I’ve bought 5421 shares in GCP for 4k.

Investment Trust Dividends

I’ve bought 5421 shares in GCP for 4k.

| unobet unobet-8.comx Ganaway15550@gmail.com 65.111.22.69 | At this time I am going away to do my breakfast, when having my breakfast coming over again to read more news. |

I hope you enjoyed your breakfast, TKU for reading the SNOWBALL

Interactive investor’s Dave Baxter has put together three hypothetical portfolios for different risk levels: cautious, balanced and adventurous.

23rd April 2026

by the interactive investor team from interactive investor

Putting together a portfolio to weather different conditions is no easy task, even in calmer times. For beginner investors it can be particularly puzzling, given there are thousands of funds to choose from.

Dave joins Kyle to explain his choices and how he arrived at the mix of assets. The duo also discuss ‘hands-off’ funds for investors on the lookout for low maintenance options.

Kyle Caldwell, funds and investment education editor at interactive investor: Hello, and welcome to On The Money, a weekly show that aims to help you make the most out of your savings and investments.

The focus for this episode is on how to approach building a portfolio from scratch, and joining me to discuss this topic is Dave Baxter, senior fund content specialist at interactive investor. Dave, welcome back to the podcast.

Dave Baxter, senior fund content specialist at interactive investor: Thanks for having me on.

Kyle Caldwell: So, Dave, you’re going to run through three hypothetical portfolios that you put together for three different risk levels. So low risk, medium risk, and high risk.

Before we delve into those, what would you say are the main considerations when starting to build a portfolio from scratch?

Dave Baxter: I’m going to make two related points. One thing to consider is your time frame and your circumstances, which of course is related. So, say you have 10 or 20 or more years to ride the ups and downs, then really you should be taking maximum levels of risk because you can tolerate that volatility and you’re going to maximise the growth that you can get.

Whereas if you’re, in retirement, for example, or if you for some reason would need your money soon, you need to be a bit more cautious.

The other thing I would highlight, which again is linked, is your appetite for risk and that’s quite interesting because sometimes that can contrast a bit with your actual circumstances. So, you might have time to ride out the ups and downs of markets, but if you’re particularly squeamish and freaked out about a big fall in your portfolio, then maybe just for your own peace of mind, you might take off a bit of that risk.

Kyle Caldwell: I completely agree with everything you’ve just said. I think also when you’re starting out, how much you’ve got to invest is a big factor, and that can help dictate how many funds or investments you choose.

If you’re just starting out with £1,000, you could feasibly just buy one fund, a global index fund or a global exchange-traded fund (ETF), for example, and that’ll give you ready-made diversification, as those types of funds own thousands of shares across the globe, and it gives you lots of exposure to different areas, different countries, different sectors, and different industries.

Whereas as your portfolio hopefully grows over time, or if you do have a larger initial investment amount, you can then consider holding more than one fund, maybe holding several and spreading diversification out even wider.

Dave Baxter: I guess there’s also the question of how interested you are in your investing point. Because perhaps you kick off and, like you said, you’re having a broad tracker and nothing else. Then over time, perhaps you’re watching what it does and then perhaps you go down the rabbit hole of studying a bit more about investing and then you can pick some of your more individual holdings.

Kyle Caldwell: In terms of what to think about when constructing a portfolio, I think the core and satellite approach is a really good rule of thumb for people to consider.

The theory is that if you have around 80% in core holdings, such as a global fund, which you can build a portfolio around, and then the remainder of 20% in more satellite positions, potentially in more adventurous areas such as funds investing in smaller companies or funds investing in the emerging markets or Asia-Pacific region.

A core/satellite approach helps give you a diversified portfolio and plenty of balance.

Dave Baxter: Yeah, definitely.

Kyle Caldwell: So, let’s move on to the three hypothetical portfolios that you have assembled.

We will put links to each article in the podcast episode description, which will contain the tables of the funds that you’ve selected for each of these hypothetical portfolios. But for those who are listening and watching on YouTube, we’re also going to show the tables during parts of this podcast recording.

Let’s first get into the lowest-risk portfolio or the cautious portfolio.

In terms of asset allocation, talk us through how you decided how much exposure to dedicate to shares, bonds, and alternative investments in this one.

Dave Baxter: To be frank, I’ve been very cautious, very conservative, and just put 20% in shares, and that’s a very diversified exposure. Some people who are cautious investors would have more in equities because even if you’re in retirement, you probably still want to keep growing your portfolio.

But one thing I wanted to explore is the dilemma with the defensive or the cautious side of a cautious portfolio. Because in the past you might simply have held a bit of equities and then put loads of money into bonds because, in theory, bonds should gain in value when stock markets fall.

But we’ve seen some challenges there. In 2022, when we saw interest rate rises, you saw bonds falling in tandem with equities and we’ve had a weird throwback to that with the conflict in the Middle East.

So, you’d be hoping that things like government bonds would be gaining in price while equity markets struggle, but they’ve also fallen because bonds hate the prospects of inflation and rate rises. So, rather than going all-in on bonds, we’ve split it up, as you mentioned.

So, we’ve got 40% in bonds, some government bonds, some corporate bonds, and some inflation-linked bonds. Then we’ve got some gold, some commodities, a bit of property, and also a so-called absolute return fund.

Kyle Caldwell:And the final 20%, is it in equities?

Dave Baxter: Yeah, it’s 20% equities. There we’ve gone for one really diversified fund, F&C Investment Trust Ord FCIT

which doesn’t stray too far from the MSCI World Index. I’ve also gone for a MSCI World ex USA tracker, just because F&C is very heavily weighted to the US and, as investors learned or remember from last year, there’s a lot going on beyond the US and there are a lot of returns to be had beyond the US, so I just wanted to give that spread.

Kyle Caldwell: You’ve arrived at 10 different funds, and they’ve all got a 10% weighting. Those listening in and watching the podcast on YouTube will now be able to see a table of your choices.

You’ve already explained F&C Investment Trust. Are there any others that you want to talk through?

Dave Baxter: A lot of these are actually ETFs. I think six of the funds are ETFs or passives of some form because we wanted some very straightforward exposure.

For gold, we simply wanted a physical gold ETC. With bonds, we’ve gone to some broad bond trackers. But perhaps to touch on a couple of more interesting options, you’ve got Schroder Real Estate Invest Ord SREI

,which is focused on physical property. Property can be a diversifier against equities and it might hold up better if we did see that inflationary environment that is going to threaten bond investors.

One other to highlight, and this might be a controversial take, is the Janus Henderson Absolute Return I Acc fund. A lot of people now probably pretty much hate absolute return funds because they haven’t done that well in recent years. But this one has quite a good record of protecting your capital. It’s a so-called long/short fund, so it does have some exposure to just buying equities, but it also does shorting, so betting on the price of a share falling.

Kyle Caldwell: Personally, I’m not a big fan of absolute return funds. I think many of them are too risky. If you see that an absolute return fund has, over a one-year time period, delivered a return of 20%-plus, then it’s not really doing its job. These funds are supposed to provide steady returns in a range of different market conditions. If a fund can go up 20% in one year, it can also go down 20% in one year as well.

Now for each hypothetical portfolio, you’ve also come up with some more hands-off options for people who might want to outsource the decision-making on a cautious portfolio. You’ve mentioned that wealth preservation investment trusts are a potential good option. Could you explain why?

Dave Baxter: Yeah, so these are names like RufferInvestmentCompany RICA

and Capital Gearing Ord CGT They do have some equity exposure, I can’t remember the levels off the top of my head, but it’s relatively moderate. They also use things like bonds, kind of some derivative instruments, exposure to gold, that kind of thing, to try and protect you when stock markets fall out a bit.

So, if you’re a pretty cautious investor and you want a bit of growth but you also want to protect what you’ve spent decades building up, then these trusts should hopefully do that job, and give you a bit of a steady option. But it’s really worth examining the different kind of levers that they use.

Some, like Ruffer, are actually a bit more complicated. They use more esoteric things. And the different funds have very different exposures to different sorts of bonds, to gold, and so on.

Kyle Caldwell: Each of those three wealth preservation investment trusts are potentially really good options for a defensively minded investor. However, the thing to bear in mind is that if you dedicate too much of a portfolio to that type of strategy, you’re potentially going to do that at the expense of long-term capital growth.

Dave Baxter: Yes. That’s the big risk that we overlook with cautious investors, that you are being too cautious and you’re, like you say, giving up growth. Also, you just need to remember that inflation is a thing and you need to keep protecting your portfolio against those rising costs.

Kyle Caldwell:Let’s move on to the medium risk/balanced hypothetical portfolio that you came up with. To start, could you talk us through the asset allocation?

Dave Baxter: So often, again, this is very subjective, but the idea of a balanced portfolio has in the past tended to land on this idea of 60/40, which traditionally was 60% in equities, and 40% in bonds. I’ve done a slightly different version of the 60/40 because of those concerns we discussed earlier about bonds and their outlook.

So, we’ve got 60% in equities but 20% in bonds and then we’ve got 20% split between a gold exchange-traded commodity (ETC) and a commodity ETF. So, hopefully, if bonds do have a rougher period, then those other assets will pick up some slack in terms of protecting investors from equity market volatility.

Kyle Caldwell: With the medium-risk portfolio, you went for 15 holdings, and you’ve dedicated 30% to the iShares Core S&P 500 ETF USD Acc GBP CSP1

. Talk us through your thought process.

Dave Baxter: I still, like everyone, slightly fear and respect the world’s biggest market. I don’t want to completely bet against the US, but I’m still going sort of underweight the US with some exposure because, as I mentioned before, lots of markets have done really well beyond the US.

There are still these questions about the outlook for the US now, and, obviously, the current president is causing a lot of headaches for markets. So, I’ve got that US exposure, and I’ve got one other US fund to give a different form of exposure, and then beyond that what I’ve done is taken exposures to the main equity markets.

So, we’ve got the UK, Japan, Asia emerging markets, which are kind of bunched together, and Europe. Rather than just picking, say, a fund for the UK and a fund for Europe, I’m trying to be aware that investment styles can wax and wane. So, of course, as we know, value funds have done pretty well in recent years, but before that, so-called quality and growth funds were doing really well. So, I’ve tried to mix or pair a growth fund with a value fund.

Kyle Caldwell:You’ve got a number of holdings that are a 3% weighting. Do you think that’s sufficiently high enough to do justice in terms of performance?

Dave Baxter: That’s an interesting critique. I mean, you could argue that you might want to be, say, 5% or higher in order to move the dial a bit better. What’s interesting about these pieces is it just really highlights how difficult it can be to build your own portfolio because you’re trying to juggle the different percentages.

I didn’t want to go too wildly underweight the US, but in my quest to do that and have diversification, it means you need to end up with some relatively small fund sizes.

Kyle Caldwell: For me, if you’ve got a holding that’s less than 1%, it’s going to be very, very difficult for that to move the performance dial even if it has spectacular performance. But we are going to come back in a year’s time to review how these portfolios have fared, both on the website and in a podcast episode. So, we will see in a year’s time how much of a difference those 3% weightings have made.

Dave Baxter: Yeah, fingers crossed 3% is the magic number.

Kyle Caldwell: So, for a hands-off investor, which type of funds fit into the category for a balanced investor? The one that springs to mind for me is something like Vanguard LifeStrategy 60% Equity A Acc fund given that it has 60% in shares and 40% in bonds?

Dave Baxter: Yeah. That’s the big beast, isn’t it? It’s a nice no-stress option. It’s very simple. They don’t move those allocations around.

I guess, though, given that I was talking about the question marks around the reliability of bonds, a big criticism of that whole LifeStrategy range is that their only diversifier is bonds.

There are rivals to LifeStrategy, for example BlackRock MyMap and a few others. They do delve a little bit into so-called alternative assets, so they try and diversify a bit differently beyond bonds.

There’s a whole universe out there, but there are also active multi-asset funds, which should try and give you that mix.

Kyle Caldwell: And, of course, at interactive investor we also have our own Managed ISA range.

Let’s now move on to the adventurous portfolio. So, if you’re investing in an adventurous manner, you could in theory have 100% of your portfolio in shares. Is that what you’ve chosen to do?

Dave Baxter: I’ve done 100% in so-called risk assets, but it’s not all shares. Obviously, that’s a very big bit of industry jargon, but it’s 92%, I believe, in equities. Then I’ve chucked the remaining 8% into different forms of private asset exposure.

There’s this argument that listed or public equity markets are shrinking and we’re no longer seeing some of those great growth stories – the most obvious example at the moment being SpaceX – and that they get a lot of their growth before they actually list on to the stock market.

So, I just wanted to spice things up a bit by giving some of that exposure and interestingly, again, it is a dilemma because perhaps some people would argue that an adventurous portfolio now needs to have more in private assets and less than I’ve put into listed.

Kyle Caldwell: And with this adventurous hypothetical portfolio, you’ve once again opted for 15 holdings, and you’ve also again selected iShares Core S&P 500 ETF as the biggest weighting – it accounts for 35% of this portfolio. Could you talk us through the rest of the line-up and how the adventurous portfolio differs from the medium-risk portfolio?

Dave Baxter: Yeah. So, I’ve tried to have a string of continuity between the three funds. In this case, I’ve stuck with the whole S&P as a core and then paired funds with different styles for given regions. To give an example, we have BlackRock European Dynamic A Acc, which is flexible but can be quite quality growthy, with WS Lightman European R Acc – that’s a value fund. So, that’s how it’s similar to the balanced portfolio.

How it’s different is that I have put in a few punchy satellite funds. So, we’ve got Scottish Mortgage Ord SMT

the future trends investment trust. We’ve got AVI Global Trust Ord AGT

which is an interesting one because it’s kind of a value fund, but it also holds things like holding companies and it has a lot in Japan. So, it’s offering you access to growth opportunities that you’re not really getting elsewhere. So, that could have some potential.

And then we’ve gone for some private exposure, as I mentioned. So, we have HarbourVest Global Priv Equity Ord HVPE that’s one of those big, sprawling private equity trusts. It has exposure to so many different funds and hundreds, I think, of underlying companies. So, that’s a well-diversified PE option.

I’ve also gone for quite a fashionable fund at the minute, which is Seraphim Space Investment Trust Ord SSIT

It’s catching that really exciting trend, again predominantly in private assets, and also riding the defence spending trend too.

Kyle Caldwell: And for a more hands-off option, which types of funds would you say fall into the adventurous category?

Dave Baxter: So, you’ve got your simple global trackers, and you can have different mixtures in terms of what exposure you have to the US. LifeStrategy has its own 100% Equity fund and that is much more UK-focused than, say, the MSCI World index.

But don’t forget the active fund because there are some global funds – I mentioned F&C before – which are quite diversified and they can try and act as a one-stop shop.

I would caution that perhaps with some of the really popular names like Scottish Mortgage and Fundsmith Equity I Acc, they can actually be quite focused funds. So, I don’t know if you would necessarily put all your money in those. You probably want to go for a wider spread.

Kyle Caldwell: Yes. Because in the case of something like F&C or Alliance Witan Ord ALW

they own hundreds of companies. That does give you greater levels of diversification, and they are a bit more ‘Steady Eddy’ than, say, a Scottish Mortgage or a Fundsmith Equity, which while they do have more potential to outperform an F&C or an Alliance Witan, at the same time, they are more likely to give you more of a volatile ride at certain points.

Dave Baxter: Yeah. It depends on your belief in those stock pickers, doesn’t it, as well, and how much risk you want to take and how much of a bet you want to take on, say, Terry Smith or the Baillie Gifford team.

Kyle Caldwell: Dave, thank you for running through each of those three hypothetical portfolios. As mentioned earlier on in the podcast, we’ll put links to each of the articles in the episode description. That’s all we have time for today. So, thanks Dave for coming on.

Dave Baxter: Thanks for having me on.

Apr 22, 2026 ETOWL, OPENAI, MSFT, GOOG, GOOGL, ANTHRO, SPACE, GOOG:CA, MSFT:CA, ZGOO:CA, ZMSF:CA, SP500, NDAQ, QQQ, SPY, TSLA

Portfolio Manager, Author, Podcaster Ben Carlson on why markets are fascinating (0:30) Private credit, banking sectors (4:40) Market cycles speeding up (8:00) Economy vs stock market (12:20) Gold and safe havens (22:50) Dividend stocks, yield, income investing and ETFs (24:30) Earnings season: Listen to how CEOs talk about consumers (28:00) AI evolution (31:20)

Transcript

Rena Sherbill: Very happy to welcome to Investing Experts, Mr. Ben Carlson. I’m sure many of you have heard him or heard of him at the very least. You are with Ritholtz Wealth Management. You manage institutions there. You have a very fabulous podcast, the Animal Spirits Podcast. You are an author too.

To wit, we are here today for the most part to talk about your newest book, Risk and Reward: How to handle market volatility and build long-term wealth. Really, really happy to have you on the show. Been listening to you, reading you for a long time. So thanks for coming on the show.

Ben Carlson: Thanks for having me.

Rena Sherbill: Talk to us. I’d be interested to hear first off, if you could share with listeners how you spend your day, how you spend your day looking at the markets, understanding them, how you digest them and then what led you to write this specific book at this specific moment.

Ben Carlson: I start my day reading the horoscope just to make sure I know what’s going on there. Listen to the stars.

Rena Sherbill: Perfect

Ben Carlson: I do a lot of writing and the best way for me to do that is by doing a lot of reading. So I’m doing a lot of reading about what’s going on. I pay attention to a lot of numbers and data.

And I personally think the markets are just fascinating. I know that there’s some people outside of finance who think like this stuff is just it’s boring numbers mumbo jumbo. I think that like the interplay between numbers and feelings and emotions in human psychology.

I think that the markets are just this like giant laboratory for studying human beings. I think it’s like one of the best places to look at the different emotions that human beings have. Fear, greed, panic, euphoria, all these different things that the markets could bring about.

And so I really enjoy just following the market. So that’s why like talking about them. I like writing about them.

Rena Sherbill: Why you called your podcast Animal Spirits, perhaps.

Ben Carlson: Yeah. On a daily basis, that’s a lot of what I’m doing. I’m talking to our financial advisors at my wealth management firm. I’m talking to clients to get a better understanding of what they’re doing.

I’m creating content. And actually, a lot of that stuff, dealing with clients and hearing their concerns and worries and what the problems they’re trying to solve, that’s really good for me in terms of producing content because that’s the stuff that I’m trying to think about.

What are people actually worried about these days? are like regular people outside of finance? What are they worried about?

So I’ve been writing my blog for a little over 10 years now. And the whole point of me writing a blog in the first place, I kind of got into a little trepidation. was right when financial blogs were kind of taking off in like the early 2010s.

So I was reading Josh Brown and Barry Ritholtz, who I’m now working with. They were some of the early blog people. And I just thought that there was a lot of negativity in the world coming out of the great financial crisis. And there was a lot of pessimism and I guess rightly so in a lot of ways because we had two huge stock market crashes and two recessions in the span of 10 years. There was a lost decade for the stock market.

People were really nervous, like, oh my gosh, the financial system almost ended. All these 100-plus-year-old firms went out of business, and the government is backstopping and saving places. I think there was a lot of people who just lacked faith and trust in the financial system. I was getting all these questions from my friends and family about, you’re the finance guy. Explain this to us. What’s going on here? That’s why I started writing my blog.

I’m always kind of glass half full kind of guy. I look for the more optimistic and I look for the good side in most things. And I just thought that there’s a lot of pessimism. That was the idea for the blog.

The book is, I’ve received a lot of pushback over the years. There’s a lot of people who’ve taken on like this whole idea of like long-term investing and thinking and acting for the long term. But I get all these people who look for exceptions. Well, what about this? Well, what do you think about this? Wasn’t this a terrible experience?

And I think for a lot of people, the whole idea of long-term investing is just it doesn’t make sense in this world. And I’m trying to prove that no, even if we open the kimono and show all the bad stuff, right? Like, let’s play devil’s advocate to my own investing philosophy.

I’m to go through point by point and show everything bad that’s happened in last 100 years and why this form of investing still makes sense. And so that was the idea just to, I look at like the risk and reward as like the yin and yang. I say that they’re attached to the hip. That’s what I wanted to show that like, despite all the nasty risks out there, like the reward is still worth it for long-term investors.

Rena Sherbill: We’ve been talking a lot recently on this podcast about the private credit sector and how it’s coming up against the banking sector. And you just talked about the great financial crisis. You talk about it in the book also, a lot of comparisons being made to what’s happening in the private credit sector to the great financial crisis.

We had Samuel Smith on talking last week about how that very much is not the case. He’s a big bullish guy on Blue Owl (OWL) specifically, and he was laying the case for why the banking establishment or banking institutions or those that run banking institutions are so down on the private credit space.

Any thoughts to share about that discussion and also I guess, bear markets and great big bear markets and where bearishness has you most worried?

Ben Carlson: It is interesting that the whole private credit space seems to be an outcropping of the financial crisis, right? A lot of the banks pulled back from that type of lending, so the private managers stepped in, and now they’re doing it.

I think the biggest difference between what happened in 2008 and now is just these loans are long, these loans are not, it’s not like an event, it’s more of a process. Let’s say that the people who are worried about the credit quality of these loans, and I can’t really speak to the credit quality, because that’s just not my expertise.

And these loans are a little harder to understand, right? But let’s say that the credit quality does go bad. It’s not like these things on one day are all going to go under, right? And all these companies are going go bankrupt.

It would be more like a death by a thousand cuts. So that’s where I think the analogy goes. Even if you thought the worst of these investments. I tend to think that these private managers have so much money and they have so much incentive to make sure that this stuff works out.

It’s hard to see this being this sort of car crash scenario. That’s kind of where I fall on it.

Obviously, I think the biggest thing if I’m like tying it back into my book, is that the biggest mismatch we’ve seen and why you’re having all of these people pull money out and look to redeem is like an asset liability mismatch. the whole,

I think my whole point of my book, one of them I hope people get from it is just the fact that when you make an investment, one of the most important things you can do is define your time horizon.

And obviously there were a lot of advisors who put clients into these funds who did not do that because all this money came rushing in and at the first sign of trouble and some bad headlines, all the redemption requests started, right?

And frankly, I think a lot of the advisors should be like kind of ashamed that they did that because these should be five, seven, 10 year holding periods for these types of funds, right? These should not be something you jump into and out of every time you worry, like they’re illiquid for a reason.

And so that asset liability in this match, I think is like the biggest problem with these funds that these are loans are meant to be held, right? They have to kind of mark them to market and provide an NAV and tell clients how they’re doing.

But because of the nature of these funds, they’re private, these are loans that are meant to be held to maturity, right? And I think that’s the thing that people got in trouble to here.

And why there were so many people freaking out is just that they didn’t have that mindset going in.

Rena Sherbill: Because you manage the institutional side at Ritholtz, but I imagine you’re also very much in touch with the retail investing side.

What would you say are the two things I guess you hear or the things that you hear from each of those groups? During this time when there’s a lot of volatility and it’s kind of hard to understand, and also maybe when it’s like very bullish and exuberant.

Ben Carlson: One of the things that I will say in doing this for a couple decades now is that I think just being part of this industry, retail investors used to get a bad rap. mom and pop used to be like this derogatory term, like, the mom and pop investors, they don’t know what they’re doing.

And I think it’s absolutely true that the retail DIY investing crowd has gotten better at what they do. I think that people beating them over the head for the past 20 or 30 years about the don’t run out of the burning building when the stock market goes down.

I think people have gotten better. And you’ve seen that in all the bear markets this decade. When things go haywire, people are buying. The flows show that the money is going in, not out, which is kind of funny because a lot of it means that the professional investors are probably selling. So I do think that retail investors have gotten better.

We have people coming to us who are DIY investors who have been very successful investing their money. They come to us not because they necessarily need help investing money. They need financial planning help. They need help with estate planning, insurance, and taxes, and all these other things.

I think a lot of people have gotten the message that we don’t freak out and panic anymore when this stuff happens. And I think that’s one of the reasons the market didn’t go down more, because I think there’s a lot of people who are beating their head against the wall going, I don’t get this. There’s a war in the Middle East.

Oil prices went crazy. The trade off for moves is closed. Like oil markets are in disarray right now. Supply and demand, it’s all over the place. Why is the market only down? Why did the market only go down like nine percent? I think there’s a lot of people who like rightfully are questioning like this doesn’t make any sense.

I think 20 years ago the stock market maybe would have fallen a lot more. But I think investors have learned and become a condition to not panic as much anymore.

And I guess the second part of your question is, what do I worry about? I guess the one concern there, even though people have gotten better at, people used to say the stock market is the only store that goes on sale and people run out of the door, right? The fact that people don’t do it as much anymore, my biggest concern would be that there is eventually some sort of complacency.

When there is a real risk, a real sort of financial crisis moment, not just a boy who cried wolf thing, are investors too complacent. Do they think that it’s going to snap back right away when in that case where we have like a more prolonged bear market and it’s more painful than people think? That’d be my one concern right now.

Rena Sherbill: So what do you say to that? What do you say to that concern? Is there something that assuages you or is there something that furthers your concern as you look to how investors, because it does very much seem that almost everything is priced into this market. Or even the more volatile, the more priced in it is.

Ben Carlson: I think this is one of the hard parts, too, is that markets are just happening faster and faster than ever. These cycles are speeding up. And I think it’s really hard to wrap your mind around how far like the I think it really started in the pandemic when the stock market kind of looked over this valley of like we shut the economy off.

And I remember when the stock market first started rallying like October or April and May of that year. And everyone said this is a dead cat bounce. There’s no way that that was it.

This thing is not getting better. There was no vaccine yet at this point. was, mean, people were, you know, the economy was still in tatter. People were at home and the stock market kind of looked over this and saw like the trillions of dollars government spending and said, all right, fine, we’re off to the races.

And I think a lot of people were just like in a state of disbelief. And I think that seems to be a lot of the case in a lot of these downturns is like disbelief that it could happen this fast and the market could move so quickly and decide to be more forward looking.

But I think the other side of that could be that we could have, because we have these impulses to move faster, you could see more flash crashes in the market, where you have these huge air pockets where things go down faster.

The COVID one was, I think, the fastest 30 % bear market from all time highs in history. That was a whatever, black swan, one-off event kind of deal. But I think those moves the other way could happen as well.

Rena Sherbill: What are your thoughts about how the economy is moving on its own and then maybe along with the market or how those are influencing each other?

Ben Carlson: I think one of the things I talk about in the book, I did a whole chapter about the stock market versus the economy. And one of the things that I’ve learned is that there are so many people who are smart and well-rounded about what’s going on in the economy.

And basically, none of them can predict what’s going to happen with it. There are more ways to slice and dice economic data than ever before. It’s not just the headline number anymore.

You can get so granular on economic data of this specific, what goes into this number, all the different variables that go up into this number and what groups it’s impacting. And it’s kind of insane how much access to economic data we have now.

And everyone’s still got it wrong in 2022 about like the fact that there’s going to be a recession. And so the way that I look at the economy now, it’s so the US economy is so big and dynamic, it’s I don’t know, 30 plus trillion dollars that it’s kind of like turning a battleship that people think that it’s going to be like a stock market where all of a sudden one day it’s just going to fall.

And I don’t think the economy really works like that. Unless there’s some exogenous event, like a pandemic or some crazy financial crisis, it seems like the economy slows in stages and grows in stages. It doesn’t just happen in one fell swoop. And I think that’s the problem most investors have is they try to equate the economy and the stock market and think all of sudden, OK, here we go.

This one data point shows me that this is happening and there’s just been so many headfakes. If you think about it, the COVID recession was technically one or two months and it wasn’t a real recession because we threw so many trillions of dollars at it. know, people lost their jobs were in some cases paid more to stay home than they were to go to the job.

Small businesses were given loans. Everyone was kind of made whole at that point. So we haven’t had a real recession. And if you can’t be on it, that ended in 2009. That’s like 17 years since we’ve had a real recession, which is kind of amazing coming out of the financial crisis when everyone thought they were going to happen all the time.

So you wonder, are the risks building or is it just that these things are happening so few and far between because government intervention is so much more prevalent than it was in the past.

Apr 23, 2026, 6:00 AM ETConagra Brands, Inc. (CAG) Stock, STWD StockMETA, AMD, AMZN, GLW, IONQ, XOM, CVX, OXY, EQT, VLO, EPD, AMLP, BIZD, USA, OBDC, CRM, OWL, BX, GE, OXY:CA, XOM:CA, ZAMD:CA, ZCRM:CA, ZCVX:CA, ZMET:CA, ZXOM:CA, OXY.WS, META:CA, AMD:CA, IONQ.WS, AMZN:CA, GE:CA, EPDU, CRM:CA, CHEV:CA, BX:CA

David Alton Clark, who runs Retirement Income Warrior, shares how he’s taking advantage of the volatility by taking profits and getting into a dividend name (0:35) Past performance (16:15) Top income pick (23:00)

Transcript

Rena Sherbill: Always happy to welcome back David Alton Clark to the show.

He runs Retirement Income Warrior and recently wrote a book called Commanding Retirement Income. Book week at Investing Experts.

Dave, welcome back to the show. Really happy to have you back on.

David Alton Clark: Thanks, Rena, it’s great to be on.

Rena Sherbill: So here we are basically in the middle of 2026. How has the year gone for you and your service? What’s been going on?

David Alton Clark: It’s been a highly volatile year, volatility also creates opportunity. So if you have the proper planning in place and discipline, you can take advantage of the volatility. It’s been pretty crazy with Trump on again and off again, war with Iran, but we’ve been able to take advantage of that and actually have already gained 93,000 in capital income from selling stocks at their highs.

I just recently took profits in four of the income growth portfolio, Meta (META), (AMD), Amazon (AMZN) and Corning (GLW) were all up 20 to 40 % at their peak just recently. They ran up really quick.

One of my rules is that if you, the faster it goes up, the faster it can come down.

I actually added those at the lows we just had about a month ago between February and March. Those are four stocks I added into the growth portfolio, which is really the portfolio where I harvest the capital gains from there and then redeploy that into the income side of the portfolio.

So that’s really the purpose of that portfolio. And when I have stocks that run up 20 and 40 % AMD was up 40 % in a month. The other three Corning, Meta and Amazon were all up 20 to 25 % just in this last month. So just recently I took profits on all of those. And so that worked out really well.

But I’m not really sure what’s going on right at this exact moment. I’m kind of holding steady and telling everyone to strap themselves in because who knows what’s gonna happen over the next day or so.

Right now, I haven’t allocated all of that money. I still have a lot of dry powder. I think at the time before I took profits in those, I was 72 % allocated and now I’m down to 58%. So I have a large amount of dry powder ready to go right now.

I did buy one thing, Conagra (CAG), which is kind of a point of max pessimism buy, they’ve paid a dividend and never missed it since 1976. It’s $1.40 and their stock has dropped significantly down over the last year to where it’s about $14 now, I think. So the dividend yield has gone up to 9%.

So it’s one of those dividend capture deals where the stock has gone down so much that the dividends rose risen high, higher than it normally should be. So I locked in a position on that, just a half a position right now. Four percent is a full position for me.

I bought a two percent initial position and I’ve got two percent back up in case it goes down more. If it starts to run away, I’ll lock in the rest of that.

But locking in that nine percent gain on a company like ConAgra that’s faithfully paid the dividends since 1976. And then they just had earnings and every one of the management team was, you know, stated that they’re dedicated to paying the dividend and they’re not thinking about a cut or anything like that.

And they actually still have about 75 % payout ratio. So they have coverage on it. So they’ve still got a little bit of cushion there. And as of their last earnings report, things are looking like they’re take the strategies they’ve implemented to make a comeback seem like they’re taking hold.

So I took a shot on that one. That’s a little bit of a higher risk one, but it’s a nice dividend to collect on that.

Rena Sherbill: Do you want to get into more detail if you would about what are the strategies that they’ve been implementing that seem to be righting the ship and also why is it a higher risk play?

David Alton Clark: Well, the strategies they’re implementing, they’re in the food business and that’s kind of shifted a little bit lately with the GLP-1 meds and things like that. People are eating differently in the different categories. So they’ve really taken a look at that and changed up their category, their food offerings in the different categories to where they include that.

And they’ve done some work on the back end as far as the cost of creating all the different foods that they make. So that’s really what they’ve done, cost reduction and avoidance.

And they’ve also expanded their different offerings to take into consideration some of the changing dietary likings of the general public right now. So they’ve kind of shifted away from some of the more high fat sugary foods to more healthy foods and things like that.

It seems to be working, they’re up like 2 % across the board on all of those things.

And you asked what makes it risky? What makes it risky is that, you know, they do have 75 % payout ratio.

The yield is 9%. They are really down at the bottom. Technically, this is what I call a point of max pessimism buy. So they have bounced slightly off the bottom of the downtrend channel.

This is from a technical perspective, which creates some of the risks. They are in a solid downtrend channel for probably the last year, but the stock just recently bounced off the very bottom of that channel and popped up a little bit.

It hasn’t made a total complete trend reversal yet. And that’s really, if that occurred, I would say it was less risky, but I wanted to take advantage of getting that 9 % yield.

So I went ahead and bought it when it just barely moved off the bottom of the downtrend channel. Right now it’s still, the momentum is against it as far as there could be further down draft selling, but I decide that’s why I kept 2 % in reserve to take another shot at it, fire another bullet at it if it does go lower.

But that’s why it’s still risky. And plus the food business, there’s a lot of competition. They’re doing really well, but there’s a generic brands now. There’s just the food, grocery businesses is super hyper competitive.

Rena Sherbill: And conversely, what would you say about the four names that you took profits on?

I know that you said that they had a price run up. What other factors played into that decision or to those decisions?

David Alton Clark: I’m glad you asked that question because what I told my members is that this wasn’t a selling of these stocks based on the long-term growth story changing.

I still believe in all four of the stocks that I sold in the long-term, but the issue is that when I’ve seen this too many times before in my history where if something runs up 40 % in less than a month and then the rest of them like 20 to 25 % in less than a month, it’s very easy to see those. It’s kind of like hot money in a way.

And you can see those gains evaporate quickly on headlines, of macro headlines, like the whole problem with the Iran war and Trump. If Trump and Iran or the US and Iran don’t make a deal by tomorrow and we start bombing Iran again, I’m thinking the market’s probably gonna drop again and maybe I’ll get another chance to get back into those at a lower point.

But also they’re in the portfolio, the growth portfolio, which I call the income garden. anytime one of those, I have a moonshot portfolio also for growth and those are ones where I don’t take profits on those like (IONQ) is in my moonshot portfolio and it was up 60 % just last week.

But I didn’t sell that one because I’m expecting that one to be a multi-bagger maybe 10 times higher or whatever a few years out from now. So that’s one where I don’t touch those but ones in the income garden growth portfolio when they eclipse the 20 % mark that’s when I review the situation and say, okay, what am I going to do here?

And then each one of those ran up so fast. We had a V-shaped recovery. The stock market went down by about 20 % or whatever on all of these stocks were trading 20 % off their highs or more.

The stock market in the beginning of April just shot right back up to where it was before. And so when I looked at all of those, I decided I’m going to go ahead and take profits on those.

Then I’m sure with all the volatility we have. then another factor that came into the fore was that we’re in a midterm year and that’s coming up pretty soon. And usually that brings on a whole other layer of uncertainty and volatility because of all the political headlines and back and forth and you don’t know who’s going to win and will the policies change. And so I’m expecting another series of volatility and downturn as far as that goes.

But those are ones that I would still join back into. It wasn’t because I thought that they actually, you know, their long-term growth story changed. And I also, that was just recently earlier in the year, I was, I think last time we talked, I told you that I loaded up on energy stocks because I felt like energy was gonna be big this year.

I had no idea that this is what was gonna cause it, but it was really such a there was such a negative narrative on energy coming into the year.

And as we’ve discussed many times before when we talk about ExxonMobil (XOM), the thing is the seeds of the coming boom are sown during the current bust is my statement on that and it’s cyclical oil.

So I bought into a lot of oil stocks. I had Chevron (CVX), (OXY), (EQT), Valero (VLO), (EPD), in each of the different categories of oil and gas. And when the war kicked off, all of those spiked up huge.

That’s what created a lot of the profits at the beginning of the year because I sold out of those earlier too.

I still have some oil exposure in ETFs like (AMLP), but it’s much reduced right now.

Rena Sherbill: To the point of how the market has been moving and it’s hard to assess, even though you’ve talked before about what your strategy is and to your point, sometimes the strategy pays off in ways that you couldn’t even predict.

But has there been anything about the this evolving market and the evolution of investing in general that has caused you to rethink or tweak anything in your strategies?

David Alton Clark: That’s another great question, Rena, to think about.

Maybe tweaking some because we are in a highly volatile market right now. And so for the last 10 years from the great financial crisis of in 2008 to 2009, all the way to 2020.

It was really easy to make money. mean, there was zero interest rate, you know, remember the ZIRP policy. And I made a lot of money during that time, but I think a lot of other people did too. It was pretty simple.

You really knew what the Fed’s policy was going to be. And anytime there was a pullback, it was by the dip and you were going to, you’re going to be a winner. So I think a lot of people were a little overconfident at that point in time thinking, man, I’m a stock market genius.

And I’m not saying they weren’t, but I’m saying it was a little bit easier to make money then. Once the pandemic hit and then we just had a series of huge macro issues that you’ve had to be able to navigate. Luckily, I learned a lot.

Previously, my experience goes all the way back to the dot com boom bust. And then, you know, I was actually out in Silicon Valley at that time. And so I was like, I feel I call I give it like I had the Icarus type experience. I was flying really close to the flame, to the sun of that. And so I learned a lot from that as far as navigating these these big macro issues.

And then the same thing with the 2008 House of Cards falling. I was actually in real estate at that time. And so I was lucky to be right there. So I think the strategy’s changed from the last 10 years, which has been pretty simple that there are going to be zero interest rates to now. It’s a little bit more, I’m a little more active than I used to be as far as these buys and sells. I usually, I would be holding them for longer.

(AMD) during that time, I bought AMD, I think back at like for $3 and something in 2011 or something like that. And then I let it ride all the way up to 140. It was like a huge winner for me. But now I’ve changed my strategy with so much volatility and I’m getting older now. And so I’m really more about harvesting income, harvesting the growth capital appreciation and redeploying it.

So that’s really what’s changed. But recently, I would say that I’m a little more focused on taking profits when I need to. And also, I’ve shrunken down my shot group. That’s one of my rules during volatility. I’m glad I finally thought of that when I was rambling on.

But in times like this, I think it’s important. It’s good to be diversified. But when things are so volatile like this, you really need to take a look at your holdings and maybe trim away the ones you’re not so convicted in and focus in more on the ones that you have more conviction in and a higher, you feel like they’re going to do better.

Right now I’ve got 22 total holdings across the portfolio when normally I might have more like 30 or something like that. So I’ve kind of trimmed them up and tightened into just my highest conviction names.

Rena Sherbill: I know people love to hear about the returns. Would you be willing to discuss some of the returns that you’ve had at Retirement Income Warrior? General performance.

David Alton Clark: As of right now, we’ve got a total return of 101 % right now since we started the service in June of 2022, which equates to about 26% total return per year. That is built on we’ve had 502,000 in income coming from distributions, dividends, and interest.

And then 479,000 has come from the harvesting of capital depreciation sold securities. Over this last, and not everything is a winner. So we have a 51% capital gains level right now since inception.

But just for 2026, I’ve got my list of all the stocks I sold. And so I’ve taken profits on some Amazon (AMZN) took profits. It was up 23%. Corning (GLW) was up 22%. AMD was up 40%. Meta (META) was up 23%.

Now, one other thing we haven’t talked about yet is the narrative on BDCs and private credit. That’s been a big issue lately and I had a couple of names that were involved with that. (BIZD), (USA), (OBDC), I actually took losses on those.

BIZD, I sold out of that one at 19%. It was a $12,000 loss, which you can use for tax loss harvesting against your gains. So it’s kind of a tax loss harvesting thing. But also on that one, I’d collected like $30,000 worth of distributions already. It was something I’d held for a long time.

So all of the ones that I sold in the income side, I took these losses of 6,000, 12,000 on OBDC, but I had huge income from those and I didn’t want to see that completely evaporate. And those are ones where I felt that that narrative had shifted. still, I still felt great about those companies. They were best in class.

But sometimes even if you feel that way yourself, if the narrative is so pervasive, you might wanna say, hey, let me just cut out of these, use it as tax loss harvesting and come back and take another look at them once this is over. So those were some of the losers. Those were the three or four, the four that were down for me were.

BIZD, USA, OBDC and I actually sold out of Salesforce (CRM) too. When I bought into that, how it’s been AI versus the software companies and Salesforce (CRM) was just beaten down.

I think it was down like 50 % or something like that. So I kind of took a flyer, a point of max pessimism buy on that at one point. But once it hit, when I buy something like that, I watch it at every percentage.

When it’s down 10, if it’s down 10 % or up 10%, I double check it. Same thing every 10%, 20%, whatever. And so it was down 10 % from the time. And I only started with a half a position and it was down 10 % and then I just reevaluated it.

And I thought, maybe I entered in a little too quick. So I went ahead and sold out of that one too.

But overall, we’re up 10 % in capital appreciation for this year, 93,000 total, including all the gains and losses.

Rena Sherbill: We had Samuel Smith on from High Yield Investor last week talking about providing some context about the private credit sector and his pick has been Blue Owl Capital (OWL), not necessarily for this year specifically, but his pick at the beginning of this year.

He was saying that the fears about that space, kind of what you were saying are overblown. Anything else that you would add to that conversation about the private credit space?

David Alton Clark: I think he’s right. Yeah, he’s right on that. And the Blue Owl Capital, it’s really, it’s really those people get confused between the public companies and private companies.

Blue Owl Capital’s issues are with their private credit where they’re there, the people are asking for to get their money out. And they have a rule where you can only get 5 % out a month. But I think Blue Owl actually said, okay, and they sold off some assets and gave people back like 40 % for what they’re asking for.

And if you really look at it, I’d have to check it again, but I was, I did check that out back in the day when Blue Owl was really in the headlines. And I think that was really their one fund that was being, people wanted to get their money back out of was only 2 % of their total earnings or their total assets under management.

So it really was kind of a misnomer to think that the blue owl was going to have trouble. There are some great ones out there.

If I was going to go back in, I’d probably go in with something like Blackstone (BX), I think is on top of that. And they had a lot of redemptions that people were asking them for redemptions.

But I think it’s more of a situation where the investors in those didn’t really understand the rules that those are hard assets and they’re not liquid. And so it’s not like you can just go in there and say, hey, I want my money out of there. Well, they have to sell something.

They got to sell some condominiums or sell an apartment complex or something to get the funds out of those types of entities. I really think it’s just everything’s coming back now too. And so I think it was just, I don’t think it’s gonna be the same thing as like the great financial crisis.

What I told my people was it reminds me of the, we had, remember we had the issue with the regional banks a while back when one went bankrupt in California and then one went bankrupt in New York and then people were like, my God, know, the regional banks are going under and the whole regional bank sector just took a dive bomb.

I feel it’s kind of a replay of that where there was a few issues, people wanting redemptions from Blackstone and Blue Owl, and then it’s kind of blown up into something bigger than it really is. So I think it’s gonna be fine. And I do still have some income stocks that are, know, adjacently related to that. And they’ve all made pretty big comebacks that were down before bigger.

But now they’ve all come back to less than down 10%.

Rena Sherbill: Do you want to say some of those names?

David Alton Clark: This is something I’m getting ready to write an article on, but I’ll give you my top income pick that I feel is the best of the breed in the higher yield sector. It’s Starwood Properties. It’s an mREIT. Barry Sternlich runs it. I’ve owned this forever and it has right now, it has a 10.47 % yield. It’s trading, I think, I didn’t look just today, but around 18, but it’s actually highly diversified. And it was down along with all the other stocks that are kind of involved in the real estate sector and the private equity.

But Barry Sternlich, I’ve been around a long time, I’m gonna kind of date myself here, back in the day when the credit, I don’t know if you remember the credit union crash or whatever of 1982, when the credit unions like went, were you? But in 1982 was really the first commercial real estate, just debacle from the credit unions were justgiving away money and not doing enough risk assessment or whatever and the whole thing came crashing down and they created something called the Resolution Trust Corporation where the government, all these commercial real estate buildings all were bankrupt and so they had to create a government entity to sell those for pennies on the dollar.

And I really remember because I was in college and I was dating a lady that was actually working for Ernst & Young and she was working with the Resolution Trust Corporation and she was telling me all about it and how all these big buildings on the Riverwalk in San Antonio were selling for pennies on the dollar and she kind of explained the whole thing to me. I was like, wow.

But Barry Sternlich was, that’s when he started his own company. He was working for another real estate developer, but he went out on his own at that point in time and bought up some of those buildings for pennies on the dollar. And then later after that, he started Starwood Properties and started paying a dividend. And one really great fact about his company is that it’s the only MREIT in history that has never cut the dividend.

So that’s really important. And he had to go through the 2000.com debacle, didn’t cut the dividend. He went through the great financial crisis, didn’t cut the dividend. And he is just over and over stresses the fact that you can count on that. Now he hasn’t grown it. It’s 48 cents a quarter.

And he’s not growing the dividend, but you can count on that 48 cents. And it’s 10 % yield right now. And it’s highly diversified. Got a great balance sheet. That dividend right now actually isn’t covered by income coming in, but he’s got so much money and so much diversification that it’s not a problem for them to cover the dividend.

The whole situation is looking up for them right now. So Starwood Properties (STWD) is my top pick for that. And I’m getting ready to do an article on Seeking Alpha about it shortly.

Rena Sherbill: What would you say has enabled them to not cut the dividend? Is it the fact that they haven’t grown it? Or what else would you attribute that to?

And what would you say are, if any, what concerns you have about Starwood?

David Alton Clark: Sometimes diversification of income streams can also, it can be a big positive, but it can also turn into a negative. So they’re not your standard mREIT, getting income from just one source. They’ve got, he’s expanded. Has several different vehicles that he can get income from.

I’m not concerned about him cutting the dividend because I think they got one or two billion in cash and cash equivalents that he could always use to pay the dividend.

Plus, he’s got a massive credit line. So there’s no issue with liquidity with Starwood. So the dividends may not be covered by the quarterly income that they have coming in, which is probably almost covering it, but it’s not 100%. But that small percentage or whatever that is missed by, he’s been going for, like I said, since 1982.

So he’s got billions of dollars and huge credit lines. And so that’s why I’m not worried about the dividend. The risks are that he is, he does have one of the non risks is that he’s not highly focused in on like apartment complexes and office, which is the office space, office buildings are kind of under attack right now because everyone thinks that AI is going to delete those people’s jobs that go to a building and sit in there in front of their computer in their cubicles.

And so a lot of people are really worried about office buildings right now. And so he’s really stayed away from that. It’s a very small percentage of the portfolio, I think less than 10%. And so he’s done a good job of focusing in on that, but also, he has a lot of different diversified areas of income, which can also be an issue at times where something seems to fall apart.

It’s kind of like the conglomerate thing, like what happened to (GE) when they were a big conglomerate and they had all these different branches and companies and it just like one was up, it was like whatever one would be up, the other would be down and you never could make it go.

That’s one of the risks with Starwood too, but he’s been handling that pretty well also. That’s one of the risks. It could be a whack-a-mole situation, but I don’t really think so. GE was definitely whack-a-mole.

Rena Sherbill: Any other whack-a-moles in the income investing space or the opposite of a mole? Any, what else are you looking at in the income space? Bonds, anything to say there?

David Alton Clark: One thing about the bonds we talked about last time. So I do have, you know, as far as income goes, I like to have some diversification in the different vehicles. And one of them is for actually for bonds, I’m not really a bond expert. So I like to outsource that to the specialists. And so I have investment in the bearings global short duration.

high yield fund and it’s a closed in fund and it yields about 10%. And the thing I like about that is that it’s got high current income while it preserves capital because it’s only short duration, less than three years, which reduces the interest rate risk. So that’s how they stay short and it’s spread out across

different geographies, US, Europe. And so that’s really where I’ve got the bonds concentrated. One thing that I wanted to say that I’m glad you brought that up is I’ve decided that I’m no longer going to invest in MLPs that create a K1. It’s actually a partnership. And I know that Samuel Smith, he invests a lot in the MLPs.

Considering it I’m going to invest in I’ve got (AMLP) which is an ETF which has a bunch of MLPs within its portfolio but there’s no k1 Tax form that you have to fill out. It’s not a partnership so you can gain exposure to MLPs by using a MLP which is one of my holdings and then skip the whole tax burden also, you can’t really hold an MLP and an IRA account.

And so just for myself, I was investing in those because I am an oil man from Texas. But finally, this last year, I decided that I sold off the MLPs that I had for the service and in my own private portfolio.

And I told my members, I said, we’re going to invest in AMLP and also maybe a pipeline company, some of them have shifted over to where they do 1099. And so MLPs are great. You get a bigger return on your capital, but it comes with a lot of red tape. And then also you can’t own them forever because it’s a partnership. they consider the distribution they give to you a return of capital.

And so at one point in time, if it’s yielding 10 % within 10 years, you should have gained back all of the money that you put towards it. And then you might start getting taxed regular income as taxed on those distributions as regular income. So it’s just a big hassle with the taxes and everything else. You might as well just own AMLP. So that’s one piece of advice that I’ve given my members recently, as far as the high yield stuff.

Rena Sherbill: I mentioned at the beginning that you recently wrote a book called Commanding Retirement Income, a disciplined framework for retirement income generation, wealth creation and capital preservation.

Short answer: GCP = safer, lower‑volatility, UK‑infrastructure‑heavy, lower growth.

SEQI = broader global infra debt, higher diversification, slightly higher risk, historically stronger total return. Both yield ~8–9%, but they behave differently.

Both are London‑listed infrastructure debt investment trusts, but their mandates diverge:

| Metric | GCP | SEQI |

|---|---|---|

| Price | 75.20p | 80.90p |

| Dividend yield | 9.33% | 8.47% |

| P/E | 34.65 | 15.74 |

| Market cap | £618m | £1.19bn |

| 52‑week range | 68.14p–80.50p | 74.10p–84.70p |

Interpretation:

| Investor priority | Better fit |

|---|---|

| Maximum stability / UK‑linked cashflows | GCP |

| Diversification across global infra debt | SEQI |

| Higher long‑term total return potential | SEQI |

| Highest current yield | GCP |

| Lower political/regulatory concentration risk | SEQI |

| Lower credit risk | GCP |

The biggest hidden difference is duration vs credit spread:

So even though both “look like infra debt trusts,” they respond to completely different macro forces.

If you want diversified infra credit with better long‑term return dynamics, SEQI is usually the stronger pick.

If you want UK‑centric, government‑linked, high‑yield stability, GCP is the cleaner, lower‑beta choice.

Maybe the best plan will be to split the investment between both Trusts.

I’ve sold TFIF, including the earned dividend and all charges for a loss of £45 as there may be better Trusts to invest then.

This is a non-independent marketing communication commissioned by Columbia Threadneedle Investments. The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

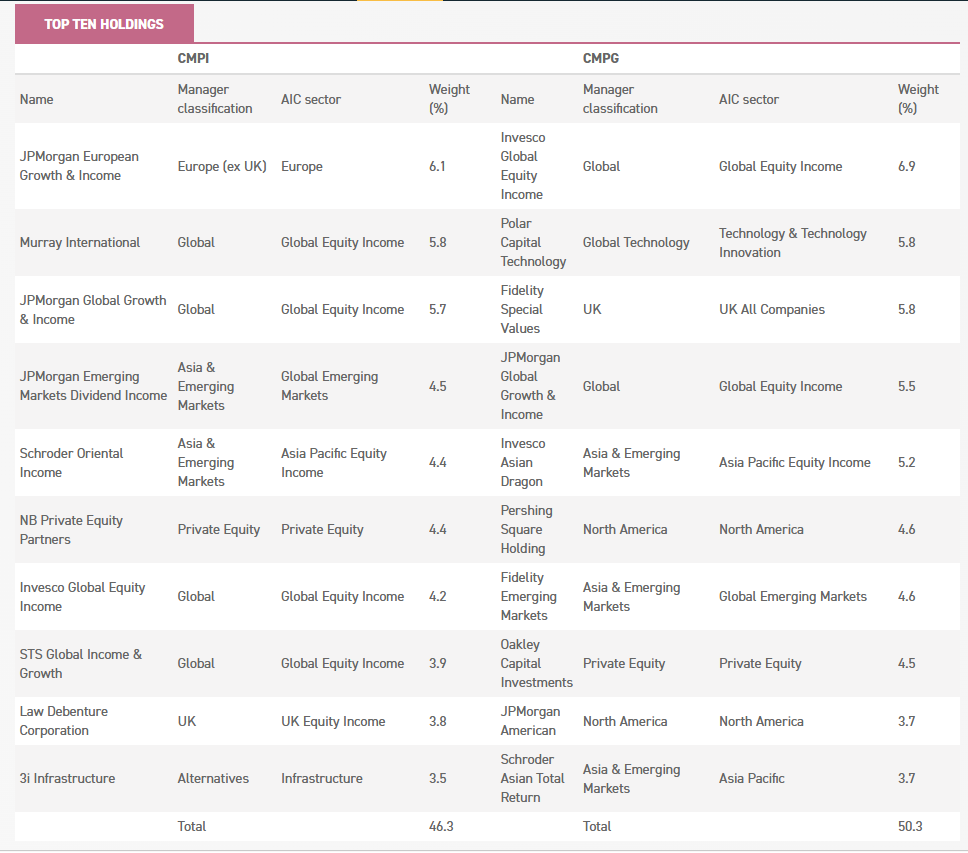

Portfolio

CT Global Managed Portfolio aims to provide investors with a long-term savings vehicle consisting of two share classes: CMPI, which aims to deliver a growing income alongside capital appreciation, and CMPG, which focusses solely on maximising capital growth. Once a year, shareholders have the option to switch between share classes at net asset value without incurring UK capital gains tax. This enables those not investing through a tax-exempt account to adjust their investments over time in line with their needs without triggering a tax liability.

Both portfolios consist exclusively of investment companies, which managers Adam Norris and Paul Green regard as best-in-class and select on a bottom-up basis. That said, they also incorporate macroeconomic views into their investment process to identify both strategic and tactical opportunities. For this purpose, they can leverage Columbia Threadneedle’s significant in-house resources, benefitting from input provided by the multi-asset team.

Adam and Paul have been increasing their exposure to risk assets in recent months. They are constructive on the outlook for corporate earnings growth, and while they remain mindful of potential headwinds, such as higher oil prices driven by ongoing geopolitical tensions in the Middle East and possible changes in trade tariff rates, they highlight supportive policy measures across several regions, including the ‘One Big Beautiful Bill’ in the US, alongside stimulus packages in Germany and Japan, as well as likely steps to bolster economic growth in China.

One area they have added to across both share classes is Asia and emerging markets, where they see attractive valuations, strong earnings growth potential, and a weakening US dollar as tailwinds. Since our previous update (published on 14/10/2025), they have topped up their positions in Fidelity Emerging Markets (FEML) and Mobius Investment Trust (MMIT), both held within the CMPG portfolio. They have also introduced Invesco Asia Dragon (IAD) into both portfolios, highlighting its style-agnostic approach. Its managers, Fiona Yang and Ian Hargreaves, invest in companies they view as undervalued relative to fundamentals or where they believe the market underestimates earnings growth potential. In addition, IAD funds its dividend from both capital reserves and income generated by its portfolio companies, targeting a payout of 4% of NAV per year. This gives the trust the flexibility to invest in companies offering low or no dividend yield but stronger long-term growth potential, while still being able to deliver an attractive income, making it compatible with CMPI’s mandate.

In fact, Adam and Paul favour this approach over traditional equity income strategies that pay a natural dividend, as they believe such strategies are typically constrained to a narrow pool of income-generating stocks, many of which they consider ‘value traps’ (i.e. stocks offering high dividend yields but limited total return potential). Consistent with this view, they have also initiated a position in Invesco Global Equity Income (IGET), a global equity income strategy targeting a dividend equivalent to 4% of NAV at the end of its previous financial year, using the same mechanism. At the end of February 2026, IGET was a top-ten holding across both CMPI and CMPG portfolios, as the table below shows.

Source: CTI, as at 28/02/2026

Conversely, Adam and Paul have continued to reduce exposure to UK equities. While these trade at a discount to their peers in other developed markets on aggregate, the managers view this as a reflection of their low growth potential and do not believe that valuations alone provide a sufficient catalyst for performance. Since their appointment, they have divested from Finsbury Growth & Income (FGT), Lowland Investment Company (LWI), Baillie Gifford UK Growth (BGUK), Law Debenture (LWDB) and Diverse Income Trust (DIVI) in the CMPG portfolio. Within CMPI, they have exited DIVI and Henderson High Income (HHI), but have retained LWI and LWDB, viewing the income stock-picking skills of James Henderson and Laura Foll — the managers of both trusts — as strong and well suited to CMPI’s mandate. While they are not seeing a broad-based recovery in UK small caps at this juncture, Adam and Paul believe there are still pockets of value within this space. To exploit these, they have introduced Odyssean Investment Trust (OIT) and Strategic Equity Capital (SEC) into the CMPG portfolio. Both strategies take sizeable positions in a limited number of stocks (fewer than 20 holdings), resulting in highly concentrated portfolios, and engage intensively with investee companies to drive improvement and unlock value.

The allocation to private equity has also been reduced since our previous update, although this was due to idiosyncratic reasons rather than a view on the asset class. For instance, Adam and Paul have trimmed their holdings in HgCapital Trust (HGT), a private equity strategy focussing on software and tech-enabled services companies, as they assessed that the type of businesses it invests in may face disruption from artificial intelligence. This concern has since materialised, with software-related businesses having experienced a sell-off in early 2026. Adam and Paul took advantage of the subsequent rebound to further trim their holdings in HGT. As a result of geopolitical uncertainty and its potential impact on the private equity market, they have not recycled the proceeds into this asset class. That said, they had added to their holdings in Schiehallion (MNTN), a late-stage private equity strategy held in the CMPG portfolio, last year. This reflects their view that clear winners are emerging within the portfolio, including SpaceX, an aerospace and space transportation company, and Bending Spoons, a company specialising in acquiring, managing, and revitalising digital apps and software businesses.

Adam and Paul have also exited multi-asset strategies such as Personal Assets Trust (PNL) and BH Macro (BHMG) in the CMPG portfolio, leading to a reduced allocation to the ‘alternatives’ category, as they are currently favouring exposure to risk assets. That said, they remain constructive on infrastructure, which also falls within the alternatives category. Since their appointment, they have introduced Cordiant Digital Infrastructure (CORD) into CMPI’s portfolio and Pantheon Infrastructure (PINT) into both portfolios. We discussed the investment theses for both CORD and PINT in our previous note.

Source: CTI

Overall, the number of holdings has been reduced in both portfolios since Adam and Paul’s appointment, reflecting their plan to adopt a higher-conviction approach. For instance, the number of holdings in the CMPG portfolio has been cut from 39 to 30 (as of 31/12/2025). Similarly, the number of holdings in the CMPI portfolio has been reduced from 38 to 30 over the same period. As a result, concentration in the top-ten holdings has also increased across both portfolios. Concentration in the top ten holdings has also increased across both portfolios. For example, while CMPG’s top-ten holdings accounted for c. 36% at the end of May 2025, this had risen to c. 50% by the end of February 2026. In the CMPI portfolio, the weight of the top-ten holdings increased from c. 42% to c. 46% over the same period.

The CMPI Snowball is different to the SNOWBALL as it invests more for the chance of capital gains but as you wait it pays a yield around 6%.

The SNOWBALL invests for higher yields and uses those higher yields to buy more shares that pay a higher yield, until you want to use those dividends to pay your bills.

This is a non-independent marketing communication commissioned by Columbia Threadneedle Investments. The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

Increased geographical diversification and a punchier approach make CMPI/CMPG a new proposition.

Overview

The managers of CT Global Managed Portfolio (CMPI/CMPG), Adam Norris and Paul Green, have significantly increased the concentration and global diversification across both Portfolios of investment companies since taking over in June 2025, seeking to create leaner portfolios with punchier performance potential. By the end of last year, the number of holdings in both the growth and income share classes decreased to 30 from 39 and 38.

In recent months, the managers have increased exposure to equities. Although mindful of potential headwinds such as higher oil prices due to ongoing tensions in the Middle East, Adam and Paul are constructive on the outlook for corporate earnings. They highlight supportive policy measures across several regions, including the ‘One Big Beautiful Bill’ in the US, the stimulus package in Germany, and likely steps in China to bolster economic growth.

Asia and emerging market equities are one area where Adam and Paul have notably been adding, given tailwinds such as attractive valuations, strong earnings growth potential, and a weakening US dollar. This includes, for example, the introduction of Invesco Asia Dragon (IAD) into both the CMPI and CMPG portfolios. They have also initiated a new position in Invesco Global Equity Income (IGET) in both portfolios, further contributing to global diversification.

Conversely, they have reduced exposure to UK equities. While these trade at a discount to peers in other developed markets, they believe this reflects their lower growth potential. The allocation to private equity has also been reduced, notably in CMPG’s portfolio. This was, however, driven by idiosyncratic reasons, as Adam and Paul have trimmed their position in HgCapital Trust (HGT), a private equity strategy focussing on software and tech-enabled services companies, amid concerns that these types of businesses may be disrupted by artificial intelligence.

Analyst’s View

In our previous note, we highlighted Adam and Paul’s plans to increase global diversification and build higher-conviction portfolios as exciting developments, and we note that significant progress has been made towards this commitment. While we believe it is too early to assess the effectiveness of these changes on Performance, we continue to think they could lead to stronger returns over time, as both share classes should be able to benefit from a broader opportunity set through selectively curated investment companies.

In addition, we believe that both CMPG and CMPI offer exposure to attractive growth themes, including technology and emerging-market equities. In particular, we view the managers’ decision to continue adding to emerging markets as promising, given their attractive valuations and earnings growth potential. We also believe that both portfolios are well positioned to benefit from a potential recovery in alternative assets, with several investment companies specialising in these areas trading at wide Discounts.

Finally, we believe that CMPI could be particularly attractive to income-focussed investors, offering a Dividend yield of c. 6.1%. This compares favourably with many equity indices and equity income-focussed investment companies. It is also higher than the yields available on long-dated gilts, such as 10- and 20-year gilts, while offering greater potential for capital appreciation than fixed-income instruments. That said, we note that CMPI is currently trading at a premium of c. 3%, which could amplify losses should this narrow.

The UK government has unveiled a broad package of energy reforms aimed at reducing the influence of volatile gas prices on electricity bills, alongside fresh support for clean power, grid investment and electrification. The measures come as renewed geopolitical tensions and disruption in the Middle East have once again exposed the UK’s reliance on international fossil fuel markets.

At the centre of the package are the government’s plans to “break the link” between gas and electricity prices by expanding the use of long-term fixed-price contracts for renewable generators and increasing the windfall tax on electricity producers benefiting from higher wholesale prices.

The most significant structural change is a proposal to offer voluntary long-term fixed-price contracts to existing low-carbon generators that are not already covered by subsidy schemes such as Contracts for Difference (CfDs). According to the government, these assets account for roughly a third of Britain’s power supply.

The aim is to shield households and businesses from spikes in wholesale electricity prices, which are often set by gas-fired peaking plant, even when cheaper renewables and nuclear supply much of the system.

The government says that Britain has already reduced the frequency with which gas sets the power price from around 90% of the time in the early 2020s to around 60% today, and this should fall further as more renewable capacity is built and comes online.