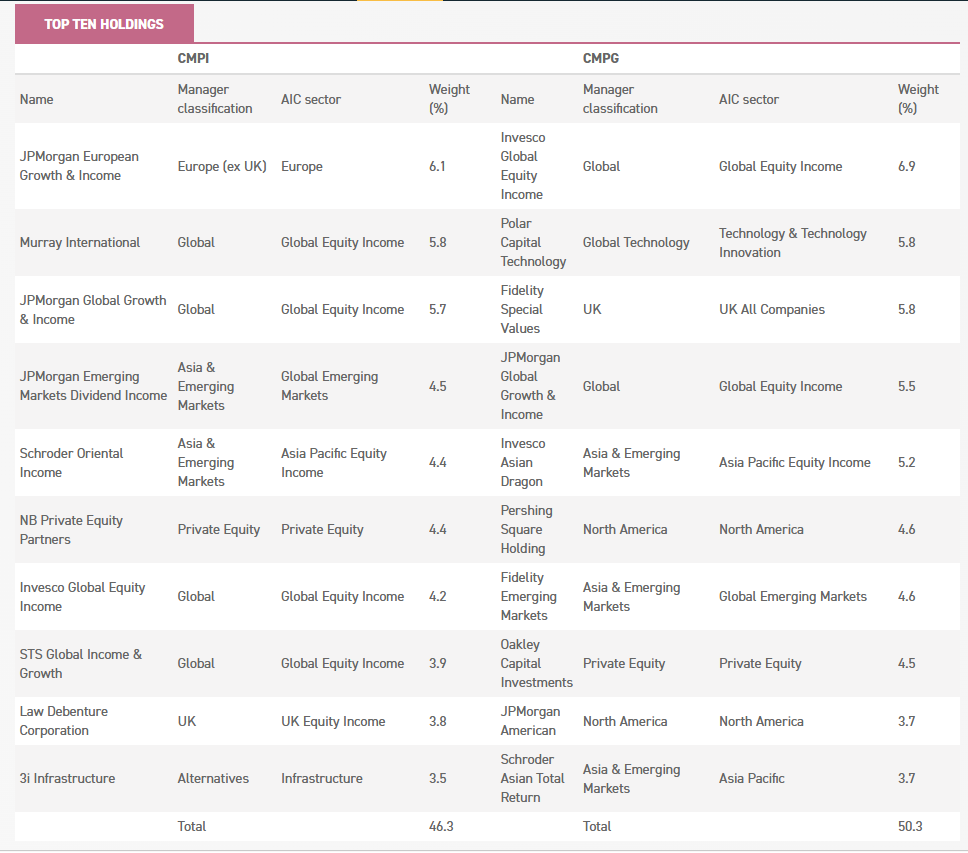

In fact, Adam and Paul favour this approach over traditional equity income strategies that pay a natural dividend, as they believe such strategies are typically constrained to a narrow pool of income-generating stocks, many of which they consider ‘value traps’ (i.e. stocks offering high dividend yields but limited total return potential). Consistent with this view, they have also initiated a position in Invesco Global Equity Income (IGET), a global equity income strategy targeting a dividend equivalent to 4% of NAV at the end of its previous financial year, using the same mechanism. At the end of February 2026, IGET was a top-ten holding across both CMPI and CMPG portfolios, as the table below shows.

TOP TEN HOLDINGS

Source: CTI, as at 28/02/2026

Conversely, Adam and Paul have continued to reduce exposure to UK equities. While these trade at a discount to their peers in other developed markets on aggregate, the managers view this as a reflection of their low growth potential and do not believe that valuations alone provide a sufficient catalyst for performance. Since their appointment, they have divested from Finsbury Growth & Income (FGT), Lowland Investment Company (LWI), Baillie Gifford UK Growth (BGUK), Law Debenture (LWDB) and Diverse Income Trust (DIVI) in the CMPG portfolio. Within CMPI, they have exited DIVI and Henderson High Income (HHI), but have retained LWI and LWDB, viewing the income stock-picking skills of James Henderson and Laura Foll — the managers of both trusts — as strong and well suited to CMPI’s mandate. While they are not seeing a broad-based recovery in UK small caps at this juncture, Adam and Paul believe there are still pockets of value within this space. To exploit these, they have introduced Odyssean Investment Trust (OIT) and Strategic Equity Capital (SEC) into the CMPG portfolio. Both strategies take sizeable positions in a limited number of stocks (fewer than 20 holdings), resulting in highly concentrated portfolios, and engage intensively with investee companies to drive improvement and unlock value.

The allocation to private equity has also been reduced since our previous update, although this was due to idiosyncratic reasons rather than a view on the asset class. For instance, Adam and Paul have trimmed their holdings in HgCapital Trust (HGT), a private equity strategy focussing on software and tech-enabled services companies, as they assessed that the type of businesses it invests in may face disruption from artificial intelligence. This concern has since materialised, with software-related businesses having experienced a sell-off in early 2026. Adam and Paul took advantage of the subsequent rebound to further trim their holdings in HGT. As a result of geopolitical uncertainty and its potential impact on the private equity market, they have not recycled the proceeds into this asset class. That said, they had added to their holdings in Schiehallion (MNTN), a late-stage private equity strategy held in the CMPG portfolio, last year. This reflects their view that clear winners are emerging within the portfolio, including SpaceX, an aerospace and space transportation company, and Bending Spoons, a company specialising in acquiring, managing, and revitalising digital apps and software businesses.

Adam and Paul have also exited multi-asset strategies such as Personal Assets Trust (PNL) and BH Macro (BHMG) in the CMPG portfolio, leading to a reduced allocation to the ‘alternatives’ category, as they are currently favouring exposure to risk assets. That said, they remain constructive on infrastructure, which also falls within the alternatives category. Since their appointment, they have introduced Cordiant Digital Infrastructure (CORD) into CMPI’s portfolio and Pantheon Infrastructure (PINT) into both portfolios. We discussed the investment theses for both CORD and PINT in our previous note.

EXPOSURE TO CATEGORIES

Source: CTI

Overall, the number of holdings has been reduced in both portfolios since Adam and Paul’s appointment, reflecting their plan to adopt a higher-conviction approach. For instance, the number of holdings in the CMPG portfolio has been cut from 39 to 30 (as of 31/12/2025). Similarly, the number of holdings in the CMPI portfolio has been reduced from 38 to 30 over the same period. As a result, concentration in the top-ten holdings has also increased across both portfolios. Concentration in the top ten holdings has also increased across both portfolios. For example, while CMPG’s top-ten holdings accounted for c. 36% at the end of May 2025, this had risen to c. 50% by the end of February 2026. In the CMPI portfolio, the weight of the top-ten holdings increased from c. 42% to c. 46% over the same period.

The CMPI Snowball is different to the SNOWBALL as it invests more for the chance of capital gains but as you wait it pays a yield around 6%.

The SNOWBALL invests for higher yields and uses those higher yields to buy more shares that pay a higher yield, until you want to use those dividends to pay your bills.

Your tips are practical and easy to apply. Thanks a lot!